Russia controls ~17% of Nickel’s total supply & obviously with that amount of supply going out of system, one would assume prices to rise

But someone expected prices to fall!

A🧵on how the 2.3x surge in Nickel prices was triggered by a short trade & not due to supply crunch

But someone expected prices to fall!

A🧵on how the 2.3x surge in Nickel prices was triggered by a short trade & not due to supply crunch

What happened exactly?

A Chinese tycoon "Xiang Guangda" who owns the Tsingshan Group, the largest nickel mining group in China had placed huge short bets on London Metal Exchange (LME), expecting the nickel prices would fall.

We wonder why he held that view👀

1/n

A Chinese tycoon "Xiang Guangda" who owns the Tsingshan Group, the largest nickel mining group in China had placed huge short bets on London Metal Exchange (LME), expecting the nickel prices would fall.

We wonder why he held that view👀

1/n

This bet went horribly wrong when Russia banned commodity exports & Nickel prices started surging

To cover a big short position, someone had to buy equivalent long positions.

This created a short squeeze & Nickel reached $1lakh/ton & inturn led to notional loss of $8 Bn+!😱

2/n

To cover a big short position, someone had to buy equivalent long positions.

This created a short squeeze & Nickel reached $1lakh/ton & inturn led to notional loss of $8 Bn+!😱

2/n

If you owe the brokers $8Mn that's ur problem. If you owe the brokers $8Bn, that's Broker's/exchange's problem!

Given the high leverage, this could blow up counterparty bankers' & brokers' accounts, taking exchange down with it.

So, ofcourse damage control had to be done

3/n

Given the high leverage, this could blow up counterparty bankers' & brokers' accounts, taking exchange down with it.

So, ofcourse damage control had to be done

3/n

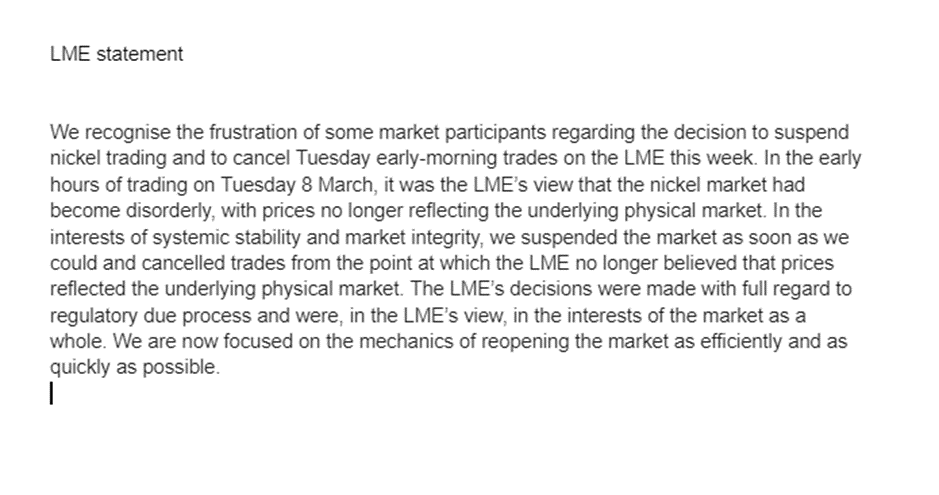

So, the brokers & exchange played dirty. (JP Morgan & China Construction Bank). The London Metal exchange decided to intervene to prevent a blowup

They rolled back all contracts & cancelled trades worth $4BN to bring the price down before closing further trades in Nickel.

4/n

They rolled back all contracts & cancelled trades worth $4BN to bring the price down before closing further trades in Nickel.

4/n

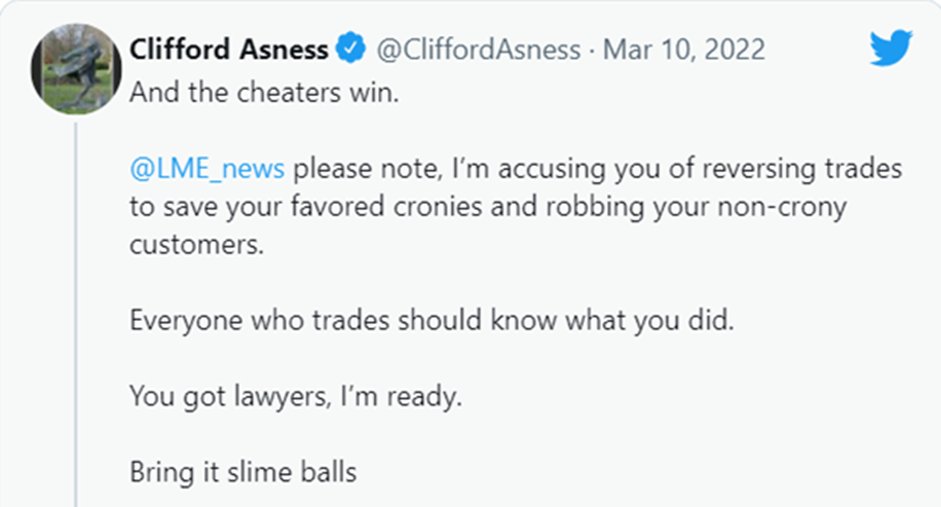

This has offended many multi-billion Hedge Fund managers such as Clifford Asness who were denied of big gains from the short squeeze.

5/n

5/n

LME did wrong & the implications: Loss of trust

This Nickel debacle shouldn't have happened.

Allowing counterparty to build a 190,000 short position in most volatile & one of least liquid metals without anticipating risk to market orderliness was neglect of responsibility

6/n

This Nickel debacle shouldn't have happened.

Allowing counterparty to build a 190,000 short position in most volatile & one of least liquid metals without anticipating risk to market orderliness was neglect of responsibility

6/n

Worse was the decision to cancel Nickel trades between willing buyers and sellers. That’s the boundary an exchange should not cross..

/The End

/The End

Loading suggestions...