Intellect Design Arena

Let us understand the business & my investment thesis.

Consider sharing/Retweeting if you find the thread useful

🧵 ⤵️

Let us understand the business & my investment thesis.

Consider sharing/Retweeting if you find the thread useful

🧵 ⤵️

Outline

1. Business Understanding

2. Drivers of Sales Growth

3. Drivers of operating leverage

4. Intellect's Right to Win / Competitive advantages

5. Financials

6. Valuation

7. Anti-thesis

8. Disclaimer

9. Summary

1. Business Understanding

2. Drivers of Sales Growth

3. Drivers of operating leverage

4. Intellect's Right to Win / Competitive advantages

5. Financials

6. Valuation

7. Anti-thesis

8. Disclaimer

9. Summary

1. Business Understanding

The world of 💵 around us is powered by banks & other financial institutions. Insurance, e-commerce, money transactions (UPI, IMPS, RTGS), trade finance (receivables, payables, inventory).

The world of 💵 around us is powered by banks & other financial institutions. Insurance, e-commerce, money transactions (UPI, IMPS, RTGS), trade finance (receivables, payables, inventory).

Commerce has been around since perhaps humanity itself. Formal Lending has been around since 1500 or so.

What has changed in the last 500 years is the way commerce occurs. What is money at the end of the day? It is an entry in a database maintained by banks, depositories.

Pre-computers & machines, people would need to manually maintain these records physically by hand. The invention of computers changed that, improved that.

quora.com

quora.com

As surprising as it may sound, the internet has not always been around.

You must remember that computers pre-date internet by about 40-50 years. Computers were invented in 1950s, perfected through the next 30-40 years, and then connected together.

You must remember that computers pre-date internet by about 40-50 years. Computers were invented in 1950s, perfected through the next 30-40 years, and then connected together.

Were the banks going to sit around for the internet to arrive? Hell no. Right after computers were invented, banks started using them as databases.

It is in this context that we musk understand what @elonmusk means when he says that money is just an entry in mainframe computers.

How important is money to you? I suppose enough because you are reading this thread. Well, guess what? Most humans are like you. This is exactly why central banks regulate financial institutions, specially full banks heavily. It's insanely hard to get a banking license anywhere.

Ask vaidyanathan sir how painful the transformation of @IDFCFIRSTBank has been in last 4 years.

This has been the experience throughout the world. Depicted well in fiction as well. Anyone remember Bobby Axelrod's bid to become a bank from Billions?

wsj.com

wsj.com

Becoming a bank is a big deal.

A bank.

does not.

want to.

screw it up.

A bank.

does not.

want to.

screw it up.

This is why most banks continue to rely on ancient mainframe (50 year old computer technology) running ancient programming language code (cobol) using ancient processes (batch mode, meaning in batches together, not one at a time).

Immediately the eager investor should note 2 things:

1. Onboarding the banks on to the digital revolution is insanely hard(see my mastek thread for more details on what digital transformation is): .

1. Onboarding the banks on to the digital revolution is insanely hard(see my mastek thread for more details on what digital transformation is): .

2. Customers are sticky. Demanding. Need the best. Reliability. Security.

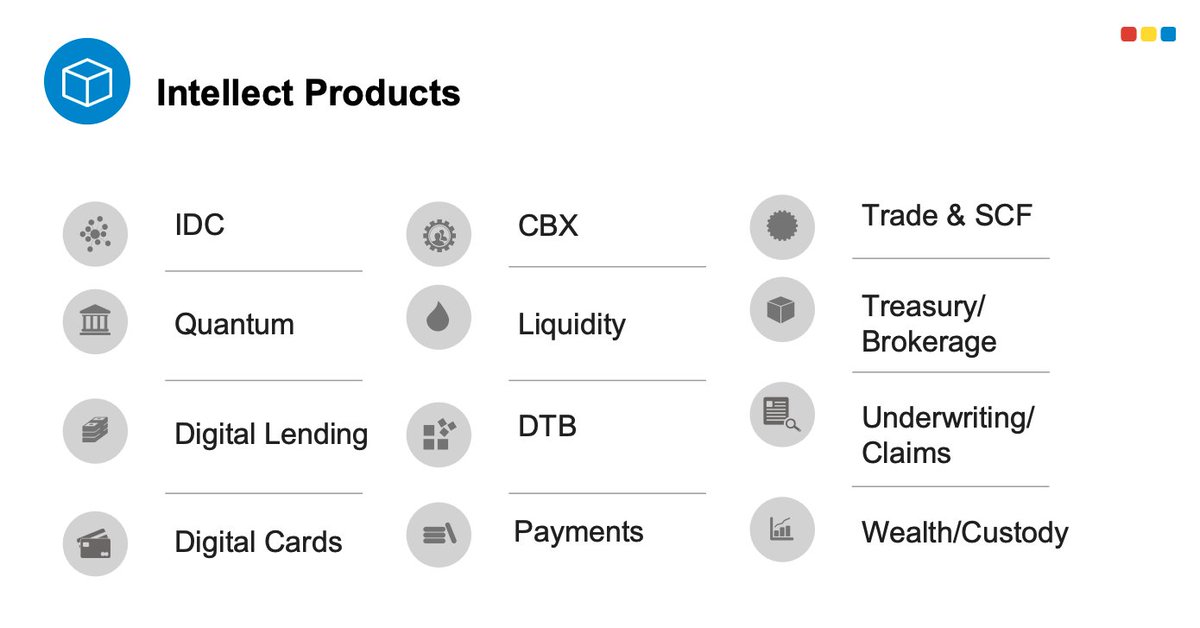

It is this methodological, structural, secure, robust, reliable digital transformation of banks & other financial institutions (insurance, credit cards, central banks) that intellect does, through its 12 products, 5 platforms, & 4 core technologies.

An inexperienced reader might ask, what are products, platforms & technologies & how are they different.

At the heart of everything digital is technology. This is the heart of programming. Artificial intelligence or machine learning is technology.

At the heart of everything digital is technology. This is the heart of programming. Artificial intelligence or machine learning is technology.

Blockchain (backbone of crypto) is a core technology.

Traditional IT cos do bespoke work for each client. Product companies look at a market need that cuts across multiple clients & builds a common "product" for all of them, leveraging core technologies (like blockchain, or web3, or machine learning).

An example of B2C product is Google search, or Facebook.

When the adoption of a product by users causes its adoption to accelerate further (a virtuous cycle known as network effects), a product becomes a platform.

A thread on platform businesses in case anyone wants to go deeper into it:

A thread on platform businesses in case anyone wants to go deeper into it:

Let us talk about intellect's products.

For each need of the customer, intellect has developed products. Intellect has 12 products, 5 platforms & leverages 4 technologies. I'll cover a few & the rest to the reader.

For each need of the customer, intellect has developed products. Intellect has 12 products, 5 platforms & leverages 4 technologies. I'll cover a few & the rest to the reader.

1. IDC: Intellect Digital Core

Are you a bank that wants to build digital experiences for CASA, WASA, deposits, customer on-boarding, wallets, cards? Then IDC is for you.

Are you a bank that wants to build digital experiences for CASA, WASA, deposits, customer on-boarding, wallets, cards? Then IDC is for you.

2. Intellect Xponent: Underwriting product For Insurance

Xponent allows reduction in combined operating operating ratio (operating costs for insurance) by leveraging machine learning based risk assessment, taking into account co's history, & leading indicators of risk.

Xponent allows reduction in combined operating operating ratio (operating costs for insurance) by leveraging machine learning based risk assessment, taking into account co's history, & leading indicators of risk.

3. CBX: Contextual banking Experience

For enterprise usage, banking has to be contextual to user's current experiences & needs. This product allows user to create alerts, buy hedges, & execute complex actions in a systematic manner digitally.

youtube.com

For enterprise usage, banking has to be contextual to user's current experiences & needs. This product allows user to create alerts, buy hedges, & execute complex actions in a systematic manner digitally.

youtube.com

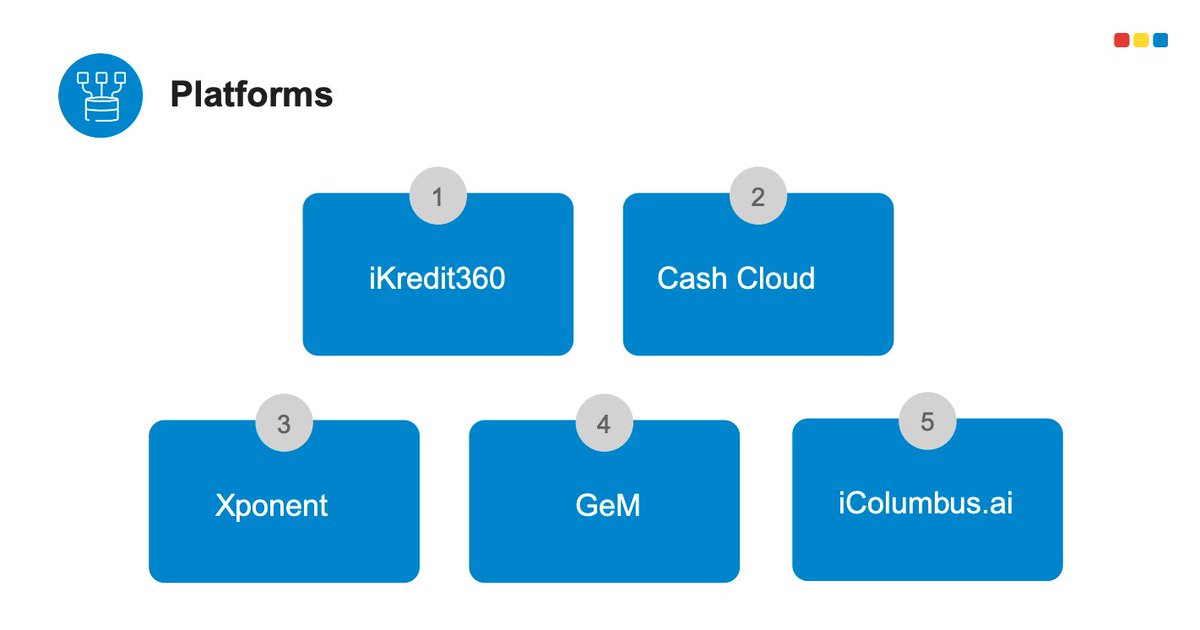

Intellect's Platforms

Rather than address customer's each need separately, intellect wanted to create platforms which enable addressing customer's digital transformational needs holistically.

Rather than address customer's each need separately, intellect wanted to create platforms which enable addressing customer's digital transformational needs holistically.

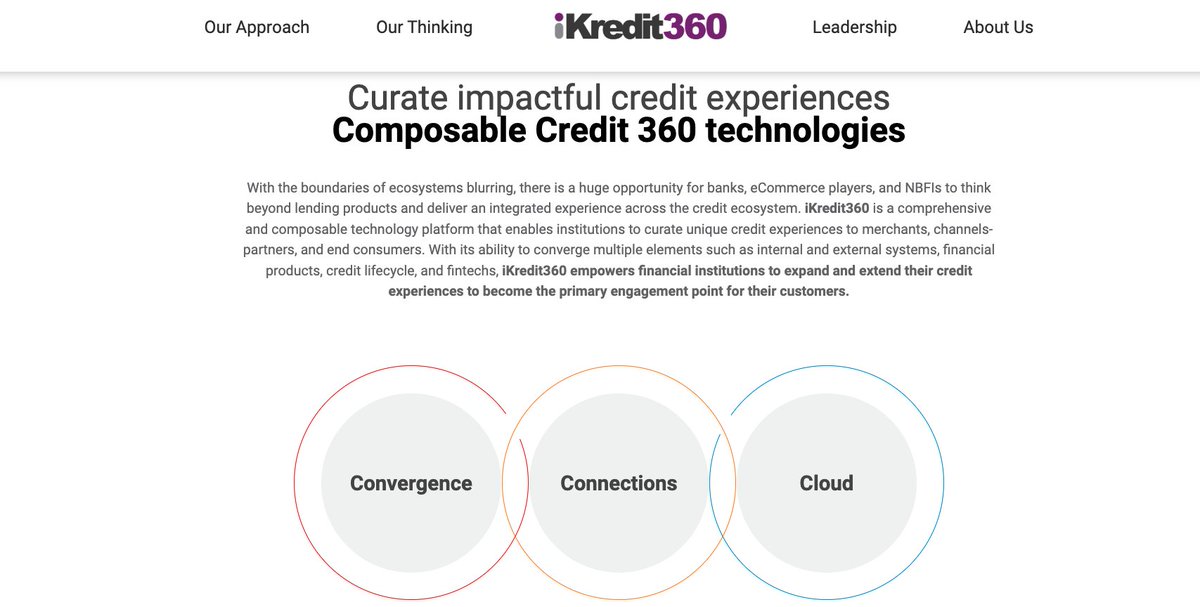

1. iKredit360:

Intellect's comprehensive composable platform which enables banks to create unique customised contextual experiences for their customers while converging te various aspects of that experience: relationship management, lending, cross-selling insurance, lifecycle management.

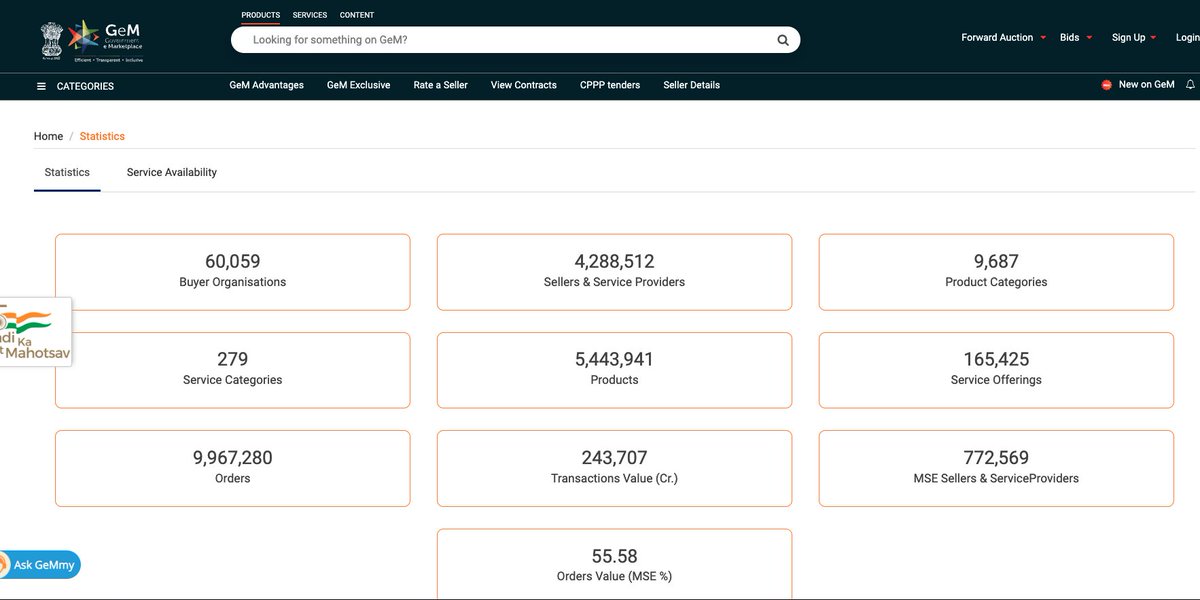

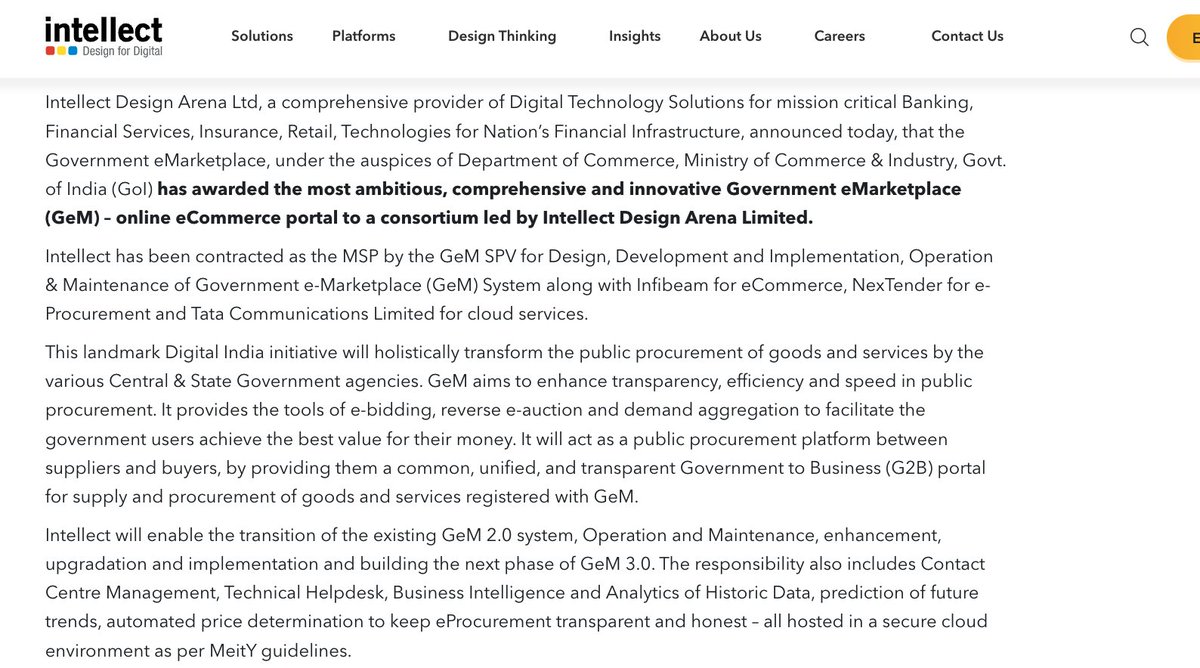

2. GeM: Government e-marketplace

Did you know?

Government of India's majority of procurement of goods & services happens on GEM, and intellect is the the workhorse behind GeM.

Did you know?

Government of India's majority of procurement of goods & services happens on GEM, and intellect is the the workhorse behind GeM.

As of August 2021, GeM has 4.2M Sellers (7 lakh+ are medium & small enterprises), 60k buyers (PSUs, government departments). It has more than 5 million products in 16409 product categories, & it has 193 service categories.

Intellect's GEM revenues growing 100% YoY.

Intellect's GEM revenues growing 100% YoY.

Intellect gets a % of that revenue. Had to automate 1000s of government purchase rules, regulations, laws into building this marketplace. As government purchases shift to GeM, intellect's revenues would grow (take rate would reduce with volumes).

youtube.com

youtube.com

2. Drivers of Sales Growth

So what will drive intellect's sales growth?

So what will drive intellect's sales growth?

How enterprise products work:

(i) Identify an unfulfilled client need.

(ii) Invest R&D rupees into building an end to end working solution.

(iii) Define your go to market strategy & execute on it to get 1st win

(iv) use 1st set of wins as references to get more wins

(i) Identify an unfulfilled client need.

(ii) Invest R&D rupees into building an end to end working solution.

(iii) Define your go to market strategy & execute on it to get 1st win

(iv) use 1st set of wins as references to get more wins

(v) repeat across geographies

All the products and platforms you saw from intellect? Are on different stages of the commerialization journey.

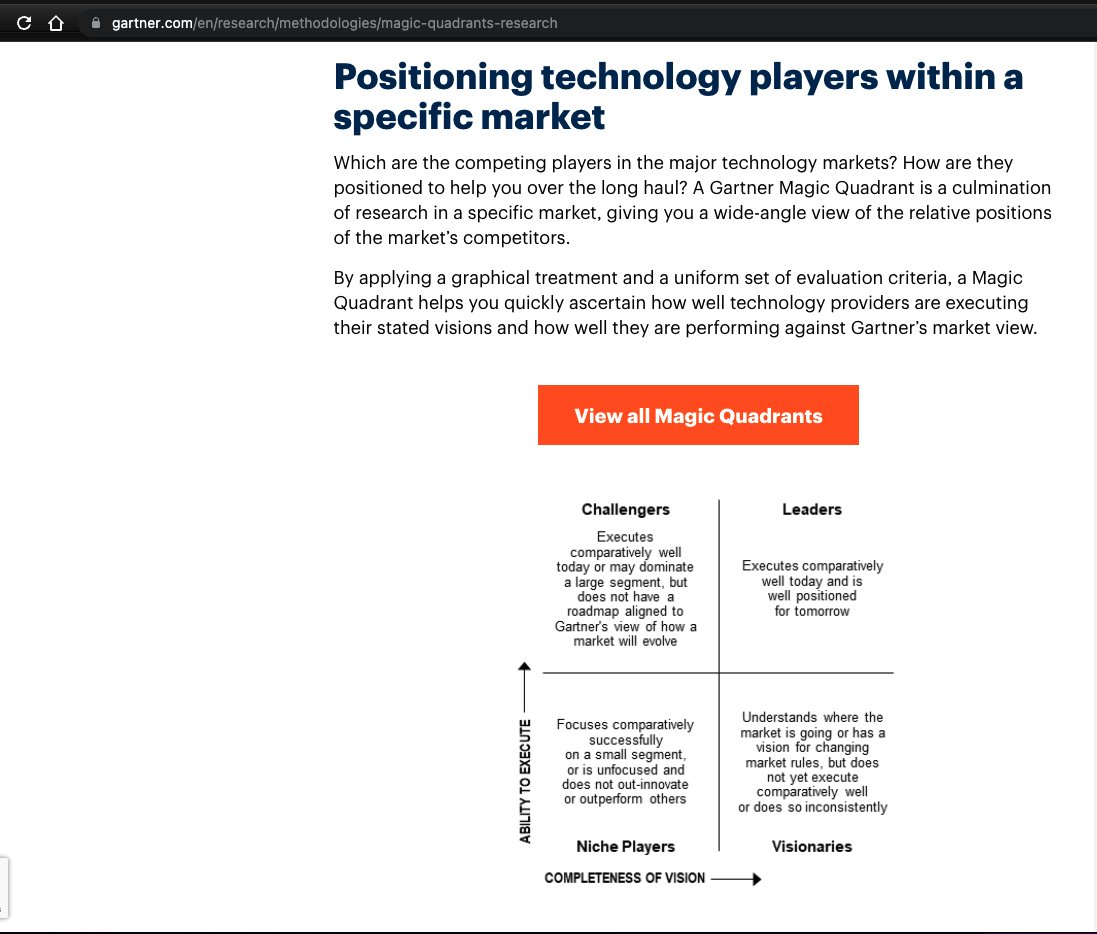

Only 3 of the 12 products are in leadership quadrant (market leadership defined by gartner). Other 9 are in various stages of adoption cycle.

Only 3 of the 12 products are in leadership quadrant (market leadership defined by gartner). Other 9 are in various stages of adoption cycle.

As intellect executes, gets 1st wins, 2nd wins the wins compound. Intellect has a brilliant GTM strategy. More on that later.

(i) More products commercialising.

(ii) More products being developed for unmet market needs

(iii) Cross-selling

(i) More products commercialising.

(ii) More products being developed for unmet market needs

(iii) Cross-selling

(iv) Going to new geographies & using initial wins as references

(v) (most important): Intellect is graduating from a platform to a marketplace company. It realizes that it cannot build each & every solution in-house.

(v) (most important): Intellect is graduating from a platform to a marketplace company. It realizes that it cannot build each & every solution in-house.

Hence, ties up with partners, & makes small strategic investments in early stage start-ups which develop in the intellect eco-system, thereby enhancing the value delivered to the customer.

This is literally out of salesforce's playbook & is a very effective way for a B2B player to behave similar to a platform co (Banks & financial institutions on one side, fintech players, start-ups, developers on the other side of the platform).

We are yet to see any benefits accruing from this. This is still in the narrative stage, could be a good optionality.

3. Drivers of operating leverage

Intellect says in almost all their concalls that they have designed this business for 20% sales & 30% EBITDA compounding. Such operating leverage is inherent in product & platform companies.

You make a product once.

Intellect says in almost all their concalls that they have designed this business for 20% sales & 30% EBITDA compounding. Such operating leverage is inherent in product & platform companies.

You make a product once.

Then reuse it at minimal incremental costs. This is why product companies typically keep improving margins.

In the near term (next 2 years or so) intellect guidance is to improve EBITDA margins from ~25% currently to ~30%.

In the near term (next 2 years or so) intellect guidance is to improve EBITDA margins from ~25% currently to ~30%.

Intellect also categorically states that it does not want to chase margins by sacrificing growth. It makes significant R&D investments (some of which are capitalized).

Around 5% of sales are R&D investments for future products which are capitalized, rest are charged to P&L (for immediate term costs like implementations).

4. Intellect's Right to Win / Competitive advantages

(i) in any product company, Culture is the moat. Intellect has created a design culture which is hyper-focussed on customer needs. Generally, digital transformation deals take 18-24 months to implement.

(i) in any product company, Culture is the moat. Intellect has created a design culture which is hyper-focussed on customer needs. Generally, digital transformation deals take 18-24 months to implement.

Intellect implements them in 6 months by breaking down the program into 4-hour work slots. this shows up in intellect's deal wins. It wins 65-70% of the deals it sits for. This itself demonstrates Intellect's moat.

(ii) Intellect has tied up with microsoft to launch banking-as-a-service. This would see azure adopt intellect as exclusive banking partner (intellect does not need to be exclusive).

(iii) Gartner ranks 3 out of 12 intellect products as leadership quadrant products. Executes comparatively well today & well poised for tomorrow.

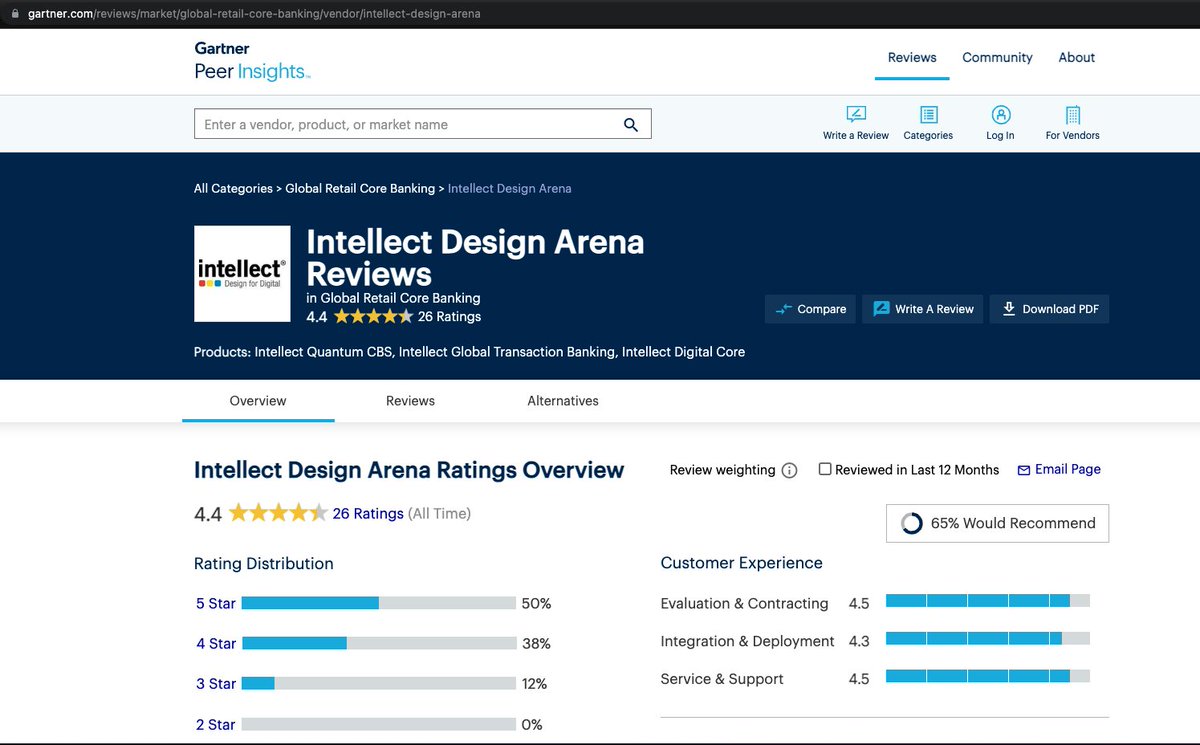

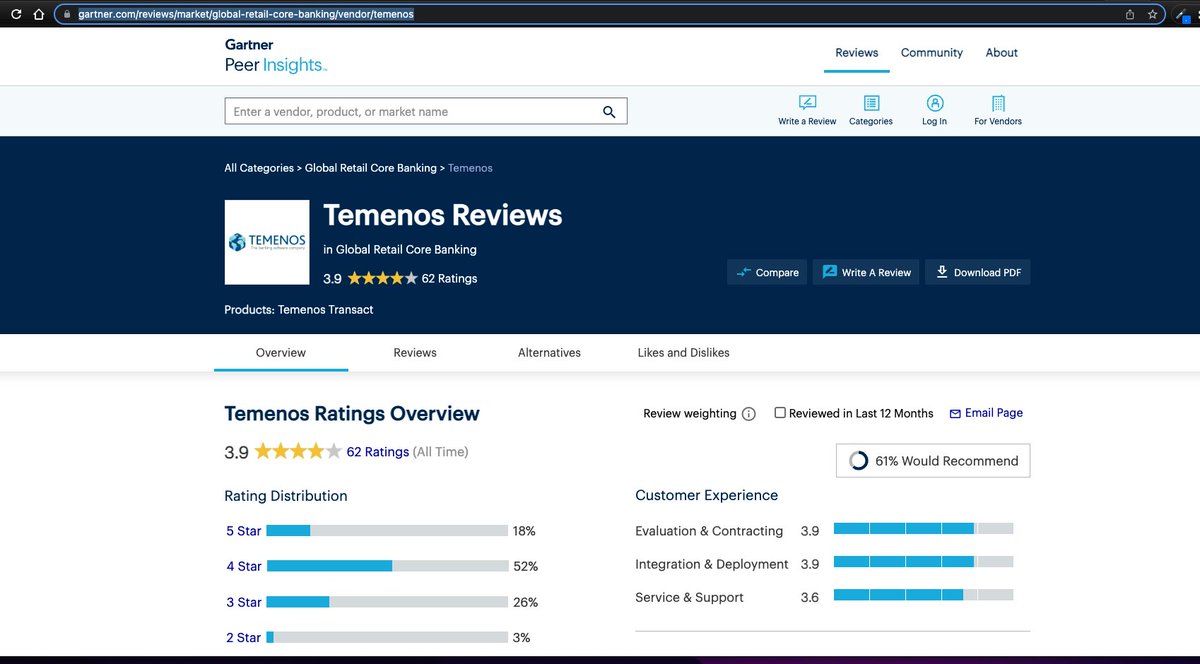

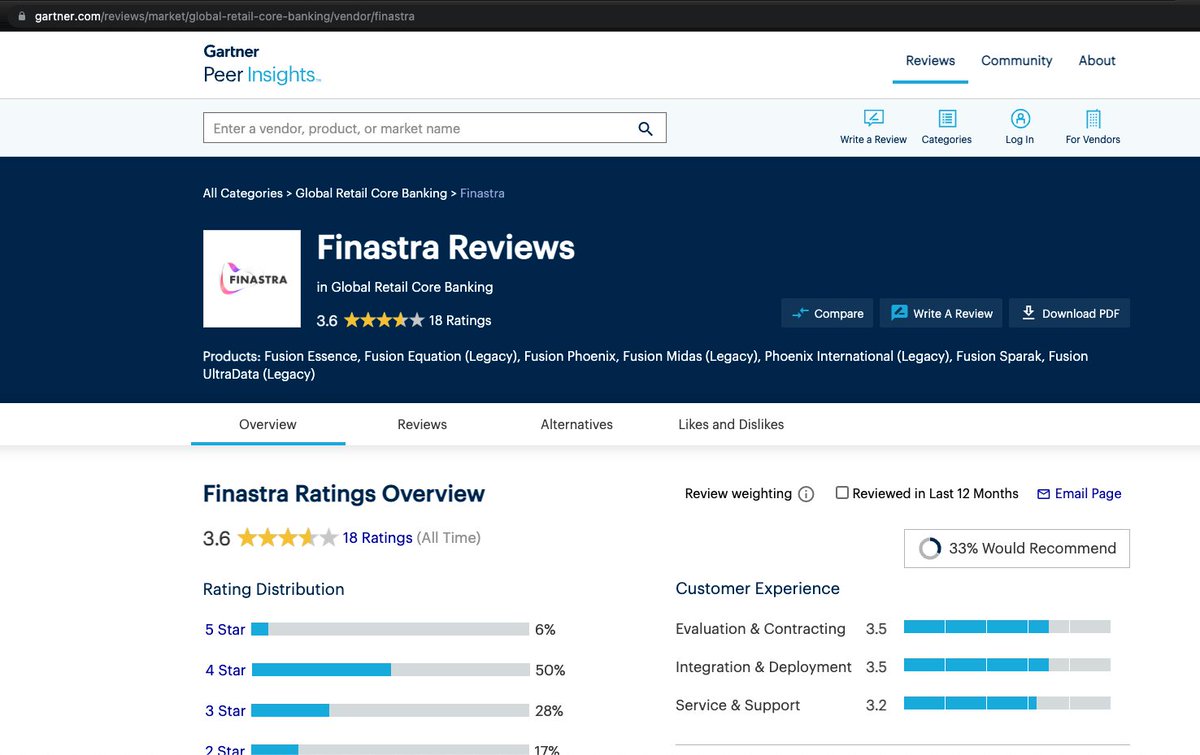

(iv) Head to gartner.com & look for the customer ratings for intellect & its competitors like Temenos & Finastra.

Finestra: 3.6

Temenos: 3.9

Intellect: 4.4

What does that tell you? Clients love intellect.

Finestra: 3.6

Temenos: 3.9

Intellect: 4.4

What does that tell you? Clients love intellect.

If you talk to some industry insiders, they will tell you that "XYZ bank is unhappy with intellect". Well, obviously. Reality is a normal distribution.

Tell them, anecdotes cant be used for making decisions where statistical evidence is available. Point them to gartner.

Tell them, anecdotes cant be used for making decisions where statistical evidence is available. Point them to gartner.

(v) I can do no better than to tell you about intellect's client list. HDFC bank, icici bank, idfc first bank, Reserve bank of india, Citi bank, HSBC, Nabad, Life corporation of India (LIC), Kotak mahindra bank

Head over to intellectdesign.com and see list of customers by product

5. Financials

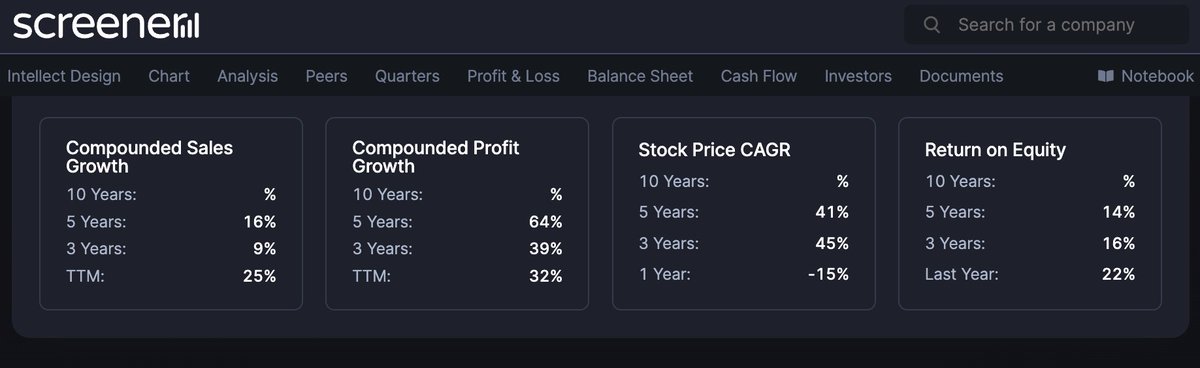

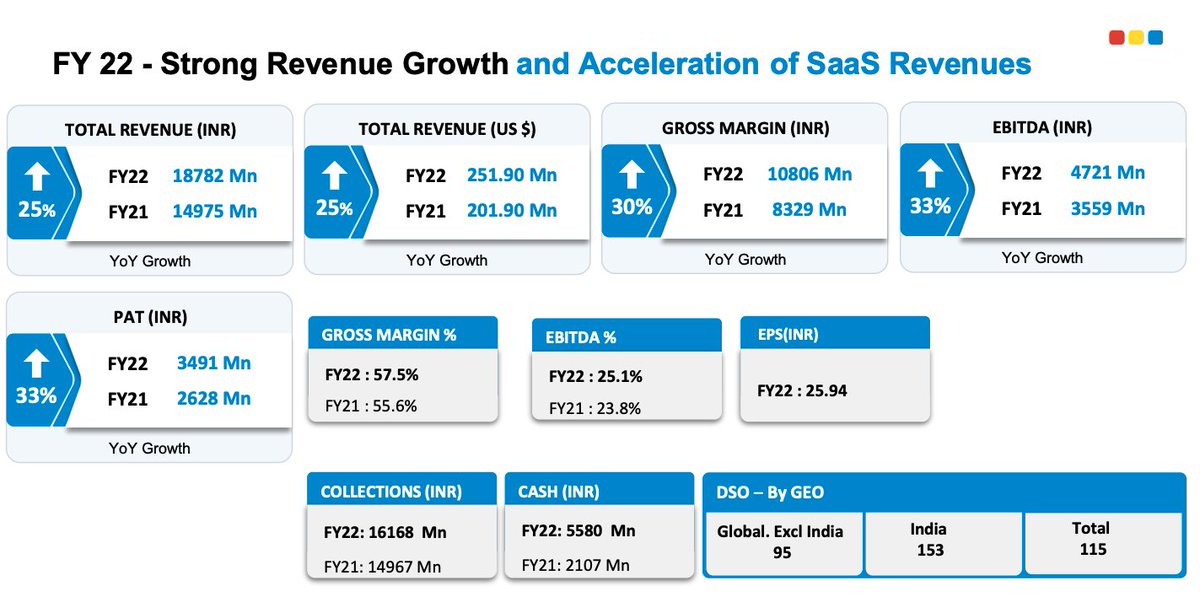

(i) 25% sales growth, 33% profit growth, gross margins expanded to 57%, cash position doubled to 558 cr.

(i) 25% sales growth, 33% profit growth, gross margins expanded to 57%, cash position doubled to 558 cr.

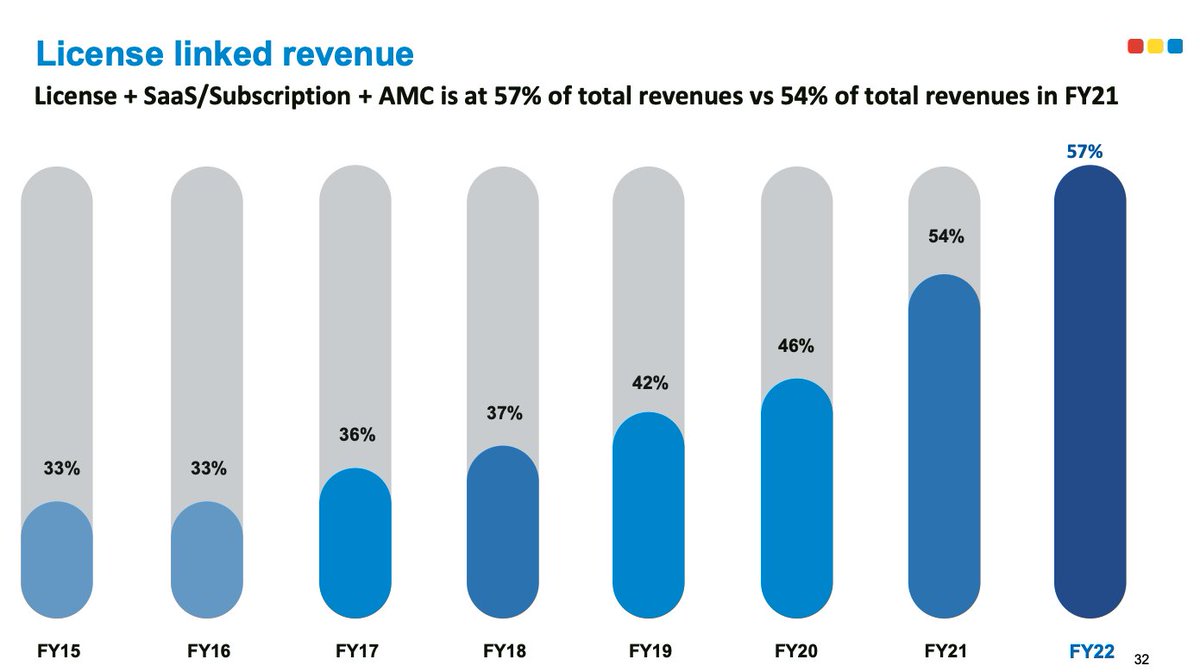

(ii) What matters most in quality of revenue. 57% of intellect's revenue now comes from their intellectual property (IP) (SaaS+AMC+license) versus 33% in FY15. This is inching up & will continue to inch up.

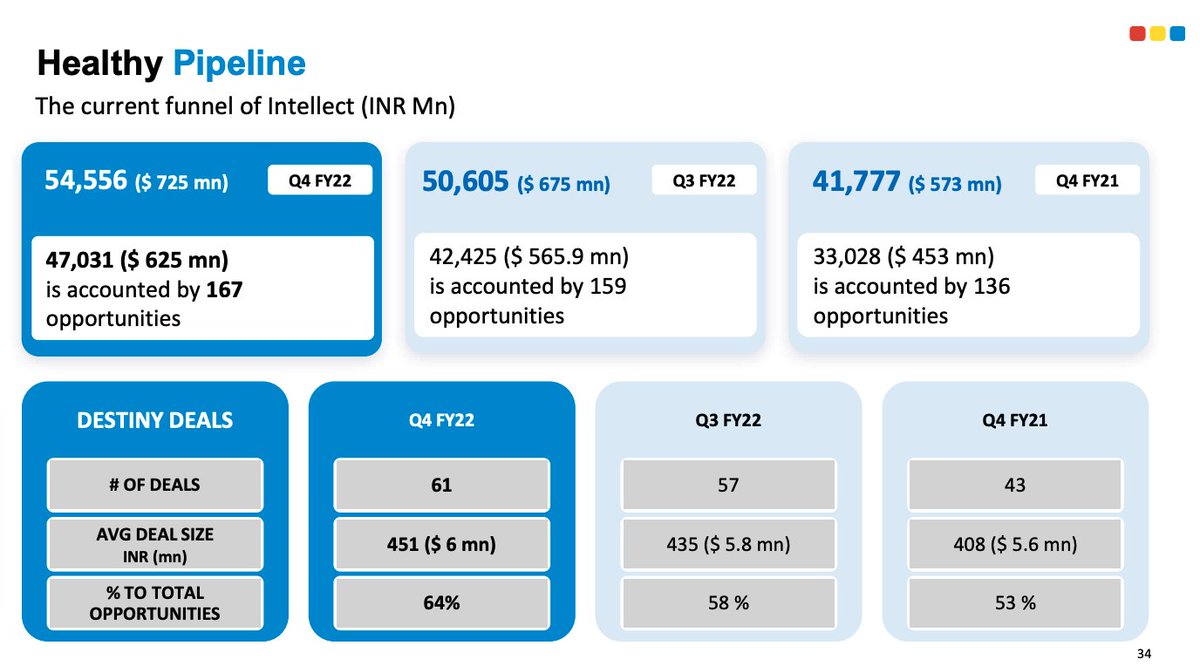

(iii) Q4 revenue will appear to be flat. This was due to 2 deals worth 30cr lost due to russia ukraine war. Had war not broken out, intellect would have grown 6% QoQ. What we need to focus on is not quarterly earnings, but earning power. Reflected in deal pipeline: up 7.5% QoQ

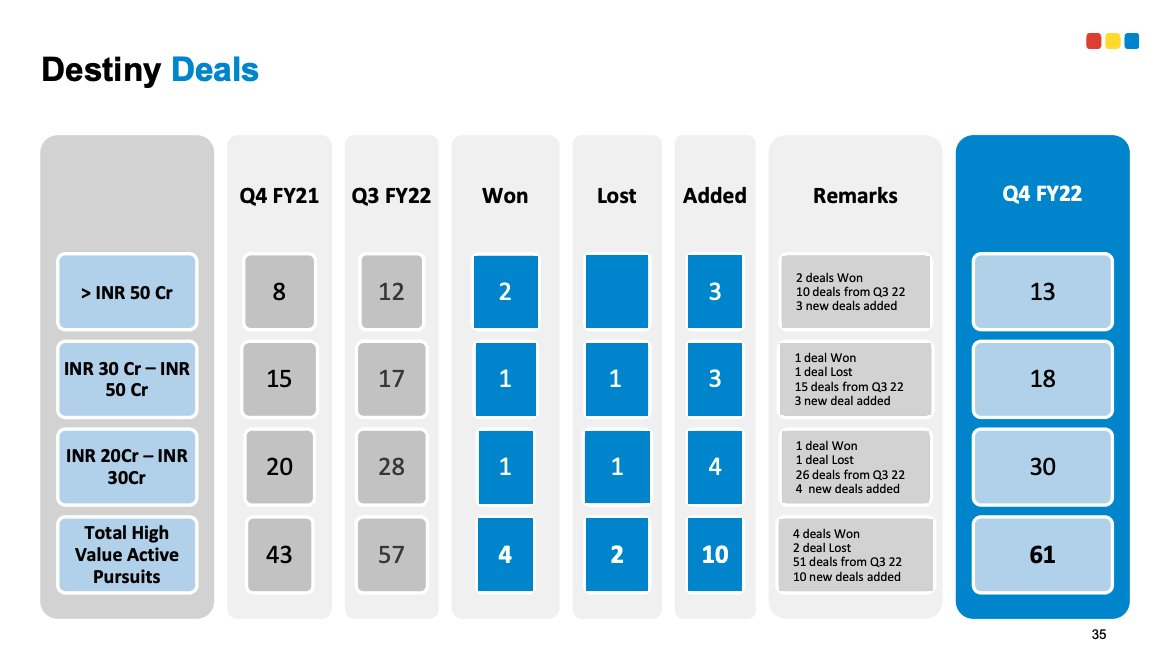

(iv) Intellect counts its high value strategic deals separately as destiny deals. See deal win rate.

(v) in FY23, the optimal tax rate goes up. to26%, but intellect has MAT credits so cash tax rate woud be 17-18%. Right metric to see profitability in next 2 years would be EBITDA.

6. Valuation

The valuation part should always be the shortest.

6. Valuation

The valuation part should always be the shortest.

Because the margin of safety is in moats + growth.

26 times trailing earnings. 22 times Q3/Q4 annualized earnings ex-cash. 17 times FY23 earnings. 25% ROCE. 20-30% growth.

26 times trailing earnings. 22 times Q3/Q4 annualized earnings ex-cash. 17 times FY23 earnings. 25% ROCE. 20-30% growth.

To a person who has strong conviction in next year growth, this can be a screaming buy.

To a person who is uncertain about earnings growth, this can appear to be expensive. This is why its a business analysts's market.

To a person who is uncertain about earnings growth, this can appear to be expensive. This is why its a business analysts's market.

Do deeper dive, either build conviction, or help destroy the investor's conviction, make the market more efficient.

7. Anti-thesis

(i) Aggressive accounting: Intellect capitalizes 5% of R&D expenses. It says that these products will last decades so similar to capex for a manufacturing co, why should we not depreciate (or ammortize) these expenses.

(i) Aggressive accounting: Intellect capitalizes 5% of R&D expenses. It says that these products will last decades so similar to capex for a manufacturing co, why should we not depreciate (or ammortize) these expenses.

this is definitely considered to be aggressive accounting.

(ii) Management Quality: Intellect twitter account retweeted their brokerage report.

Some investors find this outrageous I personally do not read too much into it. Diversity of opinions make a market, i respect everyone who disagrees with me.

Some investors find this outrageous I personally do not read too much into it. Diversity of opinions make a market, i respect everyone who disagrees with me.

(iii) Management Quality: arun jain had an insider trading case by sebi which he settled.

business-standard.com

Arun jain said in concall that he had won such case twice in past. Settled this one to avoid getting distracted from execution.

business-standard.com

Arun jain said in concall that he had won such case twice in past. Settled this one to avoid getting distracted from execution.

Up to each investor how they see this info.

(iv) Execution risk: According to me, this is most important risk. B2B digital is a very hot market. Its difficult to gauge or keep track of competitive intensity.

(iv) Execution risk: According to me, this is most important risk. B2B digital is a very hot market. Its difficult to gauge or keep track of competitive intensity.

On some metrics right now intellect seems to be ahead, but can it lose its lead? definitely.

(v) Banking, insurance is a heavily regulated pace so any adverse regulation would present risk.

8. Disclaimer/disclosure

I am invested with 5% position with average buying price 2% lower than CMP.

Of course i am positively biased. I am not a sebi registered financial advisor. Do not clone my decisions. I can change my mind in a day, week, month year or decade.

I am invested with 5% position with average buying price 2% lower than CMP.

Of course i am positively biased. I am not a sebi registered financial advisor. Do not clone my decisions. I can change my mind in a day, week, month year or decade.

This is not a buy recommendation. Do your own due diligence. only use this thread as a starting point of research, do your own deep dive OR consult with your financial advisor.

9. Summary

Intellect is digitally transforming the ancient legacy infra of banks & financial institutions through a suite of products, platforms, marketplace strategy leveraging latest technologies winning deals, delivering digital transformation. I am invested, biased.

Intellect is digitally transforming the ancient legacy infra of banks & financial institutions through a suite of products, platforms, marketplace strategy leveraging latest technologies winning deals, delivering digital transformation. I am invested, biased.

If you do find this thread useful, please consider retweeting the 1st tweet.

Please consider following me if you want to read similar threads in the future. 🙏🙏

Please consider following me if you want to read similar threads in the future. 🙏🙏

A meta thread of all my threads:

Happy weekend

Loading suggestions...