Now let's take a look at the business of the company - So the company is in the business of manufacturing decorative aesthetics for 2W, Passenger vehicle & consumer durables.

They provide complete Design-to-delivery services.

They provide complete Design-to-delivery services.

They have the widest product portfolio as compared to their peers -

- Logos

- Decals

- Stickers, aluminium badges

- Chrome plated parts

- 2D Dials

- 3D dials

- Capacitive Overlays

- IML/IMD (In mold decoration/labeling)

- Optical Plastics

- Logos

- Decals

- Stickers, aluminium badges

- Chrome plated parts

- 2D Dials

- 3D dials

- Capacitive Overlays

- IML/IMD (In mold decoration/labeling)

- Optical Plastics

If you look at the revenues, the company has been diversifying with exports increasing at a faster pace.

Increased from 9.8% in 2019 >>> 16% FY21 and expected to 25% of the revenues by 2025.

If you look at revenue split by products

Increased from 9.8% in 2019 >>> 16% FY21 and expected to 25% of the revenues by 2025.

If you look at revenue split by products

the company is diversifying with 35.8% of the revenue coming from Decals and body graphics which was 49% in 2019.

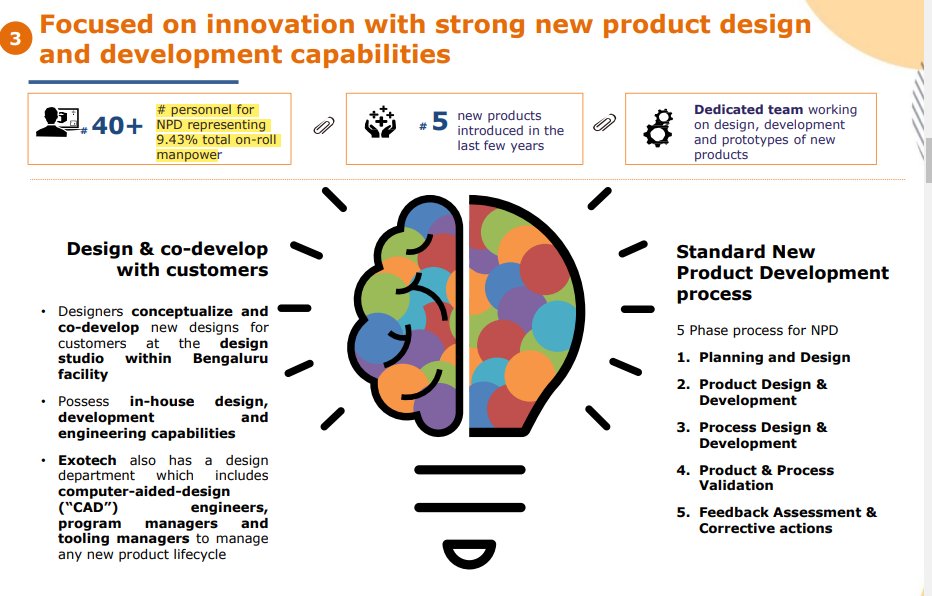

Have 9.85 of the workforce in New Product Design.

Have 9.85 of the workforce in New Product Design.

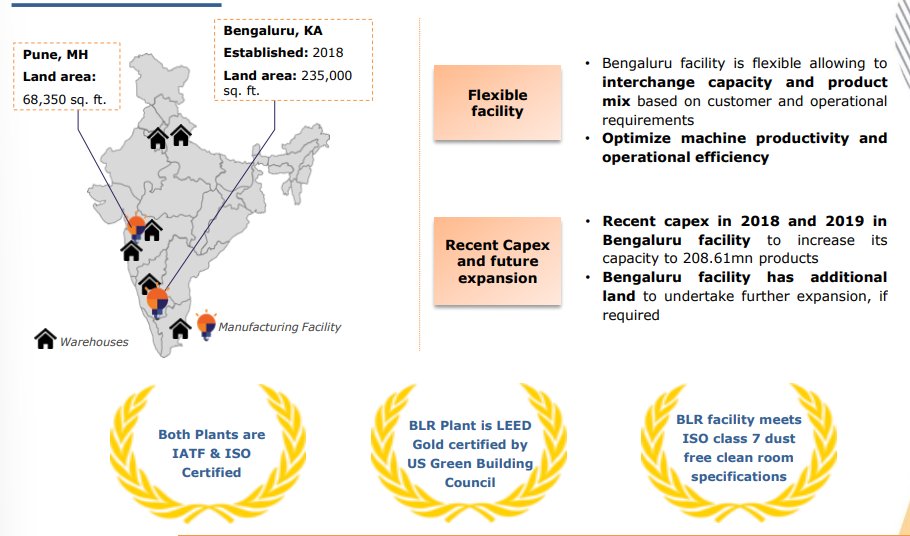

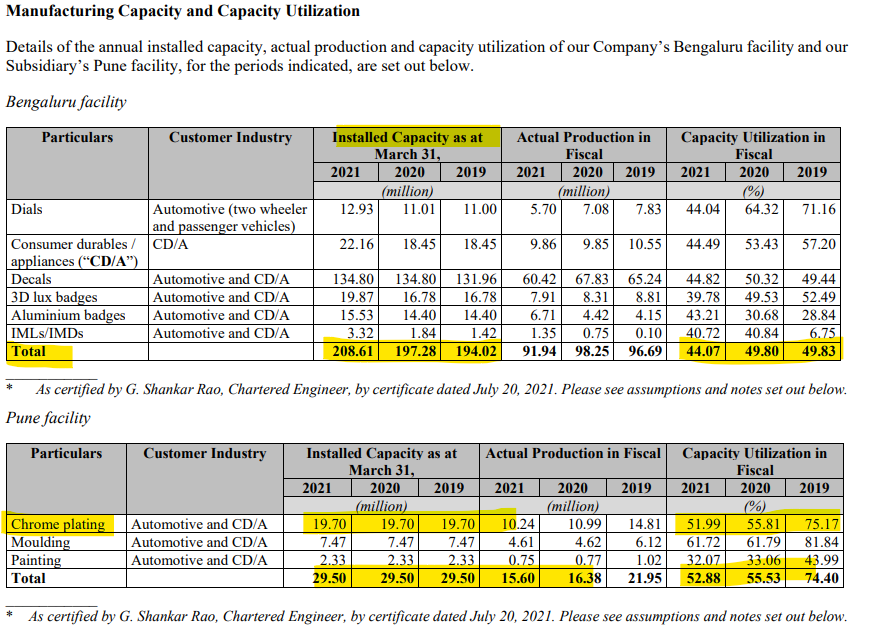

Have ISO certified 2 Manufacturing capacities - One in Bengaluru & One in Pune with total 237 million products.

Bengaluru - 208 Million

Pune - 29.50 Million

Have own 2MW solar energy generation plant.

Bengaluru - 208 Million

Pune - 29.50 Million

Have own 2MW solar energy generation plant.

The company has good relationship with customers as 10 with largest customer they have 15 year long relationship.

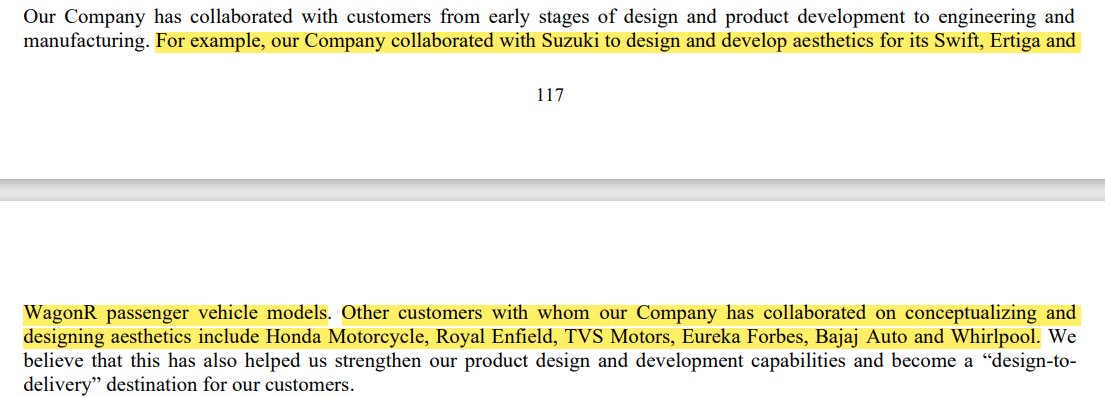

The company sometimes collaborates with the OEM's to design some specifics products as they did with Suzuki in case of "Swift" & "Ertiga"

The company sometimes collaborates with the OEM's to design some specifics products as they did with Suzuki in case of "Swift" & "Ertiga"

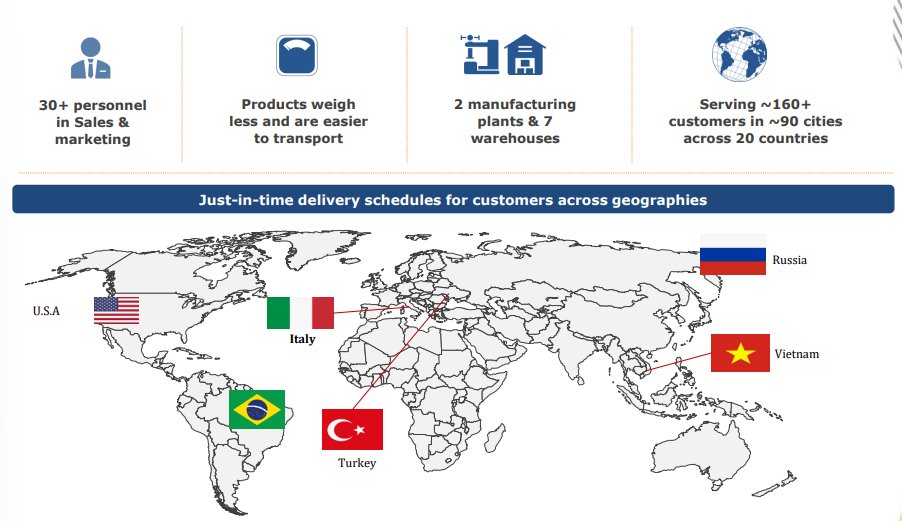

The company have more than 6000 SKUs and Supplies to more than 160 Customers across 20+ Countries.

Have 7 warehouses across India - Haryana, Uttarakhand, Maharashtra, Karnataka and Tamil Nadu.

Have 7 warehouses across India - Haryana, Uttarakhand, Maharashtra, Karnataka and Tamil Nadu.

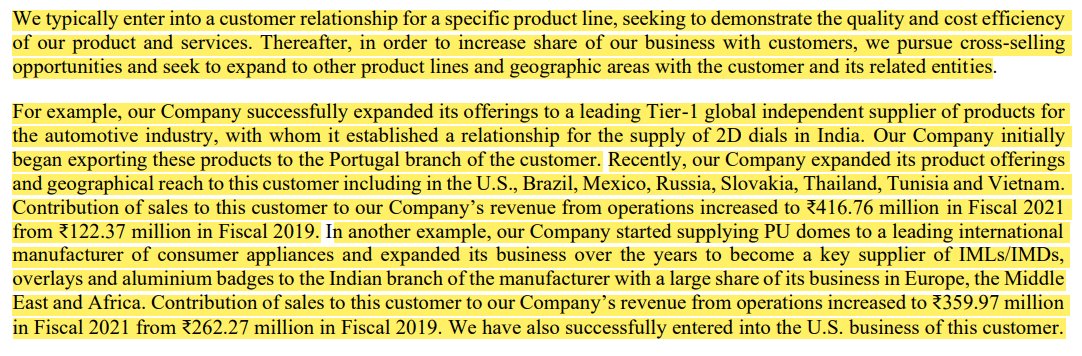

Company has the ability to cross sell, you can read the case studies in the given picture.

Key customers include - Suzuki, Honda, Bajaj Auto, Whirlpool, Samsung, Eureka Forbes, Panasonic etc.

Currently Hero is not their customer but they're trying to get them as a customer as that would be huge positive because Hero being the largest 2W in the World.

Currently Hero is not their customer but they're trying to get them as a customer as that would be huge positive because Hero being the largest 2W in the World.

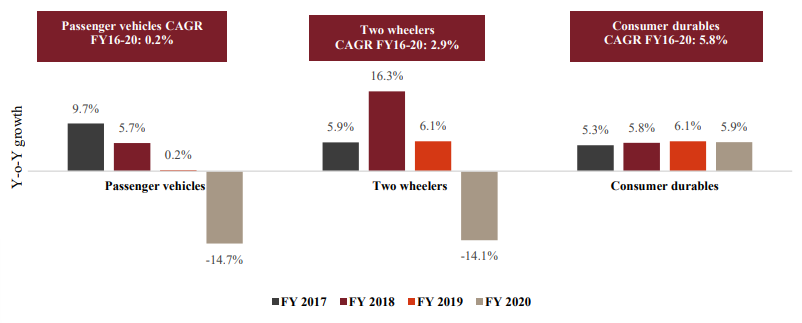

If we look at the numbers - Last 3 years sales growth has been around 4% mainly due to the end user industry growth slowing down.

For Passenger last 5 year CAGR is 0.2%

For 2W it's around - 2.9%

And for Consumer Durable - 5.8%

with 2W & Passenger vehicle dipping -14% in 2020

For Passenger last 5 year CAGR is 0.2%

For 2W it's around - 2.9%

And for Consumer Durable - 5.8%

with 2W & Passenger vehicle dipping -14% in 2020

But Last 2-3 year performance is not that bad with 16% YoY growth due to low base of 2020.

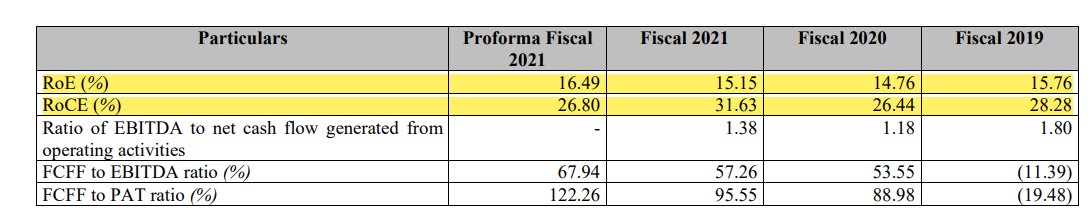

Margins have remained well above 28% and ROE >15% and ROCE >25% with 0 debt.

With 67% Free cash flow to EBIDTA

Margins have remained well above 28% and ROE >15% and ROCE >25% with 0 debt.

With 67% Free cash flow to EBIDTA

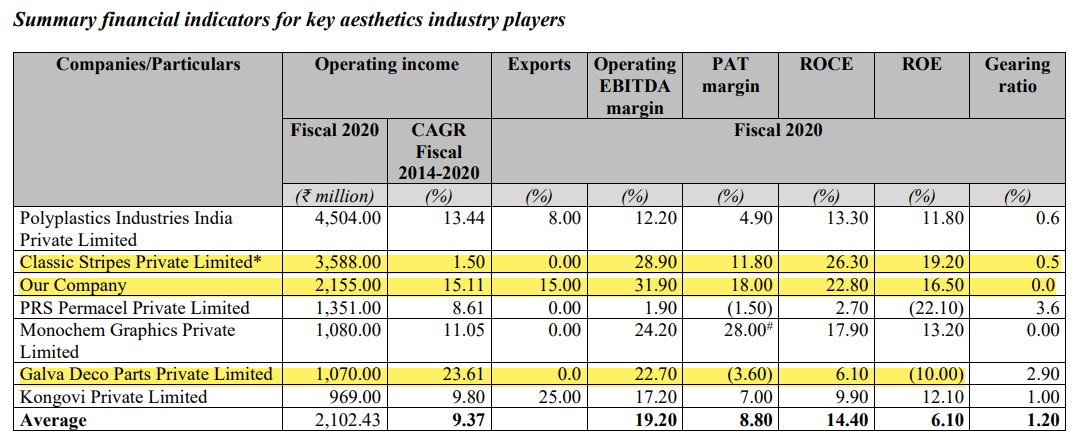

If we compare it with the Peers - The company has grown by 15% Between 2014-2020

Exports growing at 15% with 0 debt and ROE well above 15% & ROCE above 25% and highest EBIDTA margins as compared to peers.

Exports growing at 15% with 0 debt and ROE well above 15% & ROCE above 25% and highest EBIDTA margins as compared to peers.

Working Capital days and Cash Conversion Cycle is little high which the management is confident they can bring down.

Current capacity utilization is around 50% and the last capex was done in 2019-2020. They have no further need for Capex for next few years

Current capacity utilization is around 50% and the last capex was done in 2019-2020. They have no further need for Capex for next few years

and with zero debt, they will keep generating positive free cash flows.

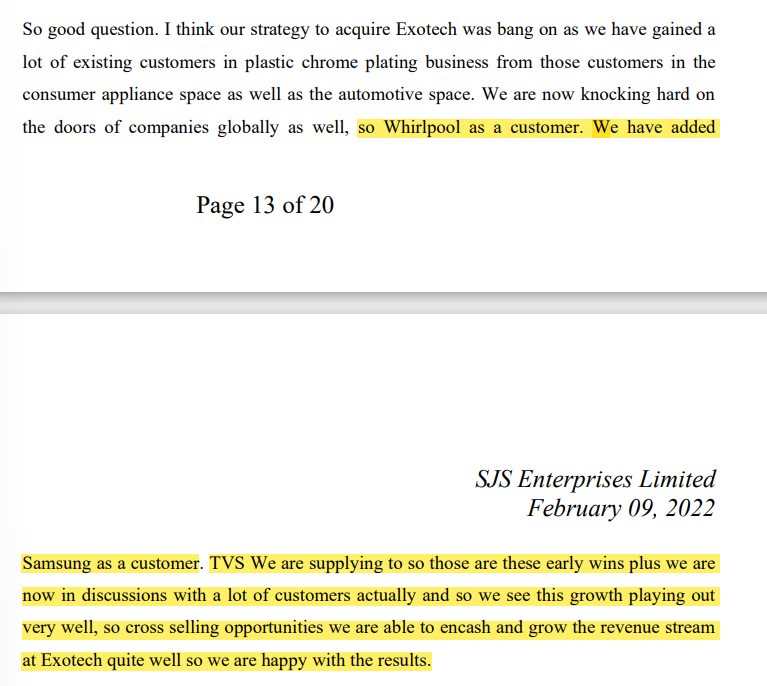

In 2020 they bought a company named "EXOTECH" for 64Cr which is in the business of Chrome Plating.

Chrome plating is a 1000Cr business but with low Margins and High ROCE

For exotech they have, Whirlpool as a customer, they also added Samsung & TVS as customer for chrome plating

Chrome plating is a 1000Cr business but with low Margins and High ROCE

For exotech they have, Whirlpool as a customer, they also added Samsung & TVS as customer for chrome plating

The company is focused on Exports as their products are light weight and easy to ship. The management is looking for Organic & Inorganic growth opportunities like acquisitions in international market etc.

If we take a look at the management team -

- KA joseph is the MD & Co-founder with 34 years of experience in the industry.

- Mr Ramesh Chandra Jain who has worked for 25 years in Eicher Motors.

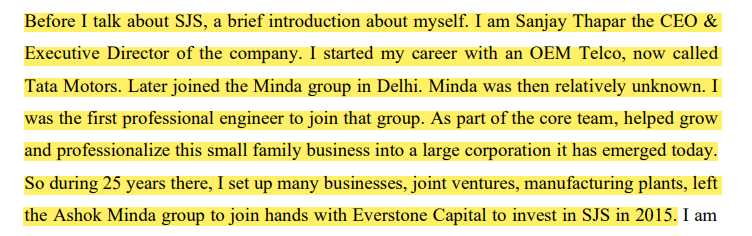

When everstone took over they bought in Sanjay Thapar as the CEO

- KA joseph is the MD & Co-founder with 34 years of experience in the industry.

- Mr Ramesh Chandra Jain who has worked for 25 years in Eicher Motors.

When everstone took over they bought in Sanjay Thapar as the CEO

Sanjay Thapar was the key person in bringing Minda group to this level. He has 25 years of experience in this industry.

Now let's take a look at some Anti Thesis Pointers -

- In a industry which has such high margins, competitors can come any time and dent the margins for SJS

- Delay in Auto Cycle revival

- Everstone selling the rest of the Stake as the 800Cr IPO was done solely for their exit

- In a industry which has such high margins, competitors can come any time and dent the margins for SJS

- Delay in Auto Cycle revival

- Everstone selling the rest of the Stake as the 800Cr IPO was done solely for their exit

- Exports not growing

- Any key customer shifting to any other competitor

- Any key customer shifting to any other competitor

Loading suggestions...