Construction

Technology

Business

Engineering

Finance

Real Estate

Industry

manufacturing

Telecommunications

Power

Automobiles

Green Energy

Railways

Proxy for Green Energy, Real Estate & Manufacturing Capex🔌☀️🔋⚡️

In this thread I will explain:

1⃣ Industry growth

2⃣Market share of different players

3⃣Different types of Wires & Cables

4⃣About KEI Industries

5⃣Business Segments

6⃣Anti-Thesis Pointers

🤿Let's dive in:

In this thread I will explain:

1⃣ Industry growth

2⃣Market share of different players

3⃣Different types of Wires & Cables

4⃣About KEI Industries

5⃣Business Segments

6⃣Anti-Thesis Pointers

🤿Let's dive in:

KEI Industries established in 1968,manufactures cables and wires, with a product portfolio ranging from housing wires to Extra High Voltage (EHV) cables, and further diversifying into the Engineering,Procurement & Construction (EPC) services for power and transmission projects.

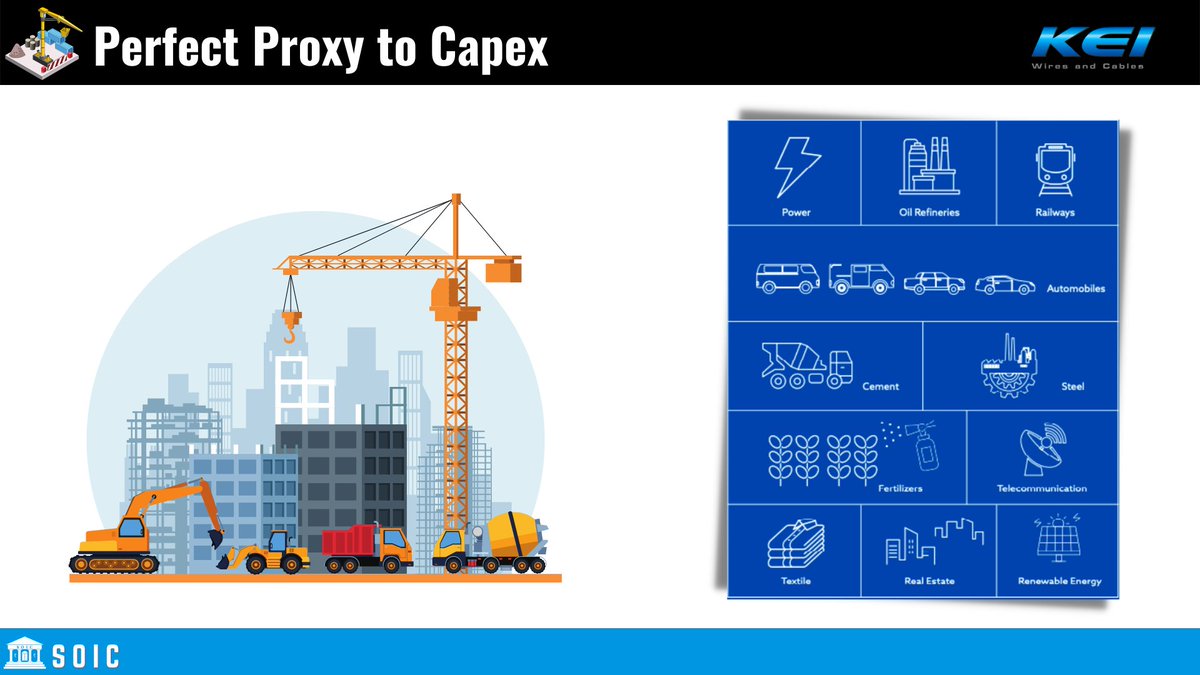

This sector is the perfect proxy to capex in various sectors like Power, Railways, Automobiles, Telecommunications, Real Estate etc. 🏗️🚗🚉

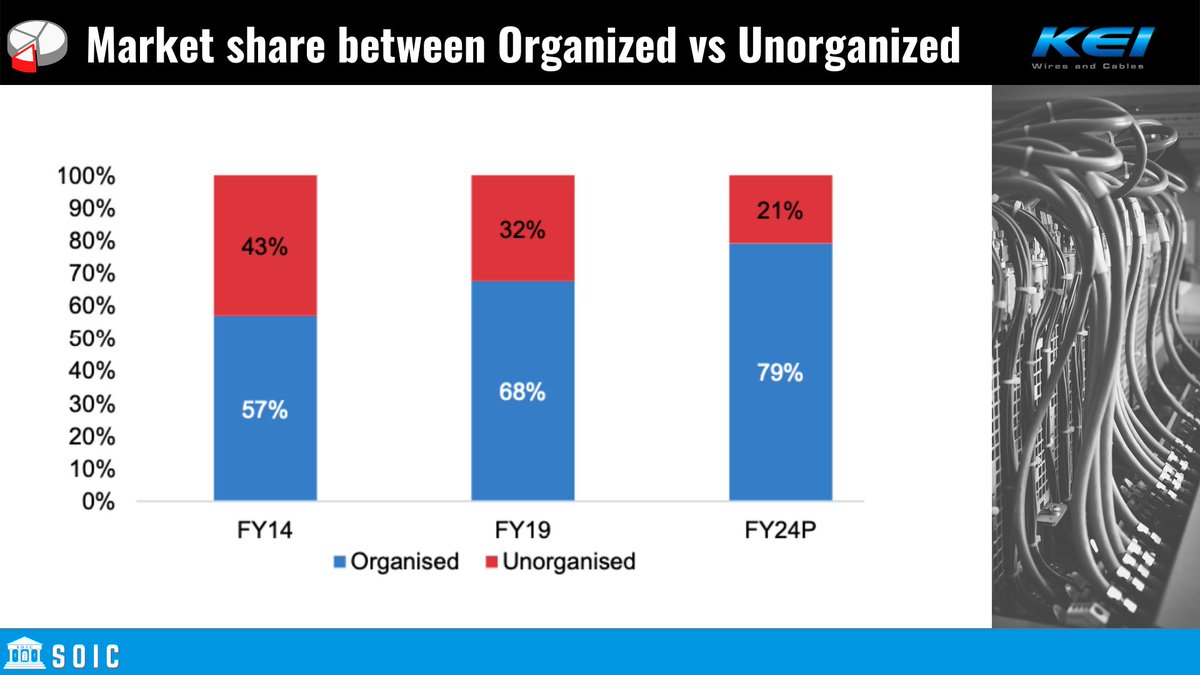

The Volume growth rate of Indian Cables and Wires manufacturers is approx. 13%. Along with that, the organized players are gaining the market share from unorganized players.🔌⚡️

📊The market share of different players in the Wires & Cables segment is as follows:

🔌The major reason for gaining the market share from unorganized players are:

▶️ Channel financing

▶️ Higher spending on advertisement & promotions

▶️ Implementation of GST

▶️ Entry barriers for small players in extra-high voltage

cables

▶️ Channel financing

▶️ Higher spending on advertisement & promotions

▶️ Implementation of GST

▶️ Entry barriers for small players in extra-high voltage

cables

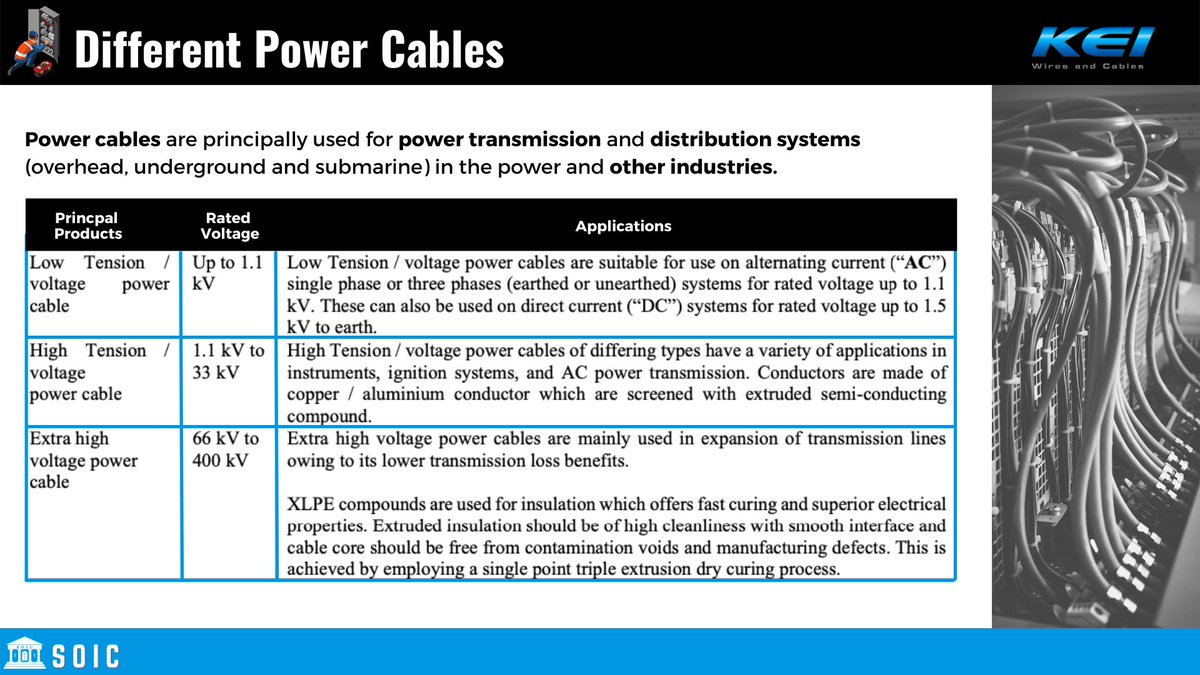

🔎Different types of Wires & Cables and their growth factors:

1⃣Power Cables: Higher investments in transmission and distribution drove the demand for power transmission cables.

1⃣Power Cables: Higher investments in transmission and distribution drove the demand for power transmission cables.

Demand for extra-high voltage (EHV) cables increased because of higher power density, lower transmission losses, and efficient bulk-power delivery by higher voltage cables. Metro rail, high-end hospitals, hotels and shopping malls use 1.1 kV HFFR cables to ensure public safety.⚡️

2⃣Building Wires: Growing penetration of mobile phones and appliances in Indian households has led to an increase in the number of electrical points, thereby driving the installation of building wires per household.

3⃣Solar Cables: An increase in solar capacity additions has increased the demand for solar cables.☀️

4⃣Control Cables: Growth in industrial automation across a wide range of industries, including oil and gas, power, pharmaceuticals, has driven the usage of control cables. ⛽️💊

4⃣Control Cables: Growth in industrial automation across a wide range of industries, including oil and gas, power, pharmaceuticals, has driven the usage of control cables. ⛽️💊

5⃣Flexible Cables: Growth in industrial automation across a wide range of industries, including automotive plants, steel, cement, has driven the usage of control cables. 🚗🧱

6⃣Fire Survival Cables: Fire survival cables are installed for feeding essential emergency services.🧯🚒

6⃣Fire Survival Cables: Fire survival cables are installed for feeding essential emergency services.🧯🚒

ℹ️ About KEI Industries:

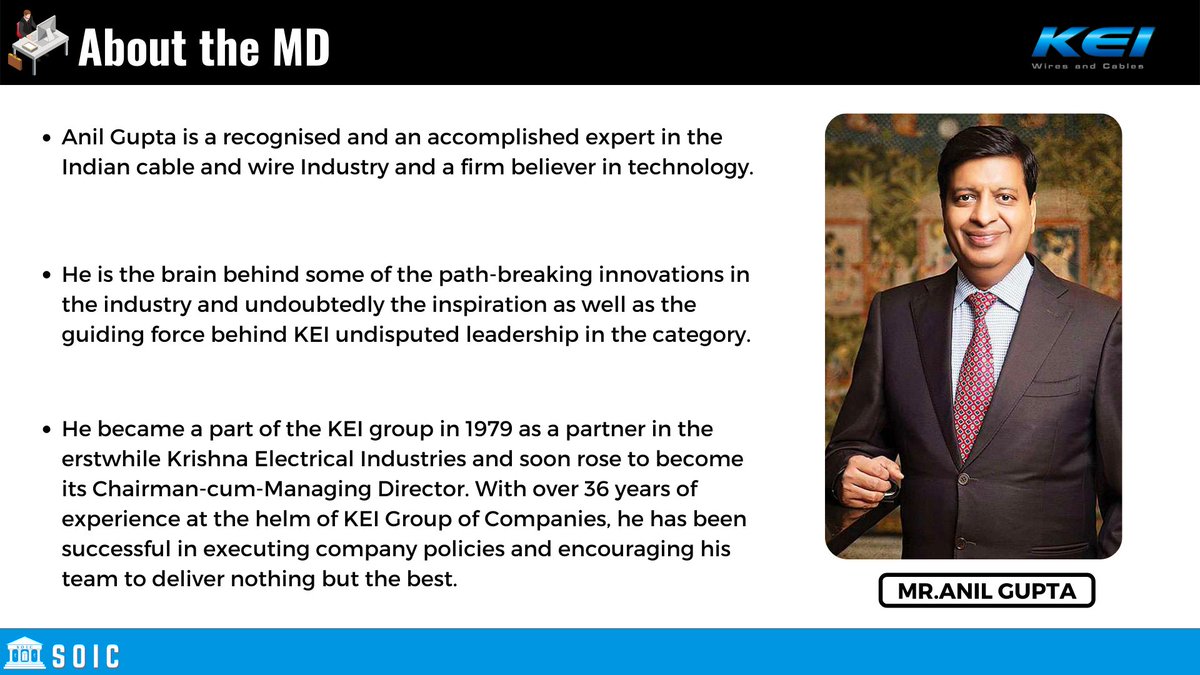

KEI was established in 1968 as a partnership firm. The current MD of the company Mr Anil Gupta became a part of the KEI group in 1979 as a partner in the erstwhile Krishna Electrical Industries and soon became its Chairman-cum-Managing Director.

KEI was established in 1968 as a partnership firm. The current MD of the company Mr Anil Gupta became a part of the KEI group in 1979 as a partner in the erstwhile Krishna Electrical Industries and soon became its Chairman-cum-Managing Director.

The journey of the company🏔️:

They have 5 plants located at different locations in Rajasthan & Silvassa with a total capacity of 128,600 kms for cables, 1,117,000 kms for wires & 7,200 MT capacity for stainless steel wires.

They have 5 plants located at different locations in Rajasthan & Silvassa with a total capacity of 128,600 kms for cables, 1,117,000 kms for wires & 7,200 MT capacity for stainless steel wires.

The company operates in 3 segments & revenue mix from the same is as follows:

➡️Institutional Business: 51%

➡️Retail: 34%

➡️Exports: 15%

➡️Institutional Business: 51%

➡️Retail: 34%

➡️Exports: 15%

In Institutional business, they supply to various EPC companies, construction companies, metro projects & government projects.🏗️🧱

Retail business is their B2C business in which they supply building wires.🔌

Retail business is their B2C business in which they supply building wires.🔌

Let’s dig deeper into Institutional Business🤿:

This segment can further be segregated into:

➡️EHV Business (Extra High Voltage)

➡️Engineering Procurement & Construction

This segment can further be segregated into:

➡️EHV Business (Extra High Voltage)

➡️Engineering Procurement & Construction

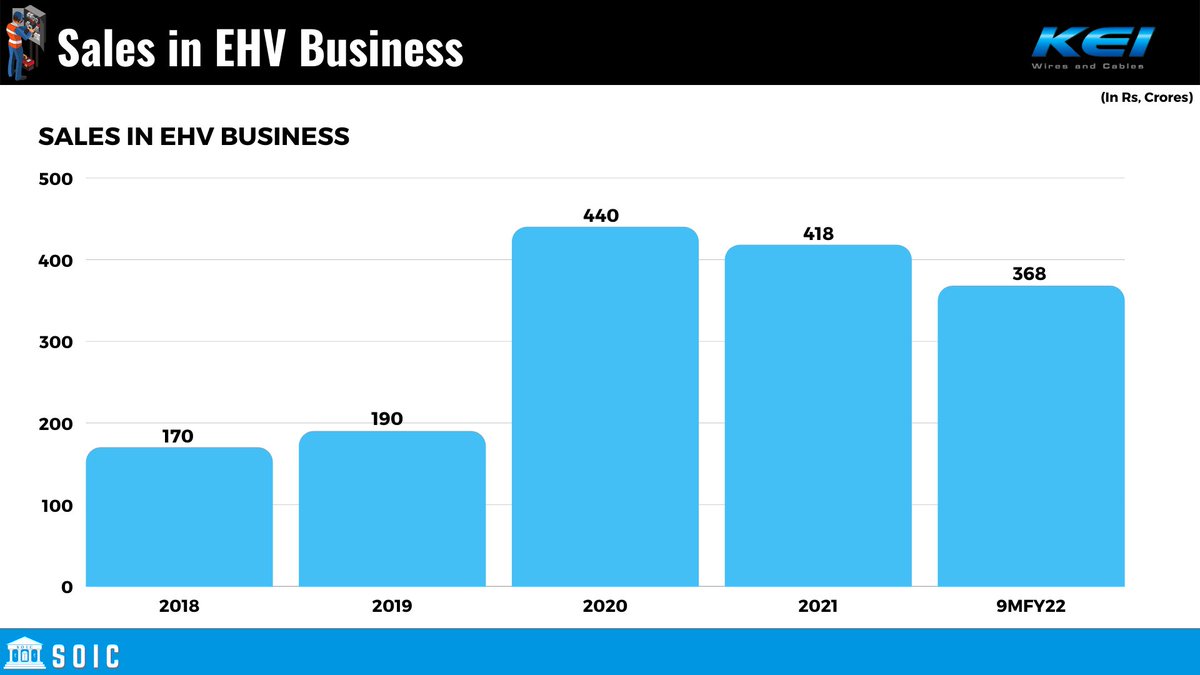

EHV Business:

EHV cables are used for underground power transmission lines. KEI is one of the few manufacturers of EHV Cables.🔌⚡️

In India, it is a duopolistic segment, with imports fulfilling the supplies. Universal cables is the only player apart from KEI.

EHV cables are used for underground power transmission lines. KEI is one of the few manufacturers of EHV Cables.🔌⚡️

In India, it is a duopolistic segment, with imports fulfilling the supplies. Universal cables is the only player apart from KEI.

So there is a huge runway for growth here. There are entry barriers, it takes at least 8 years for the new entrants to enter the market.🏔️

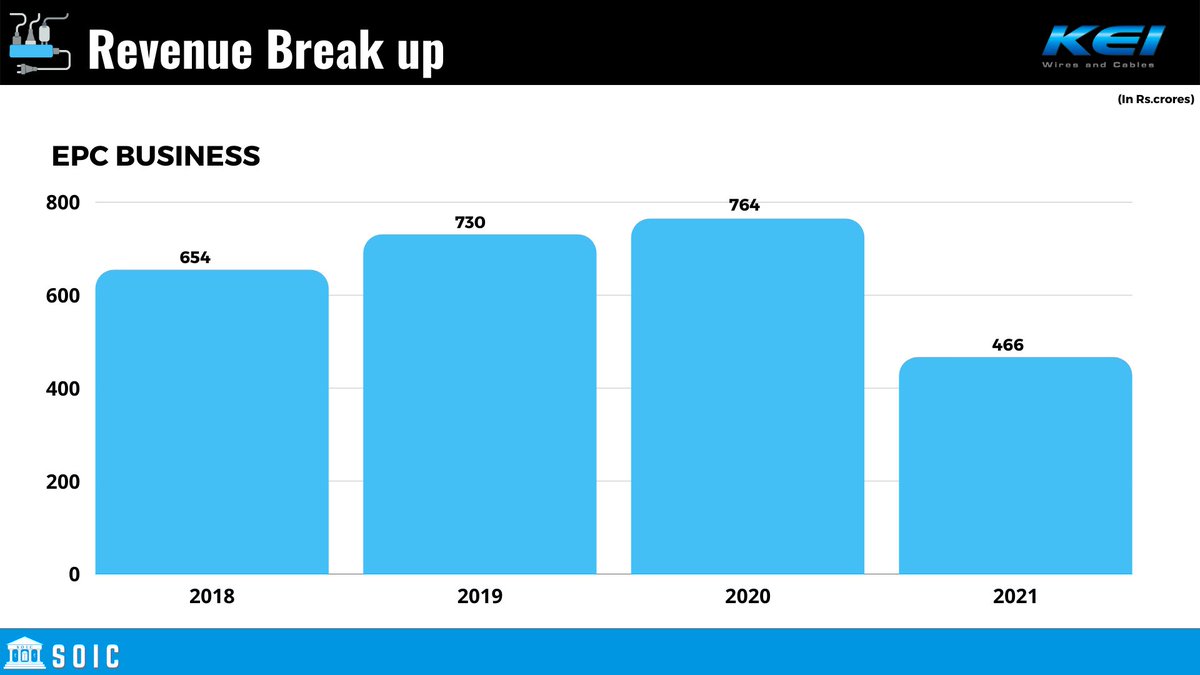

Engineering Procurement & Construction (EPC) Business: In this segment KEI helps in the process of construction and engineering of the whole project. 🏗️

As per the management, they want to degrow this section as there are various issues in this segment major being the long working capital cycle and retention money. Management has guided to restrict the EPC business to 10% of total revenue.🧱🏗️

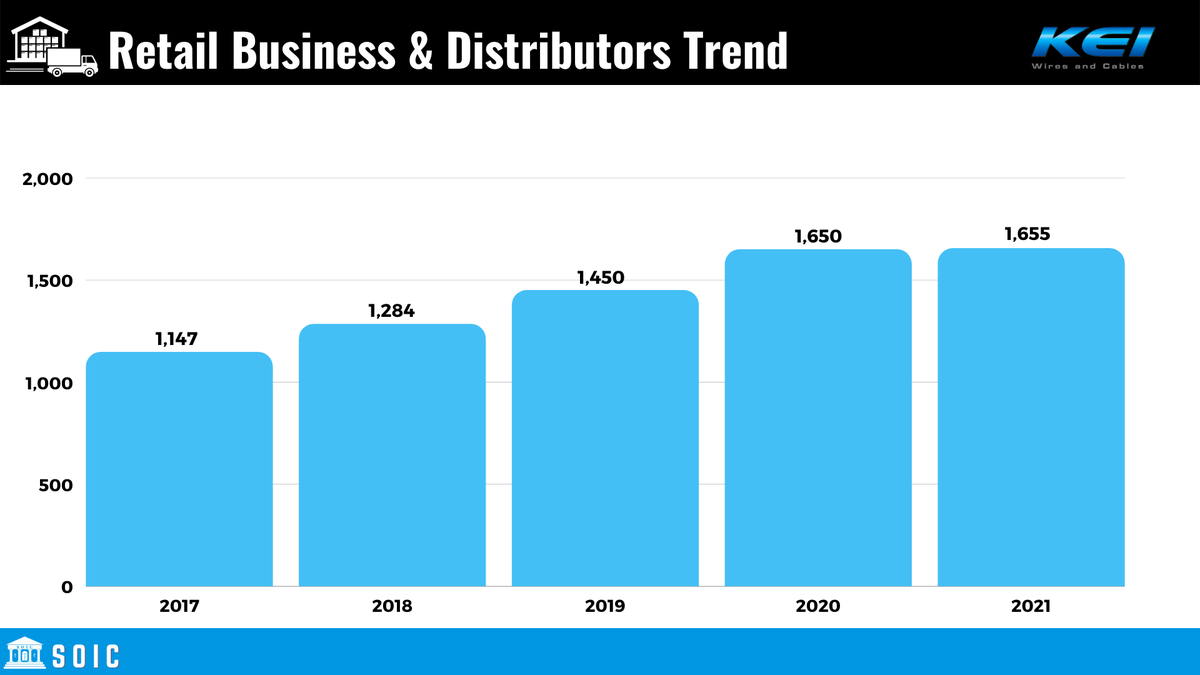

Now let's have a look at its Retail business⚡️:

In retail business they sell W&C via distributor & retailers channels, the management is guiding to take this segment to around 50% from current levels of 34% of their revenue.

In retail business they sell W&C via distributor & retailers channels, the management is guiding to take this segment to around 50% from current levels of 34% of their revenue.

🔌The major is because of 3 reasons:

1⃣Working capital-light

2⃣Better Margins

3⃣High ROCE

This segment would be a fast-growing segment for the company with increasing numbers of retailers.

In the next leg of growth for this segment, they will be launching the FMEG products.

1⃣Working capital-light

2⃣Better Margins

3⃣High ROCE

This segment would be a fast-growing segment for the company with increasing numbers of retailers.

In the next leg of growth for this segment, they will be launching the FMEG products.

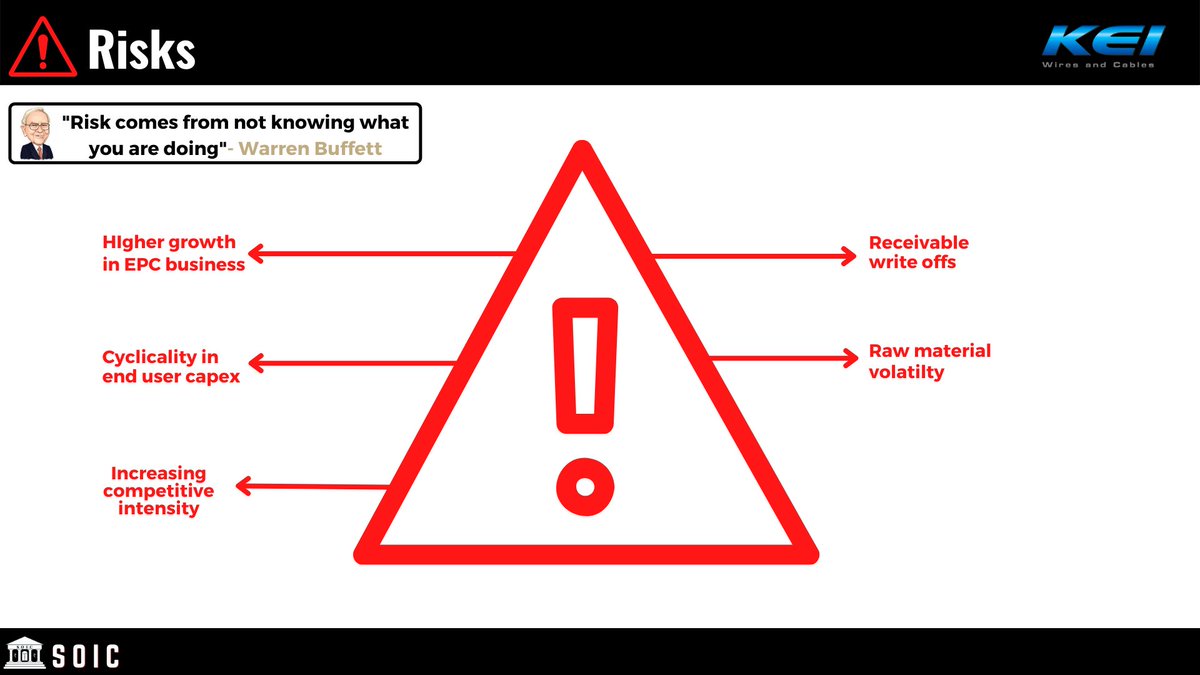

🚨Anti-Thesis and Risks:

▶️Risk of raw material volatility: The key RM for the company is copper which consists of 40% of cost, so any sharp rise in commodity prices will lead to margin deterioration if the company is not able to pass on the cost.

▶️Risk of raw material volatility: The key RM for the company is copper which consists of 40% of cost, so any sharp rise in commodity prices will lead to margin deterioration if the company is not able to pass on the cost.

▶️Higher growth in EPC segment: As discussed above, management is guiding to decrease the share of EPC business but if this segment grows then will lead to poor return ratios.

You can watch the detailed 🤿 Deep Dive into it on our YouTube channel:

youtube.com

youtube.com

Disclaimer:- Thread is only meant to teach you about how the industry works and why this can a proxy to green energy. Not an investment advice, take the Analysis and build independent conviction.

The authors do not hold the stock.

The authors do not hold the stock.

I teach a course on Fundamental analysis and this time I am covering a very important topic in investing.

How to do forensic analysis and avoid fraudulent companies with our accounting scores for more than 250 companies!

Link to register:-

pages.razorpay.com

How to do forensic analysis and avoid fraudulent companies with our accounting scores for more than 250 companies!

Link to register:-

pages.razorpay.com

Loading suggestions...