Rupa & Company Business model:

Why Abakkus fund is buying it?

Can it be next PAGE Industry?

A thread (1/20)

Why Abakkus fund is buying it?

Can it be next PAGE Industry?

A thread (1/20)

Let’s discuss brands first. Company has products ranging from economy to Super premium. Please spend some time on the image.

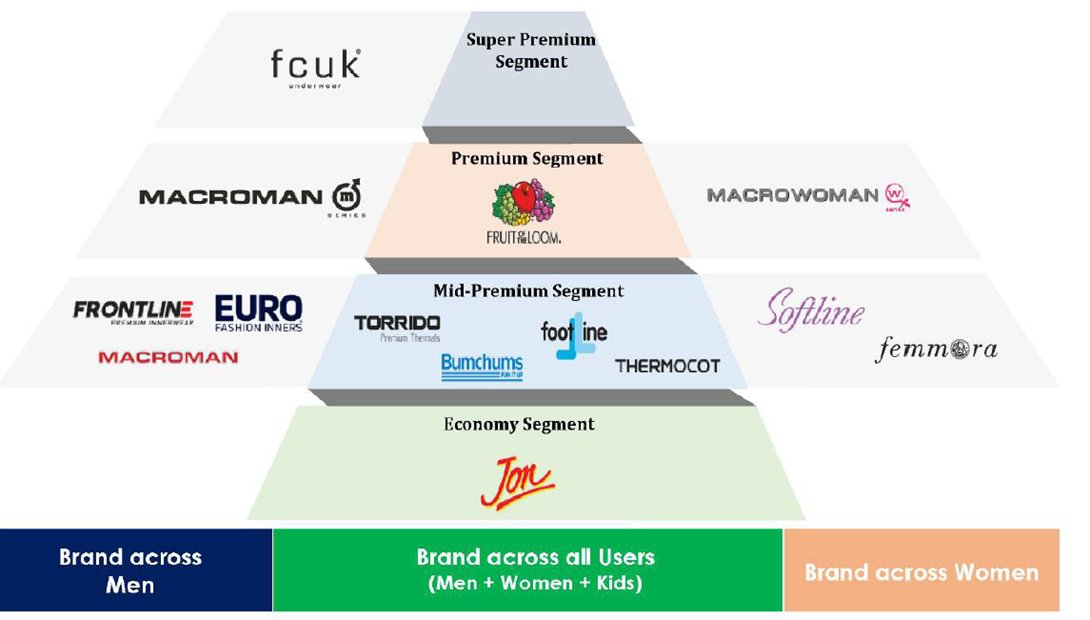

Few brands are common for man & woman. Some are specific for men (FCUK, Macroaman etc) and some are specific for women (Softline, Macrowoman etc)

(2/20)

Few brands are common for man & woman. Some are specific for men (FCUK, Macroaman etc) and some are specific for women (Softline, Macrowoman etc)

(2/20)

They are present PAN India. However not equally strong at all geography.

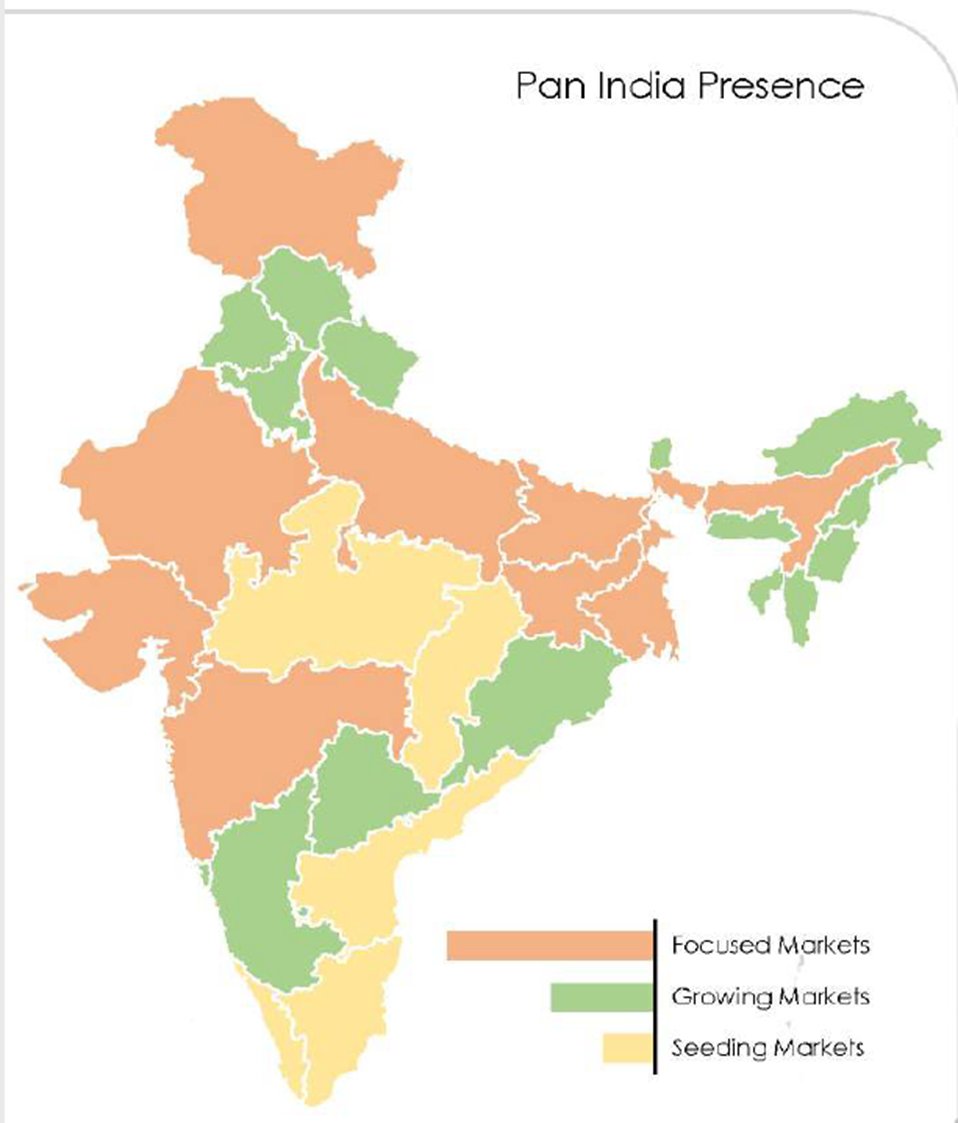

They extremely strong in East, some pockets of strength in west & north. South market is weak and trying to grow.

(3/20)

They extremely strong in East, some pockets of strength in west & north. South market is weak and trying to grow.

(3/20)

Industry is growing at 11% CAGR. Triggers are increase in working women and fashion consciousness.

As unorganised industry is almost 60%, organised players are expected to grow faster.

(4/20)

As unorganised industry is almost 60%, organised players are expected to grow faster.

(4/20)

Posted decent numbers in FY21 and same trend is going on in FY22 (except Q1). Along with revenue growth, improvement in margin is commendable.

Innerwear is transforming from “Commodity” to “Fashion” and growing premium penetration should help in margin improvement.

(5/20)

Innerwear is transforming from “Commodity” to “Fashion” and growing premium penetration should help in margin improvement.

(5/20)

Rupa has targeted few areas to grow exponentially.

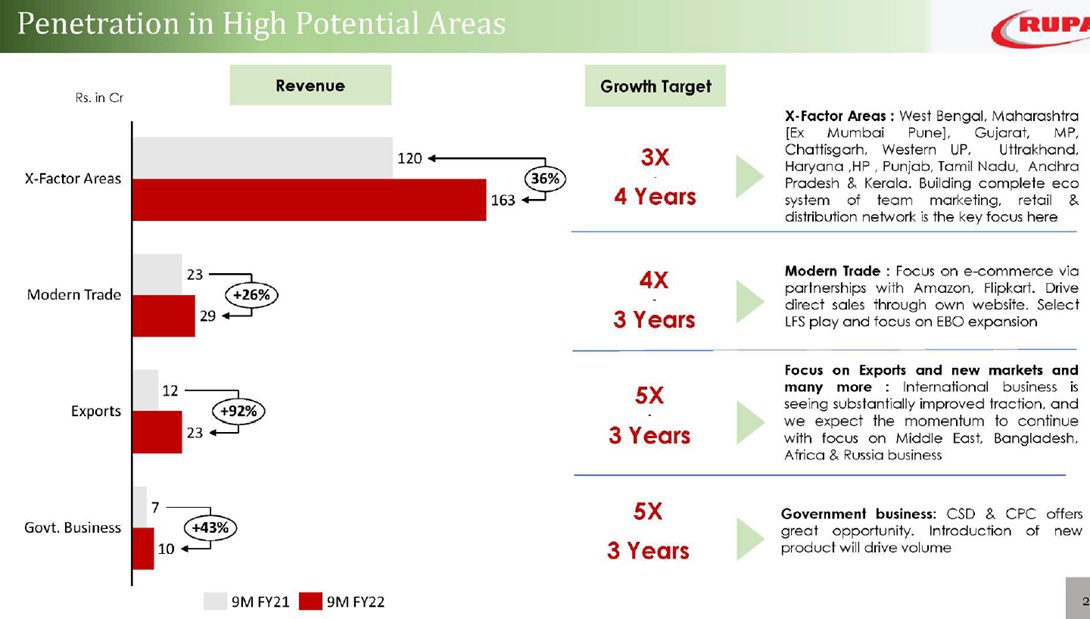

1. Few specific states mainly in West , Noth & South: 3x in 4 years

2.Ecommerce: 4x in 3 years

3.Exports: 5x in 3 years

4.Govt Business: 5x in 3 years.

(6/20)

1. Few specific states mainly in West , Noth & South: 3x in 4 years

2.Ecommerce: 4x in 3 years

3.Exports: 5x in 3 years

4.Govt Business: 5x in 3 years.

(6/20)

Most of this areas are contributing small to overall revenue pie. So this exponential growth on small base should help for high teen growth.

For example currently, Ecommerce is 2-3% of sales, targeting 8-10% ecommerce in next 2-3 years.

(7/20)

For example currently, Ecommerce is 2-3% of sales, targeting 8-10% ecommerce in next 2-3 years.

(7/20)

Woman category for Rupa is only in 11-12%.

Trying to achieve better performance in this segment and Initiative like Softline brand endorsement by Kiara Advani is being taken.

(8/20)

Trying to achieve better performance in this segment and Initiative like Softline brand endorsement by Kiara Advani is being taken.

(8/20)

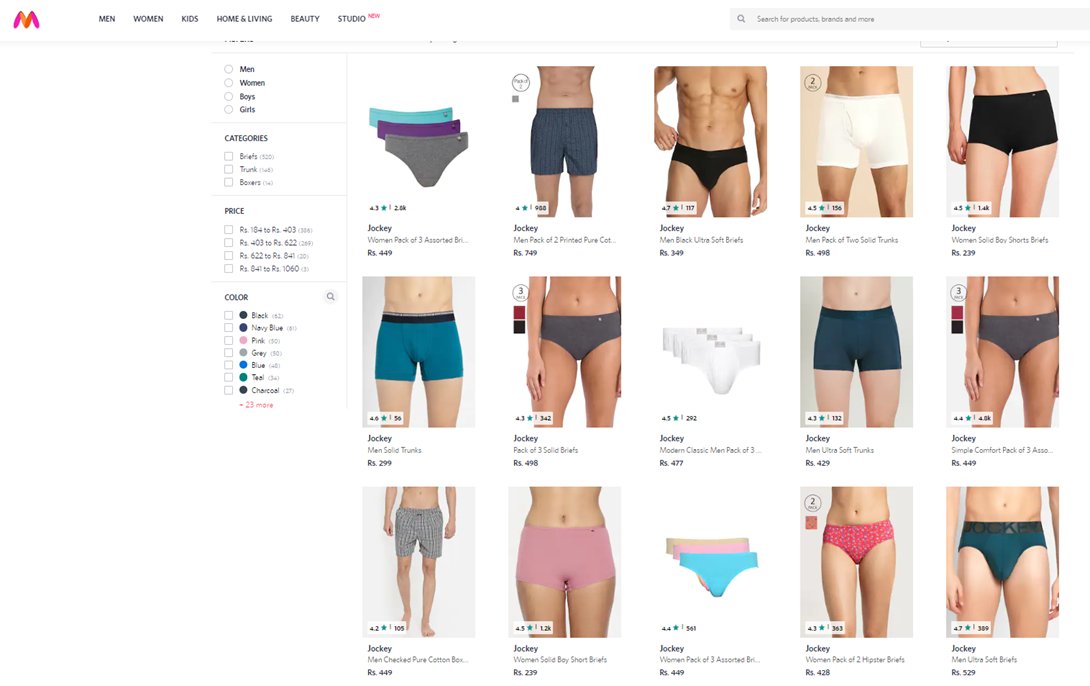

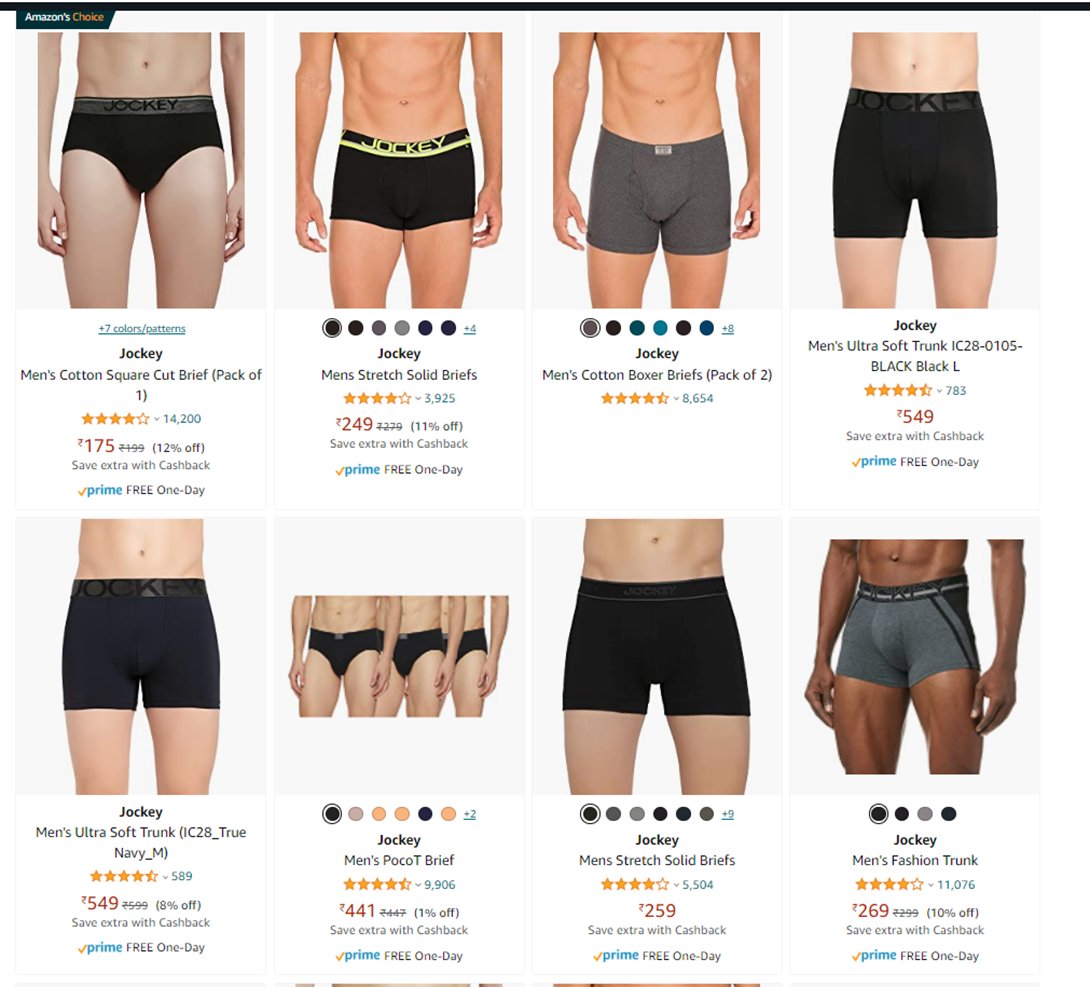

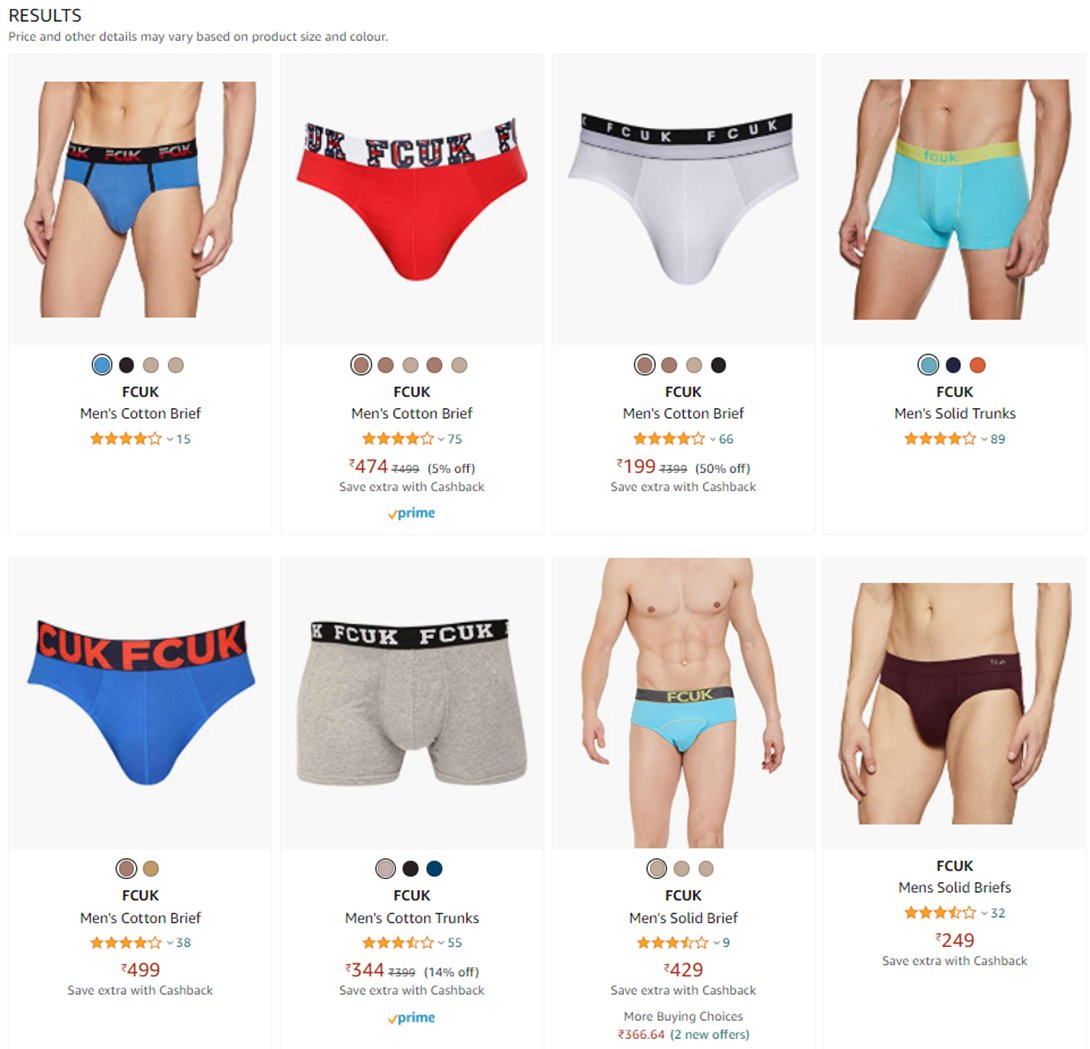

Review & price checking in ecommerce platform (Myntra & Amazon):

Avg realization of FCUK is even higher than Jockey. However avg rating is higher in Jockey.

Sale/ No of Review in Jockey is not even worth comparing with FCUK.

(9/20)

Avg realization of FCUK is even higher than Jockey. However avg rating is higher in Jockey.

Sale/ No of Review in Jockey is not even worth comparing with FCUK.

(9/20)

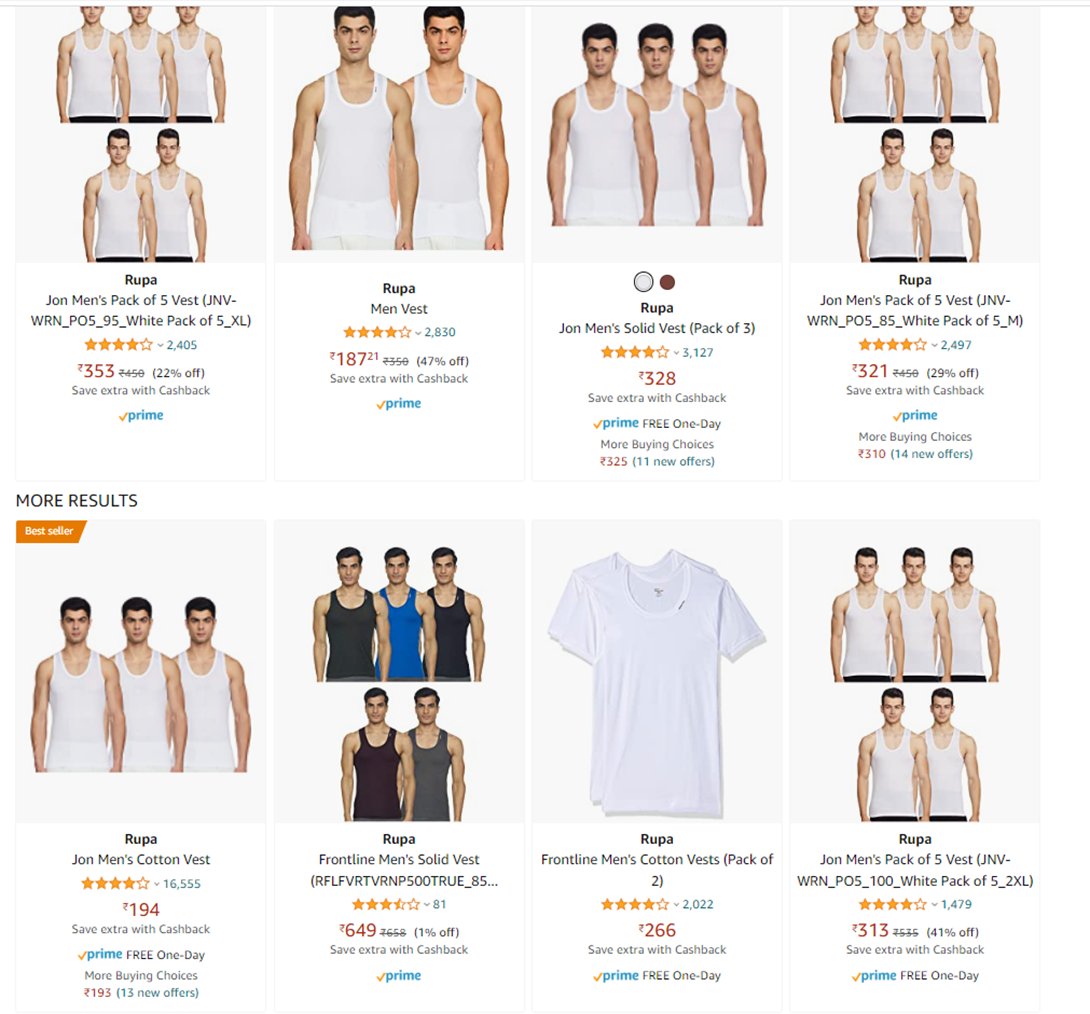

However economy brands (with lower realization) show decent review and scale.

(10/20)

(10/20)

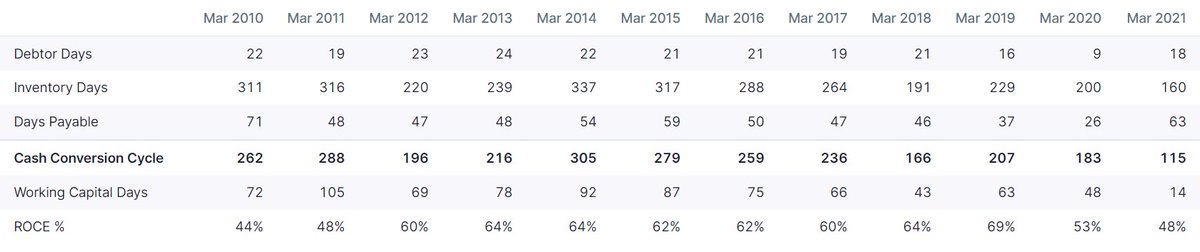

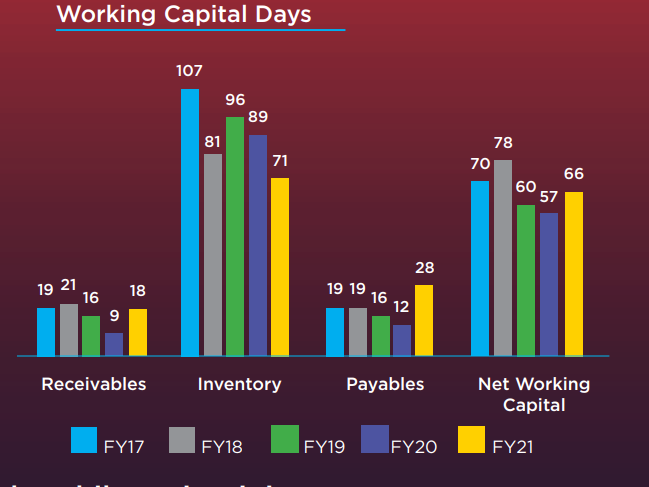

Page ROCE (50%) is way higher than Rupa (30%). Why?

Let’s Understand.

ROCE can be broken down into 3 parts.

(11/20)

Let’s Understand.

ROCE can be broken down into 3 parts.

(11/20)

1. Fixed asset turnover: Page(9x+) is slightly better than Rupa (7x), Higher Avg realization helps it.

2. Operating Margin: Margin is similar for both (20%)

3. Working captal : Ability of Page to squeeze debtors and keep receivables in limit is beyond any praise.

(12/20)

2. Operating Margin: Margin is similar for both (20%)

3. Working captal : Ability of Page to squeeze debtors and keep receivables in limit is beyond any praise.

(12/20)

Similarly they buy raw materials with extended time period compared to anyone in the Industry.

Large nos of EBO (Exclusive brand outlet) and brand recognition help it to run efficiently with lower working capital and thereby pushing ROCE in the north of 50%.

(13/20)

Large nos of EBO (Exclusive brand outlet) and brand recognition help it to run efficiently with lower working capital and thereby pushing ROCE in the north of 50%.

(13/20)

Rupa is focusing on premium products and grow their share in overall revenue pie. Currently premium segment is only at high single digit.

All competitors of page are lagging on super premium products for example Rupa (FCUK), Dollar Ind (Pepe), Lux (One8).

(14/20)

All competitors of page are lagging on super premium products for example Rupa (FCUK), Dollar Ind (Pepe), Lux (One8).

(14/20)

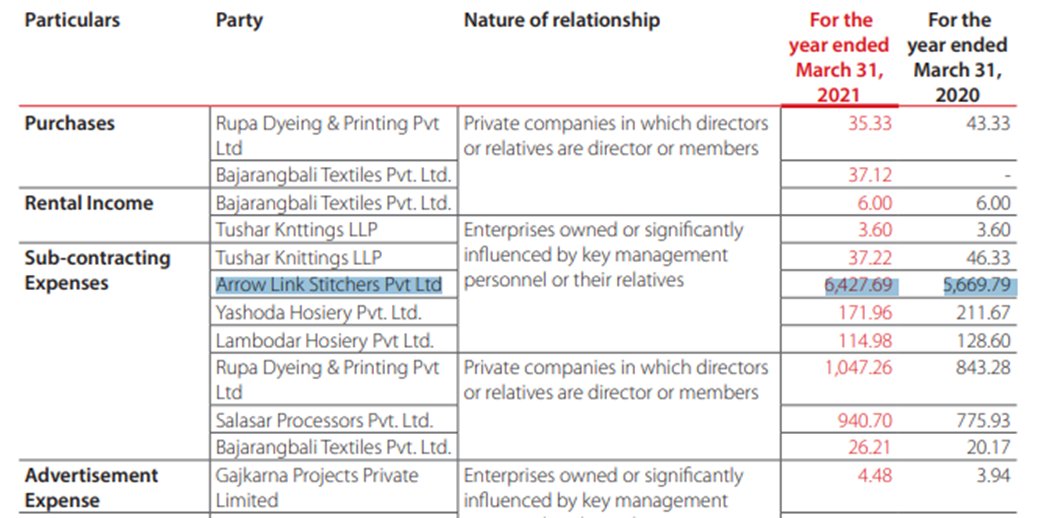

Risks:

1. Promoter group has a lot of other unlisted business even in textile space and business transactions occur with them on regular basis.

(15/20)

1. Promoter group has a lot of other unlisted business even in textile space and business transactions occur with them on regular basis.

(15/20)

2. Everyone (Rupa, Lux & Dollar) is doing the same thing

a. Pushing premium products.

b. Focusing on Women products

c. Brand endorsements by big celebrities.

d. Trying to control Working capital.

Not much differentiation in offerings with competitors.

(16/20)

a. Pushing premium products.

b. Focusing on Women products

c. Brand endorsements by big celebrities.

d. Trying to control Working capital.

Not much differentiation in offerings with competitors.

(16/20)

Page vs Rupa (TTM numbers)

Sales: 3656cr vs 1473cr

PAT: 462cr vs 206cr

Market cap: 50k cr vs 4k cr (Ridiculous?)

(17/20)

Sales: 3656cr vs 1473cr

PAT: 462cr vs 206cr

Market cap: 50k cr vs 4k cr (Ridiculous?)

(17/20)

Page market cap is 12.5x of Rupa which is beyond my understanding.

Page used to grow 30%+ CAGR during 2010-15 period. Now, it is not possible to do so.

So paying 13-14x price to sales is definitely costly.

(18/20)

Page used to grow 30%+ CAGR during 2010-15 period. Now, it is not possible to do so.

So paying 13-14x price to sales is definitely costly.

(18/20)

On the other hand Rupa is trying to grow high teen with slight margin improvement in each year.

Execution is the key. Let’s keep an eye whether management can walk the talk.

(19/20)

Execution is the key. Let’s keep an eye whether management can walk the talk.

(19/20)

Last but not the least: Business becomes “GREAT” by accident.

A perfect bonding among an intelligent fanatic, right business model and appropriate macroeconomic condition happen by chance.

Hence copy of a great business is rarely born.

(20/20)

A perfect bonding among an intelligent fanatic, right business model and appropriate macroeconomic condition happen by chance.

Hence copy of a great business is rarely born.

(20/20)

Loading suggestions...