1/ Intro to Stock-Bond Correlations

You often hear about the 60/40 Portfolio as a strategy for investors to achieve diversification.

But can stocks and bonds fall at the same time? Are the correlations truly negative?

Let's examine why this is so important now 🧵👇

You often hear about the 60/40 Portfolio as a strategy for investors to achieve diversification.

But can stocks and bonds fall at the same time? Are the correlations truly negative?

Let's examine why this is so important now 🧵👇

2/ The 60/40 Portfolio.

This is a popular strategy where investors allocate roughly 60% to equities and 40% to fixed-income.

This strategy of asset-allocation may reduce volatility, assuming that stocks and bonds are negatively correlated.

We will assess this assumption.

This is a popular strategy where investors allocate roughly 60% to equities and 40% to fixed-income.

This strategy of asset-allocation may reduce volatility, assuming that stocks and bonds are negatively correlated.

We will assess this assumption.

3/ Quick Refresher on Correlations.

Positive Correlation: Asset prices tend to move together.

Negative Correlation: Asset prices tend to move in opposite directions.

Owning uncorrelated or negatively correlated assets can reduce volatility.

Positive Correlation: Asset prices tend to move together.

Negative Correlation: Asset prices tend to move in opposite directions.

Owning uncorrelated or negatively correlated assets can reduce volatility.

4/ So... how are stocks and bonds correlated?

There isn't a completely straightforward answer to this question.

However, history can teach us something about how these two asset classes are related.

Let's track correlations over time.

There isn't a completely straightforward answer to this question.

However, history can teach us something about how these two asset classes are related.

Let's track correlations over time.

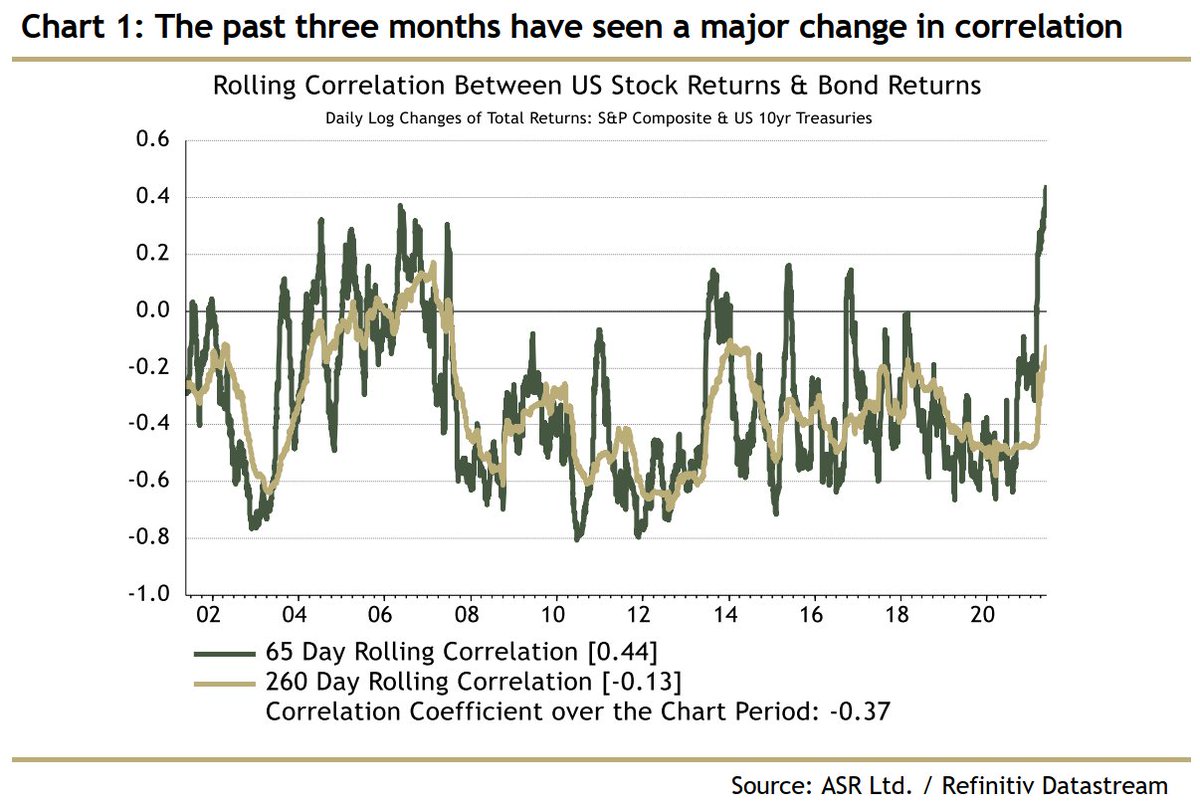

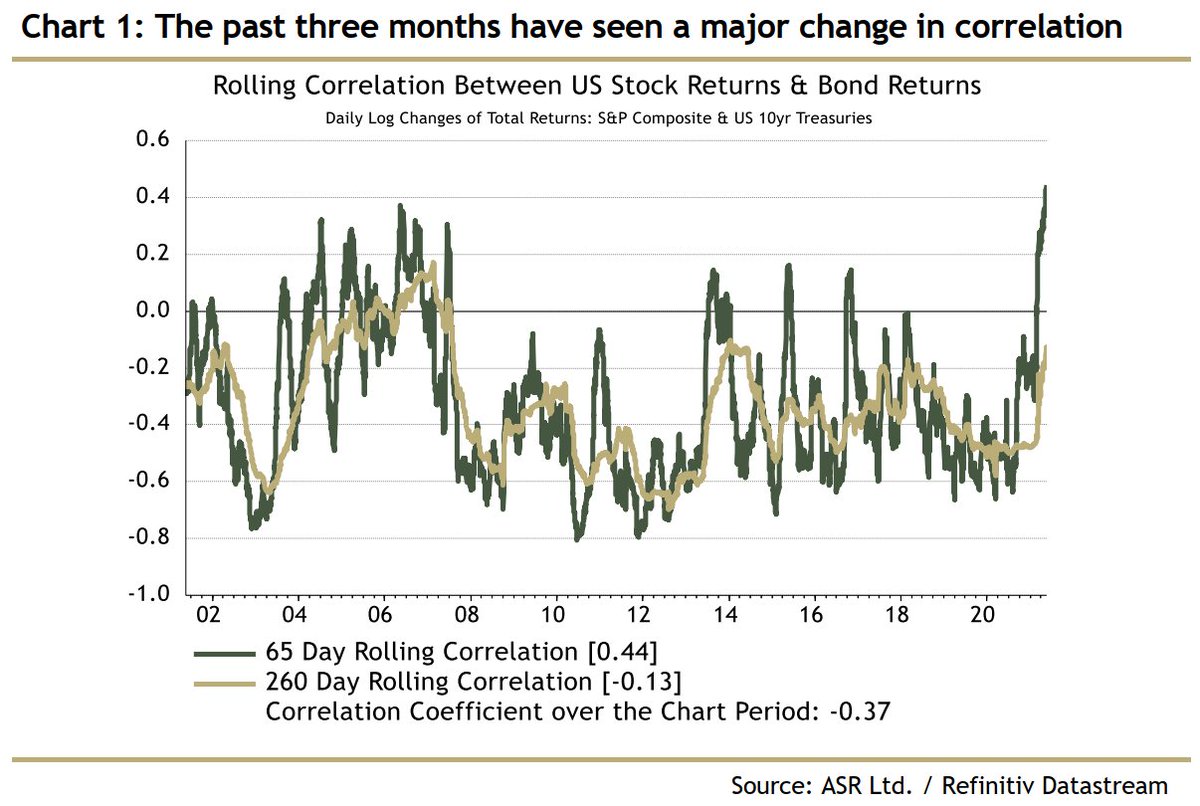

5/ Looking back 20 years.

The chart below tracks the correlation between returns on the S&P and US 10 Year Treasuries.

For the most part, correlations during this period were generally negative. The 2020 spike will make sense later on.

Let's zoom out a little more.

The chart below tracks the correlation between returns on the S&P and US 10 Year Treasuries.

For the most part, correlations during this period were generally negative. The 2020 spike will make sense later on.

Let's zoom out a little more.

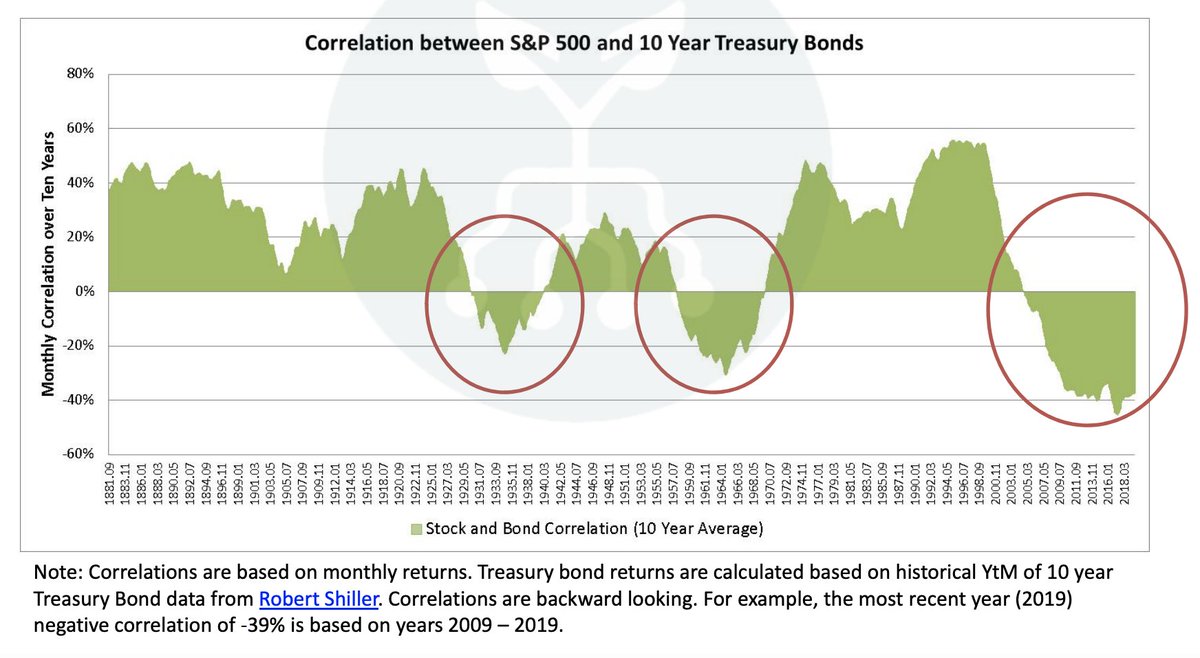

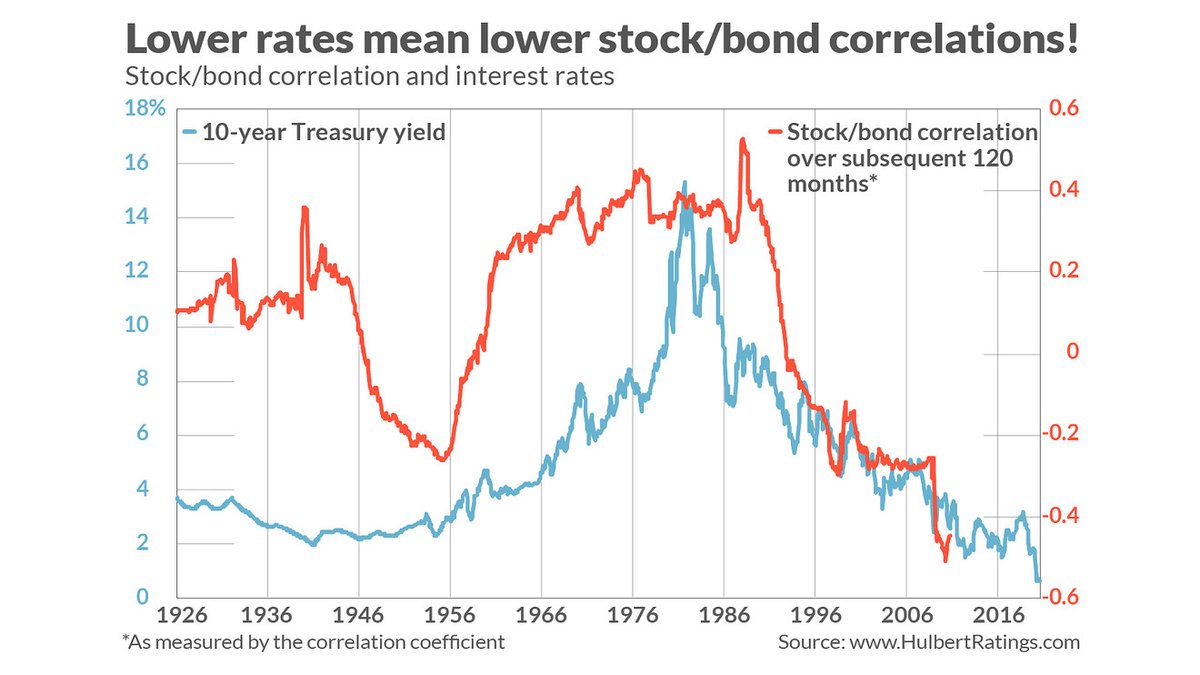

6/ Zoom out and we can see that stock-bond correlations change over time.

Correlations have been largely positive over the past 150 years.

The exceptions are the 1930s, 1960s and the 2000s.

Details on how these correlations were calculated will be linked at the end.

Correlations have been largely positive over the past 150 years.

The exceptions are the 1930s, 1960s and the 2000s.

Details on how these correlations were calculated will be linked at the end.

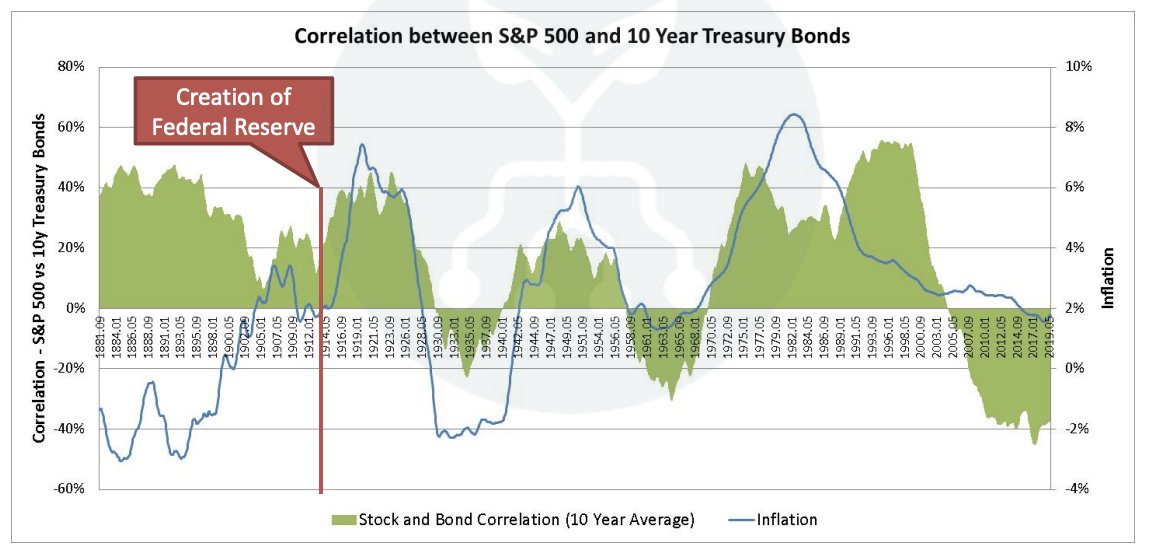

7/ What determines whether correlations are positive or negative?

Inflation seems to be the driver.

Periods of low AND predictable inflation overlap with periods of negative correlations.

One exception is the 1980s, where inflation fell rapidly. This was NOT predictable.

Inflation seems to be the driver.

Periods of low AND predictable inflation overlap with periods of negative correlations.

One exception is the 1980s, where inflation fell rapidly. This was NOT predictable.

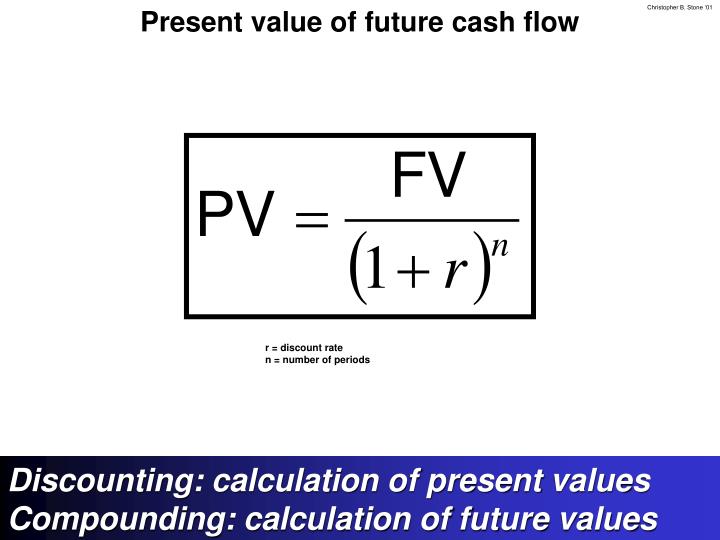

8/ Why inflation?

Cash generating financial assets (such as stocks and bonds) can be valued by discounting future cash flows.

The discount rate is a shared risk factor.

PV = Present Value

FV = Future Value

r = Discount Rate

A higher discount rate leads to a lower PV.

Cash generating financial assets (such as stocks and bonds) can be valued by discounting future cash flows.

The discount rate is a shared risk factor.

PV = Present Value

FV = Future Value

r = Discount Rate

A higher discount rate leads to a lower PV.

9/ Discount Rate.

The Discount Rate is a function of the Benchmark Rate + Risk Premium.

Benchmark Rate: Can be thought of as a "risk-free" rate such as sovereign bond yields.

Risk Premium: Expected rate of return in excess of the risk-free rate.

The Discount Rate is a function of the Benchmark Rate + Risk Premium.

Benchmark Rate: Can be thought of as a "risk-free" rate such as sovereign bond yields.

Risk Premium: Expected rate of return in excess of the risk-free rate.

10/ When inflation is rising, there is an increase in the perception of what the discount rate on future cashflows should be.

As a result, valuations in general go down for stocks and bonds (and anything that produces cashflows).

As a result, valuations in general go down for stocks and bonds (and anything that produces cashflows).

11/ If the concept of Time Value of Money is totally new to you, I recommend you check out @SahilBloom's Inflation 101:

Ok - back to correlation regimes.

Ok - back to correlation regimes.

12/ With low and stable inflation, the volatility in these benchmark rates is lessened - price movements in financial assets are then largely determined by their own unique fundamentals.

Stocks are driven by earnings.

Corporate bonds are driven by credit factors.

Stocks are driven by earnings.

Corporate bonds are driven by credit factors.

13/ All financial assets are tied to benchmark rates.

When rates become less predictable, correlations between financial assets rise.

When rates become less predictable, correlations between financial assets rise.

14/ Are we entering a positive correlation regime?

Recall this chart from earlier.

Correlations shot up in late 2020, likely due to increased inflation prints and greater uncertainty over rising interest rates.

The question is - will this positive correlation persist?

Recall this chart from earlier.

Correlations shot up in late 2020, likely due to increased inflation prints and greater uncertainty over rising interest rates.

The question is - will this positive correlation persist?

15/ Correlation regimes take years and even decades to play out.

We've been in a historically low correlation environment over the last two decades.

Whether we're entering a positive correlation regime is uncertain, but it is a scenario that should be considered.

We've been in a historically low correlation environment over the last two decades.

Whether we're entering a positive correlation regime is uncertain, but it is a scenario that should be considered.

16/ Financial institutions rely heavily on correlation assumptions when managing portfolios to limit risk.

A persistent change in correlations could destabilize models used by banks and hedge funds, leading to asset unwinding and trouble for financial markets.

A persistent change in correlations could destabilize models used by banks and hedge funds, leading to asset unwinding and trouble for financial markets.

17/ I'm not making a forecast on where correlations are headed - simply identifying a possibility.

Depending on your investing goals, you may choose to rethink how you view diversification and risk management.

Depending on your investing goals, you may choose to rethink how you view diversification and risk management.

18/ True Diversification

We don't know what the future will bring, and investors should strive to view future scenarios in probabilities and not certainties.

Explore various asset classes, strategies, geographies and currencies to achieve True Diversification.

We don't know what the future will bring, and investors should strive to view future scenarios in probabilities and not certainties.

Explore various asset classes, strategies, geographies and currencies to achieve True Diversification.

19/ True Diversification is a complex topic, but one to read deeper into depending on your appetite for risk and volatility.

I may write a thread on this topic at a later date, but here's a great introduction from @WEquilCapital on this topic:

intuitecon.com

I may write a thread on this topic at a later date, but here's a great introduction from @WEquilCapital on this topic:

intuitecon.com

20/ Further Research

If you found this topic interesting, you'll enjoy @WEquilCapital's 42 page slide deck on Correlation Regimes.

Link: tinyurl.com

Details of calculations are on the deck.

The publication is a few years old but very relevant today.

If you found this topic interesting, you'll enjoy @WEquilCapital's 42 page slide deck on Correlation Regimes.

Link: tinyurl.com

Details of calculations are on the deck.

The publication is a few years old but very relevant today.

I'll be regularly sharing my notes and research across various topics in finance.

The financial world is complex, and I aim to produce content that is valuable to readers of all levels.

A follow (@vishalinvests), like and retweet are appreciated! 👇

The financial world is complex, and I aim to produce content that is valuable to readers of all levels.

A follow (@vishalinvests), like and retweet are appreciated! 👇

Loading suggestions...