UPI stands for Unified Payments Interface.

It is a payment system that facilitates instantaneous fund transfers between person to person or from person to a merchant, with the help of a smartphone.

UPI integrates multiple bank accounts into a single mobile application. This way it merges several banking features, on one hand, and equip for seamless fund transfer or payments on the other hand.

In April 2016, the UPI system was launched on a pilot basis with 21 member banks. Later, banks started to upload their UPI-enabled apps to Google Play Store in August 2016.

UPI is unique because:

• Users can make quick money transfers 24x7x365

• Users can access multiple bank accounts in one application only

• QR code facilitates on-the-spot transfer to merchants

• No need to carry more cash

• Enhanced security through virtual address as users doesn’t have to share their personal or bank details.

• Single click authentication or confirmation.

• Users can raise disputes/queries from the App itself

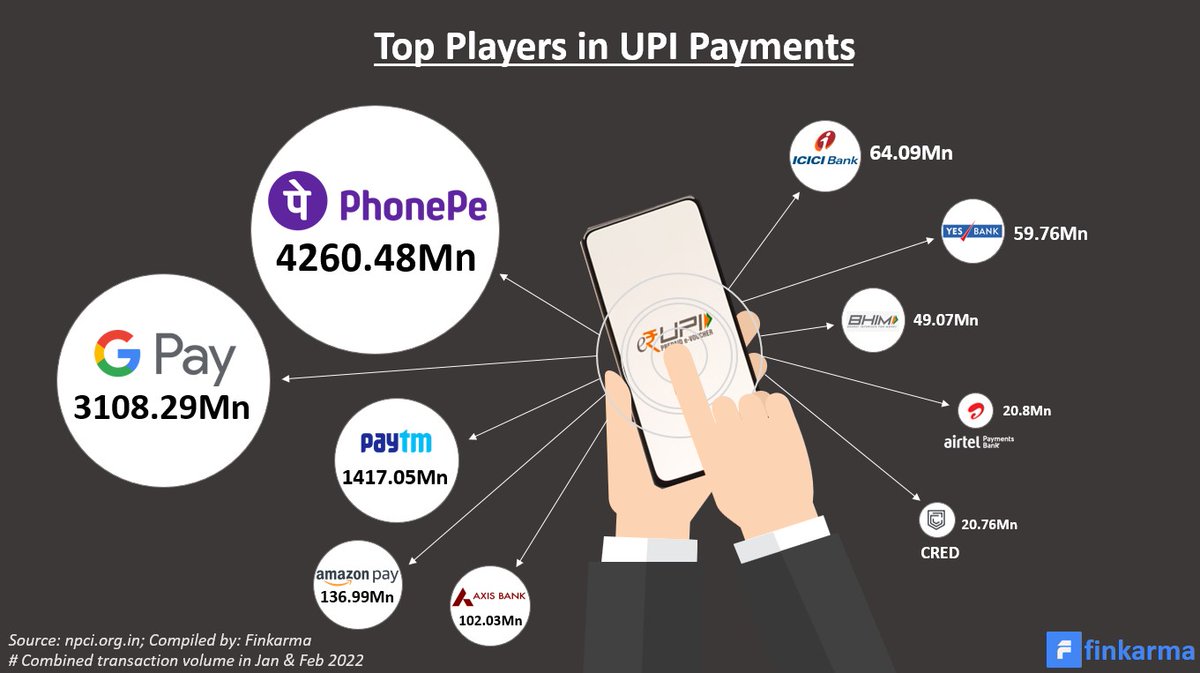

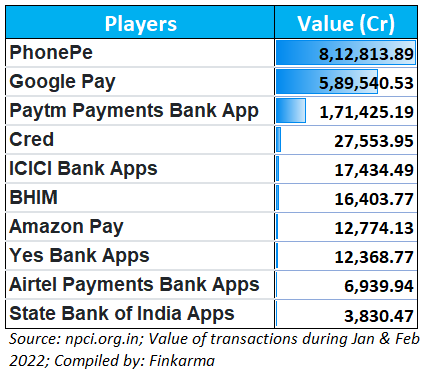

As per the latest data (Jan and Feb 2022 combined), in terms of volume (total number of transactions through UPI Apps), PhonePe occupies the first place. GooglePay, PayTM, are at number 2 and 3 resp.

However, Cred and ICICI Bank jump to place 4 and 5 resp. See top 10 by transaction value below.

Besides the benefits discussed above, UPI has helped small and medium-sized business owners as well as their customers, as a large number of UPI transactions value Rs200 or less (as per npci data).

I bet if they had to pay the same in cash, it would have cost them Rs148 (or even 150) and Rs500 resp.

They need not buy card swiping machines which would have cost them Rs10,000 or more.

Digital payments are faster and hassle-free for both of them.

If you like this thread then do share it with your friends. And yes,

Which of the above Apps do you use? Plz, mention it in the comment section.

More from this author

Breakout (BO) is a very popular technique among traders and investors who like to make their living out of stock market If you love to trade momentum...

Understand OPTIONS’ BASICS AND THETA CONCEPT “Time eats all the premium but not in all the cases” A detailed thread 🧵

Decoding your Favourite indicators ~🧵 1/ MACD The Moving Average Convergence Divergence (MACD) is a popular indicator among retail traders. It can b...

"You do not need more indicators. You need to know more about the ones you are currently using" A Moving average is one of the most widely used indic...

Recent Threads

wont tag because its a nothingburger. i think richy really hates himself more than anything else in the world and struggles with friendship because of...

🇧🇦 Bosnia have released an official World Cup song and it's an absolute BANGER. 💙💛 🎵 "I AM FROM BOSNIA, TAKE ME TO AMERICA." https://t.co/yKZs5r7vBw

New in Claude Code (research preview): dynamic workflows. Claude writes an orchestration script on the fly, then spins up a large fleet of coordinate...

What if you could take three completely different model families… and distill them into one tiny model? 🤯 📜 Paper: https://t.co/K2iKD4xFvp MOPD (Mul...

🇺🇸💥🇮🇱 Congress Just Voted to Fuse the U.S. Military With Israel’s — and Buried It on Page 847 So You Wouldn’t Notice ☠️ Section 224 of the $1.15 Tril...

Police running down harassing this guy over a post on Facebook about protesting Data Centers. https://t.co/mfqEKnGwld

Popular Threads

Ware County, Ga has broken the Dominion algorithm: Using sequestered Dominion Equipment, Ware County ran a equal number of Trump votes and Biden vote...

Winning the Chevening Scholarship + 12 Strong Samples of the Chevening Essay There are four important Essays on the Chevening Scholarship application...

Please retweet and share if you support my and others' vaccine injury recoveries. https://t.co/y8xNWwRUOO

Top 20 Players with the most goals + assists in football history, only players with assists available (following the Opta criteria for assists) Seaso...

ICT’s 2022 Mentorship Summarized: https://t.co/zFJCgIfDAR

The ICT Mentorship Core Content Month 1 Summarized: https://t.co/6tXJxPMDhm