There is lot of buzz in Lamination industry(Greenlam/Greenpanel/Rushil Decor & Stylam)

3 key RMs used in lamination process are Paper, Phenol resin (made from phenol) & Melamine resin.

These stks should have margin pressure as the prices of paper & phenol were high in Q4

1/n

3 key RMs used in lamination process are Paper, Phenol resin (made from phenol) & Melamine resin.

These stks should have margin pressure as the prices of paper & phenol were high in Q4

1/n

Lats week private equity player Lighthouse Funds has offloaded 2-2.5% & Abakkus (S. Singhania) has picked it up thus creating buzz in the market

I did quick study of the business & it sounds interesting (will share why in a min) but lets first understand the mfring process

2/n

I did quick study of the business & it sounds interesting (will share why in a min) but lets first understand the mfring process

2/n

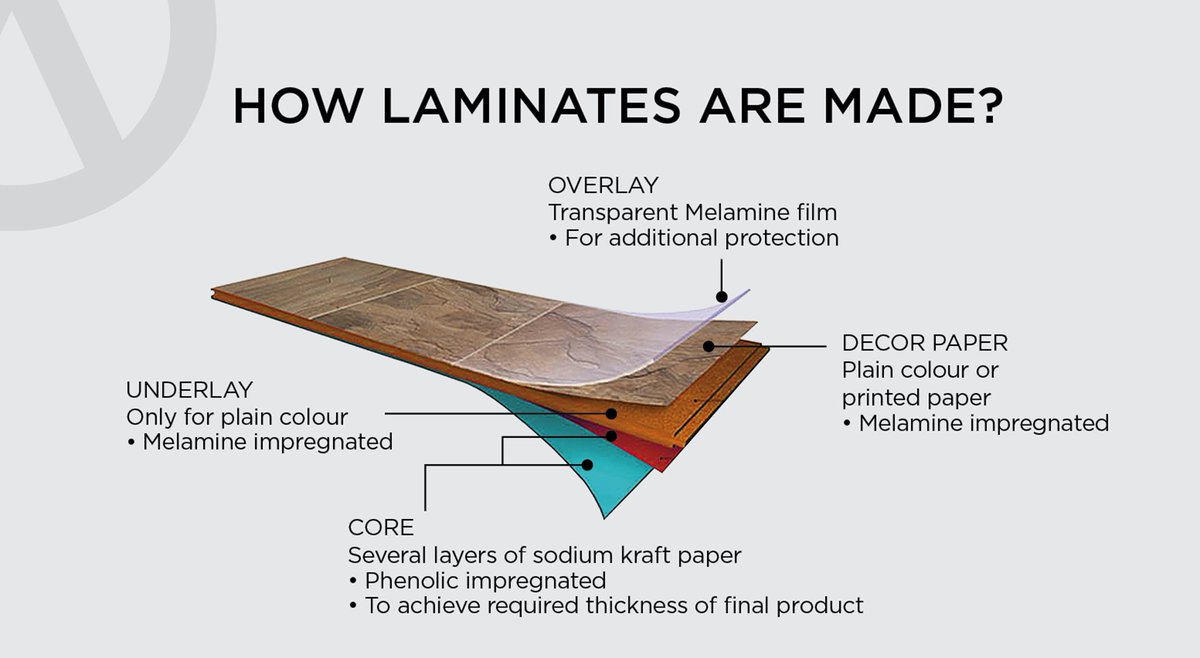

Lamination is the technique of manufacturing a material in multiple layers, so that the composite material achieves improved strength, stability & appearance

Laminates are basically a blend of paper sheets and plastic.

3/n

Laminates are basically a blend of paper sheets and plastic.

3/n

If you see the diagram, it has got four layers (thickness could vary based on the product type).

Lamination process is about combining these four layers into one thru 1) chemical soaking and 2) high-pressure pressing

4/n

Lamination process is about combining these four layers into one thru 1) chemical soaking and 2) high-pressure pressing

4/n

Besides the machinery, Raw Material includes:

1. Semi-transparent sheet (topmost layer)

2. Paper sheets (various layers)

3. Chemicals: Phenolic resin (made from phenol & bottom layer is soaked in this) & Melamine resin(for treating the decorative paper)

5/n

1. Semi-transparent sheet (topmost layer)

2. Paper sheets (various layers)

3. Chemicals: Phenolic resin (made from phenol & bottom layer is soaked in this) & Melamine resin(for treating the decorative paper)

5/n

Essentially, the paper and phenol are the RM cost drivers besides repairs and inflation of machinery.

Manufacturing process is about having cutting-edge machinery such as Drying and Cooling Machines, Cutting Machines, Machinery for Hydraulic Press & Sanding Machines.

6/n

Manufacturing process is about having cutting-edge machinery such as Drying and Cooling Machines, Cutting Machines, Machinery for Hydraulic Press & Sanding Machines.

6/n

Mfring process: Glance

1)Soaking respective sheets in Phenolic & Melamine resins

2)Drying the sheets to make them stiff & brittle

3)Hard press the sheets together under high pressure & temp

4)Sanding the non-decorative side (which is glued to plywood or other base materials)

8/n

1)Soaking respective sheets in Phenolic & Melamine resins

2)Drying the sheets to make them stiff & brittle

3)Hard press the sheets together under high pressure & temp

4)Sanding the non-decorative side (which is glued to plywood or other base materials)

8/n

Now that we understand the manufacturing process and raw materials needed, let me share why I liked Stylam.

I wont write essays elaborating, rather will share few numbers about production capacity, debt and their future plans

9/n

I wont write essays elaborating, rather will share few numbers about production capacity, debt and their future plans

9/n

Production capacity (million sheets/annum)

FY22 - 15.5

FY20 - 14.3

FY19 - 11.0

FY12 - 4.8

Debt (in Crs)

Mar 2019 - 189

Mar 2020 - 118

Mar 2021 - 59

Sep 2021 - 51

Dec 2021 - 72

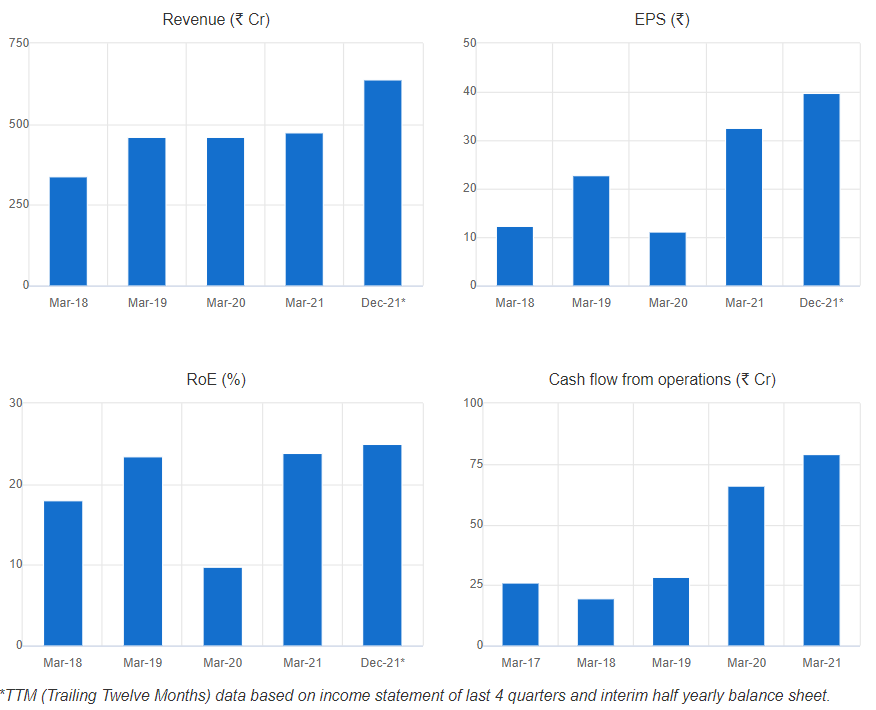

EPS (in Rs)

Mar 2018 - 20

Mar 2019 - 39

Mar 2020 - 19

Mar 2021 - 55

TTM - 68

10/n

FY22 - 15.5

FY20 - 14.3

FY19 - 11.0

FY12 - 4.8

Debt (in Crs)

Mar 2019 - 189

Mar 2020 - 118

Mar 2021 - 59

Sep 2021 - 51

Dec 2021 - 72

EPS (in Rs)

Mar 2018 - 20

Mar 2019 - 39

Mar 2020 - 19

Mar 2021 - 55

TTM - 68

10/n

Vision 2021-2025

1. Increase capacity utilisation on the back of completed expansion (capacities in place to double

revenues).

2. Augment share of value-added products

3. Strengthen domestic presence with a deeper reach and penetration and creation of a strong brand

11/n

1. Increase capacity utilisation on the back of completed expansion (capacities in place to double

revenues).

2. Augment share of value-added products

3. Strengthen domestic presence with a deeper reach and penetration and creation of a strong brand

11/n

Vision 2021-2025

4. Expand coverage across newer exports regions along with increasing business with existing partners.

5. Setting up the Plywood manufacturing facility - Stylam Panels Limited incorporated.

6. To be a net debt free Company FY 22

12/n

4. Expand coverage across newer exports regions along with increasing business with existing partners.

5. Setting up the Plywood manufacturing facility - Stylam Panels Limited incorporated.

6. To be a net debt free Company FY 22

12/n

Why setup plywood facility that has already big players?

1. Laminates are always glued to another material such as Plywood or MDF or PB etc...

2. India is predominantly a Plywood consuming market with the mix of Plywood to other panels (MDF, PB etc.) being about 80:20.

13/n

1. Laminates are always glued to another material such as Plywood or MDF or PB etc...

2. India is predominantly a Plywood consuming market with the mix of Plywood to other panels (MDF, PB etc.) being about 80:20.

13/n

3. The global Plywood market is estimated at $43bn in 2020 & is projected to reach $58bn by 2026

4. The Indian Plywood market is estimated at approximately Rs 25K cr as compared to other panels (MDF, Particle board etc.) which is about Rs 6K cr.

14/n

4. The Indian Plywood market is estimated at approximately Rs 25K cr as compared to other panels (MDF, Particle board etc.) which is about Rs 6K cr.

14/n

So if you are anyway one of the top players in laminates why not manufacture plywood as well as offer "total solution". Now, could it be a slow grower? Maybe yes, but could it be a disaster, I would think "No". So, for me, its a good tick in the box

15/n

15/n

Stylam received an approval from the Board in May 2021 to expand into the Plywood segment with an

estimated outlay of up to INR 60 crores. That's how Stylam Panels Limited was incorporated and is setup

16/n

estimated outlay of up to INR 60 crores. That's how Stylam Panels Limited was incorporated and is setup

16/n

Valuations

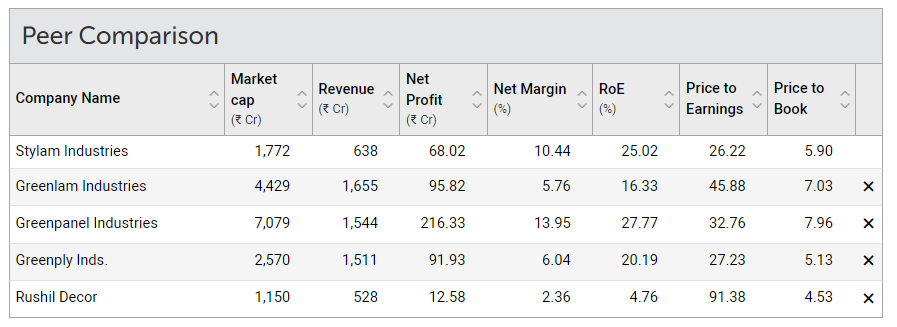

1. Quite reasonable compared against the peer group (see the table) and PEG is < 1

2. Barring Mar' 20, ROE is 20%+ and ROCE 20%+

17/n

1. Quite reasonable compared against the peer group (see the table) and PEG is < 1

2. Barring Mar' 20, ROE is 20%+ and ROCE 20%+

17/n

Risks

1. Key raw materials as I mentioned earlier have gone up and hence there could be margin pressure

2. With crude and logistics up in Q4, would definitely eat up a bit of margins

3. Rus-Ukr war disturbed the economy world over

4. Plywood foray could fail

18/n

1. Key raw materials as I mentioned earlier have gone up and hence there could be margin pressure

2. With crude and logistics up in Q4, would definitely eat up a bit of margins

3. Rus-Ukr war disturbed the economy world over

4. Plywood foray could fail

18/n

Conclusion.

If a company has ambitions to

1. Double it's revenues (mind you they don't need to expand, capacity is already there, they just need to utilize it)

2. Be debt free

3. Become "total player" by offering Ply

it's a good company to study!

19/19

If a company has ambitions to

1. Double it's revenues (mind you they don't need to expand, capacity is already there, they just need to utilize it)

2. Be debt free

3. Become "total player" by offering Ply

it's a good company to study!

19/19

Loading suggestions...