Economics

Finance

Investing

Market Analysis

Investment

Lockdown

Political Commentary

Inflation

Monetary Policy

Energy crisis

Currency Devaluation

Market liquidity

Yield

ISM PMI

Defensive Investment

Policymakers

DXY

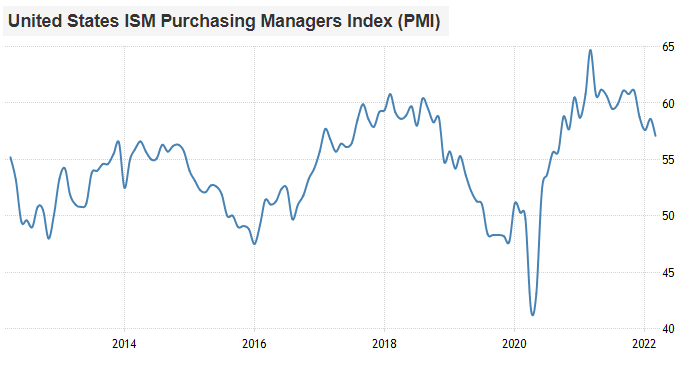

The Fed is going to tighten monetary policy until something breaks. Something like Treasury market liquidity or credit market liquidity. While ISM PMI is declining.

Being defensive makes sense until a pivot occurs. A diverse base mix of cash, gold, defensive value equities, etc.

Being defensive makes sense until a pivot occurs. A diverse base mix of cash, gold, defensive value equities, etc.

Despite me being a broad long-term inflationist for the 2020s decade, this defensive angle has been my tactical view since mid-December 2021.

Every inflationary period in history has attempted counter-moves by policymakers. From my Dec 12th 2021 report:

Every inflationary period in history has attempted counter-moves by policymakers. From my Dec 12th 2021 report:

-Europe has a self-imposed energy crisis.

-China has a self-imposed lockdown problem.

-Japan has a self-imposed currency devaluation (they didn't need to pin yields quite that low).

DXY shooting up, meaning foreign sector has trouble buying Treasuries. So, most assets go down.

-China has a self-imposed lockdown problem.

-Japan has a self-imposed currency devaluation (they didn't need to pin yields quite that low).

DXY shooting up, meaning foreign sector has trouble buying Treasuries. So, most assets go down.

The DXY is reaching higher than my base case, due to policymaker decisions outside of my base case.

Therefore, we need to be aware of the market issues that occur when this happens.

It's no milkshake (eg US increases rates and gets equity buy-in) but rather, all assets suffer.

Therefore, we need to be aware of the market issues that occur when this happens.

It's no milkshake (eg US increases rates and gets equity buy-in) but rather, all assets suffer.

If most assets go down, US tax income suffers, and deficit widens. More Treasuries issued.

If foreigners aren't aggressively buying Treasuries, it means the Fed or someone has to buy them. If private sector buys them, it is in place of equities. If Fed buys them, it's a pivot.

If foreigners aren't aggressively buying Treasuries, it means the Fed or someone has to buy them. If private sector buys them, it is in place of equities. If Fed buys them, it's a pivot.

Consumer spending is over 2/3rds of US GDP, and is concentrated within the top 10%.

If house prices, stock prices, and so forth go down, it means the 10% people will be more cautious with spending, aka consumerist GDP weakens.

If house prices, stock prices, and so forth go down, it means the 10% people will be more cautious with spending, aka consumerist GDP weakens.

To quantify it, if US debt is $30 trillion and US weighted average cost of capital reaches as high as 3%, then the federal interest expense alone would be $900 billion. Adding the deficit angle gets to well over $1 trillion that needs financing each year.

Asset prices and GDP estimates get weird, therefore, until a pivot occurs.

Due to Fed mandates (control inflation at the cost of employment), the pivot occurs only when something in financial markets breaks.

So, things get bad -> things break -> policy reversal.

Due to Fed mandates (control inflation at the cost of employment), the pivot occurs only when something in financial markets breaks.

So, things get bad -> things break -> policy reversal.

Loading suggestions...