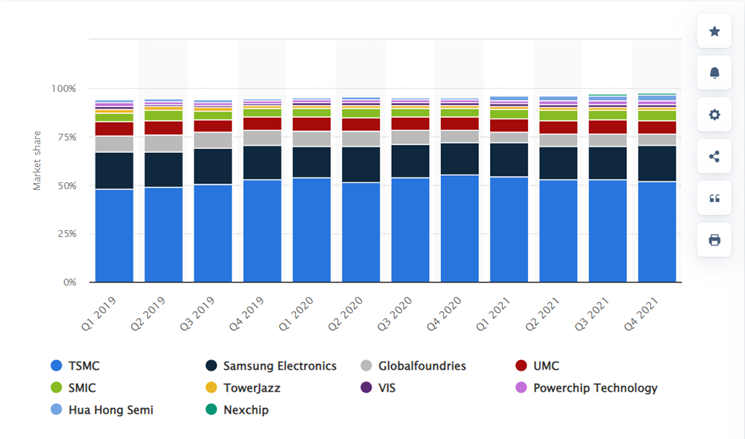

In this “Shallow Dive” I’m going to discuss $TSM. Taiwan Semiconductor is the world’s largest foundry and the second-largest foreign company (by market cap). TSM has over 50% market share in their stage of the semiconductor supply chain, so how did they do that?

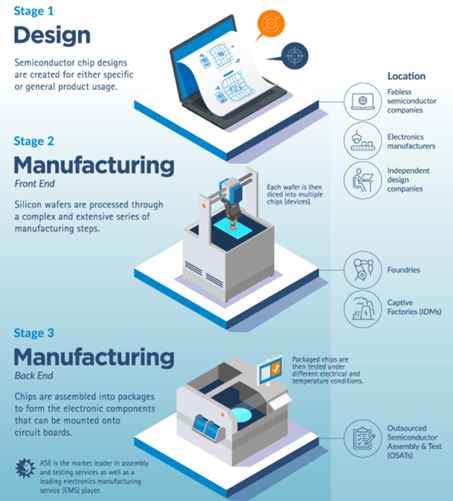

In simplified terms, there are three stages to the semiconductor supply chain. $INTC is an integrated device manufacturer, but many new upstarts like $NVDA are fabless (step 1) and rely on companies like TSM to manufacture their chips (step 2).

Many semiconductor companies are outsourcing production as manufacturing chips is very capital intensive (low ROIC). New entrants like $AAPL are designing their own chips in-house and relying on TSM for manufacturing.

TSM has economies of scale with >50% market share. In the foundry business, there are high R&D costs and fixed costs creating a barrier to entry. TSM is able to “spread” those fixed costs out on a greater base allowing them to have higher margins than the competition.

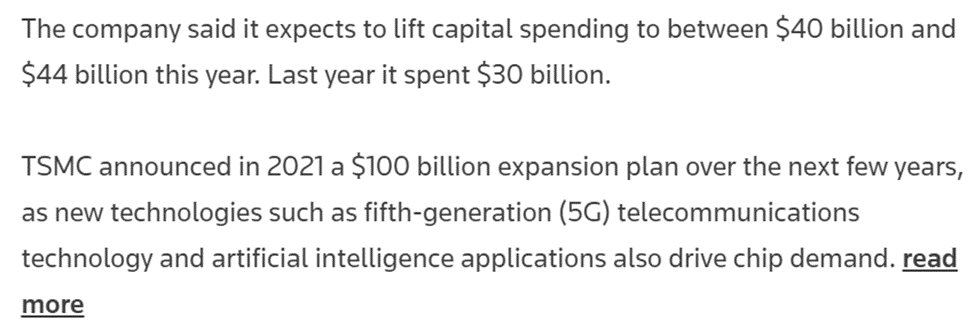

Other foundries can’t keep up with TSM’s CAPEX budget. In 2015, six companies introduced cutting-edge nodes 16/14 nm. Currently, only TSM and Samsung have released the current cutting edge 5 nm fabs and some IDMs ($INTC & $AMD) rely on TSM for their advanced semis.

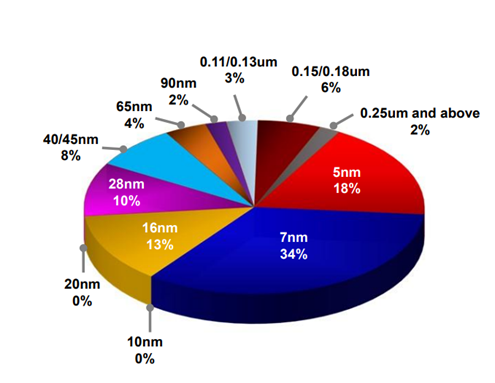

Cutting edge semiconductors are higher margin as fewer foundries can produce them. Over 50% of TSM semiconductors produced are considered cutting edge (7nm and less). TSM is able to have higher margins and less competition due to high fixed costs (barrier to entrance).

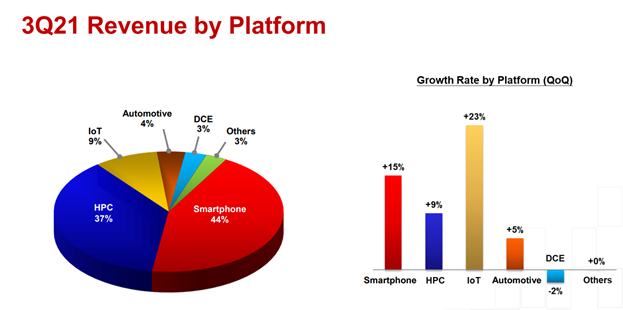

The semiconductor industry has tailwinds from multiple industries including IoT and Smartphone. As the world becomes more digital, the reliance on semiconductors increases as well. I would love to hear what others think about TSM.

Loading suggestions...