1/ $FB/Meta 1Q'22 Update

Phew! Meta is NOT dead. Well, at least, not yet.

Even after +20% AH, Meta's "Family of Apps" is still likely priced to be terminally ill business, and its shiny new "Reality Labs" is likely priced to be worth negative!

Here's my notes.

Phew! Meta is NOT dead. Well, at least, not yet.

Even after +20% AH, Meta's "Family of Apps" is still likely priced to be terminally ill business, and its shiny new "Reality Labs" is likely priced to be worth negative!

Here's my notes.

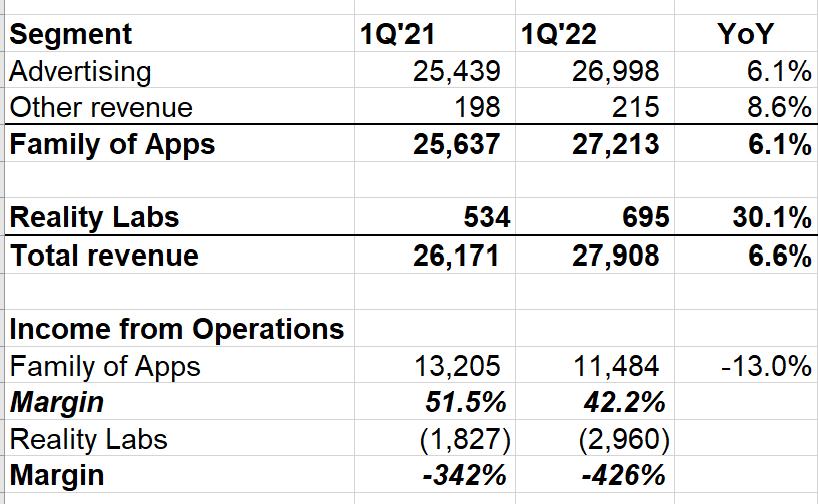

2/ Family DAP and MAP both +6% YoY

Facebook DAU +4% YoY, MAU +3% YoY

# of ad impressions +15% YoY (down YoY in North America, but decline is lower than in Q4), price per ad -8%

Facebook DAU +4% YoY, MAU +3% YoY

# of ad impressions +15% YoY (down YoY in North America, but decline is lower than in Q4), price per ad -8%

3/ Revenue growth by geography:

NA +1%

Europe flat

APAC +20%

RoW +21%

Total revenue +6.6% YoY (+10% adj for FX), but 2-yr and 3-yr CAGR still pretty healthy.

As costs continue to grow faster than revenue, operating margins continue to go down over time.

NA +1%

Europe flat

APAC +20%

RoW +21%

Total revenue +6.6% YoY (+10% adj for FX), but 2-yr and 3-yr CAGR still pretty healthy.

As costs continue to grow faster than revenue, operating margins continue to go down over time.

4/ While Reality Labs grow much faster (low base), it continues to be an immense cash burning exercise. For better or worse, only a founder with majority voting power can possibly think of doing this!

FoA margins are also down by 931 bps QoQ.

FoA margins are also down by 931 bps QoQ.

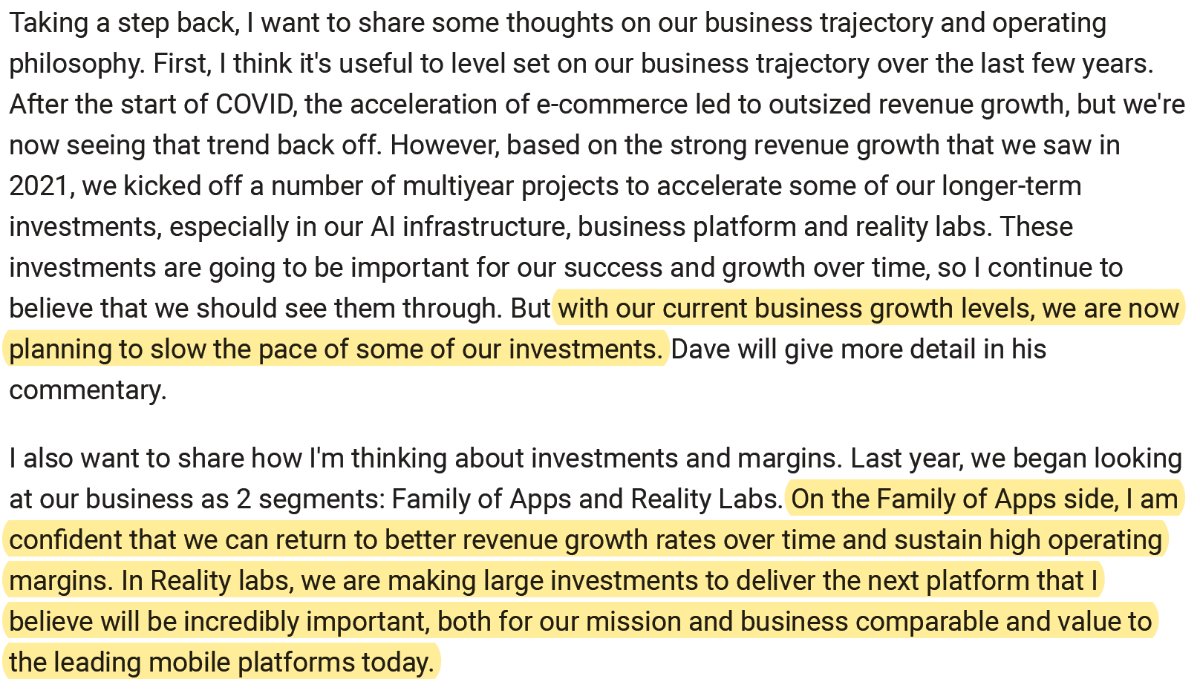

5/ "with our current business growth levels, we are now planning to slow the pace of some of our investments."

"On the Family of Apps side, I am confident that we can return to better revenue growth rates over time and sustain high operating margins."

"On the Family of Apps side, I am confident that we can return to better revenue growth rates over time and sustain high operating margins."

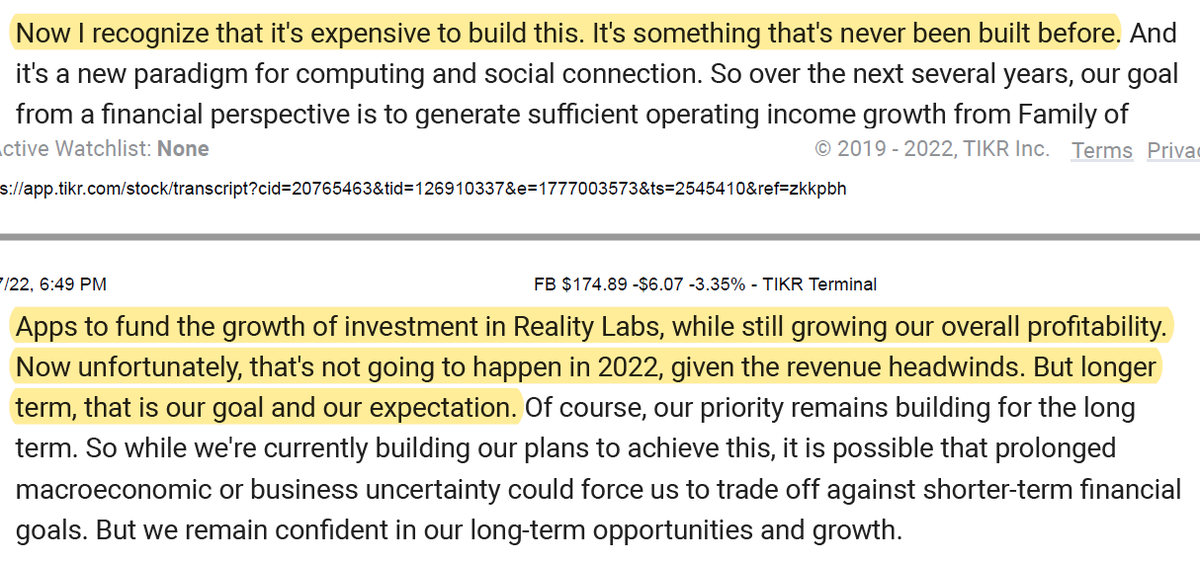

6/ "Now I recognize that it's expensive to build this. It's something that's never been built before...our goal from a financial perspective is to generate sufficient operating income growth from Family of Apps to fund the growth of investment in Reality Labs.."

7/ ""Reels already makes up more than 20% of the time that people spend on Instagram. Video overall makes up 50% of the time that people spend on Facebook and Reels has grown quickly there as well."

Essentially almost no monetization for 20% of time spent on IG today

Essentially almost no monetization for 20% of time spent on IG today

8/ "We're making major AI investments to build the most advanced models and infrastructure in the industry. Over the next year or 2, we hope that this drives better recommendations for people, higher returns for advertisers and increases our revenue growth..."

9/ "Later this year, we'll release a higher-end headset code-named Project Cambria, which will be more focused on work use cases and eventually replacing your laptop or work setup."

10/ "One way we're helping advertisers get better insights with less data is with conversion modeling. This can help them understand measurement and campaign performance, even when we're notable to see or aggregate certain conversions"

11/ "engagement for both Facebook and Instagram, remain above the levels they were at pre-pandemic and that's true both globally and in the U.S"

"Reels does pull time away from other surfaces, but we do believe it's additive to overall engagement"

"Reels does pull time away from other surfaces, but we do believe it's additive to overall engagement"

12/ On the question of talent attrition, I loved Zuck's explanation.

If u think Meta is new tobacco or targeting ad is just "surveillance capitalism", I hope u resign from Meta immediately (or never join). Not bad to have divisive commentary out there as it can sort talent out.

If u think Meta is new tobacco or targeting ad is just "surveillance capitalism", I hope u resign from Meta immediately (or never join). Not bad to have divisive commentary out there as it can sort talent out.

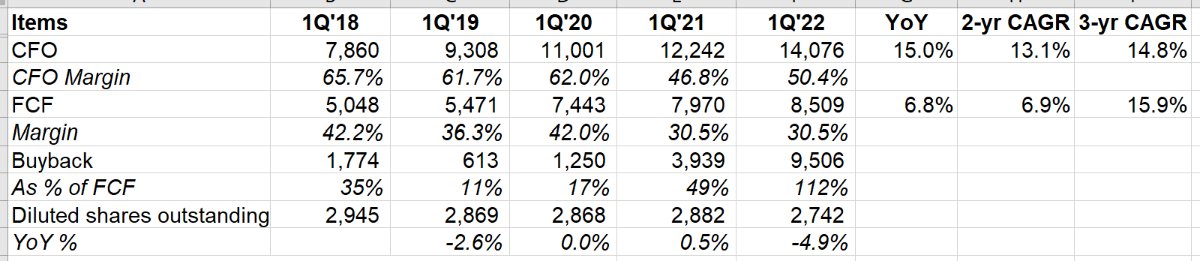

13/ CFO increased +6.8% YoY, driven by WC benefits. Buyback> FCF.

My guess is we'll continue to see buyback somewhat equals FCF. Diluted shares outstanding -4.9% YoY. If they buyback another ~$30 Bn at this price this year, that's another ~5% decline in shares. Net cash $31 Bn.

My guess is we'll continue to see buyback somewhat equals FCF. Diluted shares outstanding -4.9% YoY. If they buyback another ~$30 Bn at this price this year, that's another ~5% decline in shares. Net cash $31 Bn.

14/ Outlook

Global MAU likely to be flat to down in 2Q'22, driven by loss of users in Russia

Revenue $28-30 Bn (assumed 3% FX headwind) i.e. flat YoY at mid-point

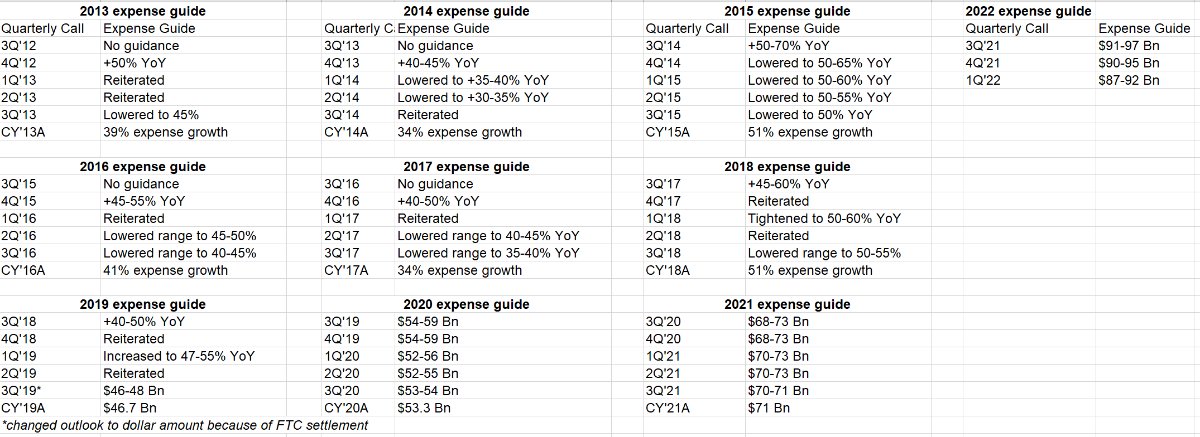

Expense outlook down to 87-92B. Hopefully, it'll be $85-87 Bn by 3Q'22 (see image)

Capex outlook remains $29-34B

Global MAU likely to be flat to down in 2Q'22, driven by loss of users in Russia

Revenue $28-30 Bn (assumed 3% FX headwind) i.e. flat YoY at mid-point

Expense outlook down to 87-92B. Hopefully, it'll be $85-87 Bn by 3Q'22 (see image)

Capex outlook remains $29-34B

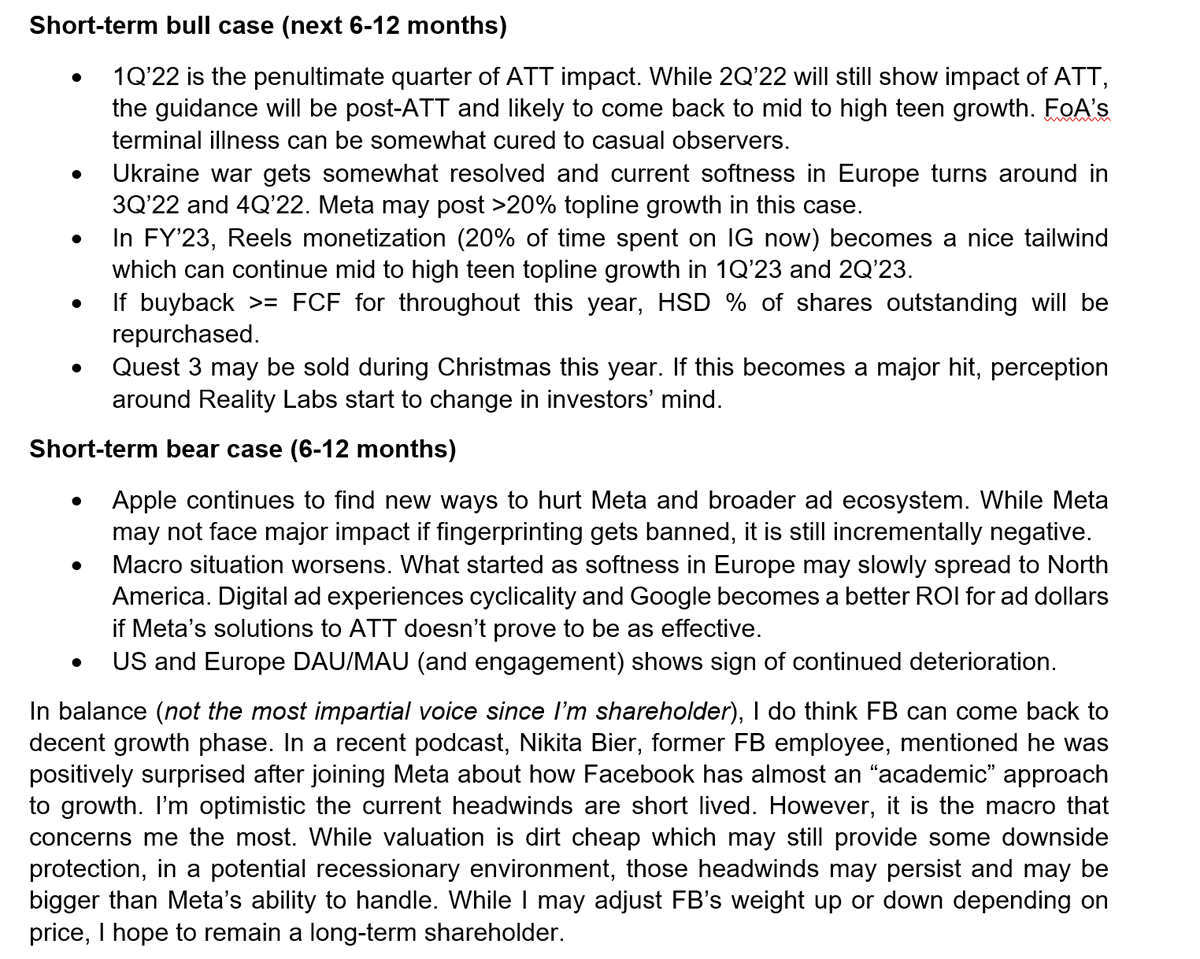

15/ So, what now? I can assure you Meta's shareholders did not enjoy the last few months (tbh few years).

This is what I wrote for short-term bull/bear case for Meta.

This is what I wrote for short-term bull/bear case for Meta.

End/ Here's what I wrote a few weeks ago about what's implied in Meta's stock price (no paywall): mbi-deepdives.com

I'll cover $AMZN tomorrow.

I'll cover $AMZN tomorrow.

Loading suggestions...