Piramal Enterprises Ltd is undertaking a demerger.

Is there value in the stock?

A thread🧵explaining both the Financial Services and the Pharma business

Hit "Retweet" to educate maximum retail investors

Lets go👇

(1/20)

Is there value in the stock?

A thread🧵explaining both the Financial Services and the Pharma business

Hit "Retweet" to educate maximum retail investors

Lets go👇

(1/20)

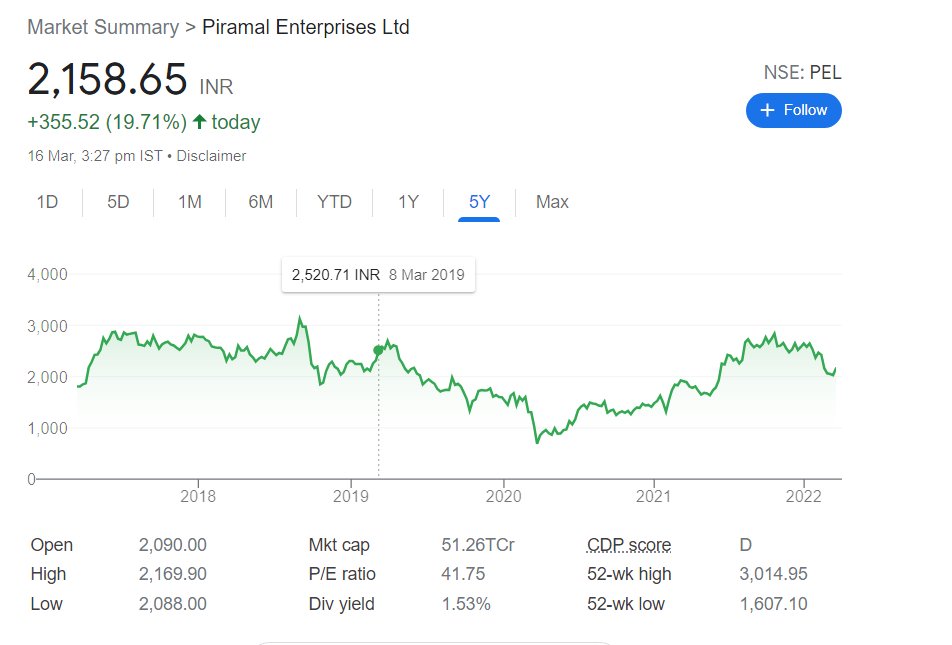

Piramal Stock has underperformed the markets over the last 2-3 years

The company went ahead and declared a demerger b/w the pharma and the financial services business.

(2/20)

The company went ahead and declared a demerger b/w the pharma and the financial services business.

(2/20)

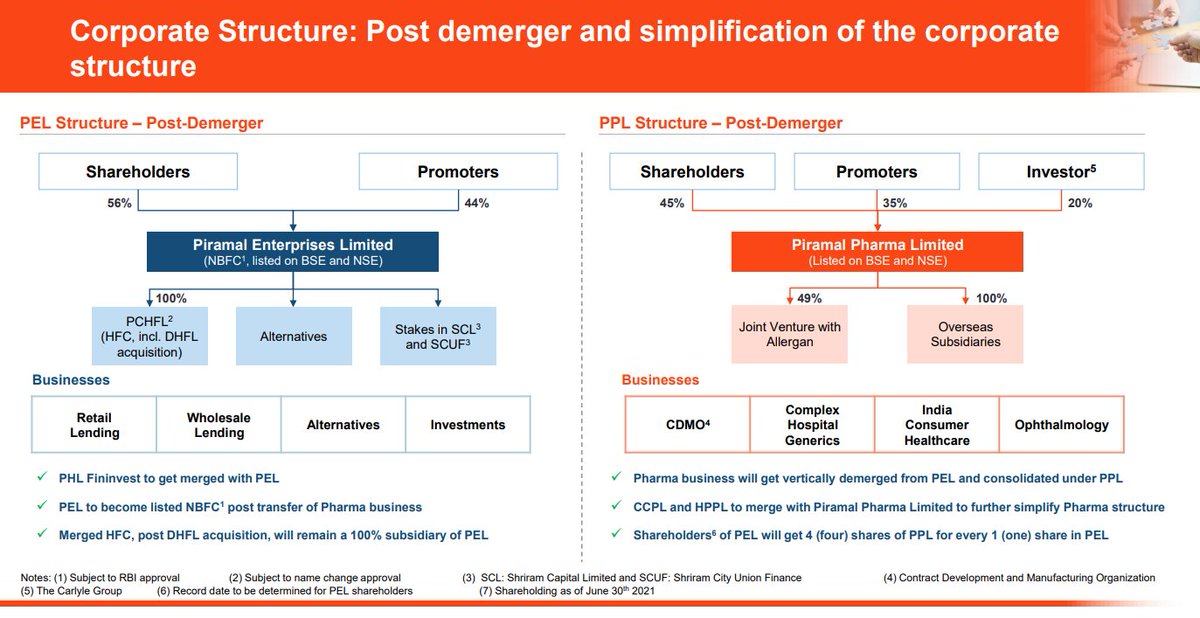

The demerger:-

To simplify the corporate structure

Piramal Pharma is the soon-to-be demerged vertical of Piramal Enterprises: 4 shares of Piramal Pharma for 1 share of the listed entity

(3/20)

To simplify the corporate structure

Piramal Pharma is the soon-to-be demerged vertical of Piramal Enterprises: 4 shares of Piramal Pharma for 1 share of the listed entity

(3/20)

Let us analyze both these businesses

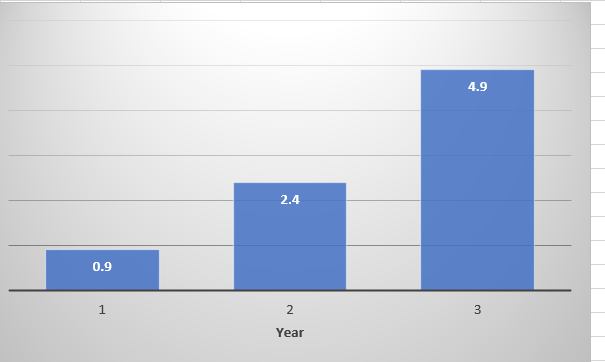

Financial Services:-

Piramal was one of the worst-hit by the IL&FS crisis and the subsequent fallout.

Piramal has most of its book to real-estate developers which took a massive hit

Gross NPA rose from 0.9% to about 4.9% in 2021

(4/20)

Financial Services:-

Piramal was one of the worst-hit by the IL&FS crisis and the subsequent fallout.

Piramal has most of its book to real-estate developers which took a massive hit

Gross NPA rose from 0.9% to about 4.9% in 2021

(4/20)

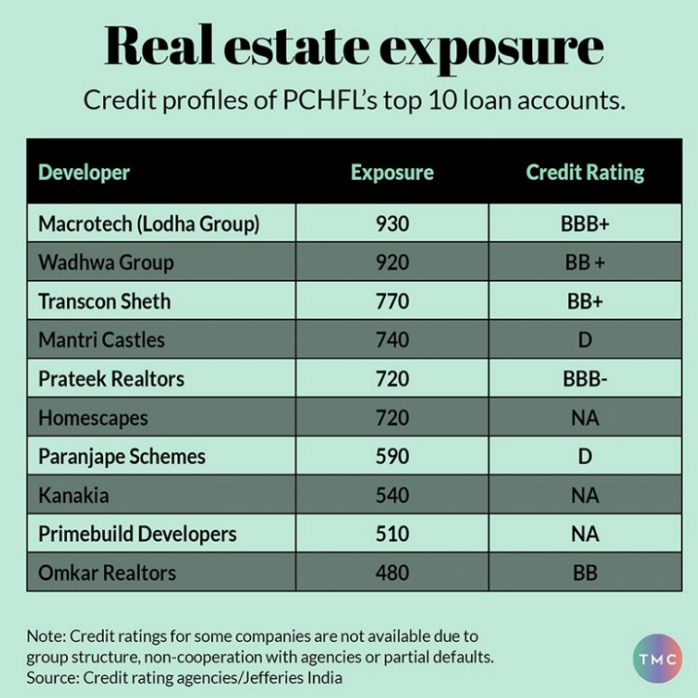

Exposure to toxic builder loans

As the IL&FS crisis choked builders,Piramal faced severe problems.

85% exposure to wholesale developers came to bite them.

(5/20)

As the IL&FS crisis choked builders,Piramal faced severe problems.

85% exposure to wholesale developers came to bite them.

(5/20)

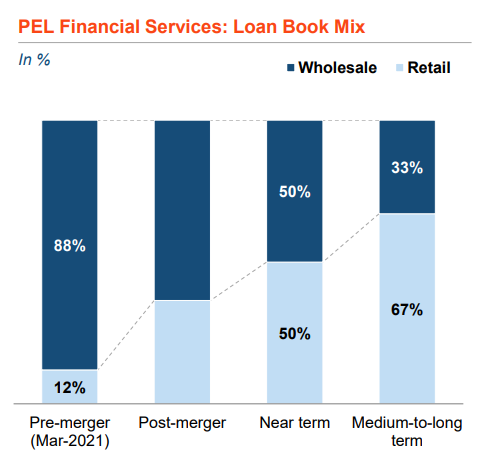

Change in strategy:-

Realizing the vulnerability to real estate developers,

Piramal changed its strategy:-

From 85% wholesale book now they want to target 67% retail book and began to run down the wholesale book.

(6/20)

Realizing the vulnerability to real estate developers,

Piramal changed its strategy:-

From 85% wholesale book now they want to target 67% retail book and began to run down the wholesale book.

(6/20)

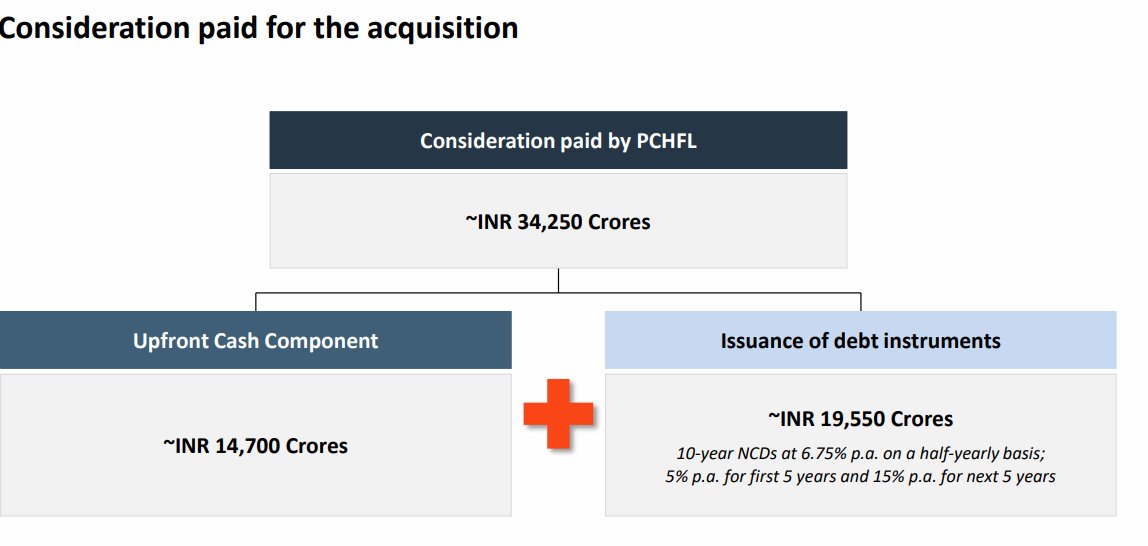

DHFL acquisition:-

In order to strengthen the retail business,Piramal bought the stressed DHFL for nearly 34,250cr.

This helped Piramal to increase its reach and scale massively.

Thus forging the path to be a solid retail lender

(7/20)

In order to strengthen the retail business,Piramal bought the stressed DHFL for nearly 34,250cr.

This helped Piramal to increase its reach and scale massively.

Thus forging the path to be a solid retail lender

(7/20)

The seasoning of the DHFL book remains to be seen.

However the discounted price paid by Piramal should take care of any rise in the NPAs.

(8/20)

However the discounted price paid by Piramal should take care of any rise in the NPAs.

(8/20)

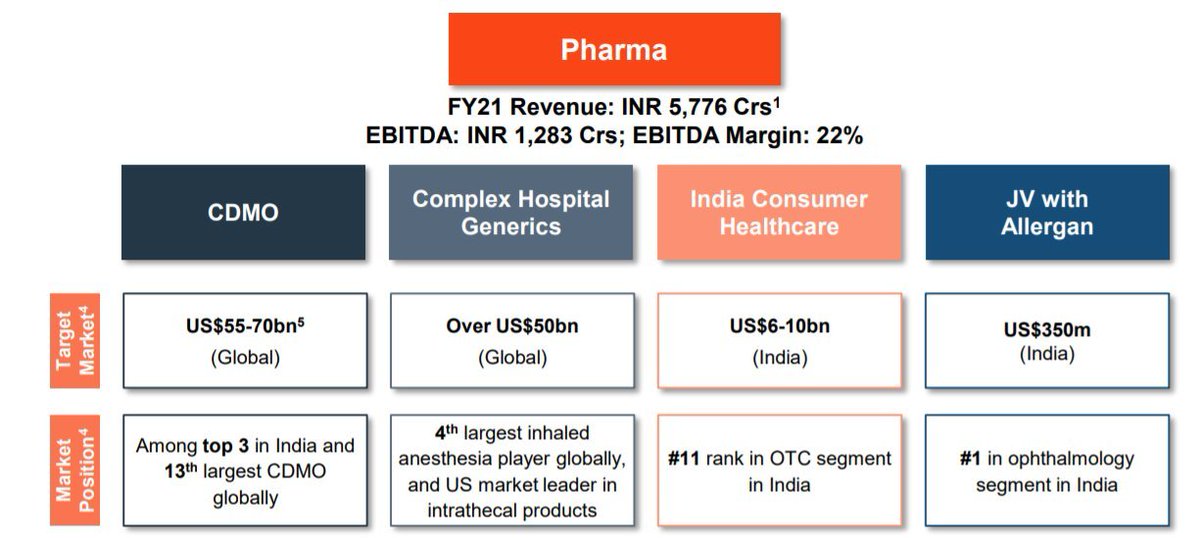

The jewel in the crown-

Pharma Business:-

Piramal Pharma's TTM Rev: 6K crs

CDMO: 3.7K crs

Complex Hospital Generics: 1.8K crs

Indian Consumer Healthcare: 0.6K crs

JV with Allergen: 0.4K crs (49% stake)

TTM EBITDA of Piramal Pharma: 1.3K crs

(9/20)

Pharma Business:-

Piramal Pharma's TTM Rev: 6K crs

CDMO: 3.7K crs

Complex Hospital Generics: 1.8K crs

Indian Consumer Healthcare: 0.6K crs

JV with Allergen: 0.4K crs (49% stake)

TTM EBITDA of Piramal Pharma: 1.3K crs

(9/20)

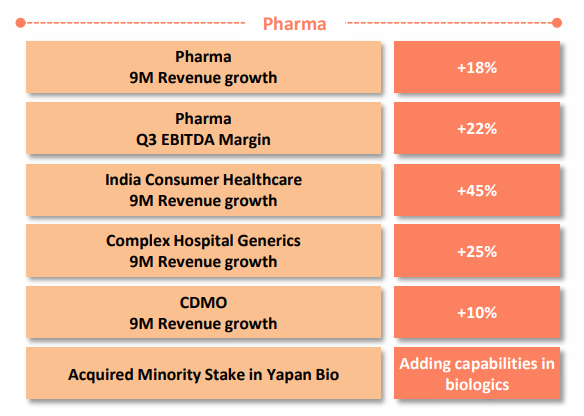

The CDMO business reported strong performance over the 2-3 quarters.

In fact the management has also upgraded the growth and the margin guidance for the coming quarters.

(10/20)

In fact the management has also upgraded the growth and the margin guidance for the coming quarters.

(10/20)

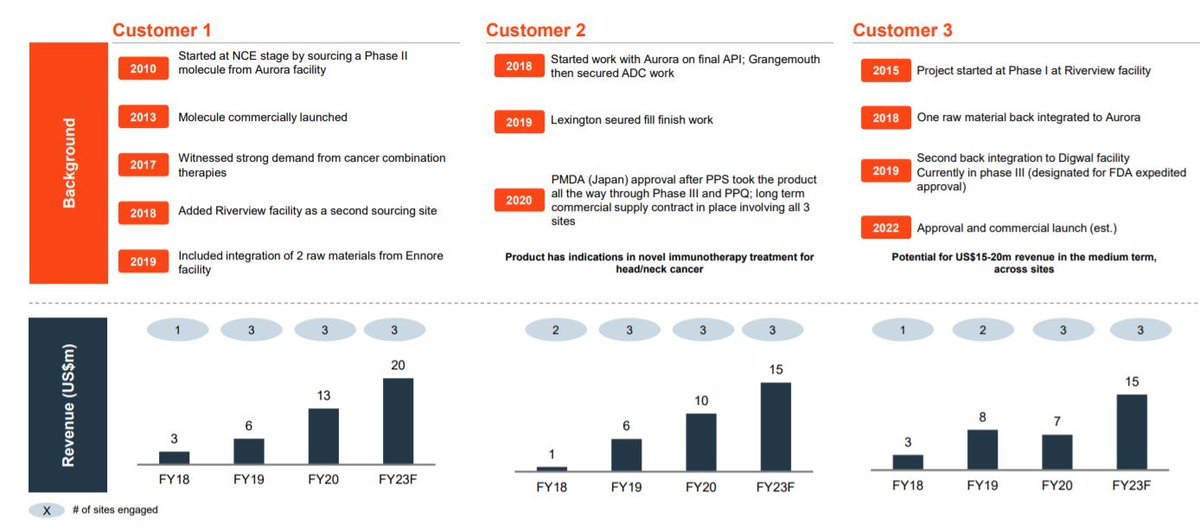

Positive business optionalities for Piramal Pharma

CDMO: 3x increase in phase III molecules from 10 in FY17 to 30 in FY21 & Significant growth in commercial products under patent from 11 in FY19 to 19 in FY21 with 500+ customers

The potential scale-up 💥👇

(11/20)

CDMO: 3x increase in phase III molecules from 10 in FY17 to 30 in FY21 & Significant growth in commercial products under patent from 11 in FY19 to 19 in FY21 with 500+ customers

The potential scale-up 💥👇

(11/20)

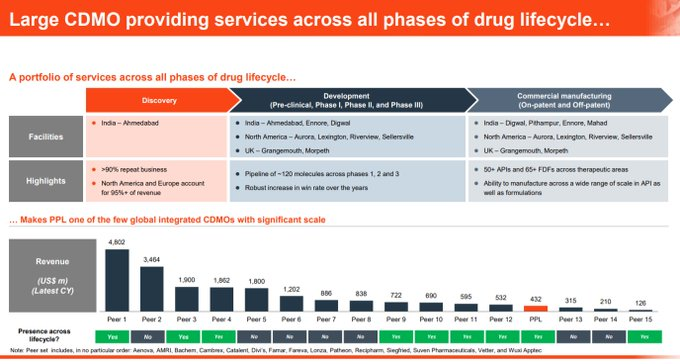

Expertise in niche, complex, and high margin areas like HPAPI, sterile injectables, hormones & peptide API

13th largest CDMO in the world & present across all phases of the drug lifecycle (for example,even Syngene isn't till now, it is trying to enter manufacturing)

(12/20)

13th largest CDMO in the world & present across all phases of the drug lifecycle (for example,even Syngene isn't till now, it is trying to enter manufacturing)

(12/20)

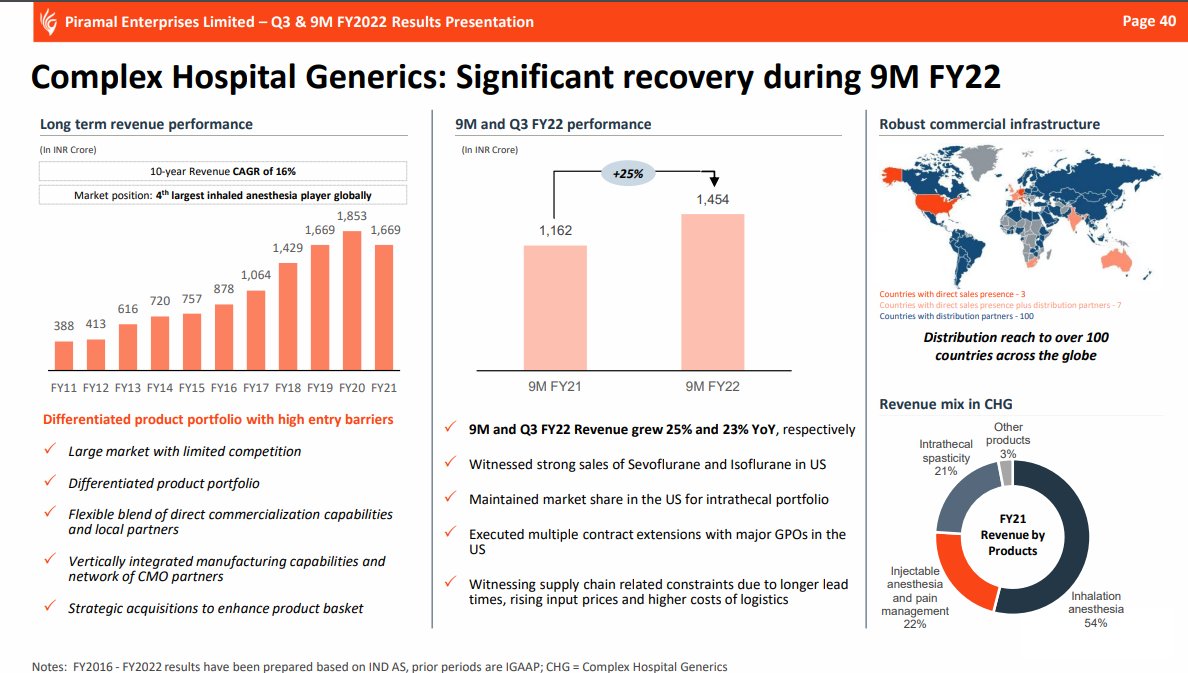

Complex hospital business continues to recover after a slump due to COVID-19

(13/20)

(13/20)

Valuation:-

The financial services business has a book value in the range of 30,000cr-33000cr.

A severe de-rating of the stock has been seen over the last 2 years due to poor performance in the financial service space.

(14/20)

The financial services business has a book value in the range of 30,000cr-33000cr.

A severe de-rating of the stock has been seen over the last 2 years due to poor performance in the financial service space.

(14/20)

As the upcycle in credit comes over the next 1-2 years the financial services business will start to get valued at Book Value or above.

(15/20)

(15/20)

If I take in a Price to book of 1x for Financial services

Value of 80% of Piramal Pharma at 35K crores - Total Mcap of 44K crores & EV of 47K crores

Valuations:

EV/EBITDA- 36x

EV/Sales- 7.7x

(16/20)

Value of 80% of Piramal Pharma at 35K crores - Total Mcap of 44K crores & EV of 47K crores

Valuations:

EV/EBITDA- 36x

EV/Sales- 7.7x

(16/20)

What valuation is comfortable for the Pharma business?

As per its high entry barrier business segments,we have observed that similar global assets trade anywhere b/w 15-20x EBITDA

Note that they sold 20% of the business to Carlyle at 4x EV/Sales & 20x EV/EBITDA.

(17/20)

As per its high entry barrier business segments,we have observed that similar global assets trade anywhere b/w 15-20x EBITDA

Note that they sold 20% of the business to Carlyle at 4x EV/Sales & 20x EV/EBITDA.

(17/20)

Conclusion:-

Piramal's financial services has taken a severe beating over the last 2-3 years.

Due to this, the true value of the Pharma business is not reflected.

(18/20)

Piramal's financial services has taken a severe beating over the last 2-3 years.

Due to this, the true value of the Pharma business is not reflected.

(18/20)

Ingredients are all in place for the financial services business to come back.

-Transformation to a retail franchise

-Upcycle in credit will mean an easing of credit costs.

(19/20)

-Transformation to a retail franchise

-Upcycle in credit will mean an easing of credit costs.

(19/20)

So is Piramal an oppotunity?

It all depends on the performance of the Financial Sevices business.

If that business does well....both Piramal stocks on listing can give bumper returns and unlock value.

(20/20)

It all depends on the performance of the Financial Sevices business.

If that business does well....both Piramal stocks on listing can give bumper returns and unlock value.

(20/20)

Loading suggestions...