EQUITAS SMALL FINANCE BANK result came yesterday.

I'm a bit disappointed with the results. Here's a summary :-

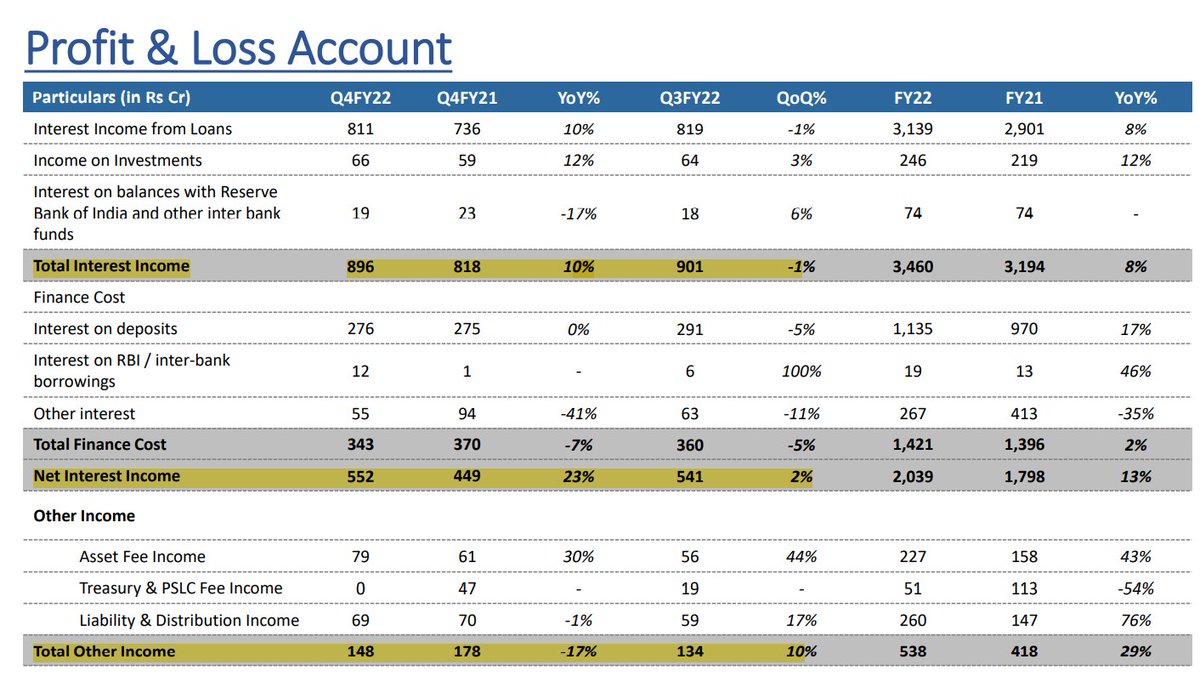

Total income - Up 10% YoY, Down -1% QoQ

NII - Up 23% YoY, 2% QoQ

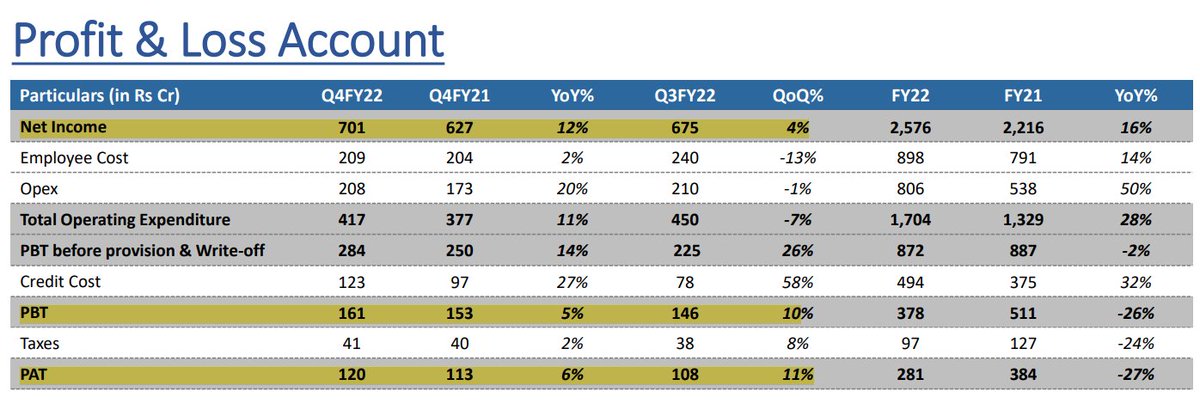

PBT - Up 5% YoY, 10% QoQ

Credit Cost - Up 58% YoY, 27% QoQ

PAT - Up 6% YoY, 11% QoQ

I'm a bit disappointed with the results. Here's a summary :-

Total income - Up 10% YoY, Down -1% QoQ

NII - Up 23% YoY, 2% QoQ

PBT - Up 5% YoY, 10% QoQ

Credit Cost - Up 58% YoY, 27% QoQ

PAT - Up 6% YoY, 11% QoQ

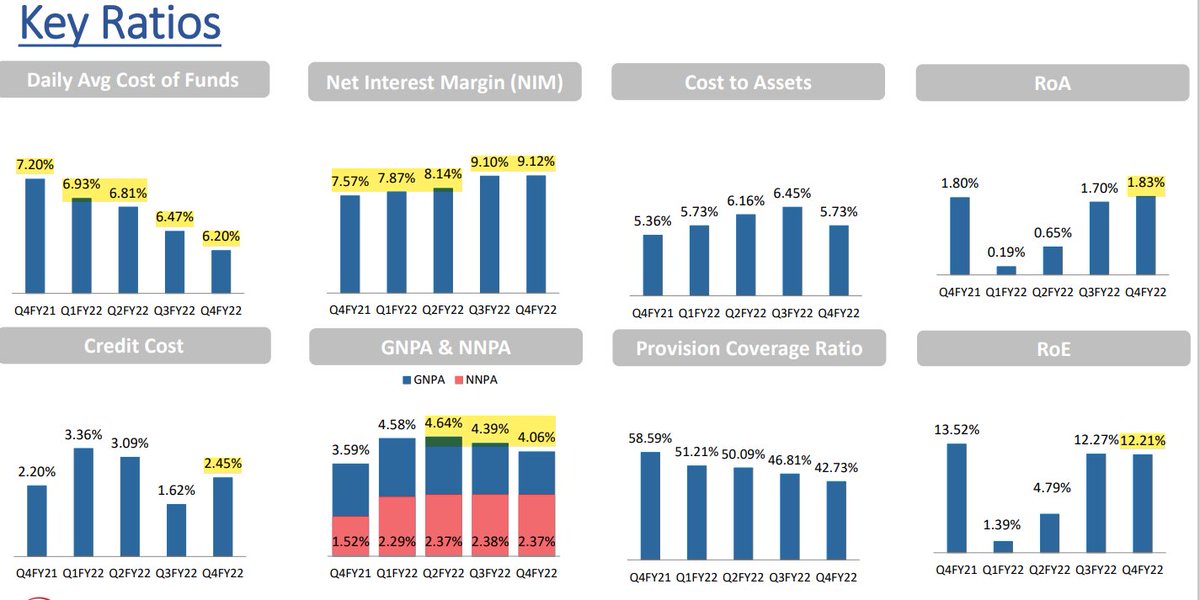

Quarterly Trend - CoF - Down to 6.20% from 7.20% YoY

NIM - 9.12% (Consistently increasing QoQ)

ROA - 1.83%

ROE - 12.21%

PCR - 42.73% (Not sure why it's coming down every quarter, not good)

Credit Cost - 2.45%

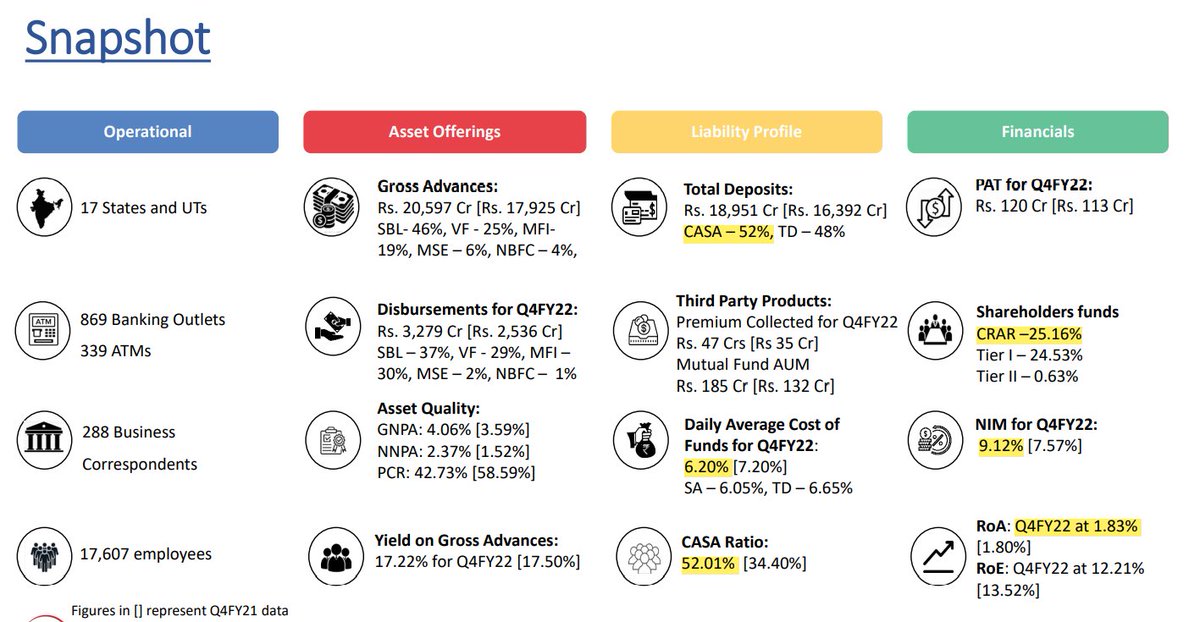

GNPA - 4.06% (Coming down after peak in Q2FY22)

NIM - 9.12% (Consistently increasing QoQ)

ROA - 1.83%

ROE - 12.21%

PCR - 42.73% (Not sure why it's coming down every quarter, not good)

Credit Cost - 2.45%

GNPA - 4.06% (Coming down after peak in Q2FY22)

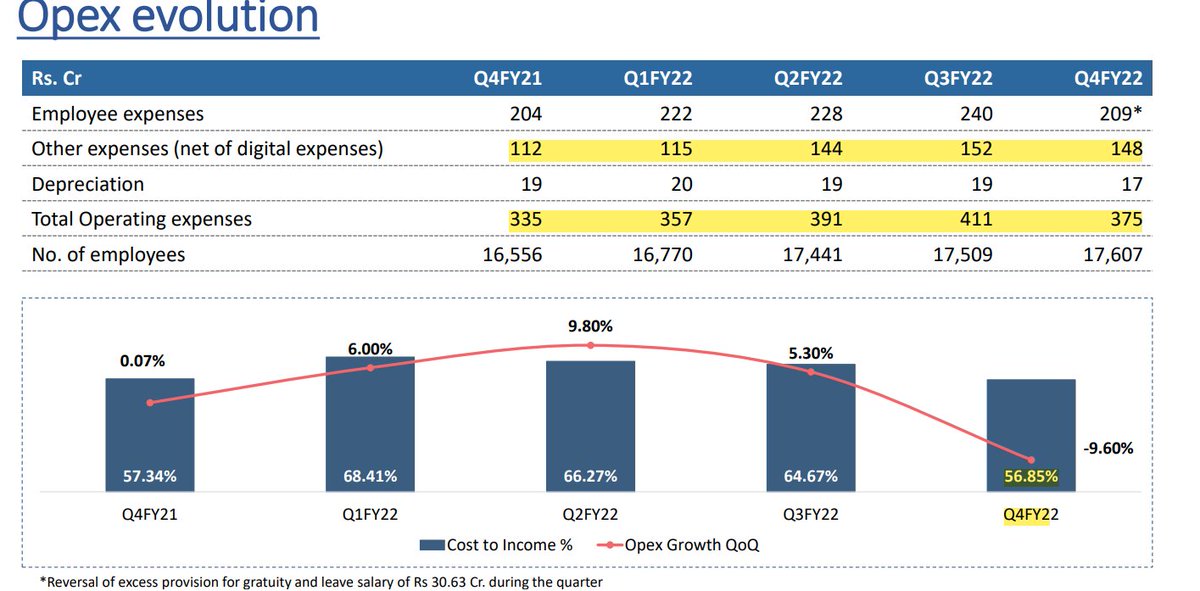

Cost to income - Down to 56.85% from 64.67% QoQ

(Not sure why they had such high Cost to income last quarter)

(Not sure why they had such high Cost to income last quarter)

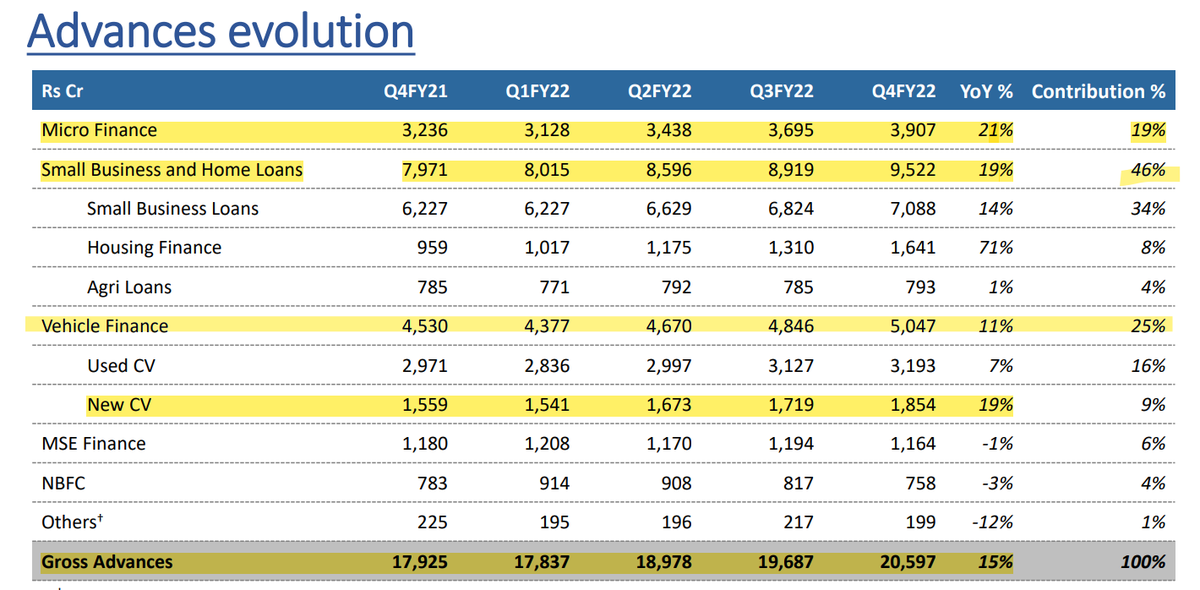

Gross Advances up 15% YoY to 20,597Cr (Not so great)

Small business loans up 19% (46% of overall advances)

Microfinance - Up 21% (19% of overall advances)

New CV - Up 19% YoY (9% of overall advances)

Small business loans up 19% (46% of overall advances)

Microfinance - Up 21% (19% of overall advances)

New CV - Up 19% YoY (9% of overall advances)

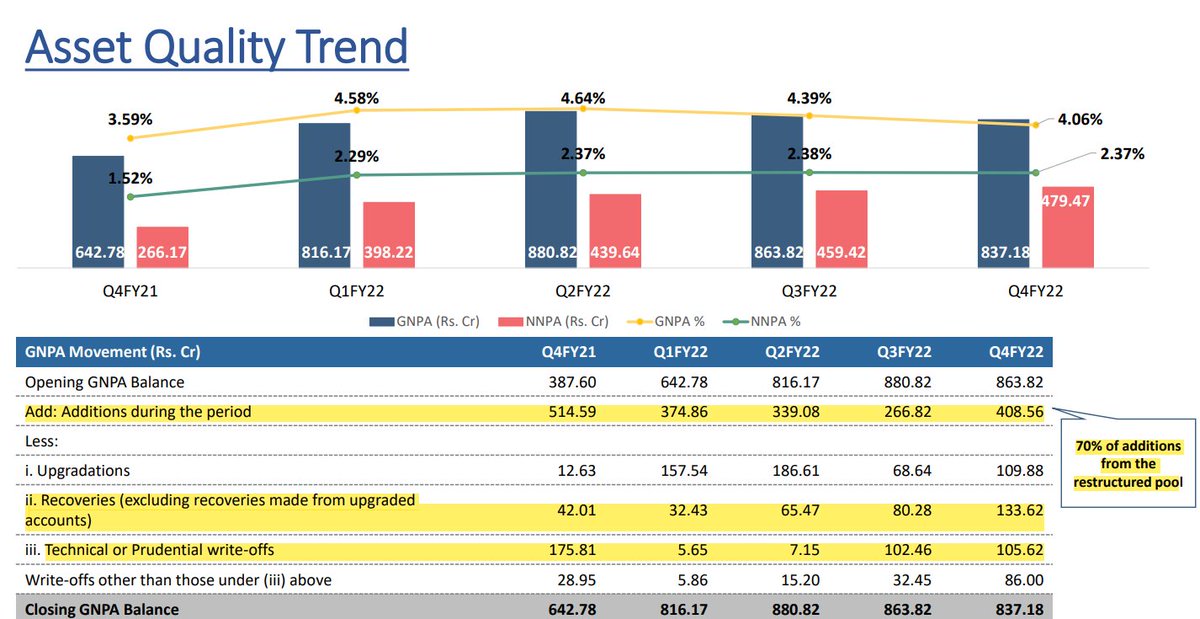

Asset Quality - GNAP - Down to 4.06% after forming a peak in Q2FY22 of 4.64%

NNPA - Flat at 2.37%

Net Additions - 408Cr (High, 70% came from restructured pool)

Recoveries - 133Cr (Improving trend)

Write-offs - 191Cr (High)

NNPA - Flat at 2.37%

Net Additions - 408Cr (High, 70% came from restructured pool)

Recoveries - 133Cr (Improving trend)

Write-offs - 191Cr (High)

Liability Side - Cost of funds consistently coming down (Down to 6.20%)

CASA - 52% (Need to see how will they be able to retain it)

CASA - 52% (Need to see how will they be able to retain it)

Loading suggestions...