Meghmani finechem ltd. Conducted their Q4 & FY 22 conference call today.

“ Aim to generate 5000+ crore of Revenue from operations by 2027”

Here are the key takeaways..

“ Aim to generate 5000+ crore of Revenue from operations by 2027”

Here are the key takeaways..

Business overview

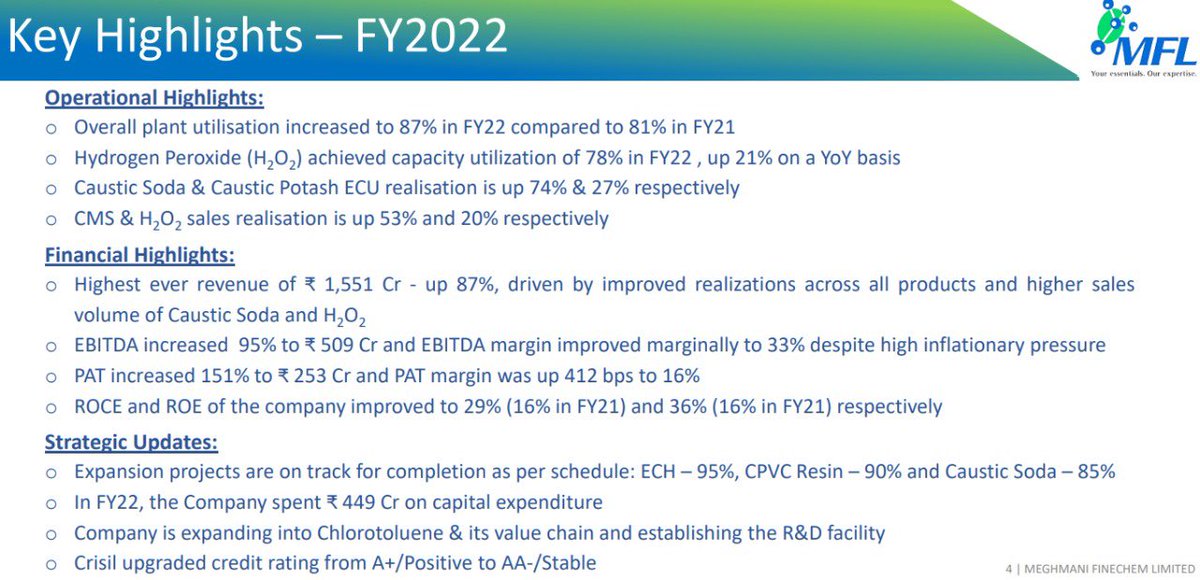

- The manufacturer and seller of Chloe alkali and value added derivatives has delivered great results during this period.

- They have increased the capacity utilisation of H2O2 by 21% on YoY basis.

- The manufacturer and seller of Chloe alkali and value added derivatives has delivered great results during this period.

- They have increased the capacity utilisation of H2O2 by 21% on YoY basis.

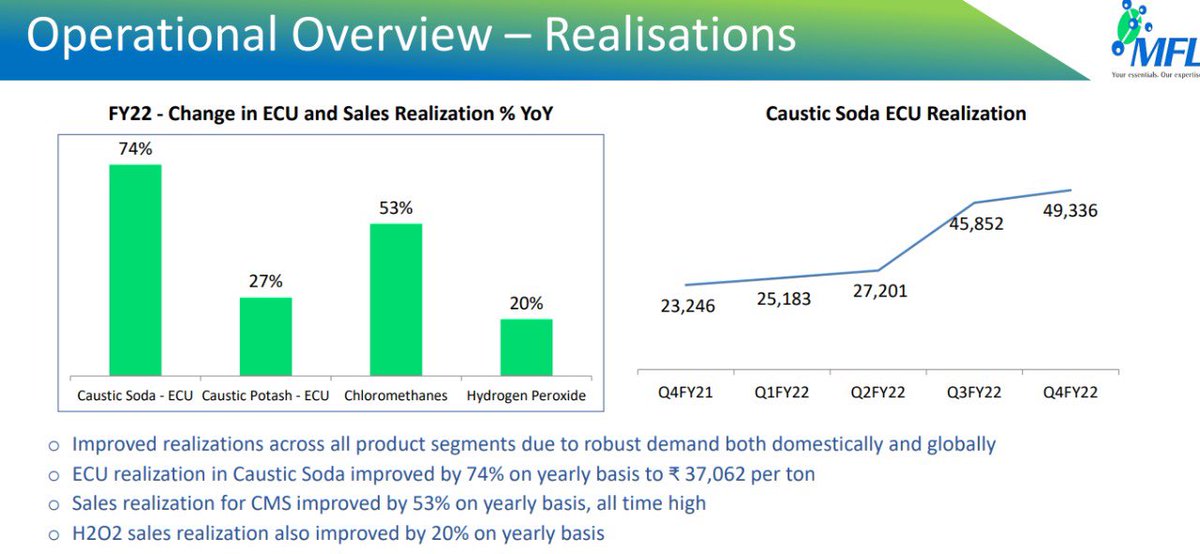

- For caustic soda and caustic potash ECU their realisation were up by 74% and 27% respectively.

- In terms of Revenue break-up 74% of the revenue comes from Chlor-Alkali segment and rest 26% comes from derivatives business.

- In terms of Revenue break-up 74% of the revenue comes from Chlor-Alkali segment and rest 26% comes from derivatives business.

- The ECU demand is increasing a lot from a variety of areas and along with this there are logistics challenges are there due to which local demand has increased which acts beneficial for them.

Expansion

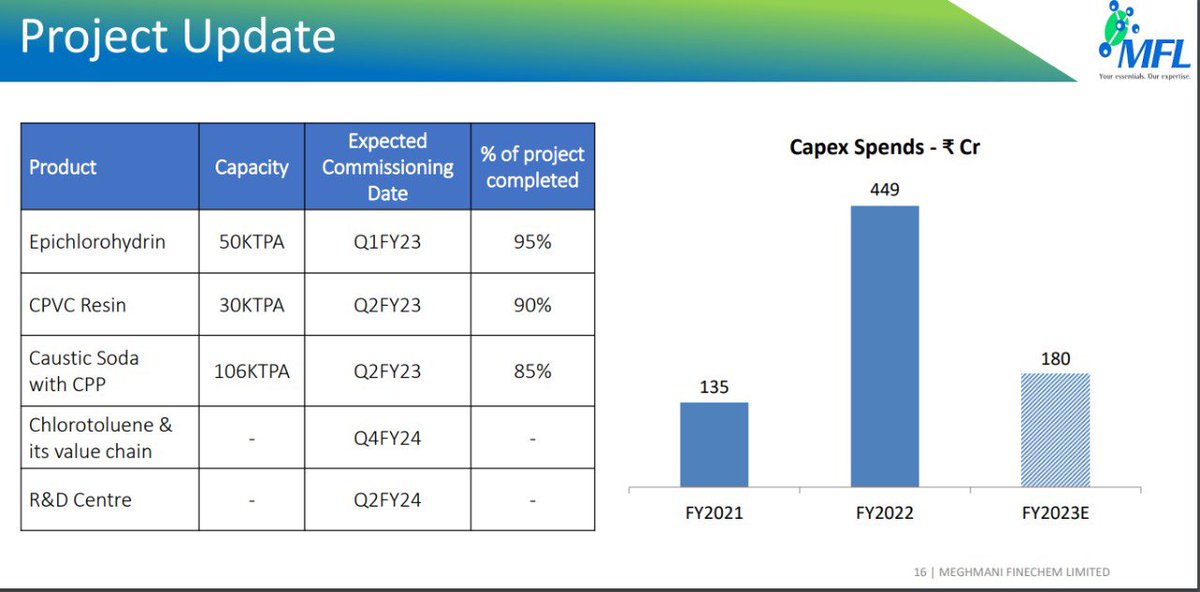

- The company is on its track for completion of its projects.

ECU -95%

CPVC Resin -90%

Caustic Soda -85% levels are completed.

- For FY22, the company has spent 450 crores approximately.

- They are expanding their business into chlorotoluene and it’s value chain.

- The company is on its track for completion of its projects.

ECU -95%

CPVC Resin -90%

Caustic Soda -85% levels are completed.

- For FY22, the company has spent 450 crores approximately.

- They are expanding their business into chlorotoluene and it’s value chain.

- They are also establishing a research facility for upcoming projects.

- For FY 23 they for now has a capex expenditure plan of 180 crore and will increase it as per need.

- They also aim to maintain a Sales growth of approx 50%

- For FY 23 they for now has a capex expenditure plan of 180 crore and will increase it as per need.

- They also aim to maintain a Sales growth of approx 50%

- From the new caustic capacity that are going be ready from FY23, the company is skeptical to comment on its future growth.

- India being a net exporter of caustic business, looking at current levels they have good export growth for the company.

- India being a net exporter of caustic business, looking at current levels they have good export growth for the company.

- The margins are expected to be same and volumes are expected to increase with their high value products.

- The company is able to maintain their margins because they are able to pass majority of their cost to customers.

- The company is able to maintain their margins because they are able to pass majority of their cost to customers.

- Once a year an update is to be made to the caustic soda business and ECU business to meet all the demand of the industry.

- The above mentioned 50% growth, is possible due to sectors like paper. With increase in use of their caustic.

- The above mentioned 50% growth, is possible due to sectors like paper. With increase in use of their caustic.

- For next period, with new businesses the company looks bullish from pharma, household, water treatment and paper industries.

- The next 5 years will bring double digit growth for their ECU business.

- It’s important to note company has done just 5% of export business.

- The next 5 years will bring double digit growth for their ECU business.

- It’s important to note company has done just 5% of export business.

- Moderation will be done into the business as per the market situation.

- The above mentioned 3 business will add approximately 1000 crore revenue in times to come.

- To achieve 5000 crores revenue target all projects will be taken on Step by step basis

- The above mentioned 3 business will add approximately 1000 crore revenue in times to come.

- To achieve 5000 crores revenue target all projects will be taken on Step by step basis

Financials

- Company has generated highest sales ever of 1551 crore up by 87% compared to previous year.

- This is mainly due to better realisation and higher volume of caustic soda and H2O2.

- The company has been able to improve its EBITDA margins despite inflation.

- Company has generated highest sales ever of 1551 crore up by 87% compared to previous year.

- This is mainly due to better realisation and higher volume of caustic soda and H2O2.

- The company has been able to improve its EBITDA margins despite inflation.

- Their PAT margins were up to 16% during this period and have increased by 151%.

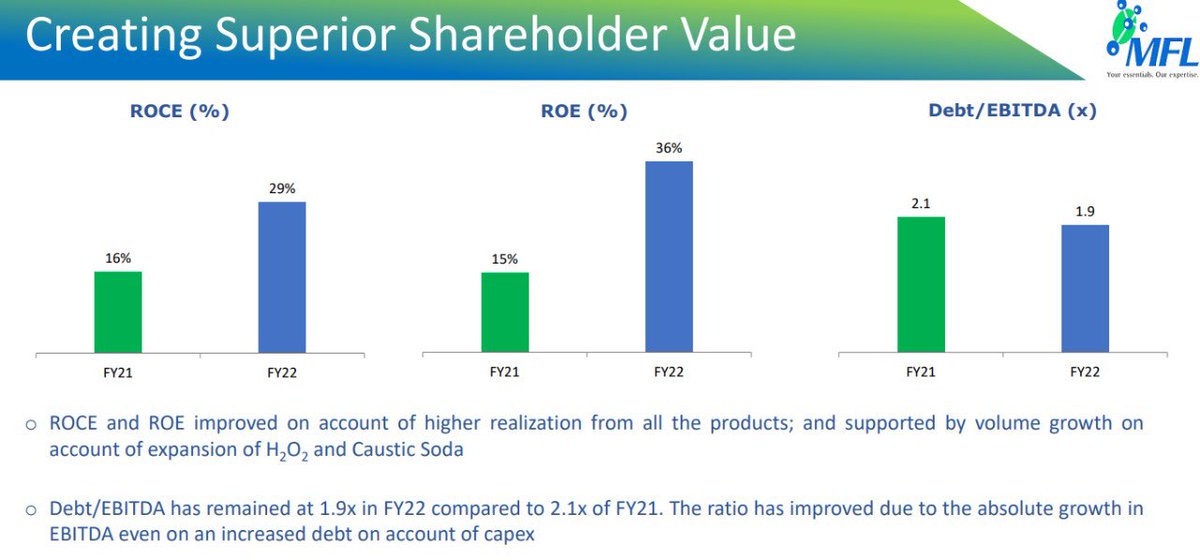

- ROCE and ROE of the company has also improved to 30% approx double from FY21 levels.

- The company expected a better asset turnover for their business

- ROCE and ROE of the company has also improved to 30% approx double from FY21 levels.

- The company expected a better asset turnover for their business

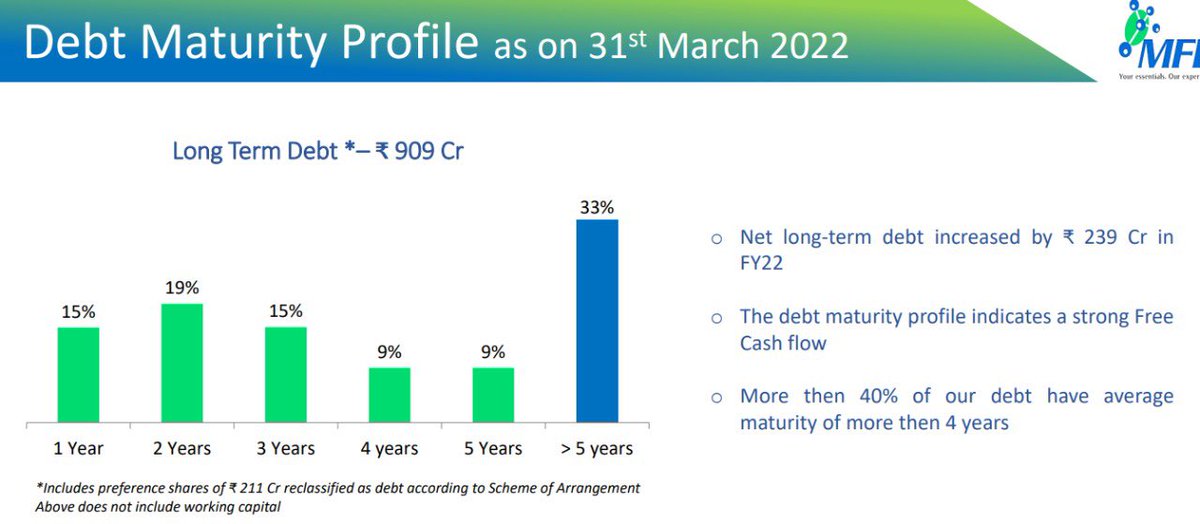

- In terms of debt profile, company has a long term debt of 909 crore.

- 239 crore were recently added to this term.

- In this more then 40% of the debt has a maturity of more then 4 years.

- They have a target to sustain their net debt to ebitda at 2.0x

- 239 crore were recently added to this term.

- In this more then 40% of the debt has a maturity of more then 4 years.

- They have a target to sustain their net debt to ebitda at 2.0x

- Now debts it’s at its peak levels and further investment will be through internal accruals and a constant debt payment of 150-200 crores will be done without fail

- By looking at their historic income statement there has been a constant decline in their gross margin levels since FY 19.

- And is first time since FY 18 that their PAT margins have moved up compared to last year.

- In present levels, the caustic are in price range of 50000.

- And is first time since FY 18 that their PAT margins have moved up compared to last year.

- In present levels, the caustic are in price range of 50000.

- One of the highest cost that company incurred is its energy cost.

- For last year, 7.67 avg per unit price was paid. And it is likely to increase further.

- The company has a location near port so they import it from Indonesia.

- For last year, 7.67 avg per unit price was paid. And it is likely to increase further.

- The company has a location near port so they import it from Indonesia.

- With this they just maintain coal stock for 3-4 weeks.

- This increasing cost is less of their concern as they are able to pass on its cost to customers. So, they don’t hedge.

- At present levels, current cost of acquisition is very difficult to tell.

- This increasing cost is less of their concern as they are able to pass on its cost to customers. So, they don’t hedge.

- At present levels, current cost of acquisition is very difficult to tell.

- 211 crore preference share a provision is made of 8% interest and will be paid on yearly basis and not on quarterly basis.

- In next 2 months before 30th June first payment will be made.

- Their redemption is in 20 years and company is not expecting to redeem it for now.

- In next 2 months before 30th June first payment will be made.

- Their redemption is in 20 years and company is not expecting to redeem it for now.

- This will be based upon the following factors

Free cash flow

Dividend policy

Market situation

Free cash flow

Dividend policy

Market situation

Loading suggestions...