A Thread 🧵on a small IT company that can grow fast and name of that company is BIRLASOFT

We're gonna take a look at History of the company

What changed?

Financials

What's next?

We're gonna take a look at History of the company

What changed?

Financials

What's next?

Before getting into the details about the company, 1st let's try to understand what exactly IT services companies do.

So Broadly speaking there are mainly 2 types of IT companies -

Product based & Service Based.

So Broadly speaking there are mainly 2 types of IT companies -

Product based & Service Based.

So the Product based companies are the companies that produce products and sells them directly to the customers like Google (Android), Microsoft ( Windows & MS Office) etc.

So basically it's a D2C type of business where you're directly dealing with the end consumer.

So basically it's a D2C type of business where you're directly dealing with the end consumer.

On the other hand Service based companies provides service to other companies, let's try to understand it with an example -

You've used amazon right? So as you know the product catalog is updated literally every single minute right?

So who's working in the background?

You've used amazon right? So as you know the product catalog is updated literally every single minute right?

So who's working in the background?

Or as you go to any bank's website, I'm sure who's come across some kind of virtual assistant right?

Just like this one.

Ever wondered who built that bot?

That's basically what IT service companies do.

Just like this one.

Ever wondered who built that bot?

That's basically what IT service companies do.

This is just the simplest example that came to my mind, they actually do a lotttttttt of different stuff.

Just like banks are the backbone of Economy, similarly IT services is the backbone of DIGITAL WORLD.

Now that we've understood what these IT services companies do

Just like banks are the backbone of Economy, similarly IT services is the backbone of DIGITAL WORLD.

Now that we've understood what these IT services companies do

Let's take a look at the market size globally and domestic and the size of opportunity

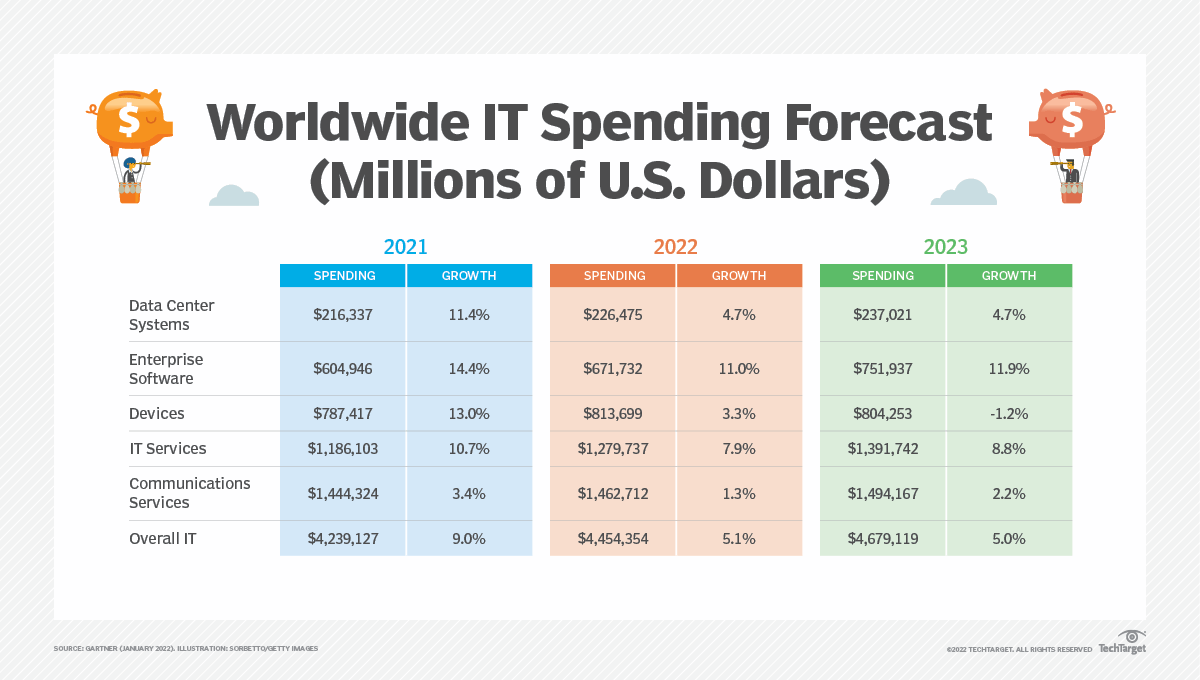

Gartner's worldwide spending forecast, released this week, anticipates 7.9% year-over-year growth for IT services in 2022 The global IT services market is expected to reach $1.3 trillion this

Gartner's worldwide spending forecast, released this week, anticipates 7.9% year-over-year growth for IT services in 2022 The global IT services market is expected to reach $1.3 trillion this

year.

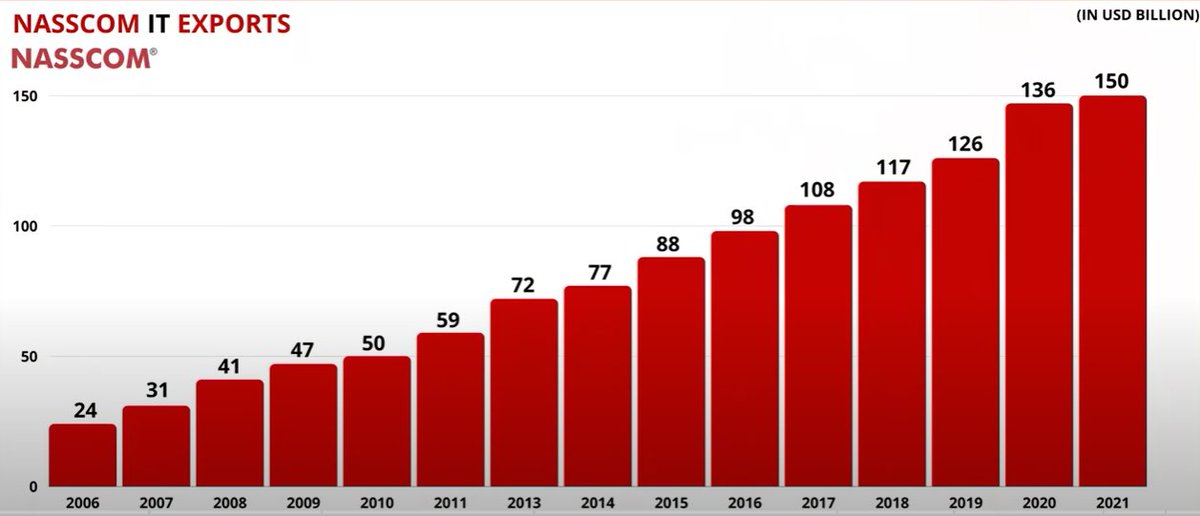

According to NASSCOM, Indian IT industry is expected to reach US$ 350Bn by 2025 against US$ 198 Bn FY21.

Currently Indian IT Exports industry is valued at 150$.

According to NASSCOM, Indian IT industry is expected to reach US$ 350Bn by 2025 against US$ 198 Bn FY21.

Currently Indian IT Exports industry is valued at 150$.

Now let's take a look at BRILASOFT

1st lets start with the HISTORY -

Birlasoft is part of the CK Birla Group, a 2.8$ Bn conglomerate.

It was formed in 1995 with General Electric as it's anchor client.

1st lets start with the HISTORY -

Birlasoft is part of the CK Birla Group, a 2.8$ Bn conglomerate.

It was formed in 1995 with General Electric as it's anchor client.

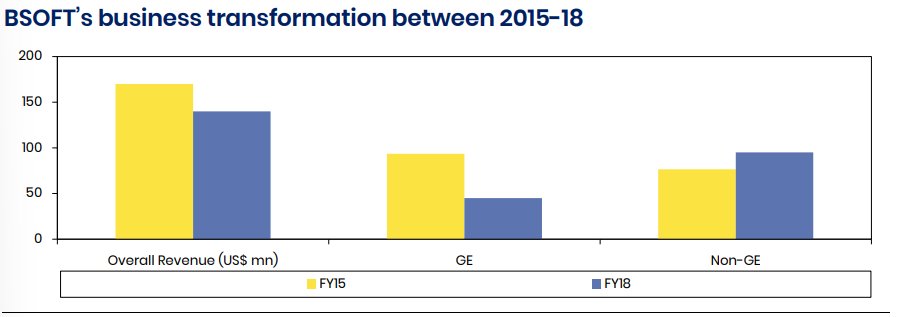

The company had revenue of US$ 170 mn in FY15 and 55% of the was coming from General Electric.

The real story began in 2015 when Mr Anjan Lahiri a veteran from Mindtree joined as the CEO.

The real story began in 2015 when Mr Anjan Lahiri a veteran from Mindtree joined as the CEO.

He took all the right steps and bought down the GE's revenue share down to 25% in 2018 from 55% in 2015.

Company sold the remaining GE business on a slump sale basis to Genpact for 15$ Mn.

At the same time, Non GE business reached to 100$ Mn.

Company sold the remaining GE business on a slump sale basis to Genpact for 15$ Mn.

At the same time, Non GE business reached to 100$ Mn.

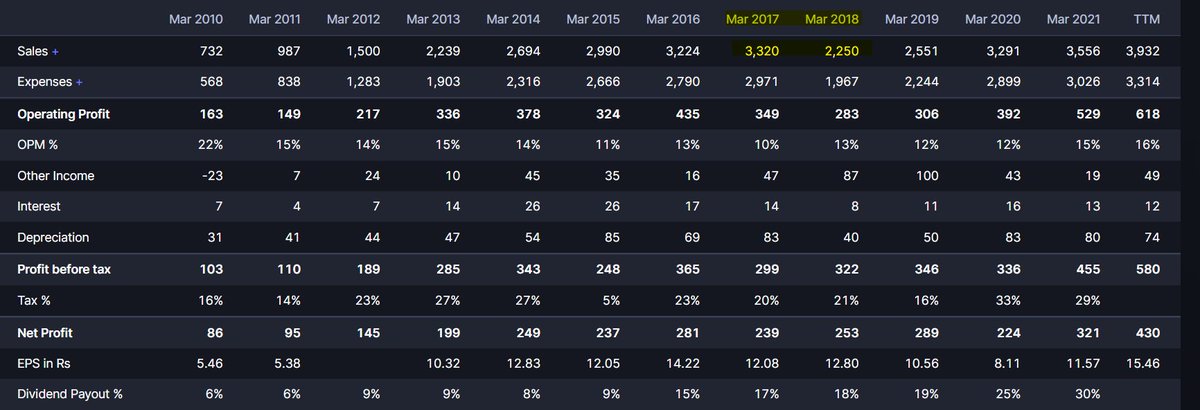

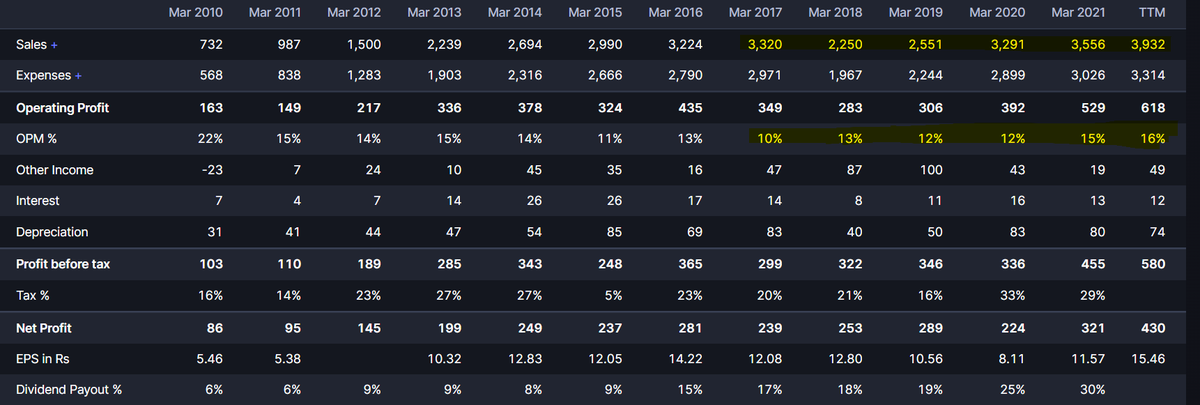

You can see the impact on revenues of GE business sale, the revenue went down from 3320 Cr to 2250 Cr.

Why did they sold the business? GE itself has been struggling from many years and soo much concentration on one client is dangerous.

If the client goes down, you go down.

Why did they sold the business? GE itself has been struggling from many years and soo much concentration on one client is dangerous.

If the client goes down, you go down.

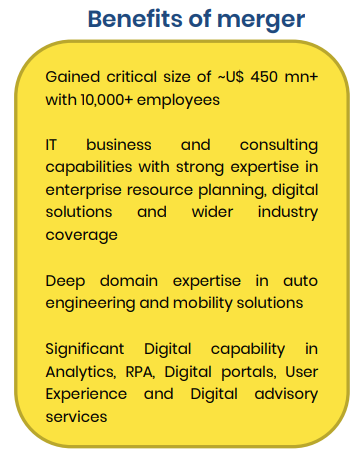

The 2nd stage of transformation began in 2019 when Legacy IT business of KPIT was merged with BIRLASOFT.

KPIT had legacy IT business with revenues of US$ 300 Mn in FY19 of which 70% was ERP (Enterprise Resource Planning, more on this later)

KPIT had legacy IT business with revenues of US$ 300 Mn in FY19 of which 70% was ERP (Enterprise Resource Planning, more on this later)

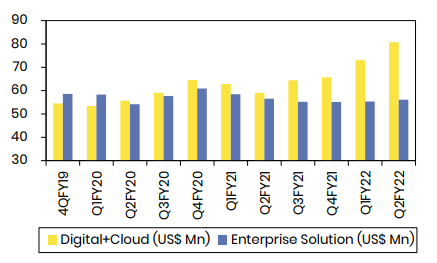

After the merger, more than 50% revenue was coming from the Enterprise Solutions, which is kind of a legacy business and fast forward to Q2FY22 60% revenues comes from Digital and cloud solutions (Growing >25% YoY) and only 40% comes from enterprise solutions.

But unfortunately Mr Anjan Lahiri took exit in 2020 and Mr Dharmender Kapoor who was the COO of the company was promoted to the position of CEO.

He has total 30 years of experience in IT industry. He started taking all the right steps, BIRLASOFT started hiring business head from

He has total 30 years of experience in IT industry. He started taking all the right steps, BIRLASOFT started hiring business head from

Tier-1 Companies.

Before Dharmeder Kapoor became CEO, birlasoft was horizontally focused, meaning? They had small-small deals mainly 1$Mn and had many clients and that reduced the focus.

What he did, he made birlasoft a Vertically focused company and they started focusing on

Before Dharmeder Kapoor became CEO, birlasoft was horizontally focused, meaning? They had small-small deals mainly 1$Mn and had many clients and that reduced the focus.

What he did, he made birlasoft a Vertically focused company and they started focusing on

Cross-selling. Meaning? They started offering other services to their existing clients.

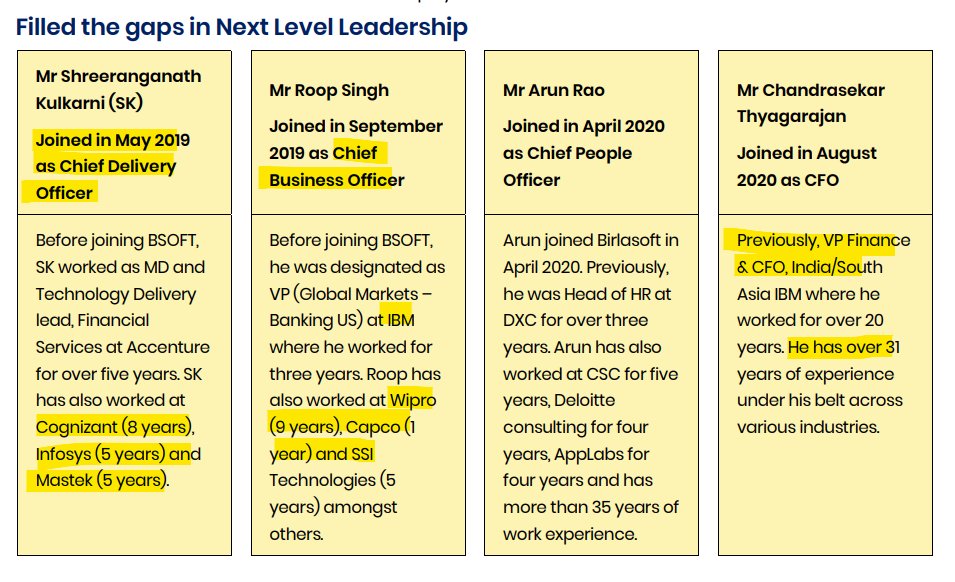

They've hired Mr Shreeranganath Kulkarni as Chief Delivery Officer. He has worked in organizations like Cognizant, Infosys, IBM, Mastek.

Mr Roop Singh as Chief Business Officer, he has previously worked in Wipro, Capco, SSI tech.

Mr Roop Singh as Chief Business Officer, he has previously worked in Wipro, Capco, SSI tech.

Mr Arun Rao as Chief People Officer and Mr Chandrasekar Thyagarajan as CFO who has 31 years of experience.

Mr Ashutish Mankar as VP Infra & Cloud Services, he has worked in Infosys, Cognizant and Microland.

Mr Vijay Mishra as Global Head SAP.

Mr Ashutish Mankar as VP Infra & Cloud Services, he has worked in Infosys, Cognizant and Microland.

Mr Vijay Mishra as Global Head SAP.

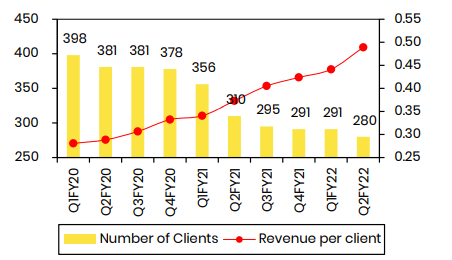

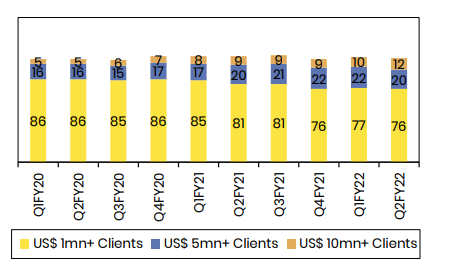

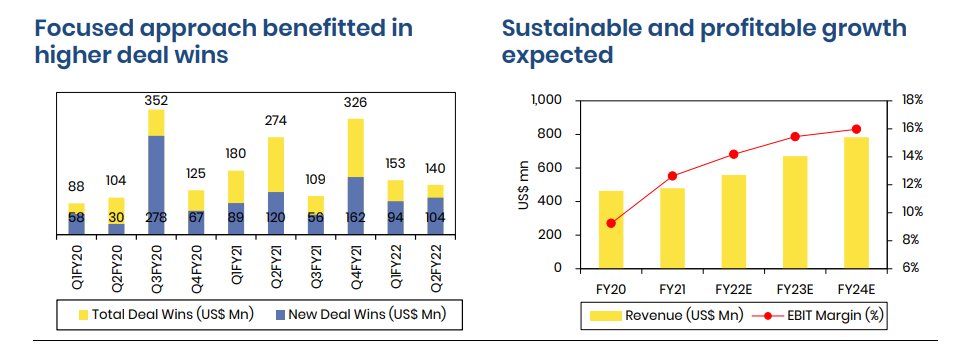

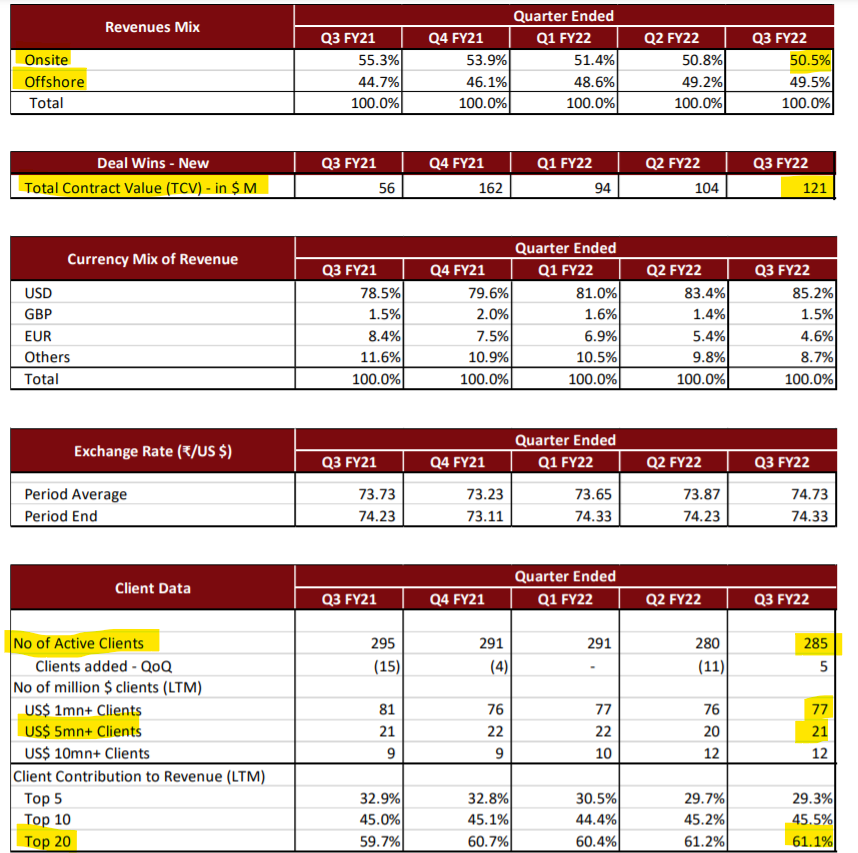

The plan is simple "Consolidation". They've started reducing the no. of tail accounts, total down from 398 Clients in FY20 to 280 Clients in Q2FY22 and revenue per client has been going up continuously.

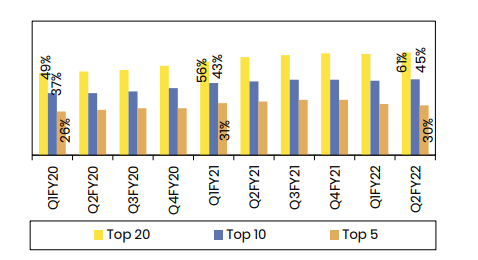

The share of Top 20 Clients has been going up from 45% >>> 61% (Cross-selling).

1$ mn clients have come down from 86 to 76 and 10$ Mn clients have gone up from 5 to 12 (Significant Improvement).

1$ mn clients have come down from 86 to 76 and 10$ Mn clients have gone up from 5 to 12 (Significant Improvement).

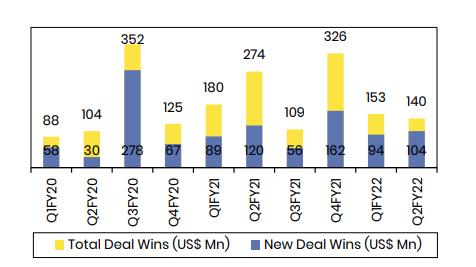

Total deal wins have been mostly above 100$ Mn since Q1FY20.

The share of digital and cloud has been increasing which has reach 60% of the total revenues.

The share of digital and cloud has been increasing which has reach 60% of the total revenues.

Now let's talk about their business segments, what they actually do and what services they offer.

So they have 2 main Business segments - SERVICES & SOLUTIONS.

So they have 2 main Business segments - SERVICES & SOLUTIONS.

Under SERVICES segment, they have 2 business segments - DIGITAL & ENTERPRISE SOLUTIONS.

Under Digital they offer -

Cloud

Blockchain

Customer Experience

Data Analytics

Connected Products

Intelligent Automation

Under Digital they offer -

Cloud

Blockchain

Customer Experience

Data Analytics

Connected Products

Intelligent Automation

Cloud is the talk of the town but what's cloud?

Let's try to understand this with a very simple example - You've used Ms excel or maybe powerpoint etc right?

For that you need to download the MS office and install it in your computer right? That's on premise

Let's try to understand this with a very simple example - You've used Ms excel or maybe powerpoint etc right?

For that you need to download the MS office and install it in your computer right? That's on premise

which is how to old world works.

But now I'm sure you've come across something called Google sheets or google docs or google drive right? or maybe you're a fan of Microsoft then Microsoft 365 right?

But now I'm sure you've come across something called Google sheets or google docs or google drive right? or maybe you're a fan of Microsoft then Microsoft 365 right?

Now you just need internet connection and a web browser and you're good to go.

So then where all the data you're storing is going?

That going on cloud. And where is cloud? The server and the data centers of some cloud computing giants like your Google cloud, Microsoft & AWS.

So then where all the data you're storing is going?

That going on cloud. And where is cloud? The server and the data centers of some cloud computing giants like your Google cloud, Microsoft & AWS.

They are called hyperscaler and they're growing more than 40-50% QoQ🤯🤯.

So what the benefit for our IT services companies?

They're the ones who are helping business to Migrate to Cloud.

Simply they're riding on the back of these Hyper-Scalers.

So what the benefit for our IT services companies?

They're the ones who are helping business to Migrate to Cloud.

Simply they're riding on the back of these Hyper-Scalers.

In cloud they offer all Public cloud, Private cloud and Hybrid cloud and other services like SAP HANA (Which is cloud ERP) etc etc.

They depend their ties with Microsoft Azure and announced strategic partnership with Freshworks (Which is a Saas company - Software as a service)

In Data Analytics they offer services like Data Management, Data Visualization etc.

We're generating tons and tons of data every single second. How to make that data useful is what matters and these companies are helping businesses doing just that.

We're generating tons and tons of data every single second. How to make that data useful is what matters and these companies are helping businesses doing just that.

They're even have presence in Blockchain although not very significant.

In that they offer services like - warranty management, container tracking, supply chain sustainability etc.

In that they offer services like - warranty management, container tracking, supply chain sustainability etc.

Now let's take a look at the legacy part of their business which is Enterprise Solutions.

In this segment they offer services like JD EDWARD ( One of the leaders of on premise ERP era), Oracle ( King of Database management) SAP ( Leader in ERP) etc.

In this segment they offer services like JD EDWARD ( One of the leaders of on premise ERP era), Oracle ( King of Database management) SAP ( Leader in ERP) etc.

Plus they offer services like Customer Relationship Management

Product Lifecycle Management

Supply chain Management

Application development, management, testing etc.

Product Lifecycle Management

Supply chain Management

Application development, management, testing etc.

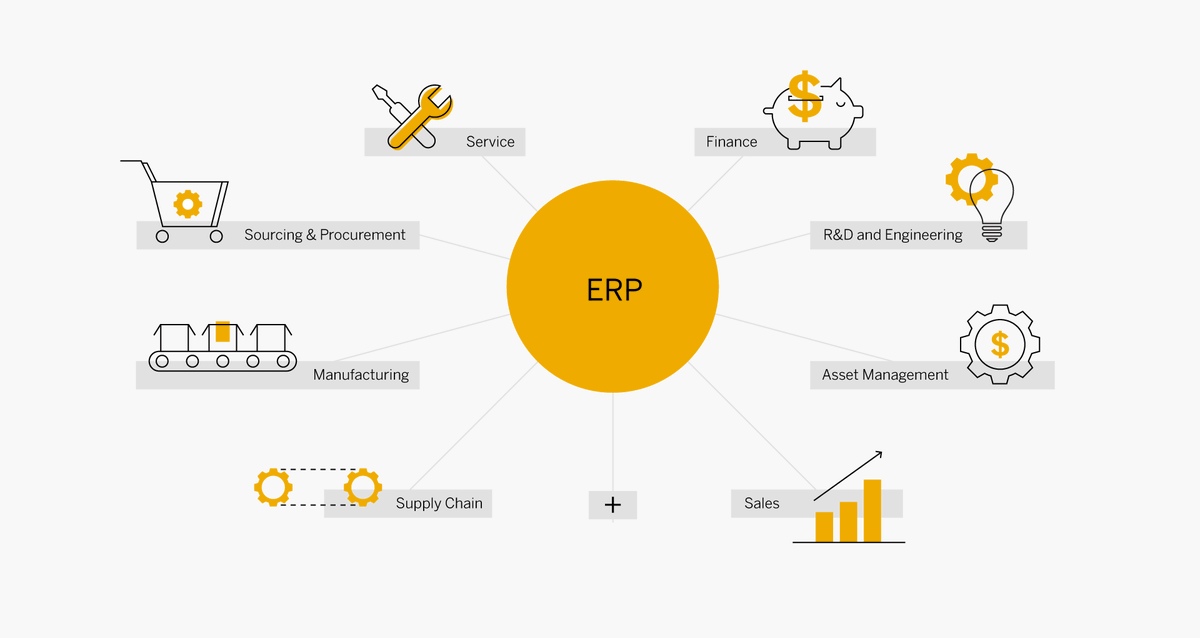

I've repeatedly used the word ERP, let's to understand what ERP actually is.

Let's start with the full form, EPR - Enterprise resource planning.

It's simply a central hub where all the communication b/w different parts of a busines takes place.

Let's start with the full form, EPR - Enterprise resource planning.

It's simply a central hub where all the communication b/w different parts of a busines takes place.

Every business has different department like finance, HR, Service, R&D, Supply chain, Sales etc and they need real time and information sharing a smooth communication b/w them.

So who's helping them? That's where ERP comes in - it helps to connect all those elements under

So who's helping them? That's where ERP comes in - it helps to connect all those elements under

single central entity.

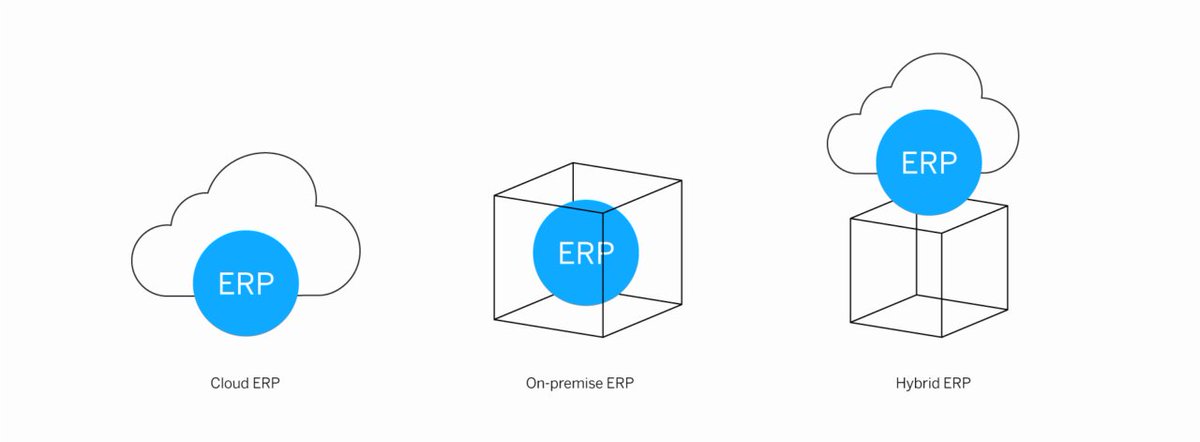

ERP can also be implemented on Cloud, On premise or Hybrid ( Cloud + On premise)

The likes of JD Edward are your on-premise ERP software suite and Oracle Cloud and SAP HANA (one of the most popular) are your Cloud EPR solutions.

ERP can also be implemented on Cloud, On premise or Hybrid ( Cloud + On premise)

The likes of JD Edward are your on-premise ERP software suite and Oracle Cloud and SAP HANA (one of the most popular) are your Cloud EPR solutions.

Now let's take a look at the SOLUTIONS part of their business.

Let's talk about them 1 by 1.

1) intelliOPEN - They launched this solution during the COVID times to help businesses open safely.

Smart, touchless, contactless screen and monitoring solution

Let's talk about them 1 by 1.

1) intelliOPEN - They launched this solution during the COVID times to help businesses open safely.

Smart, touchless, contactless screen and monitoring solution

that provides Environmental Health Safety (EHS) solution in COVID times.

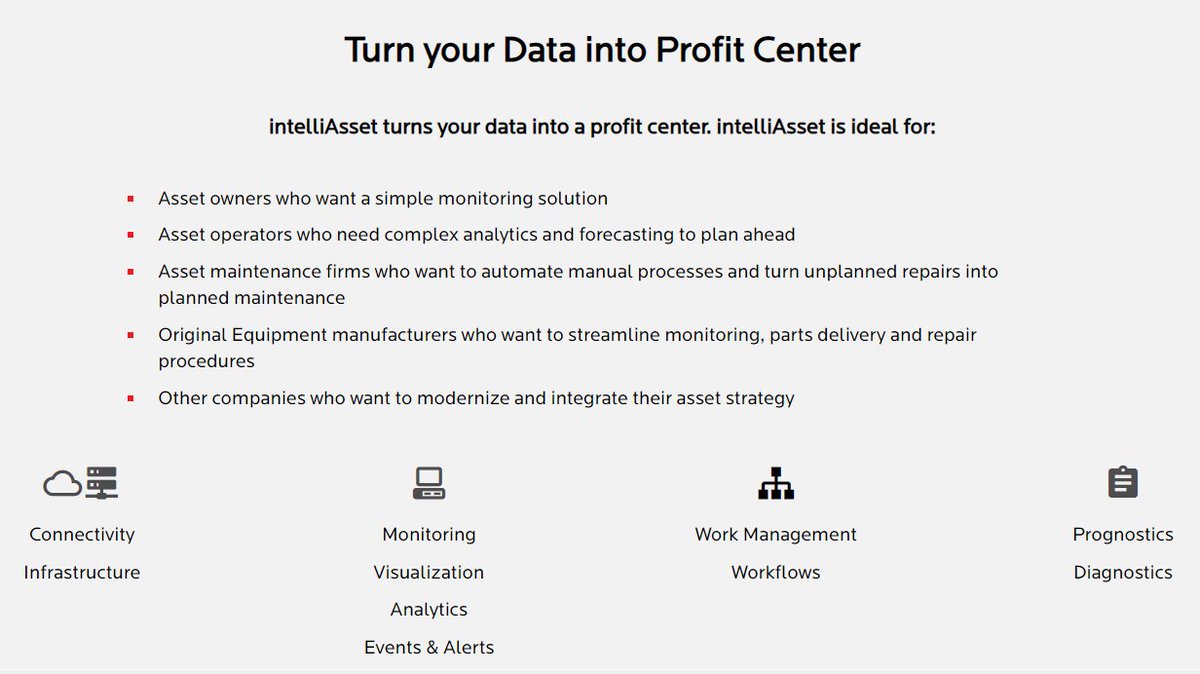

2) intelliAsset - Asset monitoring solution that enables remote asset visualization, analysis & enable diagnosis, maintenance activities.

2) intelliAsset - Asset monitoring solution that enables remote asset visualization, analysis & enable diagnosis, maintenance activities.

3) TruView CLM - Contract lifecycle management, enables guided customer onboarding, contract management and tracking payments.

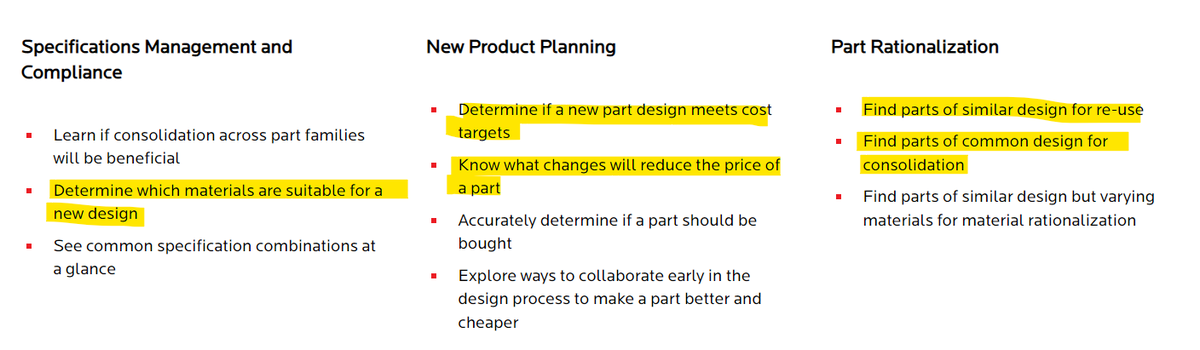

4) Akoya - Helps companies stay compliant to industry standards. Helps them plan new products, find parts that can be re-used and supply chain management.

Determining suitable materials for new parts, knowing what changed will reduce the price and find similar designs for re-use

Determining suitable materials for new parts, knowing what changed will reduce the price and find similar designs for re-use

5) TrueServ FMS - Field service management, IoT integration for touchless processes.

It's a cloud solution build on salesforce.

It's a cloud solution build on salesforce.

6) TrueLENS - This is a tool built on salesforce platform to provide insights on existing salesforce implementation.

Now that we're understood what the company actually does, let's talk about numbers and opportunity and risks.

IT services is a very commoditized business, specially for the small guys it's difficult because the big 4 (TCS, Infosys, Wipro & HCL) have all the capabilities

IT services is a very commoditized business, specially for the small guys it's difficult because the big 4 (TCS, Infosys, Wipro & HCL) have all the capabilities

and are present across the entire value chain.

What these small companies do that they build their niche, they remain in a specific area where they can provide the solutions for low lost as compared to the peers and win the customers.

What these small companies do that they build their niche, they remain in a specific area where they can provide the solutions for low lost as compared to the peers and win the customers.

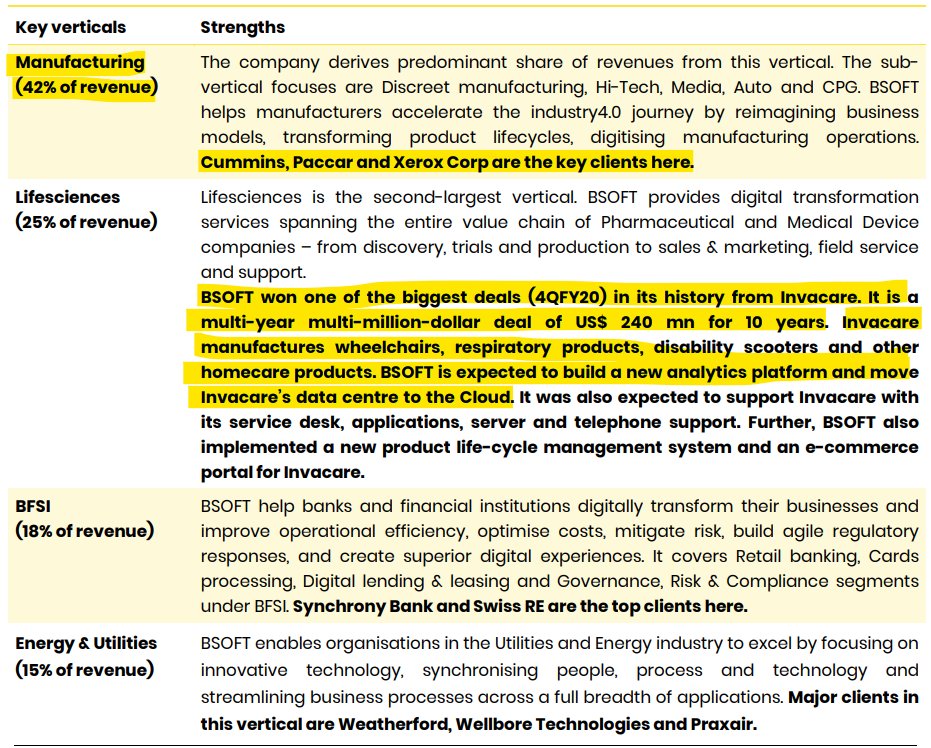

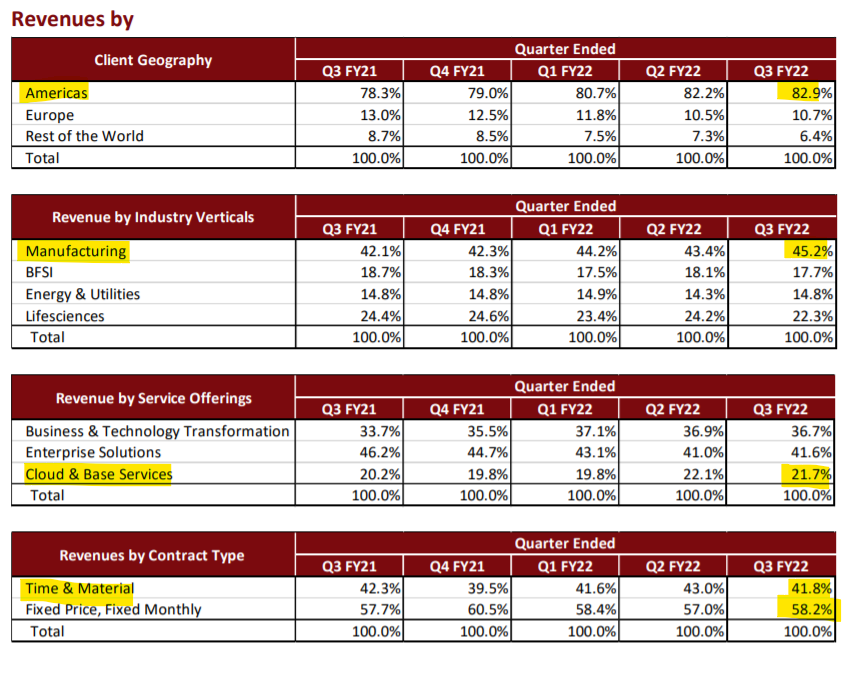

They mainly service manufacturing industry (42% of revenues), life sciences (25%0, BFSI (18%) and Energy and Utility (15%)

Majority of revenues comes from manufacturing sector which is kind of a little cyclical as it gets effects due to broader economic slowdown.

Majority of revenues comes from manufacturing sector which is kind of a little cyclical as it gets effects due to broader economic slowdown.

And the slowdown in the growth of end user industry will directly affect them as many of them won't prefer spending much on IT during the downcycle.

So that's something that remains to be seen.

They recently won a very big deal from a company name Invacare

So that's something that remains to be seen.

They recently won a very big deal from a company name Invacare

who manufactures wheelchairs, respiratory prodcuts etc.

BIRLASOFT will build a new analytics platform for them and move their data center to cloud. ( DEAL SIZE - 240$ Mn for 10 years)

BIRLASOFT will build a new analytics platform for them and move their data center to cloud. ( DEAL SIZE - 240$ Mn for 10 years)

Revenue growth has not been that strong and margins have been very volatile.

After selling the GE business, revenues fell from 3320Cr to 2250Cr.

From past few years, margins haven been expanding ( From 10% In 2017 to 16% on TTM basis)

After selling the GE business, revenues fell from 3320Cr to 2250Cr.

From past few years, margins haven been expanding ( From 10% In 2017 to 16% on TTM basis)

Post GE deal has posted the revenue CAGR for 12%.

Bright side? New management is cutting the tail accounts and focusing on cross-selling and getting the big clients.

Deal pipeline has been strong ( >100Mn $ from past few quarters).

Bright side? New management is cutting the tail accounts and focusing on cross-selling and getting the big clients.

Deal pipeline has been strong ( >100Mn $ from past few quarters).

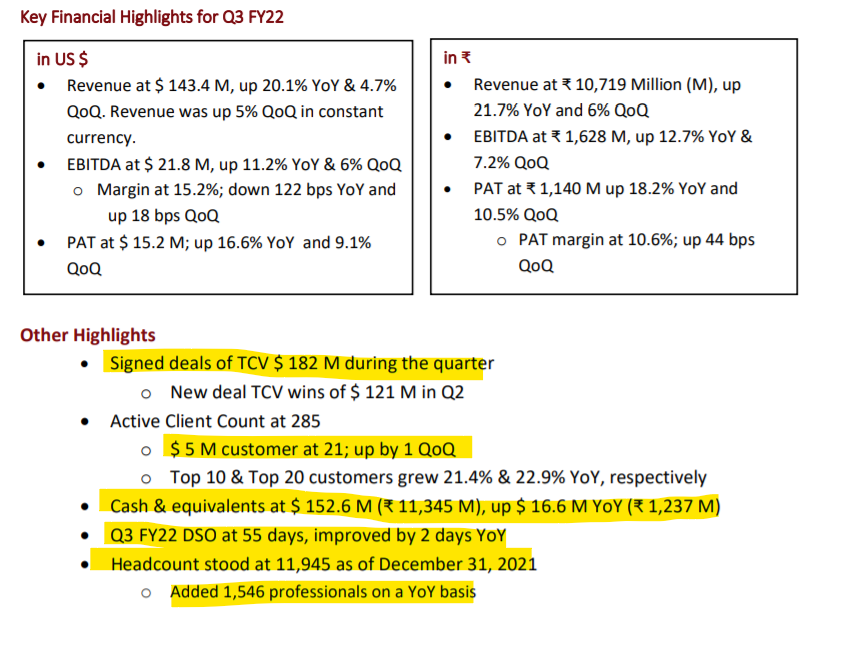

Latest Quarterly highlights -

Signed deals worth 182$ Mn during the quarter.

5$ Mn client at 21, up by 1 QoQ

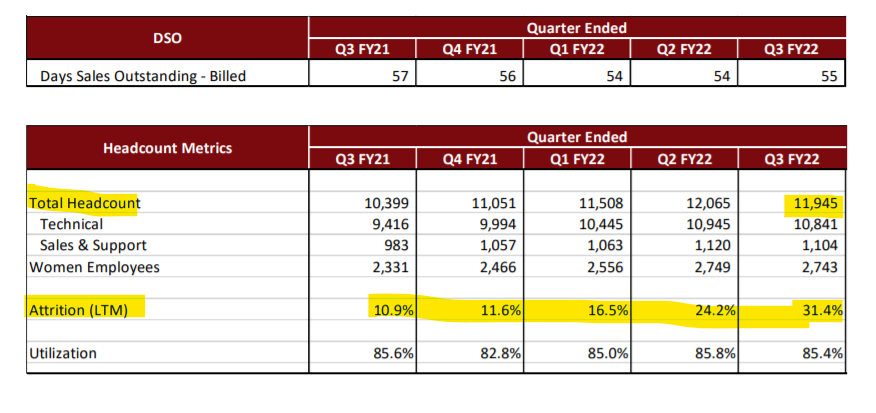

DSO ( Day sales outstanding) at 55 days

Added 1,546 new employees

Signed deals worth 182$ Mn during the quarter.

5$ Mn client at 21, up by 1 QoQ

DSO ( Day sales outstanding) at 55 days

Added 1,546 new employees

Geographical concentration - 82.9% revenues from America.

Contribution of Manufacturing sector further increased to 45%

Cloud based solutions at 21%

Time & Material contracts at 41.8% & Fixed priced at 58.2% (Maintaining margins in fixed contracts is difficult)

Contribution of Manufacturing sector further increased to 45%

Cloud based solutions at 21%

Time & Material contracts at 41.8% & Fixed priced at 58.2% (Maintaining margins in fixed contracts is difficult)

Onsite - offshore mix almost at 50-50 ( Offshore has better margins)

New deal wins at 121$ Mn

Added 5 new clients during the quarter

Contribution of Top 20 clients now at 61%

New deal wins at 121$ Mn

Added 5 new clients during the quarter

Contribution of Top 20 clients now at 61%

Total Headcount down QoQ to 11,945 from 12,065

Attrition has jumped to 31.4% 🤯🤯 (Amongst the highest in the industry) good thing is it's on lower levels not among the senior level employees.

Attrition has jumped to 31.4% 🤯🤯 (Amongst the highest in the industry) good thing is it's on lower levels not among the senior level employees.

Opportunity -

- Cloud migration going on in full swing

- Deal Pipeline is strong

- Economic cycle turning ( Will help the manufacturing sector)

- Management taking right step - removing tails accounts and becoming vertically focused

- Cloud migration going on in full swing

- Deal Pipeline is strong

- Economic cycle turning ( Will help the manufacturing sector)

- Management taking right step - removing tails accounts and becoming vertically focused

Risks -

- Deal momentum slowing down

- High attrition hurting the margins

- Churn in top level management

- High dependence on manufacturing sector

- Higher %age of fixed contracts ( Hard to maintain margins in current environment)

- Salary hikes will impact margins directly

- Deal momentum slowing down

- High attrition hurting the margins

- Churn in top level management

- High dependence on manufacturing sector

- Higher %age of fixed contracts ( Hard to maintain margins in current environment)

- Salary hikes will impact margins directly

- Valuations at fair level, any slow down in deal momentum and revenue growth will hurt the valuations.

If you enjoyed the thread please like, share and Re-tweet this 1st tweet.

@sahil_vi @soicfinance @ishmohit1 @suru27 @itsTarH @shubhfin @shivang_ran @Finstor85 @mehrotra_saket

@sahil_vi @soicfinance @ishmohit1 @suru27 @itsTarH @shubhfin @shivang_ran @Finstor85 @mehrotra_saket

Loading suggestions...