Spent some time tonight updating my #uranium enrichment graphics. A monolithic SWU price doesn't really tell us anything without context. I'll walk through a few examples below.

You can follow my math on Urenco's handy SWU calculator: urenco.com

You can follow my math on Urenco's handy SWU calculator: urenco.com

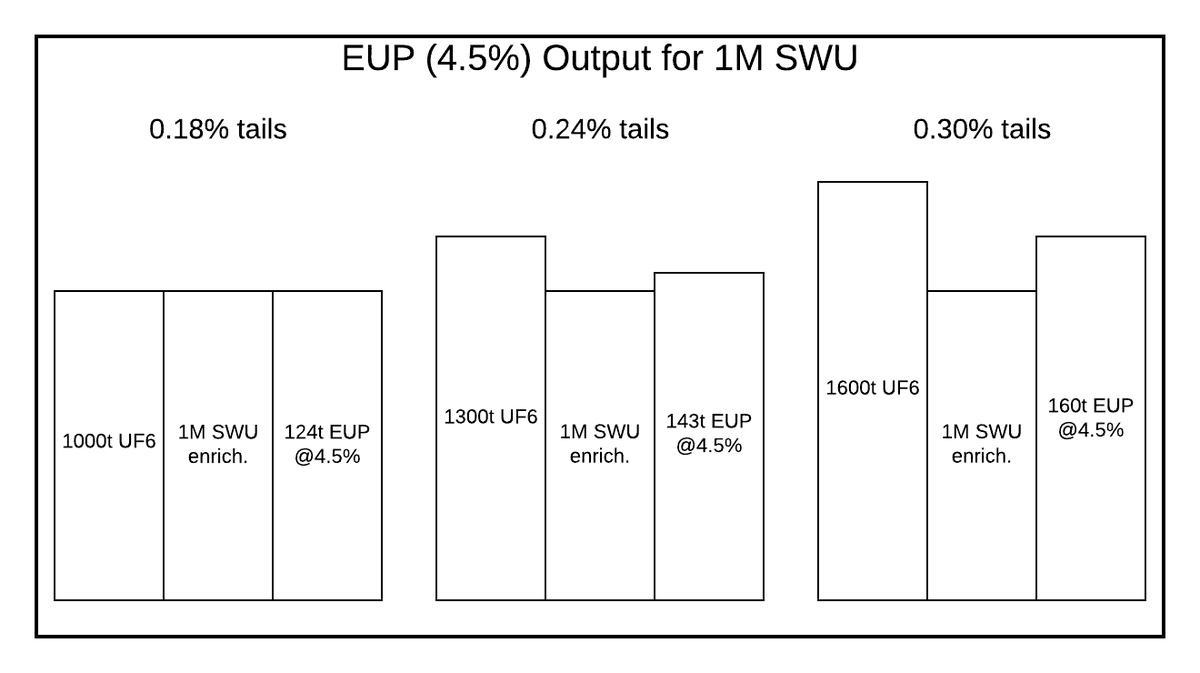

Tails assay is the residual uranium-235 contained in enrichment facility waste ("tails"). Over the last 10 years, average tails assay has crept down from 0.30% to 0.18% (or lower).

Tails assay governs the ratio of uranium to enrichment work (SWU) used to make enriched uranium.

Tails assay governs the ratio of uranium to enrichment work (SWU) used to make enriched uranium.

To produce one kilogram of uranium mass (kgU) contained in enriched uranium product (EUP) at 4.5% enrichment assay, the amount of uranium and enrichment required varies based on the tails assay.

[Handy tip - 1 kgU of UF6 contains 2.61285 pounds of U3O8.]

[Handy tip - 1 kgU of UF6 contains 2.61285 pounds of U3O8.]

You can think of SWU ("separative work units") as a cost to swap a quantity of natural uranium for a quantity of enriched uranium. The ratio of components is determined by the tails assay.

For existing centrifuges, this trade is governed by the replacement cost of UF6.

For existing centrifuges, this trade is governed by the replacement cost of UF6.

Looking at it from the other side, enrichment facilities have a nominal capacity in SWU per year. Operators of enrichment facilities try to choose an operational tails assay for their facility which maximizes their revenue across their current contract book and future sales.

Imagine an enrichment facility with a capacity of 1 million SWU/year. From 0.18% to 0.30% tails, there is a 30% increase in EUP produced by 1M SWU but it requires 60% more uranium feed to do so.

SWU at a lower tails assay commands a higher price per SWU, as it reduces UF6 costs.

SWU at a lower tails assay commands a higher price per SWU, as it reduces UF6 costs.

Now, both enrichers and their utility customers have access to roughly the same information on the public nuclear fuel market - but opinions and internal projections vary so contractual tails assay is a good leading indicator for forward uranium price sentiment in "good times."

If Western utilities lose access to Russian supply, it means that they need more EUP from Western sources. In the very short term, this means that Western enrichment facilities must be recalibrated to produce more EUP (i.e. operated at a higher tails assay).

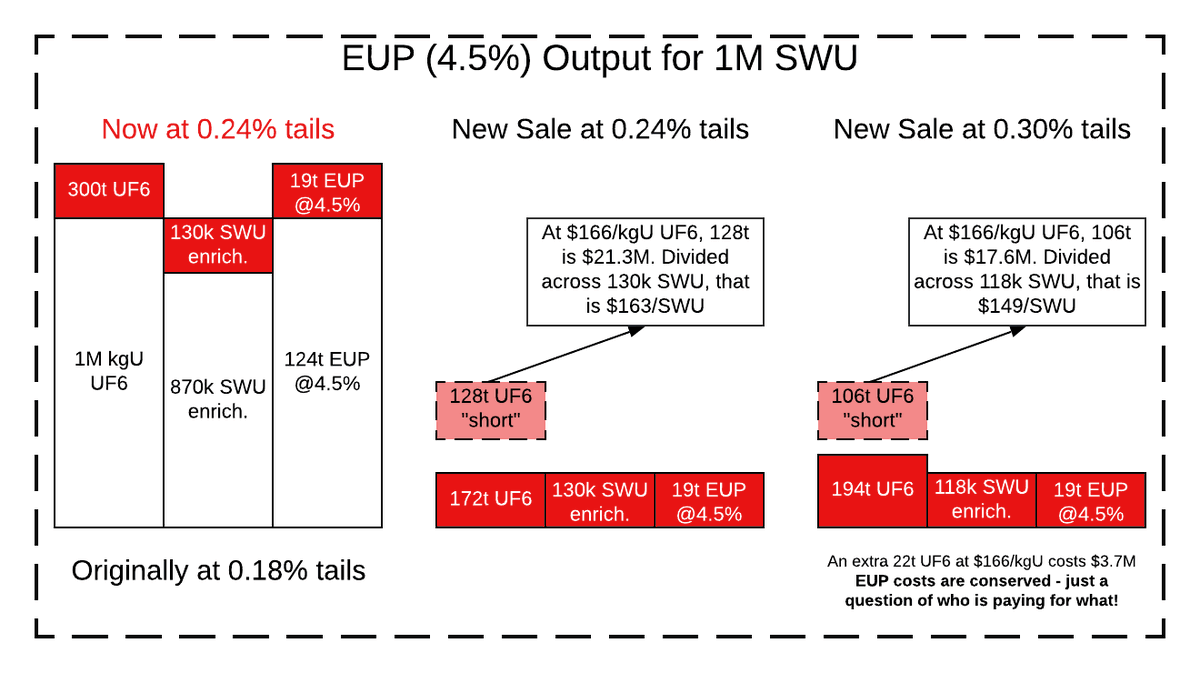

If our 1M SWU plant needs to increase its EUP output by 15%, operating at 0.24% tails instead of 0.18% will produce an additional 19t of 4.5% EUP (15% more).

But it will require 300t more UF6 as feed.

Who pays for that extra UF6? The utilities who need the extra EUP, of course!

But it will require 300t more UF6 as feed.

Who pays for that extra UF6? The utilities who need the extra EUP, of course!

Some of the 300t UF6 feed gap will be provided by the utility as part of the transaction.

A sale for 19t EUP at 0.24% tails will deliver 172t UF6 as feed material, so the remaining 128t shortfall will be distributed across the 130k SWU to form an ad-hoc SWU price ($163/SWU).

A sale for 19t EUP at 0.24% tails will deliver 172t UF6 as feed material, so the remaining 128t shortfall will be distributed across the 130k SWU to form an ad-hoc SWU price ($163/SWU).

[To be explicit - the 128,000 kgU shortfall at $166/kgU is worth $21.3M. That $21.3M is distributed over the nominal quantity of 130,000 SWU in the transaction, which comes out to about $163/SWU. The SWU aren't "real" outside of the sense that they are standing in for the UF6.]

A higher tails assay (0.30%) will deliver more UF6 in the transaction, so the resulting SWU price will be lower.

But if the utility is buying that UF6 at the prevailing market price, their savings on SWU will be spent on the UF6 they are delivering as part of the transaction.

But if the utility is buying that UF6 at the prevailing market price, their savings on SWU will be spent on the UF6 they are delivering as part of the transaction.

Now, these hypothetical SWU prices are higher than the values you're seeing in the trade press, but this exercise should at least give you an idea of how an overfeeding-SWU price might form in relation to values we can estimate (how much more EUP do we need? what does UF6 cost?).

What this means in uranium-land is that, over the next few years, Western tails assay will increase and uranium requirements will increase with it.

What this means in conversion-land is that there's a sudden prompt demand for conversion services. Conversion is the bigger story.

What this means in conversion-land is that there's a sudden prompt demand for conversion services. Conversion is the bigger story.

Almost lost in this discussion is:

*NEW ENRICHMENT CAPACITY*

Centrifuges can't be built overnight, but published SWU prices + contracting appetite are converging into the previously-unthinkable deployment of new enrichment capacity. That's your takeaway - new tubes soon (maybe)

*NEW ENRICHMENT CAPACITY*

Centrifuges can't be built overnight, but published SWU prices + contracting appetite are converging into the previously-unthinkable deployment of new enrichment capacity. That's your takeaway - new tubes soon (maybe)

Final thought - there's currently no ban on Russian EUP imports to the US and Western Europe. And the US could move in a different direction than Europe on this issue. Nothing is written in stone (yet), so treat this as a potential outcome rather than a certain one.

@casperj33081634 SWU is a derived unit so it’s not really a market in the same way uranium is. Prices are going up, but it is more accurate to say that those prices represent the near-term opportunity cost of changing the operational parameters of enrichment facilities.

Loading suggestions...