The Basics of a Cash Flow Statement explained from scratch 🏧🎰🧮

In this thread we will talk about -

1. How Cash flow statement is made?

2. What is CFO,CFI and CFF?

3. Why is CFO/Ebitda important?

4. Finally, we will talk about Free Cash flow statement

Retweet for max reach!

In this thread we will talk about -

1. How Cash flow statement is made?

2. What is CFO,CFI and CFF?

3. Why is CFO/Ebitda important?

4. Finally, we will talk about Free Cash flow statement

Retweet for max reach!

A Cash flow statement shows inflow and outflow of cash and cash equivalents from various activities of a company during a particular period.

The net cash flow at the end of the year tells us about the movement of cash on the balance sheet.

The net cash flow at the end of the year tells us about the movement of cash on the balance sheet.

Why is cash flow important? ⤵️

Companies maintain books of accounts as per accrual principle, that means we book revenue or expense as and when it is incurred.

Companies maintain books of accounts as per accrual principle, that means we book revenue or expense as and when it is incurred.

Let's say we make sales of 10,000 so we will record it as when sale is completed and prepare P&L accordingly, here it doesn't matter whether cash is received or not.

Cash flow helps us in knowing whether that 10,000 has been received in cash or not.

Cash flow helps us in knowing whether that 10,000 has been received in cash or not.

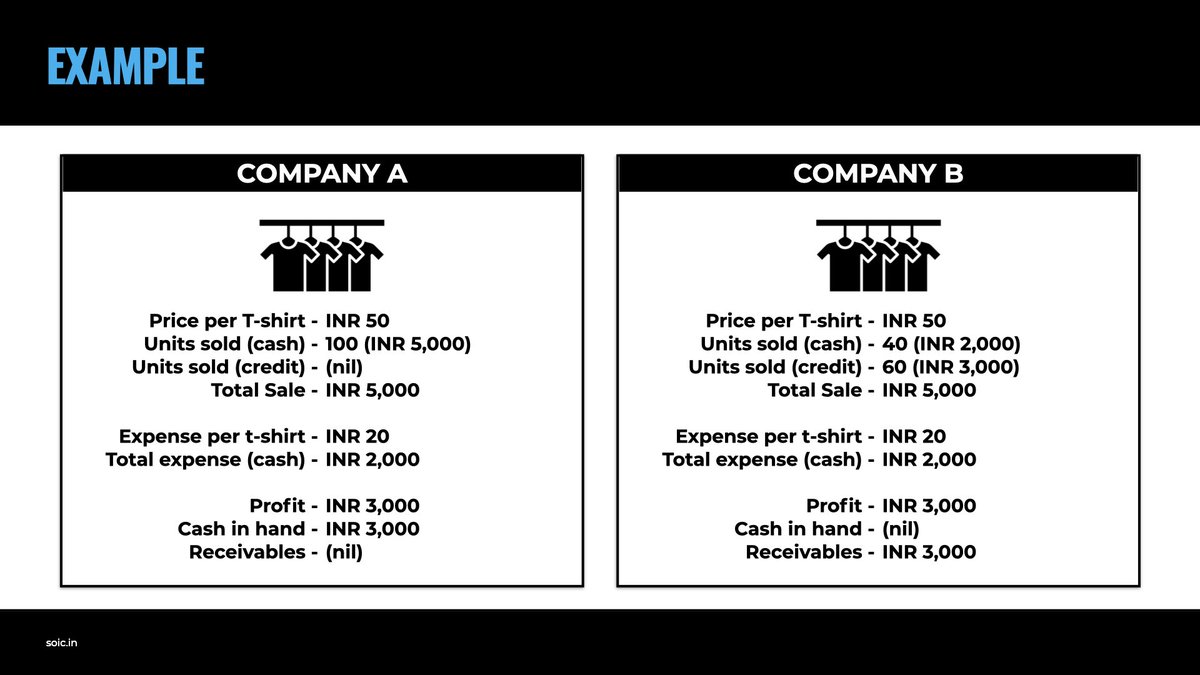

For Example:- There are 2 companies selling T-shirts and doing the following transactions:

1⃣ Company A did Sales of 100 units of a product at Rs. 50 per unit. All sales are in cash so they recorded the sales of Rs. 5000 and cash received is Rs. 5000.

Assuming the expenses are of Rs. 20 per unit so Company A recorded the profit of 3000 and A has this 3000 in cash.

Assuming the expenses are of Rs. 20 per unit so Company A recorded the profit of 3000 and A has this 3000 in cash.

2⃣Company B did Sales of 100 units of the same product at Rs. 50 per unit but out of this 100 only 40 units are sold in cash and other 60 units are sold on credit (you can give me money later).

So they recorded the sales of Rs. 5,000 here.

So they recorded the sales of Rs. 5,000 here.

The cost is 20 per unit so the total cost is 2,000. Now in P&L company has done the profit of 3,000 but when we look at its cash flow they have 0 cash profits when compared to Company A.

So here they recorded the sales of all 100 units as per accrual principal but received cash only for 40 units and the amount of remaining 60 units are receivable from debtors.

One can say quality of sales and cash flow is better for Company A. The reason why CFS is important

One can say quality of sales and cash flow is better for Company A. The reason why CFS is important

A cash flow statement can be broken down into three types:-

1⃣Cash Flow from Operating Activities

2⃣Cash Flow from Investing Activities

3⃣Cash Flow from Financing Activities

1⃣Cash Flow from Operating Activities

2⃣Cash Flow from Investing Activities

3⃣Cash Flow from Financing Activities

Cash Flow from operating activities: As the name suggests CFO gives us the details about cash generated by the company from its core business activities.

A simple way to remember this is, that whatever is to do with operations of the business is included in CFO.

A simple way to remember this is, that whatever is to do with operations of the business is included in CFO.

Whatever cash that isn’t earned from the operational activities is excluded or subtracted out.

Let’s dig deeper into it and see how it looks like with an example:

Laurus Labs CFO Statement🔽🔽

Laurus Labs CFO Statement🔽🔽

So as we can see it starts with profit before tax and after that we have to do some adjustments in that, let’s find the reasons for such adjustments:

1⃣Finance cost: Finance cost means interest paid on borrowings during the year. You will think why is it added back?

1⃣Finance cost: Finance cost means interest paid on borrowings during the year. You will think why is it added back?

Since this is not part of the day-to-day business activities, so it will be added back and will be covered in cash flow from financing activity.

2⃣Depreciation and Amortisation cost:

Depreciation means cost of Physical assets divided in years when assets will be used.

2⃣Depreciation and Amortisation cost:

Depreciation means cost of Physical assets divided in years when assets will be used.

For example, you bought an asset of Rs. 1 lakh which you will use for next 5 years so here depreciation amount will be Rs. 20,000 (Rs. 1,00,000 / 5 yrs). Now you will charge this 20k per year in P&L as Depreciation.

(Assuming Salvage value is 0)

Why is this added back?

(Assuming Salvage value is 0)

Why is this added back?

As my cash outflow is -100,000 in Year 1 to purchase the asset, so the 20,000 per year is non cash expense so it will be added back.

This is why Depreciation is known as a Non cash expense and is added back to PBT while calculating Cash flow from operations.

This is why Depreciation is known as a Non cash expense and is added back to PBT while calculating Cash flow from operations.

3⃣Profit/ loss on sale of Assets or Investment:

Since these are not part of my core business activities it will be adjusted here, if sold at a gain then we will reduce it from PBT or if at a loss then we will add it back.

Eg:- Selling Excess Land the business has at a gain.

Since these are not part of my core business activities it will be adjusted here, if sold at a gain then we will reduce it from PBT or if at a loss then we will add it back.

Eg:- Selling Excess Land the business has at a gain.

4⃣Dividend Income: Dividend income is also not part of business activities so it will be subtracted while calculating Cash from operations. This is included under Cash Flow from Investing activities.

(More on that later)

(More on that later)

After these adjustments we reach to Operating profit before working capital changes.

Now we will be required to adjust working capital changes, but before going to that lets understand the meaning of working capital.

Now we will be required to adjust working capital changes, but before going to that lets understand the meaning of working capital.

Working capital means the capital of a business which is used in its day-to-day trading operations.

Working capital adjustments:

When assets increase we deduct it from operating profit and when assets decrease we add it into operating profit.

Working capital adjustments:

When assets increase we deduct it from operating profit and when assets decrease we add it into operating profit.

So there is an inverse relationship in working capital changes.

When liabilities increase we add it in operating profit before working capital changes because it is fund inflow whereas if liabilities decreases we deduct it from operating profits because it is fund outflow.

When liabilities increase we add it in operating profit before working capital changes because it is fund inflow whereas if liabilities decreases we deduct it from operating profits because it is fund outflow.

For Example:- when a company buys more inventory, current assets increase. This positive change in inventory is subtracted because it is seen as a cash outflow.

It’s the same case for accounts receivable. When it increases, it means the company sold their goods on credit.

It’s the same case for accounts receivable. When it increases, it means the company sold their goods on credit.

On the other hand, if a current liability item such as accounts payable increases, this is considered a cash inflow because the company has more cash to keep in its business, so this is then added back.

Thus, Always remember these 4 things when it comes to working capital movement:-

1. When current assets increase🔼, your cash flow decreases🔽.

2. When Current assets Decrease🔽, your cash flow increases🔼.

3. When current Liabilities increase🔼, your cash flow Increases🔼.

1. When current assets increase🔼, your cash flow decreases🔽.

2. When Current assets Decrease🔽, your cash flow increases🔼.

3. When current Liabilities increase🔼, your cash flow Increases🔼.

4. When Current Liabilities Decrease🔽, your cash flow decreases 🔽

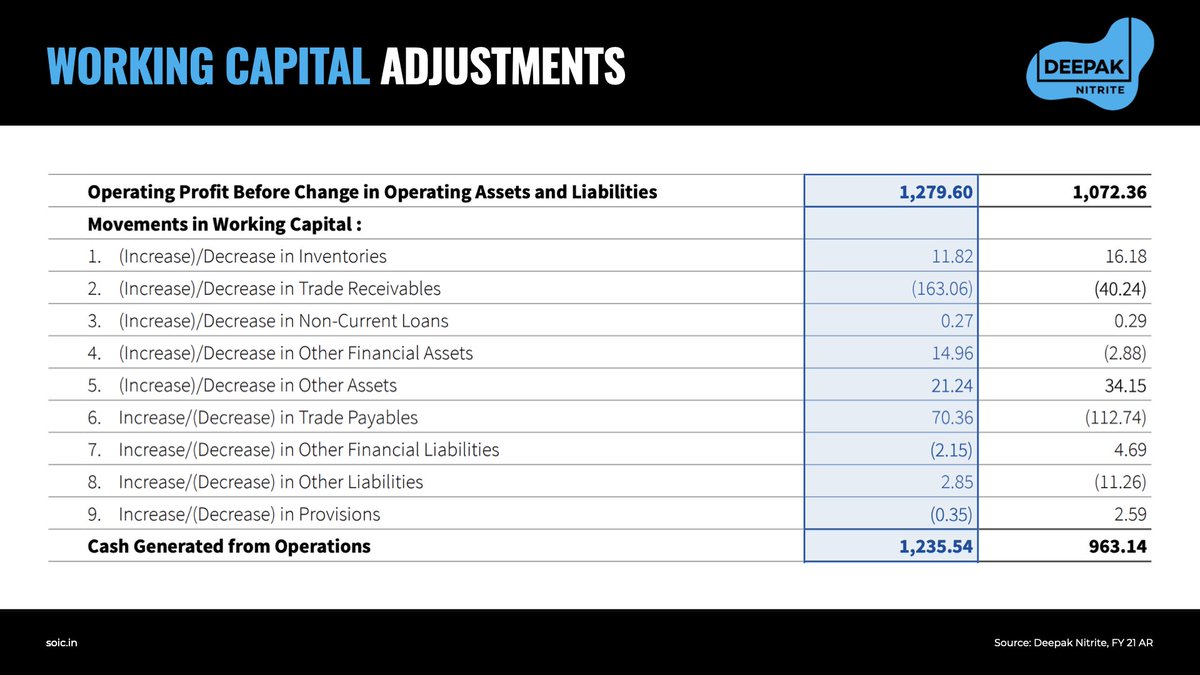

Let’s see it in the example of Deepak Nitrite:

Let’s see it in the example of Deepak Nitrite:

After all the working capital adjustments we reach to cash generated from operations and here we are left with one last adjustment of Taxes Paid to get Net cash generated from operating activities.

Income Tax paid: In the last adjustment of CFO we deduct the income tax paid.

Here income tax will be deducted which is actually paid during the year. These are also known as cash taxes paid.

Here income tax will be deducted which is actually paid during the year. These are also known as cash taxes paid.

After adjusting the tax paid we will come to the final destination of Net cash flow from operating activities.

Now we look into the key ratio which needs to be tracked with respect to CFO:

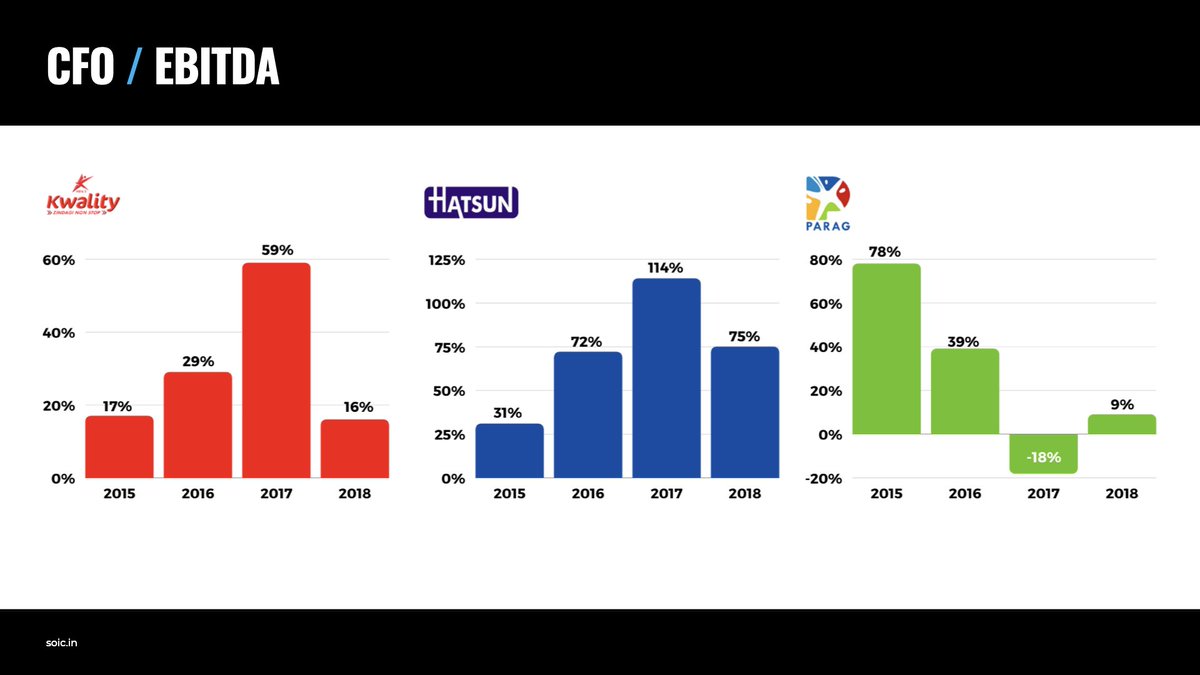

CFO to EBITDA: CFO to EBITDA (Earnings before Interest, Tax, Depreciation and Amortization) will reflect whether operating profit is converting into cash or not.

CFO to EBITDA: CFO to EBITDA (Earnings before Interest, Tax, Depreciation and Amortization) will reflect whether operating profit is converting into cash or not.

A good conversion should be 70% when it comes to B2C business and should be at least 60% when it comes to B2B business.

It can be used as a matrix to compare peers and their quality of revenue in the same sector!

For Example:- All 3 companies from the milk sector🔽🔽

It can be used as a matrix to compare peers and their quality of revenue in the same sector!

For Example:- All 3 companies from the milk sector🔽🔽

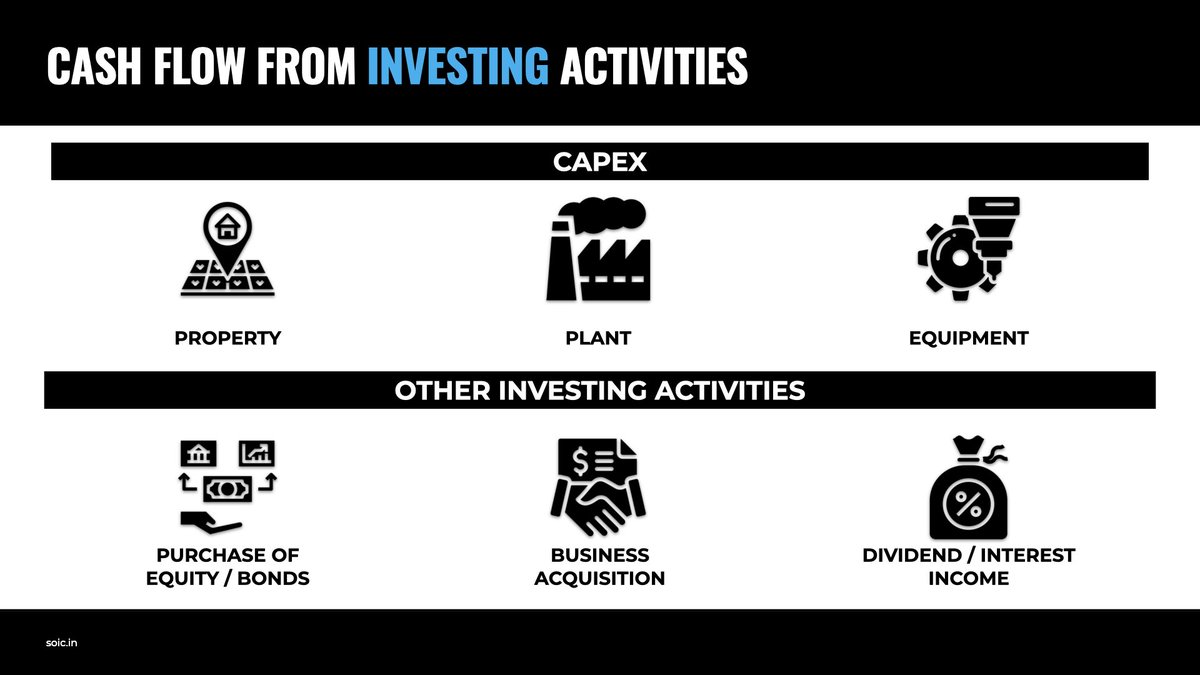

Cash Flow from Investing Activities:

Whenever you do any investment for the future or receive interest from your investments. Then all such cash generated or used is termed under cash flow from investing activities.

Whenever you do any investment for the future or receive interest from your investments. Then all such cash generated or used is termed under cash flow from investing activities.

Investing activities are the acquisition and disposal of long-term assets and investments. Investing activities relate to purchase and sale of long-term assets or fixed assets such as machinery, furniture, land and building, etc.

All items under CFI 🔽🔽🔽

All items under CFI 🔽🔽🔽

Thus,

1⃣ Whenever a business purchases a Fixed asset. It is shown as a cash outflow under CFI. Shown as negative.

2⃣ Whenever a business sells assets, it is shown as positive cash inflow. Thus, cash flowing in under CFI.

1⃣ Whenever a business purchases a Fixed asset. It is shown as a cash outflow under CFI. Shown as negative.

2⃣ Whenever a business sells assets, it is shown as positive cash inflow. Thus, cash flowing in under CFI.

3⃣ Whenever a business earns dividends, it is Cash inflow under Cash flow from investing activities.

P.S. Always remember, all capital expenditure of a business reflects under CFI statement.

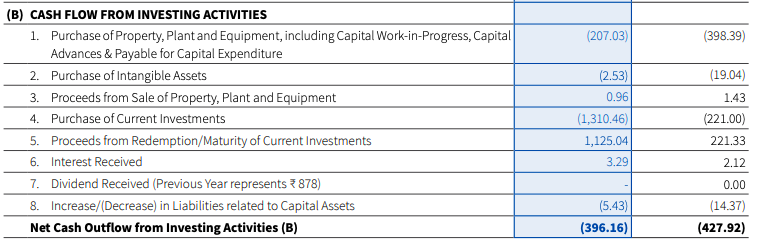

Example:- CFI statement of Deepak Nitrite ⤵️⤵️

P.S. Always remember, all capital expenditure of a business reflects under CFI statement.

Example:- CFI statement of Deepak Nitrite ⤵️⤵️

Finally the last one,

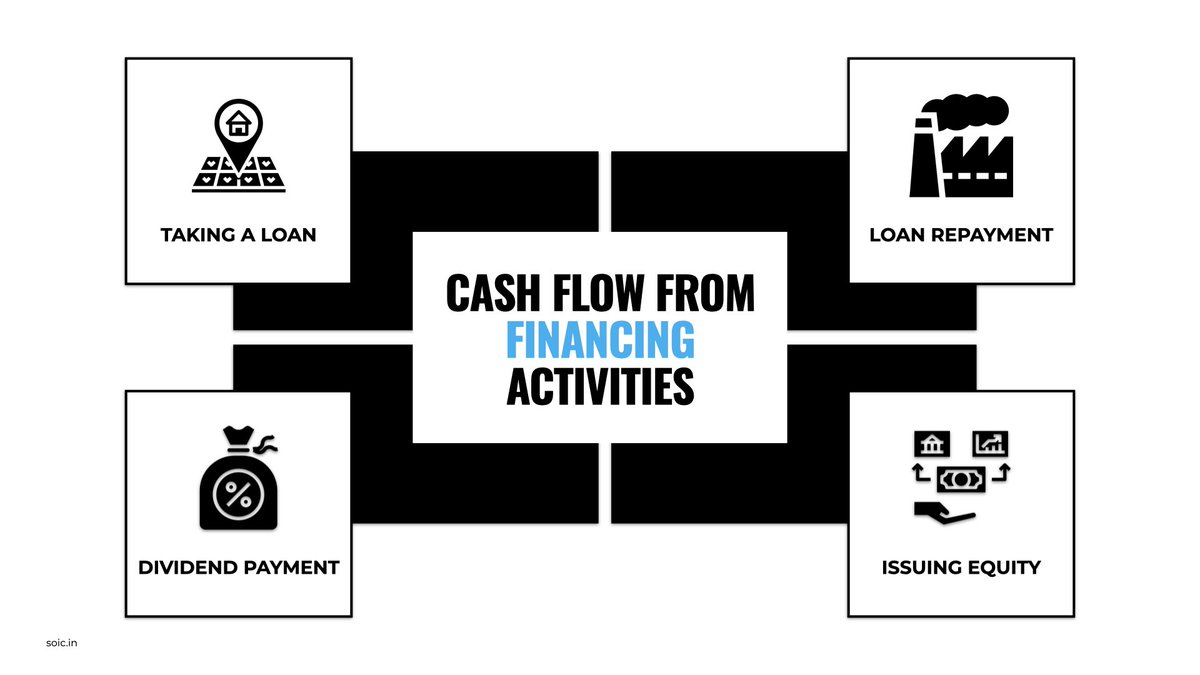

Cash Flow from Financing Activities:-

Financing activities are those activities which a company uses to fund its business like borrowings, repayment of borrowings, issue of equity, buyback or payment of dividend.

Includes all these items:-

Cash Flow from Financing Activities:-

Financing activities are those activities which a company uses to fund its business like borrowings, repayment of borrowings, issue of equity, buyback or payment of dividend.

Includes all these items:-

Whenever a business raises debt or borrowings then it shown as positive cash inflow under Cash Flow from Financing Activities. When a business repays borrowings, funds flow out. Thus, it shown as cash outflow under Financing activities.

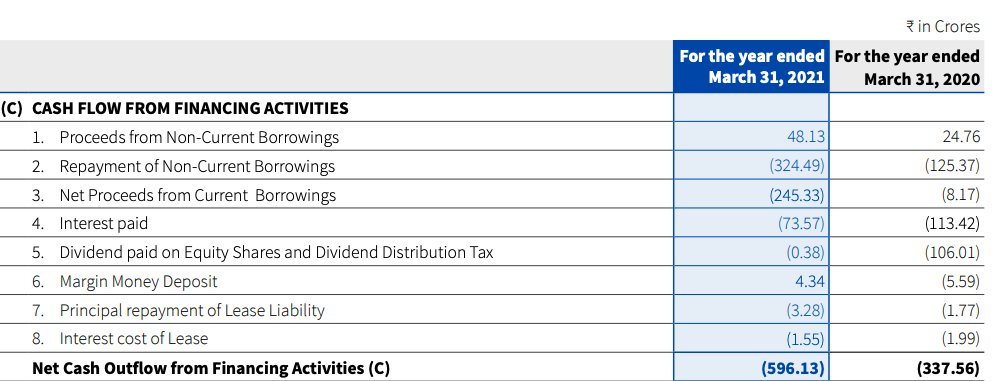

Just look at CFF of Deepak Nitrite⤵️

Just look at CFF of Deepak Nitrite⤵️

How all the three interact?

Coming to the important concept of Net cash flow.

If you add Cash flow from operations+Cash flow from Investing activities+Net cash flow from Financing activities.

You get to the net cash generated by the the business in a given period :)

Coming to the important concept of Net cash flow.

If you add Cash flow from operations+Cash flow from Investing activities+Net cash flow from Financing activities.

You get to the net cash generated by the the business in a given period :)

In Deepak Nitrite's case-

Cfo=999 Crores

CFI=-396 crores

CFF=-596 crores

Net cash flow= 6.75 crores

Which reflect in the Net cash flow statement and in the movement of cash in current assets on the balance sheet as compared to the last year🔽🔽

Cfo=999 Crores

CFI=-396 crores

CFF=-596 crores

Net cash flow= 6.75 crores

Which reflect in the Net cash flow statement and in the movement of cash in current assets on the balance sheet as compared to the last year🔽🔽

Thank you so much for reading. If you understood Cash flow from operational activities, Cash flow from investing activities, Cash flow from Financing activities and Net Cash Flow. Do consider retweeting this thread!

---The End---

---The End---

Everything about Free Cash Flow:-

Loading suggestions...