Bancor V3 might be a great next step for DeFi.

Bancor has divided opinion over the years, but give me a chance, anon.

@Bancor V3 🧵

Bancor has divided opinion over the years, but give me a chance, anon.

@Bancor V3 🧵

I know a lot of you have written Bancor off because they have taken a long time to ship V3.

But, I think you will be pleasantly surprised by the innovation if you keep reading.

But, I think you will be pleasantly surprised by the innovation if you keep reading.

You can read this as a longer substack, or just continue with the thread.

alphapls.substack.com

alphapls.substack.com

I don’t know about you, but I’m personally fed up of new ponzi-esque designs that simply create another race for people to dump on each other.

It’s not just me, I’ve seen a lot of people who have been around the space a long time asking “where’s the innovation right now?”.

It’s not just me, I’ve seen a lot of people who have been around the space a long time asking “where’s the innovation right now?”.

Bancor V3 might be a great next step for DeFi.

I say this when I think about the experience for the average DeFi user.

I say this when I think about the experience for the average DeFi user.

A quick TLDR on Bancor for those that have never heard of the protocol.

You could argue that Bancor invented DeFi.

They were the first to invent liquidity pools.

The pool token, the DEX mechanism and the bonding curve concept was all a Bancor innovation.

They first launched the protocol in 2017.

They really are the DeFi OGs.

They were the first to invent liquidity pools.

The pool token, the DEX mechanism and the bonding curve concept was all a Bancor innovation.

They first launched the protocol in 2017.

They really are the DeFi OGs.

They have been pretty loud about all of the things they think are wrong with DeFi.

• Forced exposure (being forced to hold another token in a pool to earn yield)

• Impermanent loss (IL)

• Forced exposure (being forced to hold another token in a pool to earn yield)

• Impermanent loss (IL)

Uniswap is the biggest DEX in DeFi and I use it on a weekly basis, but being a V3 LP is way too difficult and not profitable for most users.

Ultimately, users shouldn't have to know about IL. It's a very complex subject and in a fast moving crypto world difficult for even the most qualified to get right.

It's a product problem.

It's a product problem.

Bancor V2 looked to solve some of these problems.

Single-sided staking made Bancor unique.

You could hold whatever percentage of tokens you wanted and earn yield.

And you were guaranteed IL protection after 100 days, assuring that you would leave with at least the money you put in to the pool.

You could hold whatever percentage of tokens you wanted and earn yield.

And you were guaranteed IL protection after 100 days, assuring that you would leave with at least the money you put in to the pool.

I used Bancor V2. I am fully aware of the memes and problems that existed with the protocol:

• Very high (!) gas fees to deposit, withdraw or claim rewards

• No space in the pools for people to enter, due to the way the insurance worked

• Very high (!) gas fees to deposit, withdraw or claim rewards

• No space in the pools for people to enter, due to the way the insurance worked

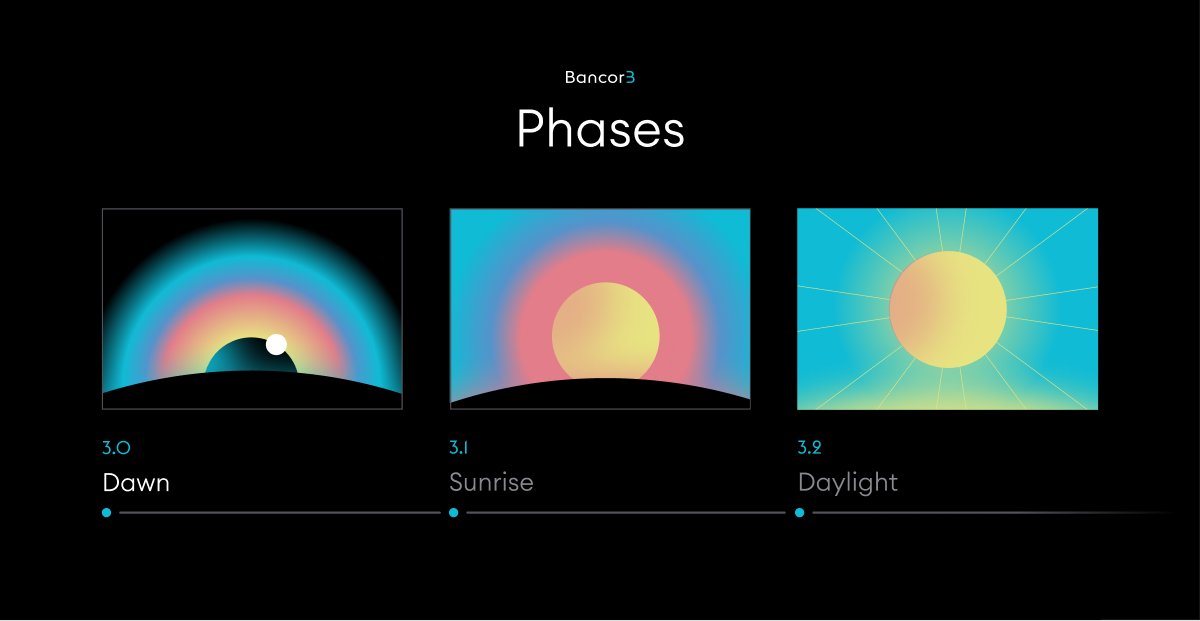

So, after aeons of research, gathering feedback and assessing product market fit, Bancor V3 has just launched in beta.

This is called the Dawn Phase and will be followed by two subsequent phases.

Here are the innovations which have launched in the Dawn Phase:

Here are the innovations which have launched in the Dawn Phase:

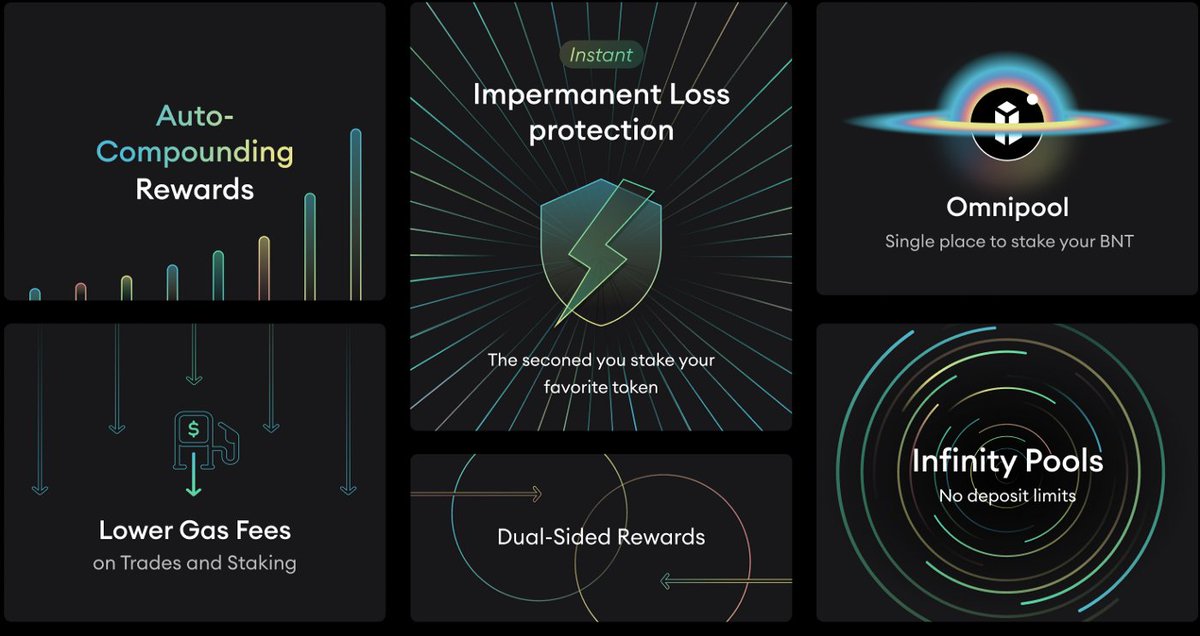

Instant IL protection

100% protection from day 1. No insurance schedule.

Obviously this is much better for the user, but it's cheaper for the protocol too.

100% protection from day 1. No insurance schedule.

Obviously this is much better for the user, but it's cheaper for the protocol too.

There is a clever algorithm working in the background with the sole priority of managing the protocol's liquidity.

Protocol-owned liquidity associated with one pool can be used to compensate users whose staked tokens are associated with another pool.

The benefits of this are two-fold:

1. It is less likely the protocol will need to mint new BNT to compensate for a user’s IL.

2. it is more likely a user will receive their IL compensation entirely in the token they’ve staked, instead of partly in BNT.

1. It is less likely the protocol will need to mint new BNT to compensate for a user’s IL.

2. it is more likely a user will receive their IL compensation entirely in the token they’ve staked, instead of partly in BNT.

Omnipool

BNT has been taken out of the pools and amassed into one location.

The pools then become, in @MBRichardson87's words:

"An orbit around the BNT rather than a collection of buckets of different tokens."

BNT has been taken out of the pools and amassed into one location.

The pools then become, in @MBRichardson87's words:

"An orbit around the BNT rather than a collection of buckets of different tokens."

The Omnipool is a central pool and contains all of the tokens of the Bancor Network, including BNT.

This is in contrast to discreet liquidity pools that contain their own token.

And here comes a significant gas saving!

This is in contrast to discreet liquidity pools that contain their own token.

And here comes a significant gas saving!

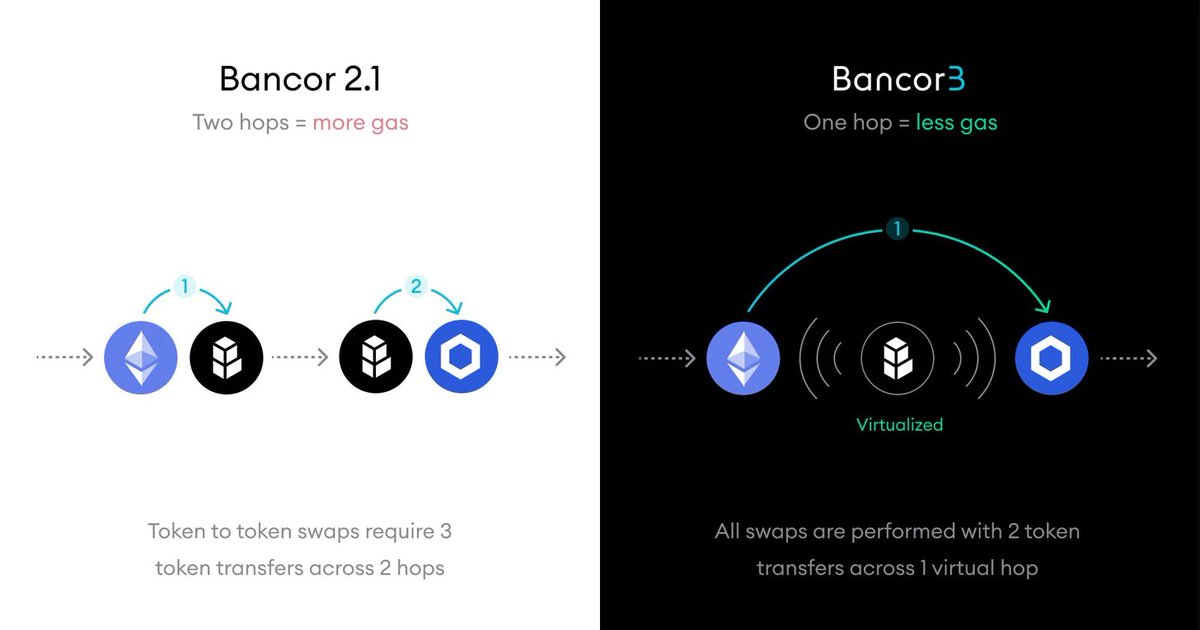

Previously, if you wanted to buy LINK with ETH, this was the process:

1. Send ETH into the ETH pool

2. ETH pool would send a BNT token to the LINK pool

3. The LINK pool would then send that $LINK token to you

Two hops. No bueno for gas.

1. Send ETH into the ETH pool

2. ETH pool would send a BNT token to the LINK pool

3. The LINK pool would then send that $LINK token to you

Two hops. No bueno for gas.

Now in V3, all trades can now occur in a single transaction.

With single-hop trades, Bancor can:

• Attract more trading fees with the same level of liquidity

• Make the protocol more capital efficient.

• Reduce staking costs

A much better user experience.

With single-hop trades, Bancor can:

• Attract more trading fees with the same level of liquidity

• Make the protocol more capital efficient.

• Reduce staking costs

A much better user experience.

Infinity Pools

In V3 you can contribute as much capital as you want to the protocol.

In V3 you can contribute as much capital as you want to the protocol.

In V2 there was a limited capacity for single sided staking because of the way the insurance worked.

It created a big bottleneck for how much TVL the protocol could lock up.

There was a huge demand & users were always waiting to get in.

This pissed people off.

It created a big bottleneck for how much TVL the protocol could lock up.

There was a huge demand & users were always waiting to get in.

This pissed people off.

This bottleneck is now a thing of the past with V3.

Lots of people don't want IL and I would expect there to be a huge swell in TVL as a result.

Lots of people don't want IL and I would expect there to be a huge swell in TVL as a result.

Infinity pools also introduce the concept of “Superfluid Liquidity”.

Superfluid Liquidity can be used simultaneously for market-making and other fee-earning strategies that are native and external to the protocol.

(e.g. “superlinear” staking of LINK tokens, ETH validator staking on Beacon chain, and so on)

(e.g. “superlinear” staking of LINK tokens, ETH validator staking on Beacon chain, and so on)

That more than one activity can be simultaneously represented in the APY

garnered on a pool token is termed “superfluid liquidity”.

garnered on a pool token is termed “superfluid liquidity”.

Auto-compounding rewards

V3 introduces auto-compounding rewards at the hardware level.

V3 introduces auto-compounding rewards at the hardware level.

Now both fees and liquidity mining rewards are auto-compounding.

This means earnings are instantly re-added to the pool, improving the network’s liquidity and increasing your potential to earn more fees and rewards, with no user action required.

It's completely set & forget.

This means earnings are instantly re-added to the pool, improving the network’s liquidity and increasing your potential to earn more fees and rewards, with no user action required.

It's completely set & forget.

This is a huge improvement and innovation, as previously you had to spend crazy gas fees to manually re-add your rewards.

Other DeFi auto-compounders like YieldYak don't work this way, so this is a new invention.

Other DeFi auto-compounders like YieldYak don't work this way, so this is a new invention.

Dual-Sided Rewards

In Bancor V2, only Bancor could incentivize its liquidity pools with BNT rewards.

In V3, third-party protocols can now also offer rewards on their pools, so depositors can benefit from dual-sided rewards, earning more BNT and more of the token they staked.

In Bancor V2, only Bancor could incentivize its liquidity pools with BNT rewards.

In V3, third-party protocols can now also offer rewards on their pools, so depositors can benefit from dual-sided rewards, earning more BNT and more of the token they staked.

Both BNT and non-BNT rewards are free from the risk of impermanent loss, reducing the cost of running rewards programs for third-party protocols.

This will be another way to collab with token projects, growing the Bancor TVL.

This may also cause a lot of DAOs to move their treasuries to Bancor.

Multichain

V3 is sufficiently lightweight so the contracts can be moved between blockchains quite easily.

This will be a DAO decision, but Bancor v3 will end up on an Alt L1 or/and L2.

My money is on Avalanche having seen Mark Richardson at the Avax Summit.

V3 is sufficiently lightweight so the contracts can be moved between blockchains quite easily.

This will be a DAO decision, but Bancor v3 will end up on an Alt L1 or/and L2.

My money is on Avalanche having seen Mark Richardson at the Avax Summit.

There's no doubt that this will be huge for Bancor, as L1 gas costs have stopped many using the protocol.

Liquidity Direction

The DAO can now vote to shrink the protocol-owned BNT in any pool if the pool is under-performing, and direct the BNT liquidity to more profitable pools.

The DAO can now vote to shrink the protocol-owned BNT in any pool if the pool is under-performing, and direct the BNT liquidity to more profitable pools.

By directing BNT towards the most performant pools in the network, the DAO can more effectively manage risk and optimize fees earned by the protocol, BNT holders and LPs.

An important component of V3 is how they are addressing inflation. Bancor were forced to adopt liquidity mining with V2 as a necessary marketing expense. But, Bancor will now be weaning themselves off liquidity mining and will be “getting back to more sensible fiscal policy.”

In V3, a maximum of 40,000,000 BNT will be distributed over an infinite time period. The distribution rate follows an exponential decay curve.

It will be an aggressive tapering off of inflation.

It will be an aggressive tapering off of inflation.

If you are still reading, I just want to say I appreciate you! This is getting a tad long now, but I’m going to wrap up shortly.

Additional features in v3:

• Third-party impermanent loss protection

• Integration of Chainlink Keepers to facilitate more efficient token burning

• A revamped front-end and single-click migration from Bancor V2 and other DeFi protocols.

• Third-party impermanent loss protection

• Integration of Chainlink Keepers to facilitate more efficient token burning

• A revamped front-end and single-click migration from Bancor V2 and other DeFi protocols.

All of this is just the DAWN phase.

According to Mark, these new features “just drop out of the contracts with the new architecture design.”

According to Mark, these new features “just drop out of the contracts with the new architecture design.”

But, the reasons those features exist is for yet to be announced products.

Bancor clearly has a lot more up their sleeves.

Mark did suggest to me that there is nothing currently in the industry like what Bancor has planned.

Bancor clearly has a lot more up their sleeves.

Mark did suggest to me that there is nothing currently in the industry like what Bancor has planned.

Parting Thoughts

Once Bancor V3 comes out of beta, I believe it could be the best place for the average DeFi user to park their idle assets and earn yield without the risk of IL.

Once Bancor V3 comes out of beta, I believe it could be the best place for the average DeFi user to park their idle assets and earn yield without the risk of IL.

In terms of the BNT token, I am not going to speculate on what happens with the price. But, I think we should see Bancor’s TVL swell, liquidity deepen and trading fees increase.

The ability to collaborate with other projects and DAOs is quite unique to Bancor and it’s clear that the protocol will become the home for many DAO treasuries.

I want to be balanced here as well. The DEX space is one of the most competitive verticals in crypto.

It is very hard to predict who the long term winners will be. We have so many players across many chains now, and accurately predicting who is still going to be here in five years is very, very difficult.

It’s entirely possible that Bancor still doesn’t manage to meaningfully chip away at Uniswap despite these upgrades.

I can't deny I am rooting for this protocol. They have really set about trying to solve DeFi pinch points and actually move the space on.

It's clear a ton of work has gone into V3, and the time it takes to actually innovate isn't always respected in this fast moving space.

It's clear a ton of work has gone into V3, and the time it takes to actually innovate isn't always respected in this fast moving space.

Bullish on OG teams who keep shipping you say?

I am hopeful Bancor v3 is going to be a leap forward for all DeFi users no matter the size of their capital.

In their words:

"Bancor3 is designed for the future of DeFi."

In their words:

"Bancor3 is designed for the future of DeFi."

Massive thanks to @MBRichardson87 from Bancor for taking the time to answer our questions and @here2defi for her help in organising the opportunity to talk with Mark.

If you enjoyed the thread then please RT the first tweet here and follow me @alpha_pls

And subscribe to the alpha please substack. It's free.

alphapls.substack.com

alphapls.substack.com

Loading suggestions...