A thread 🧵about a bank whose 2nd name is "Consistency" and it's name is - CITY UNION BANK

Grab a cup of water and relax because it's gonna be a verryyyy long thread.

And don't forget to Re-tweet for wider reach.

Grab a cup of water and relax because it's gonna be a verryyyy long thread.

And don't forget to Re-tweet for wider reach.

HISTORY - City Union Bank is the oldest private sector bank in India, started in 1904 as Kumbakonam Bank in the Tamil Nadu as 'The Kumbakonam Bank Limited'.

It's amongst the very few banks that have survived for over 100 years and has remained profitable.

It's amongst the very few banks that have survived for over 100 years and has remained profitable.

But before we get into the details about the bank, I wanna establish a base that how a bank works and what ratios one should look for.

So banking is a realllly simple business but at the same time it's not.

So banking is a realllly simple business but at the same time it's not.

So the typical function of a bank is, they provide a place for people to keep their money and give that money to someone else. (It's simple right? You take money from one person and give that money to other person)

So how do they make money?

So why would a person deposit it's money in a bank?

Because 1st of all, you can't keep that much amount lying at your house and 2nd of all you get some interest on the money that you've deposited with them.

So why would a person deposit it's money in a bank?

Because 1st of all, you can't keep that much amount lying at your house and 2nd of all you get some interest on the money that you've deposited with them.

And bank is not gonna do that for free right? They use those deposits and give that money to people who need money at an interest.

So let's try to understand it with an example - Bank is giving 4% on deposits & charges 7% on the loans that they've given.

So 7% - 4% = 3%

So let's try to understand it with an example - Bank is giving 4% on deposits & charges 7% on the loans that they've given.

So 7% - 4% = 3%

So this 3% that the bank is earning is known as "Net Interest Margin"

(Interest received - Interest paid/Average assets = Net Interest Margin)

Think of it as Net Profit Margin in any other business.

(Interest received - Interest paid/Average assets = Net Interest Margin)

Think of it as Net Profit Margin in any other business.

So the bank is gonna make 3% after giving the money to the depositors. But wait it can't be that simple right?

What if someone doesn't pay the money back? How will the bank pay the depositors back in case they want to withdraw their money?

What if someone doesn't pay the money back? How will the bank pay the depositors back in case they want to withdraw their money?

That concept is called - "Asset Liability mismatch". Banks need to maintain enough capital that if someday all the depositors decide to withdraw their money so banks can pay them back.(Although such is only theoretically possible, and if happens someday banks block the withdrawal

We have a special name for someone who doesn't pay money back.

They're called NPA or Non Performing Asset.

Suppose if somebody hasn't paid any EMI or the principle amount for 90 days they're classified as NPA.

They're called NPA or Non Performing Asset.

Suppose if somebody hasn't paid any EMI or the principle amount for 90 days they're classified as NPA.

So whenever an account turns NPA, bank have to set aside some money from the profit to make up for the potential loss that can occur due to that account.

So the amount of money that has to be set aside is knows as "Provision".

So the amount of money that has to be set aside is knows as "Provision".

NPA is also of two types - GNPA & NNPA.

So as I said earlier if somebody hasn't paid the interest or principle amount back for 90 days that is known as Gross Non performing Asset or GNPA.

And remember we set aside some money in case of potential loss?

So as I said earlier if somebody hasn't paid the interest or principle amount back for 90 days that is known as Gross Non performing Asset or GNPA.

And remember we set aside some money in case of potential loss?

So when we deduct that money from GNPA, we get NNPA.

GNPA - Provisions = NNPA

So now that've understood what Net Interest Margin, GNPA, NNPA & provision are let's try to understand few other important concepts like - CASA, CRAR, Treasury operations, Provision Coverage Ratio etc

GNPA - Provisions = NNPA

So now that've understood what Net Interest Margin, GNPA, NNPA & provision are let's try to understand few other important concepts like - CASA, CRAR, Treasury operations, Provision Coverage Ratio etc

So 1st let's try to understand what CASA is.

So CASA means = Current Account - Saving Account

So in bank we can open two types of accounts (Broadly speaking) - Savings account or current account.

So CASA means = Current Account - Saving Account

So in bank we can open two types of accounts (Broadly speaking) - Savings account or current account.

Most business people open a current account because there's a continuous flow of money.

And we normal people open saving account to keep the extra money somewhere safe.

There are many other types of accounts in a bank like - Business accounts, Salary accounts etc etc.

And we normal people open saving account to keep the extra money somewhere safe.

There are many other types of accounts in a bank like - Business accounts, Salary accounts etc etc.

So why do banks prefer having high CASA and why CASA ratio the higher the better?

Because on current account banks doesn't have to pay any interest & on saving account they have to say low interest as compared to fixed deposits or bonds and it's stick in nature.

Because on current account banks doesn't have to pay any interest & on saving account they have to say low interest as compared to fixed deposits or bonds and it's stick in nature.

Because most people won't just spend their saving right away, right? So as long as that money is in account, the better.

That's why banks with high CASA ratio can earn more money because their interest out go is lower as compared to a bank who has more raised money

That's why banks with high CASA ratio can earn more money because their interest out go is lower as compared to a bank who has more raised money

through more fixed deposits and Bonds.

In CASA also, the higher the retail deposits the better as compared to a single customer with a large account.

CASA RATIO = CASA DEPOSTIS/TOTAL DEPOSITS (As a thumb rule - Higher the better)

In CASA also, the higher the retail deposits the better as compared to a single customer with a large account.

CASA RATIO = CASA DEPOSTIS/TOTAL DEPOSITS (As a thumb rule - Higher the better)

Then we have SMA 0, SMA1 & SMA 2.

So if you remember I told you about something called NPA, right?

That if someone hasn't paid back the interest or principle amount for more than 90 days, they're qualified as NPA.

But what if someone hasn't paid back for say 30 days or 60 days

So if you remember I told you about something called NPA, right?

That if someone hasn't paid back the interest or principle amount for more than 90 days, they're qualified as NPA.

But what if someone hasn't paid back for say 30 days or 60 days

What do we call them?

Here comes the concept of SMA or Special Mentioned Accounts.

We have SMA 0 - If the stress has remained overdue for 0 - 30 days

SMA 1 - If the stress has remained overdue for 30-60 days

SMA 2 - If the stress has remained overdue for 6- -90 days.

Here comes the concept of SMA or Special Mentioned Accounts.

We have SMA 0 - If the stress has remained overdue for 0 - 30 days

SMA 1 - If the stress has remained overdue for 30-60 days

SMA 2 - If the stress has remained overdue for 6- -90 days.

And one of the most Ratio that one needs to definitely take a look at while analyzing a bank - CAR or Capital Adequacy Ratio

It means - Capital Adequacy Ratio (CAR) is the ratio of a bank’s capital in relation to its risk-weighted assets and current liabilities.

It means - Capital Adequacy Ratio (CAR) is the ratio of a bank’s capital in relation to its risk-weighted assets and current liabilities.

The Capital Adequacy Ratio (CAR) helps make sure banks have enough capital to protect depositors’ money.

I has two components - Tier 1 & Tier 2 capital.

Tier 1 - Tier 1 capital can be used to absorb losses without a bank having to stop its operations.

I has two components - Tier 1 & Tier 2 capital.

Tier 1 - Tier 1 capital can be used to absorb losses without a bank having to stop its operations.

Tier 2 - Tier 2 capital can be accessed by shutting down operations and selling off assets, which is a more extreme type of security against risk.

And the combination of both Tier 1 + Tier 2 should be more than 10.5% including the buffer.

And the combination of both Tier 1 + Tier 2 should be more than 10.5% including the buffer.

How do we calculate CAR?

It's simple - Tier 1 + Tier 2/Risk Weighted Assets = Risk weighted Assets.

You don't need to calculate this, you can find it in their investor presentation.

As for the thumb rule remember one thing, For a bank it should be above 10.5%

It's simple - Tier 1 + Tier 2/Risk Weighted Assets = Risk weighted Assets.

You don't need to calculate this, you can find it in their investor presentation.

As for the thumb rule remember one thing, For a bank it should be above 10.5%

For universal banks (Like hdfc, icici, axis etc) It should be within the range of 15-20%

And for high risk Microfinance NBFCs etc, it should be around 20-25%.

And for high risk Microfinance NBFCs etc, it should be around 20-25%.

Now that we've gone through a mini course on banking. Let's talk about the bank, this thread is originally about.

City Union Bank is a regionally focused bank operating mainly in Tamil Nadu and it's more than 100 years old.

One really interesting thing about this bank is that, in it's history of more than 110 years, it has seen only 7 CEO's till date. Yes you heard it right, Only 7 CEO's

One really interesting thing about this bank is that, in it's history of more than 110 years, it has seen only 7 CEO's till date. Yes you heard it right, Only 7 CEO's

till date.

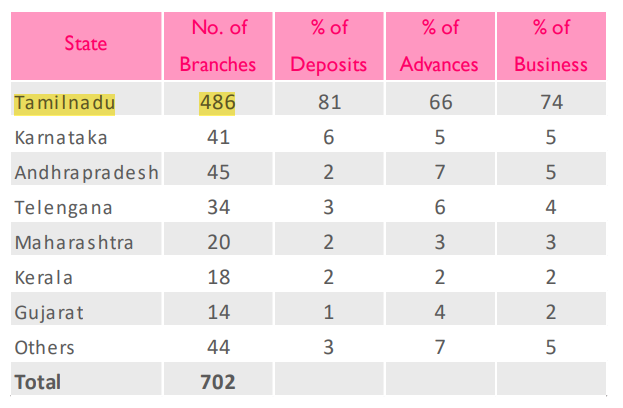

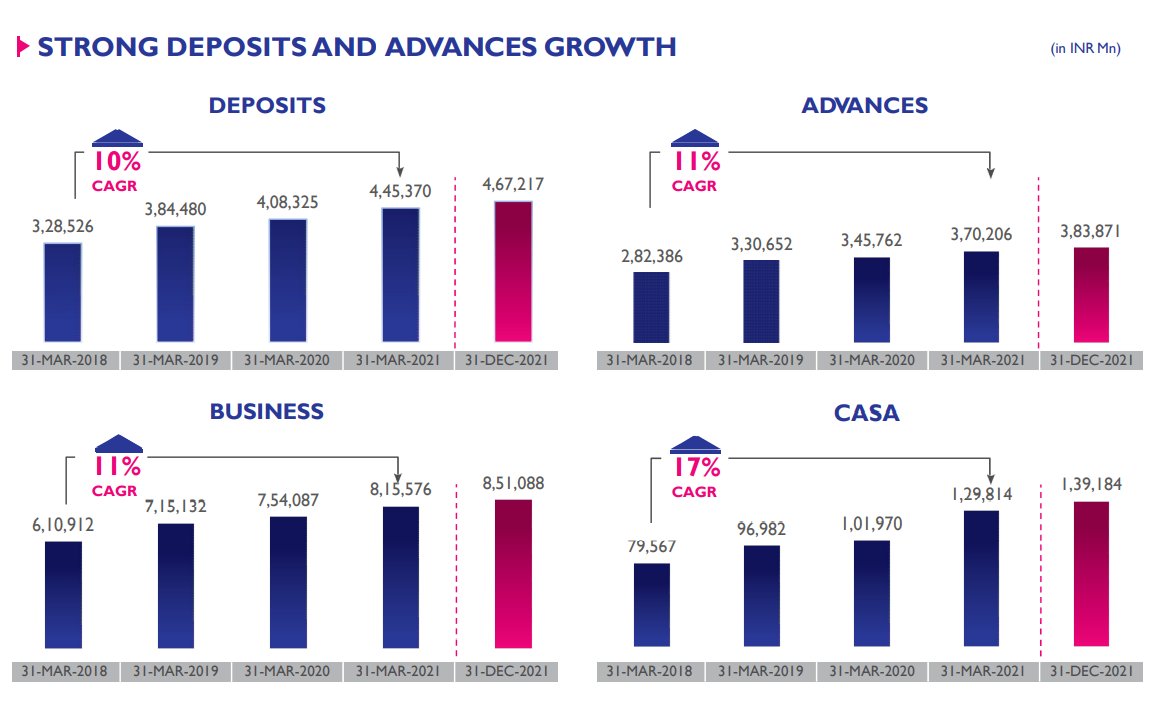

As i said earlier, it's a regionally focused bank with 486 branches out of 700 in just Tamil nadu.

66% Of the advances are from Tamil Nadu

81% Deposits are from Tamil Nadu

(High geographical Concentration)

As i said earlier, it's a regionally focused bank with 486 branches out of 700 in just Tamil nadu.

66% Of the advances are from Tamil Nadu

81% Deposits are from Tamil Nadu

(High geographical Concentration)

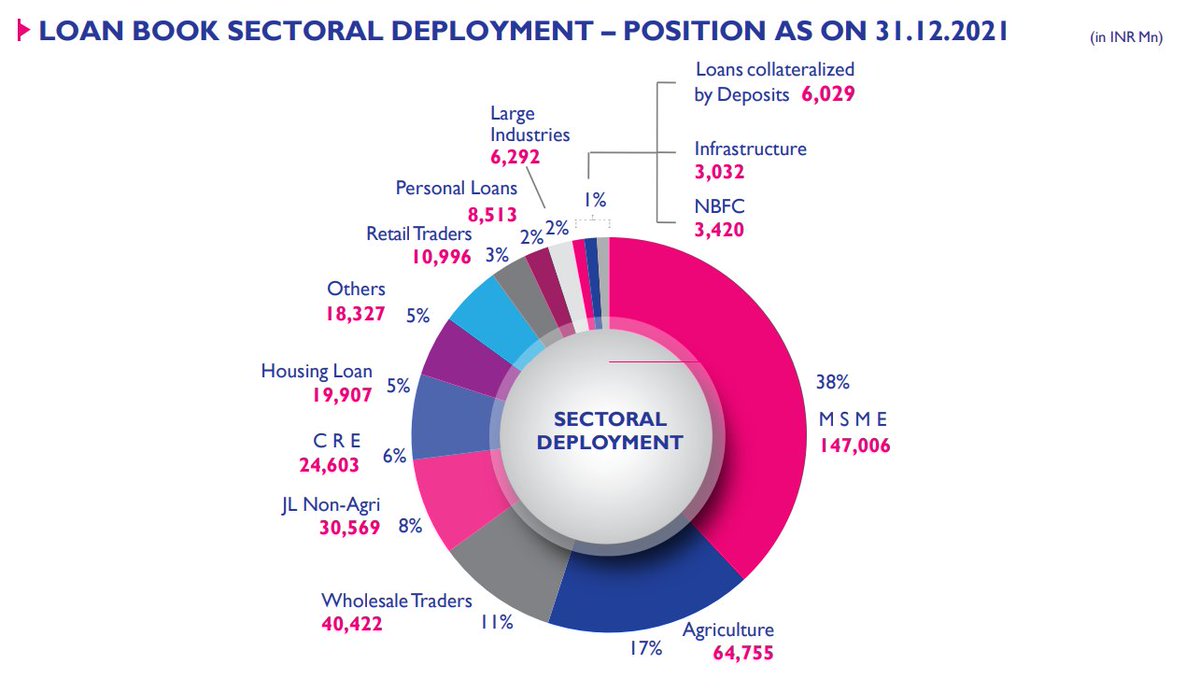

Their loan book is 99% secured and they mainly give loans to MSMEs, Traders and Agriculture loans.

66% loan book is to these segments (High risk as these segments are very vulnerable to economic condition)

38% - MSME

17% - Agriculture

11% - Wholesale Traders

66% loan book is to these segments (High risk as these segments are very vulnerable to economic condition)

38% - MSME

17% - Agriculture

11% - Wholesale Traders

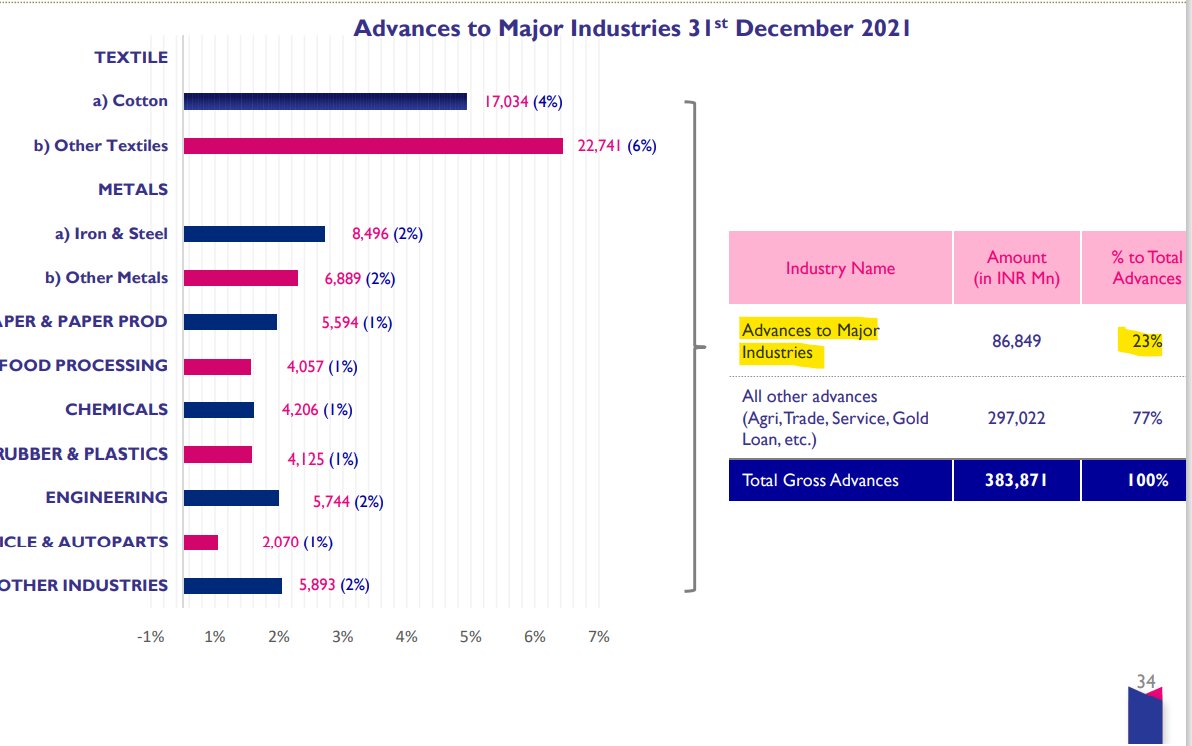

No major industry constitutes for more than 6% of the total advances and of the overall loan book, only 23% advances are to major Industries.

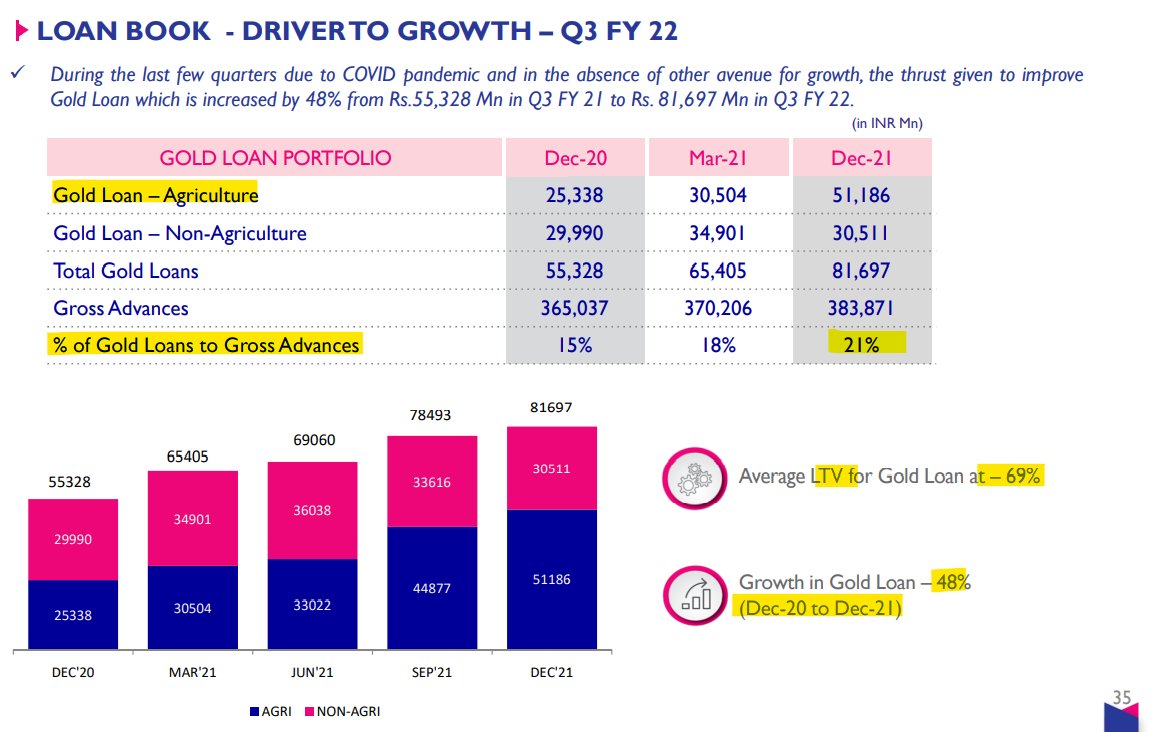

Majority of their Agricultural loans are backed by gold and as of December 2021, Gold loans are 21% of the total advances.

For past one year, gold loans have grown at - 48%

And LTV (Loan to Value) ratio for them is - 69%

For past one year, gold loans have grown at - 48%

And LTV (Loan to Value) ratio for them is - 69%

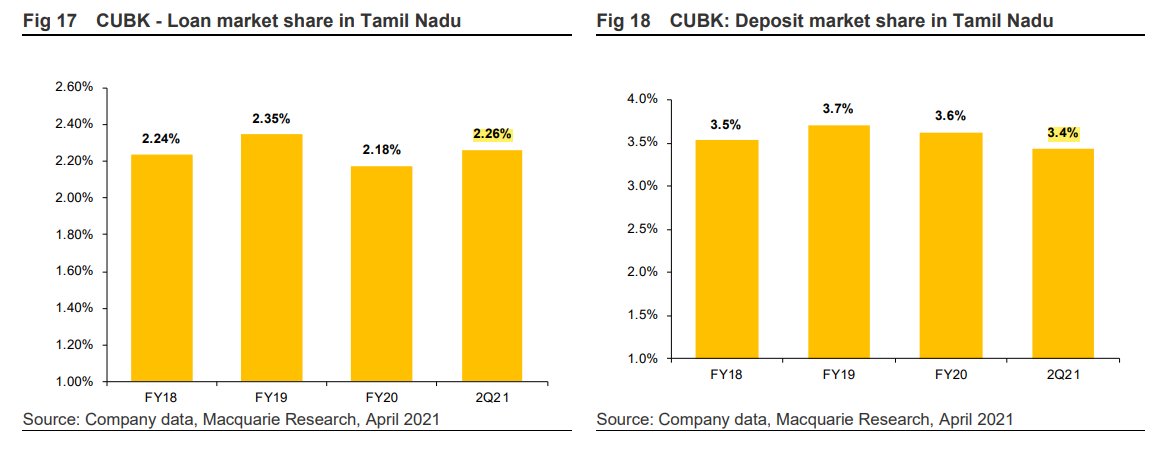

In Tamil Nadu itself they have the opportunity to grow and expand market share.

Their total market share in Tamil Nadu in Advances is 2.26% & in deposits its - 3.4%

Huge Runway for growth in the state itself if they can capture market share.

Their total market share in Tamil Nadu in Advances is 2.26% & in deposits its - 3.4%

Huge Runway for growth in the state itself if they can capture market share.

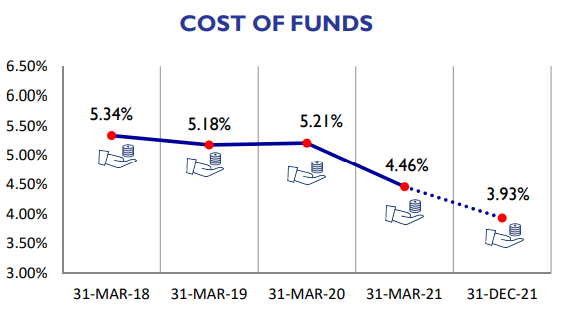

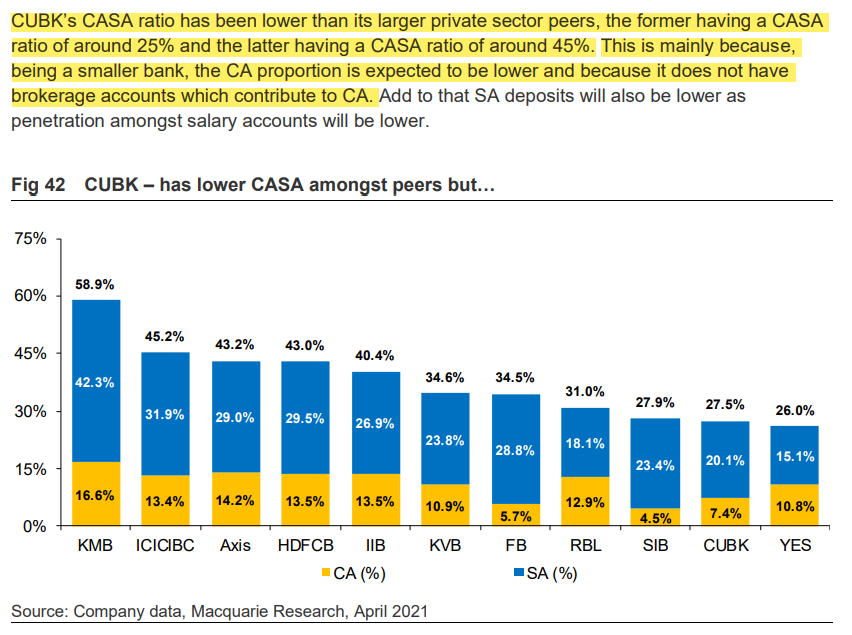

If we take a look at the liability side, their Cost Of Funds has come down significantly to 3.93% (Although lower as compared to HDFC, KOTAK, ICICI)

COF is high as compared to peers due to lower CASA - 32% (In the latest quarterly update, Q4FY22)

COF is high as compared to peers due to lower CASA - 32% (In the latest quarterly update, Q4FY22)

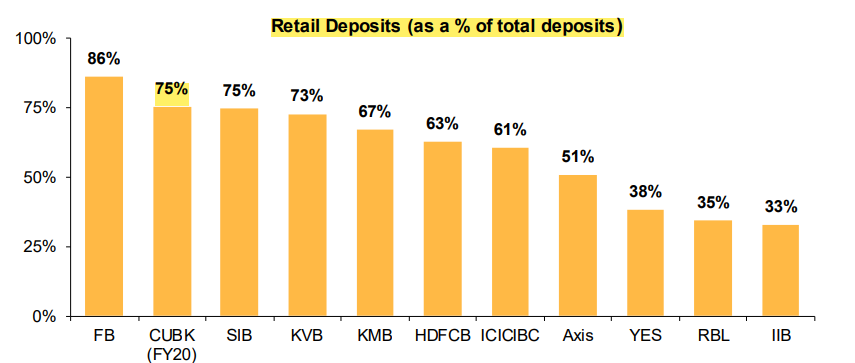

But good thing is, out of the CASA 75% are retail deposits.

Concentration of top 20 Depositos is low around - 9%

and concentration of top 20 Advances is also low around - 5.4%

Concentration of top 20 Depositos is low around - 9%

and concentration of top 20 Advances is also low around - 5.4%

Advances CAGR from 2015-2021 has been around 14% (Which is lower as compared to big banks like Hdfc, ICICI etc)

And since 2018 it has been around 11%

And since 2018 it has been around 11%

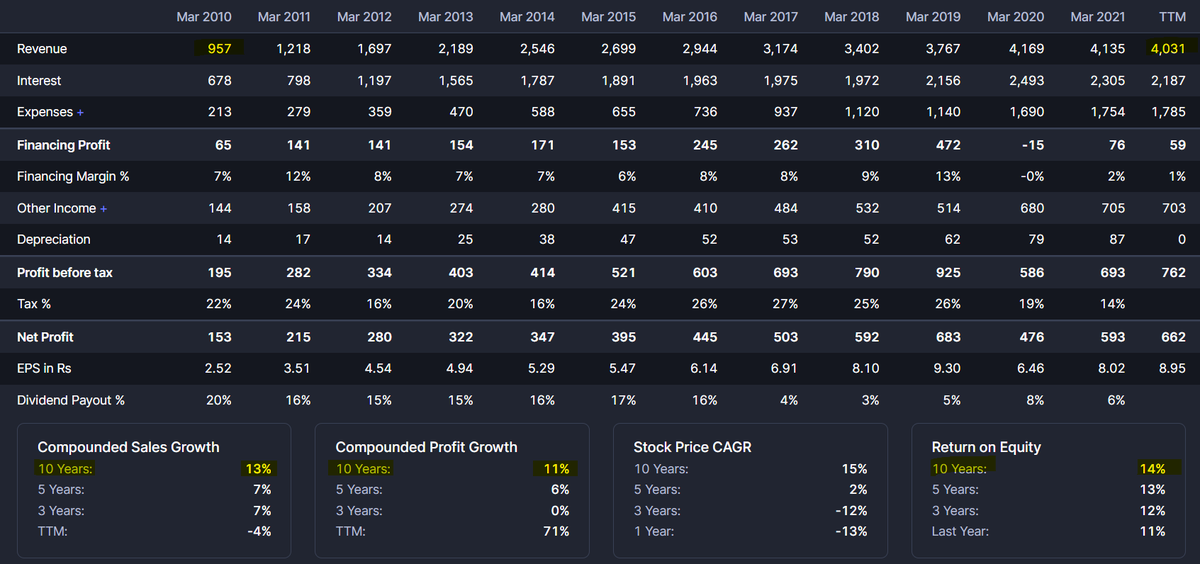

If we take a look at the financials, Last 10 years topline growth has been around 14% (Similar to loan book growth) and bottomline has grown at 11% CAGR.

The has successfully maintained ROE of 14% from past 10 years, even in the downcycle.

The has successfully maintained ROE of 14% from past 10 years, even in the downcycle.

But since covid, the situation has not been that great.

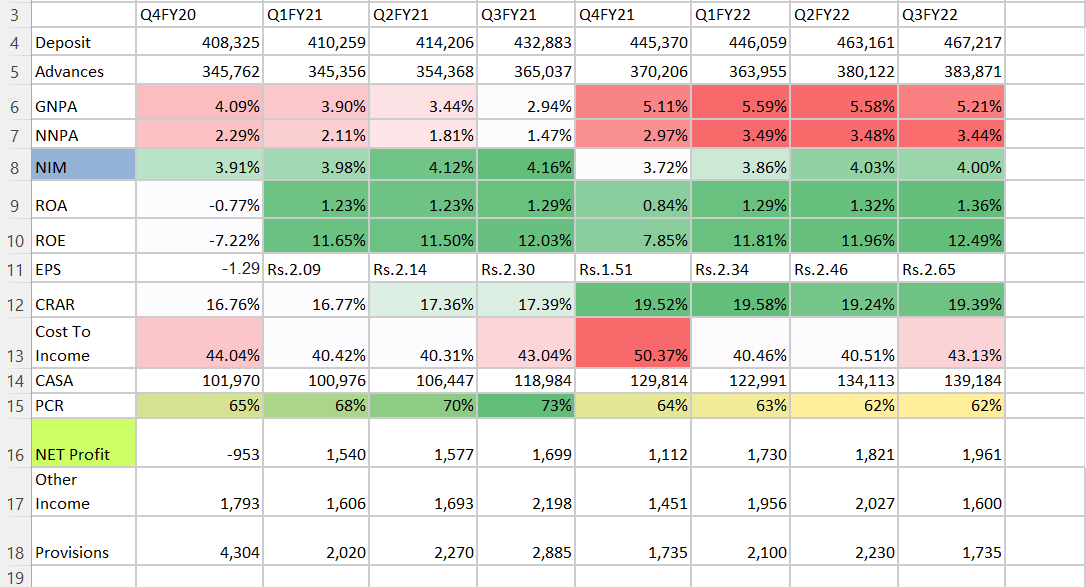

Deposits grew from 40k Cr in Q4 FY20 to 46K Cr in Q3FY22

Advances grew from 34k Cr to 38K Cr.

NIMs have remained stable around 4%

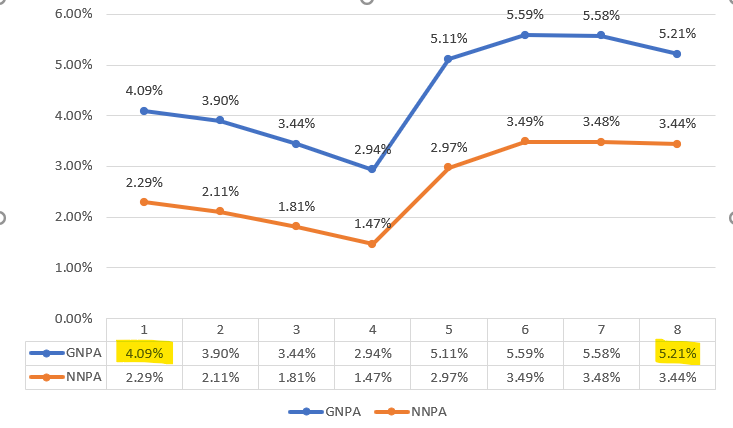

NPA shot up from 3% to >5%.

ROE dipped to 10-11%

ROA has been below 1.5%

Deposits grew from 40k Cr in Q4 FY20 to 46K Cr in Q3FY22

Advances grew from 34k Cr to 38K Cr.

NIMs have remained stable around 4%

NPA shot up from 3% to >5%.

ROE dipped to 10-11%

ROA has been below 1.5%

After the Covid fall, the share price has been laggard and that is mainly due to this sudden rise in NPA.

But after hitting a high of 5.59% in Q1FY22, NPAs have been coming down as thing are getting stable.

But after hitting a high of 5.59% in Q1FY22, NPAs have been coming down as thing are getting stable.

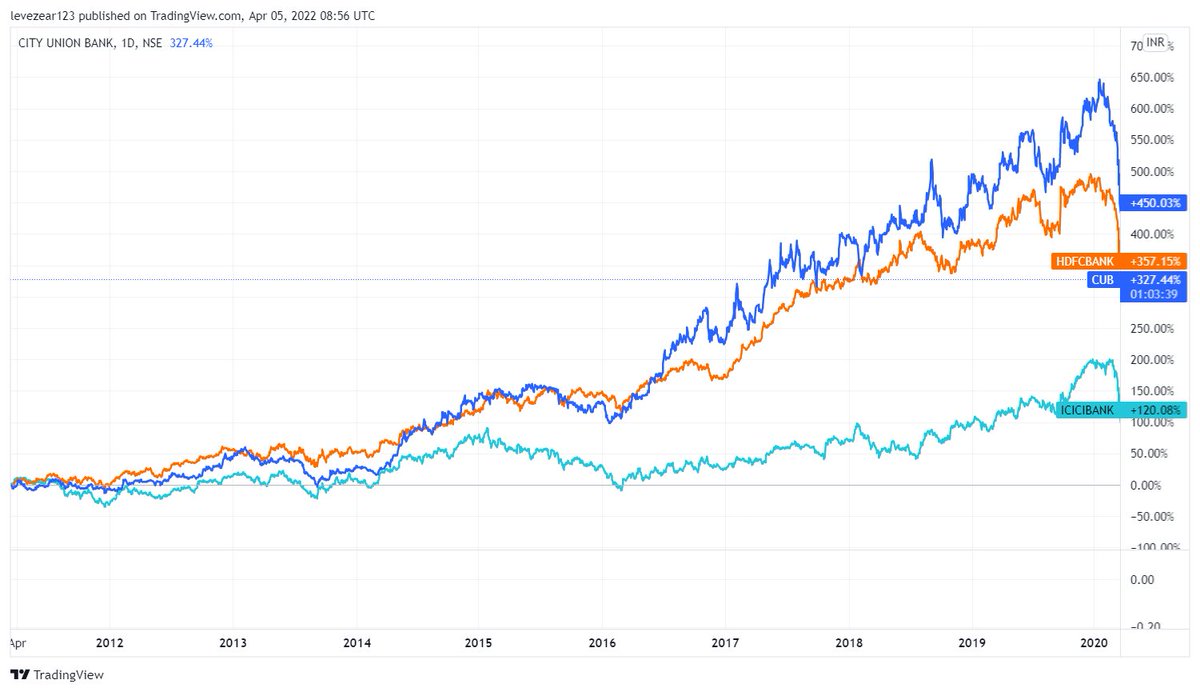

Before Covid has been a great wealth creator. Has outperformed HDFC Bank & ICIC Bank in terms of returns. Why?

- Have maintained ROA of > 1.5% from 2010-2020

- ROE >14%

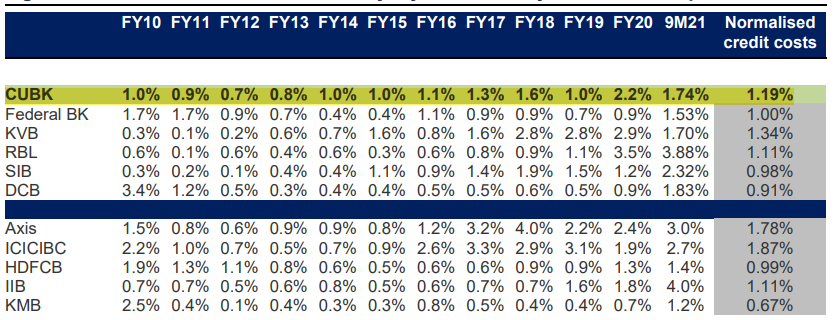

- Around 1-1.2% Credit Cost ( Even after giving high risk loans like MSME & Agriculture Loans)

- Have maintained ROA of > 1.5% from 2010-2020

- ROE >14%

- Around 1-1.2% Credit Cost ( Even after giving high risk loans like MSME & Agriculture Loans)

- No union strike in past 100 years of history

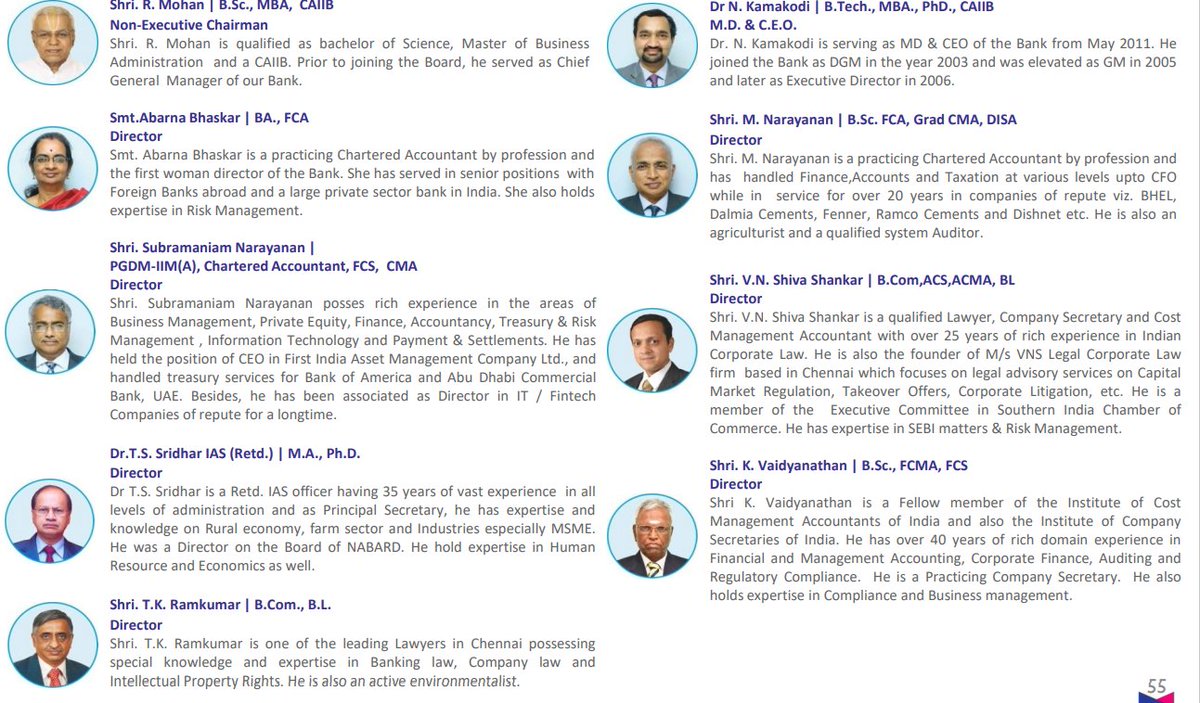

- 89% directors on board are independent directors

- Has added 45 branches & 300 employees every year from 2010-2020

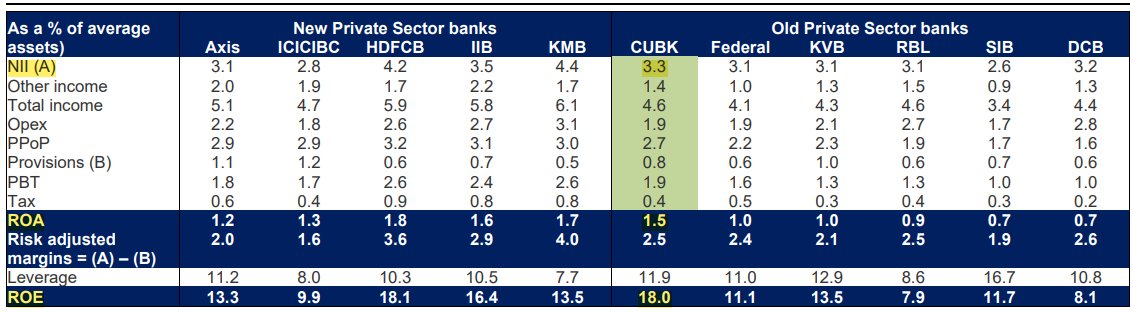

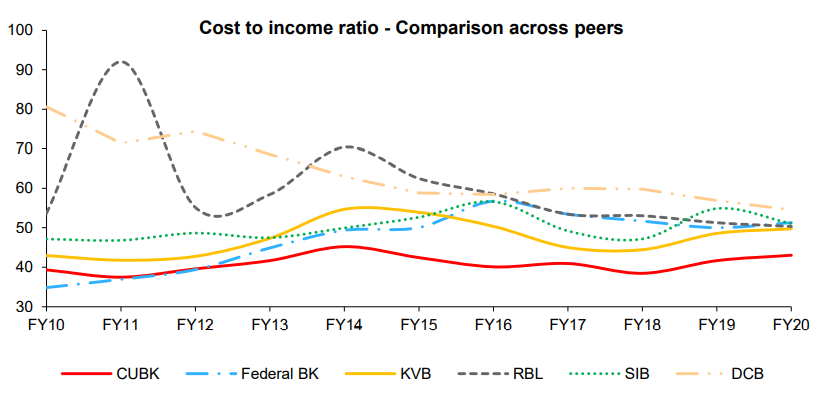

- Cost to income Ratio has been lower around 40-43% , which is lower than it's peers.

- 89% directors on board are independent directors

- Has added 45 branches & 300 employees every year from 2010-2020

- Cost to income Ratio has been lower around 40-43% , which is lower than it's peers.

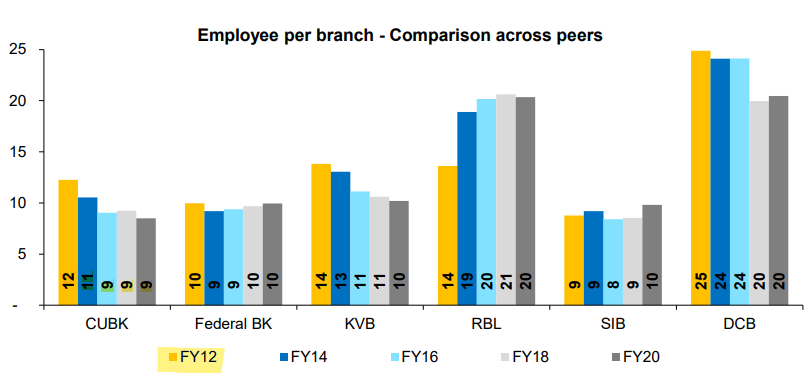

- Have lower number of employees per branch as compared to peers and reducing them even further.

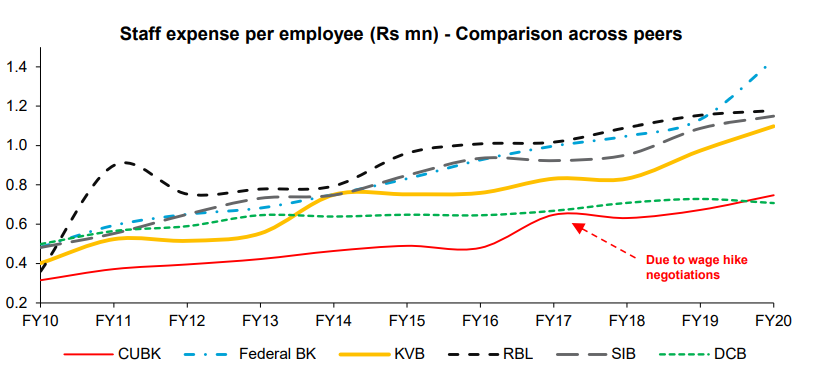

- Lower staff expense as compared to peers.

- Lower staff expense as compared to peers.

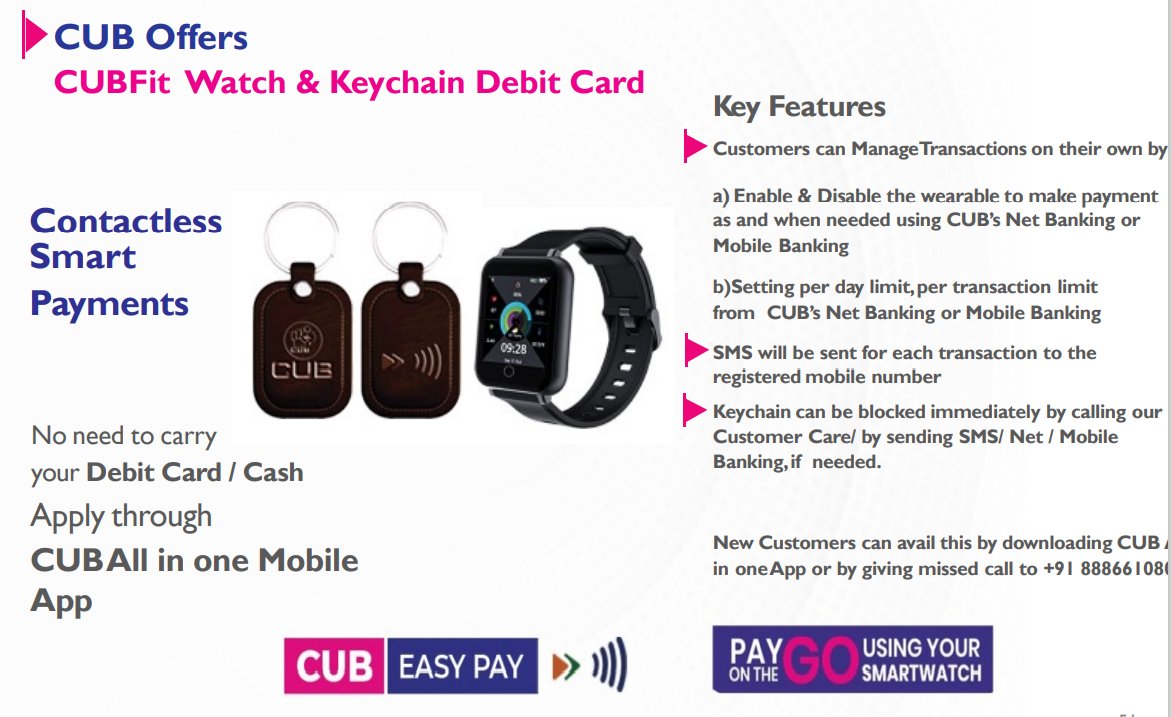

Have taken some digital initiatives like

- Fully integrated mobile banking App

- Key chain debit card & Smart watch payment system

- Was amongst the earliest bank to embark on digital journey, hired TCS for Core Banking Solutions back in around 2001.

- Fully integrated mobile banking App

- Key chain debit card & Smart watch payment system

- Was amongst the earliest bank to embark on digital journey, hired TCS for Core Banking Solutions back in around 2001.

Not a promoter run bank.

Mr N kamakodi one of the most trusted and respected banker have been the CEO since 2011

Mr N kamakodi one of the most trusted and respected banker have been the CEO since 2011

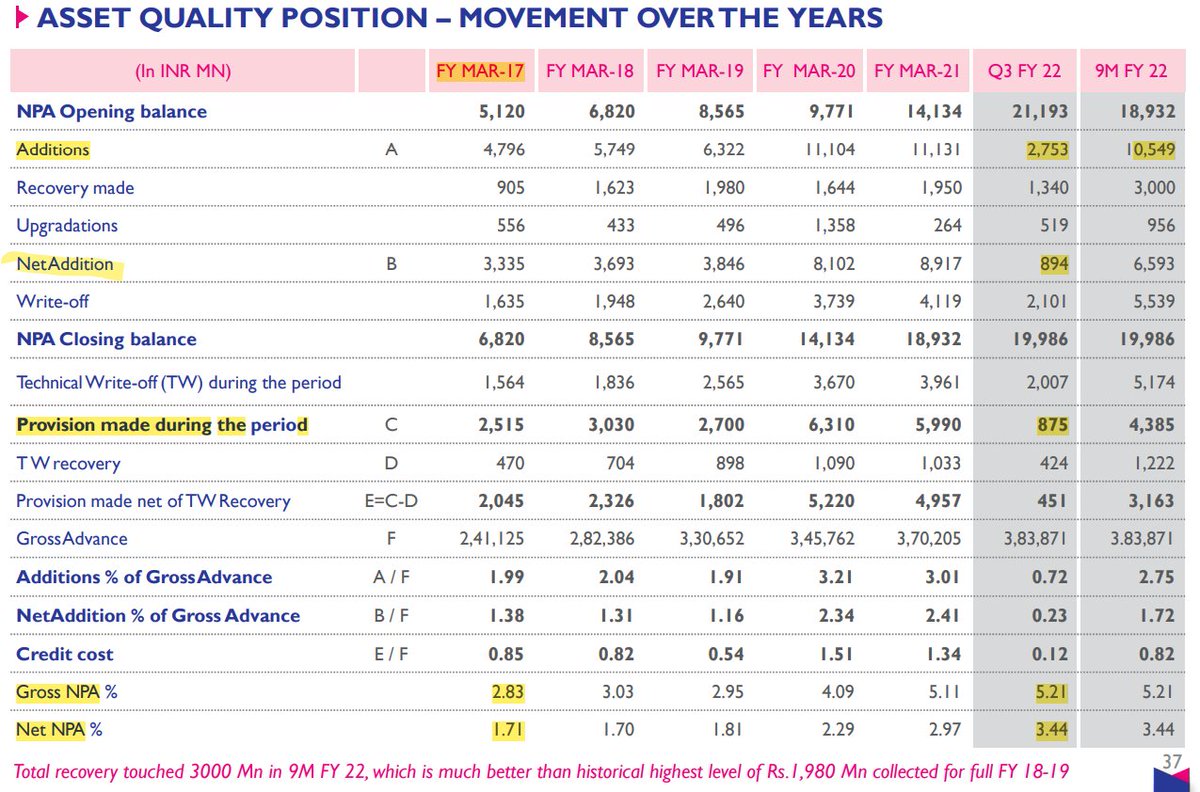

If we do the current NPA analysis - GNPA increased from 2.83% in 2017 to 5.21% in Q3 FY22 ( Mainly due to Covid).

Good thing is, provisions have come down & new additions are also coming down.

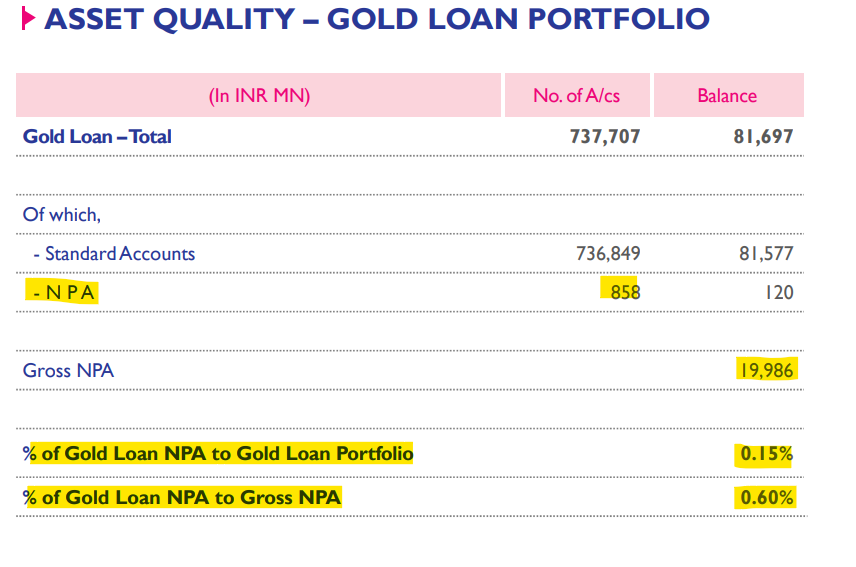

Gold loan portfolio is strong with <1% NPA.

Good thing is, provisions have come down & new additions are also coming down.

Gold loan portfolio is strong with <1% NPA.

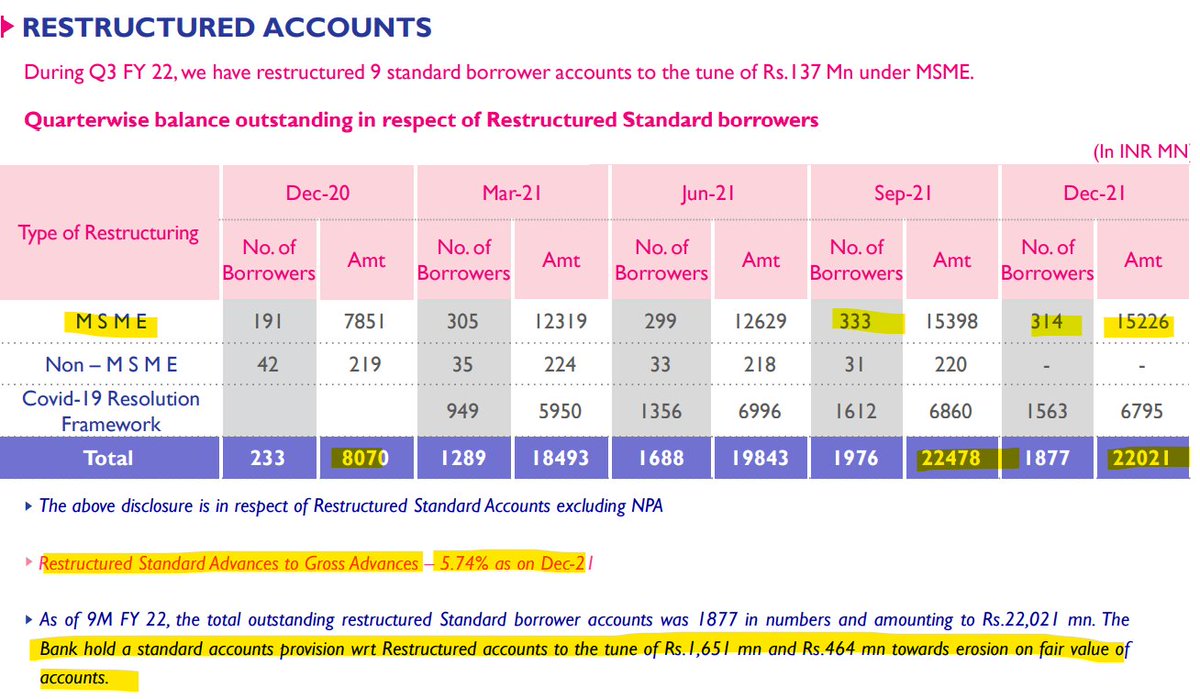

Total restructured account are around 5.74% of the total advances.

Total no. of restructured accounts have come down QoQ.

Bank holds around 1400 Cr provision for restructures accounts.

Total no. of restructured accounts have come down QoQ.

Bank holds around 1400 Cr provision for restructures accounts.

Given the quality of management and past track record of maintaining 14% loan book growth with stable asset quality and ROA >1.5% AND ROE >14%.

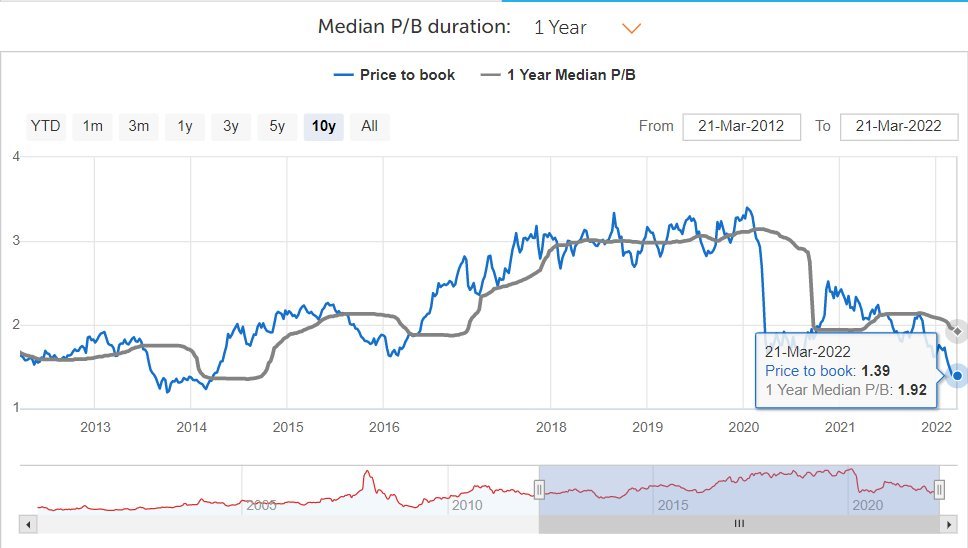

Currently available near decade low p/b can be a good opportunity.

Disclosure - Invested, Not a recommendation

Currently available near decade low p/b can be a good opportunity.

Disclosure - Invested, Not a recommendation

If you enjoyed the thread and learned something, please re-tweet the 1st post.

@suru27 @shubhfin @saketreddy @ishmohit1 @soicfinance @sahil_vi @DrdhimanBhatta1 @Arthavruksha12 @badola_arjun

@suru27 @shubhfin @saketreddy @ishmohit1 @soicfinance @sahil_vi @DrdhimanBhatta1 @Arthavruksha12 @badola_arjun

Loading suggestions...