The Fed's minutes today are very likely to detail its plans for the runoff of its asset portfolio.

Powell said last month that the minutes "will lay out pretty much the parameters of what we're looking at."

Brainard yesterday added similar color wsj.com

Powell said last month that the minutes "will lay out pretty much the parameters of what we're looking at."

Brainard yesterday added similar color wsj.com

Powell also said that the contours of the plan "will look quite familiar," which means that the initial portfolio run-off will, as in 2017-19, most likely allow securities to mature passively.

That leaves a couple questions for the minutes to fill in.

That leaves a couple questions for the minutes to fill in.

For the moment, the Fed is reinvesting the payments of maturing Treasury and mortgage-backed securities into new securities.

Question 1: How many securities should be allowed to mature every month?

Last time, the Fed was very concerned about portfolio runoff, which was new.

Question 1: How many securities should be allowed to mature every month?

Last time, the Fed was very concerned about portfolio runoff, which was new.

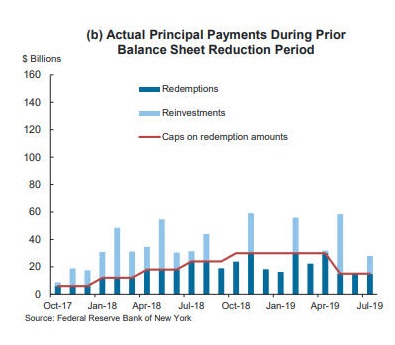

As a result, the Fed allowed relatively small amounts of securities to mature for the first year of runoff. Ultimately, it would allow up to $30 billion in Treasurys to mature every month.

But as you can see in the chart, those caps were binding only one month every quarter.

But as you can see in the chart, those caps were binding only one month every quarter.

Fed officials, including Brainard on Wednesday, have indicated that the reinvestment caps will be higher this time because the Fed has many more securities than last time.

She also indicated that the Fed would have a much faster run-up to the terminal redemption caps.

She also indicated that the Fed would have a much faster run-up to the terminal redemption caps.

In the NY Fed's bank survey in January, the median respondent thought the Fed would allow $150 billion in Treasury securities to mature every quarter

That would be consistent with a UST redemption cap of ~$60 billion per month (again, it would only bind in one month per quarter)

That would be consistent with a UST redemption cap of ~$60 billion per month (again, it would only bind in one month per quarter)

Brainard yesterday led to some speculation that the redemption caps might be higher.

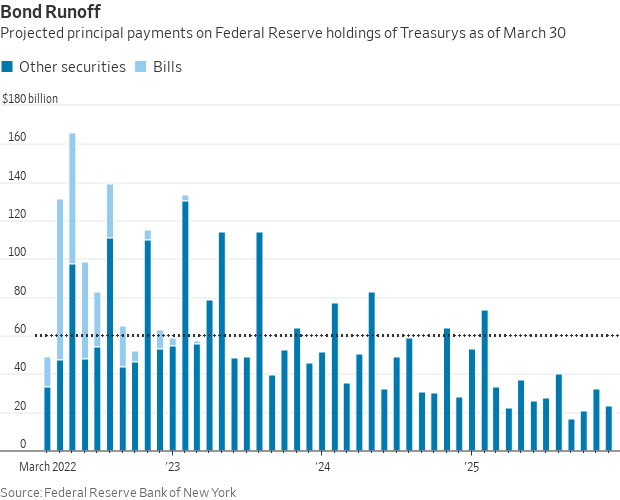

But as you can see here, Treasury redemptions don't rise much with larger caps. If the cap is at $80 billion, that would result in average monthly redemptions of $60 billion this year.

But as you can see here, Treasury redemptions don't rise much with larger caps. If the cap is at $80 billion, that would result in average monthly redemptions of $60 billion this year.

One difference from 2017-19 is that the Fed owns $326 billion in T-bills.

It didn't have any bills last time, leading to Question 2: How will the Fed treat Bills in any runoff?

(For simplicity, the above back-of-the-envelope numbers assume bills aren't subject to these caps)

It didn't have any bills last time, leading to Question 2: How will the Fed treat Bills in any runoff?

(For simplicity, the above back-of-the-envelope numbers assume bills aren't subject to these caps)

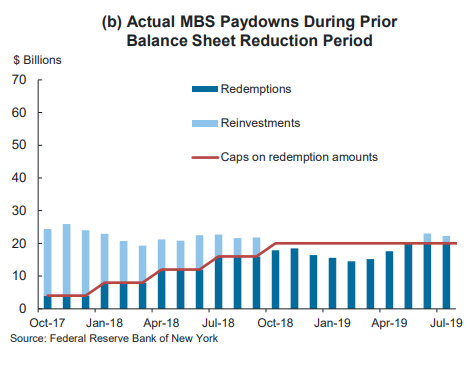

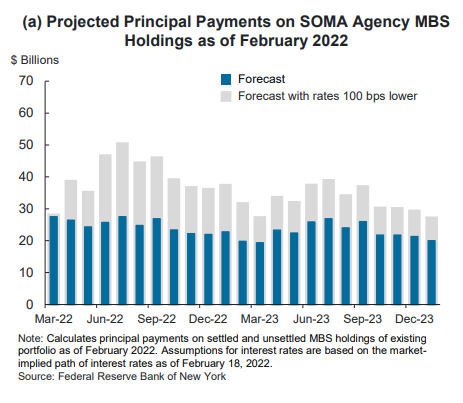

Finally, there is the Q of where to set the runoff cap for MBS. The FRBNY dealer survey in January assumed maximum net redemptions of $30 billion per month.

Last time, there was a slow ramp up; the terminal redemption cap of $20 billion didn't bind until rates fell in June '19.

Last time, there was a slow ramp up; the terminal redemption cap of $20 billion didn't bind until rates fell in June '19.

If the Fed were to set the MBS runoff cap at $30 billion, so long as refinances are low (because rates are higher), that cap isn't likely to bind. In other words, passive MBS runoff isn't likely to exceed $30 billion per month at current rates.

From Lorie Logan's 3/2 speech:

From Lorie Logan's 3/2 speech:

While it isn't a given the Fed will lay out the redemption caps in the minutes, it seems like a good bet based on

1) what Powell said last month

2) the desire to announce runoff in May

3) how the Fed used the Sept FOMC minutes to reveal proposed quantities for the asset taper.

1) what Powell said last month

2) the desire to announce runoff in May

3) how the Fed used the Sept FOMC minutes to reveal proposed quantities for the asset taper.

Loading suggestions...