Beta Drugs conducted the conference call for Q4 FY22.

"Mgmt targets to grow at 30% CAGR for next 3-4 years"

Here are the concall highlights

🧵👇

"Mgmt targets to grow at 30% CAGR for next 3-4 years"

Here are the concall highlights

🧵👇

Business Updates:

• Exports, Price Realization and innovation in drugs led to growth for the company.

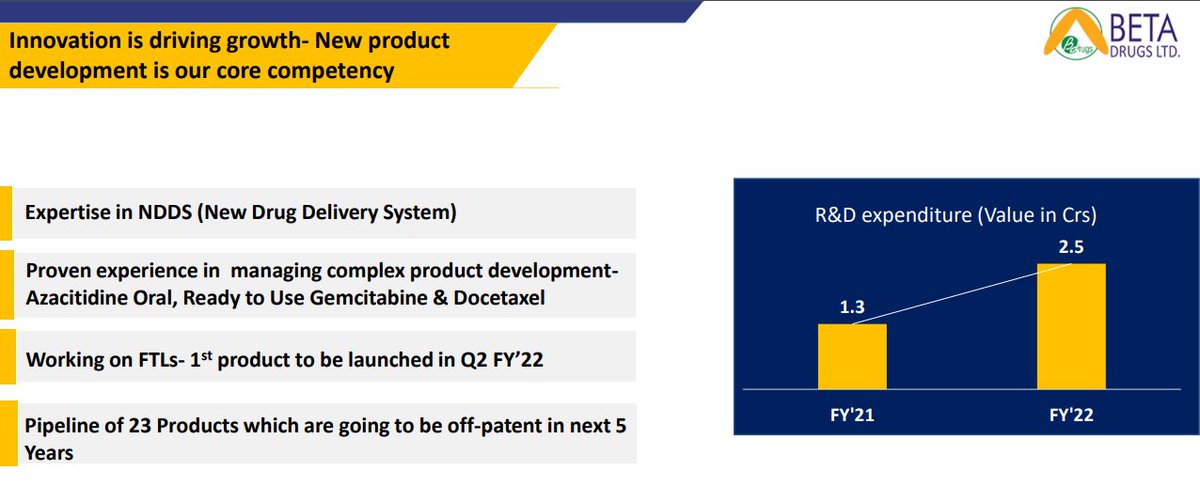

• In FY22, Beta has launched 15 new molecules and got DCI approval of Azacitidine Oral tablet.

• In april co. also got approval of Cabozantinib for API & formulation.

• Exports, Price Realization and innovation in drugs led to growth for the company.

• In FY22, Beta has launched 15 new molecules and got DCI approval of Azacitidine Oral tablet.

• In april co. also got approval of Cabozantinib for API & formulation.

Product Portfolio:

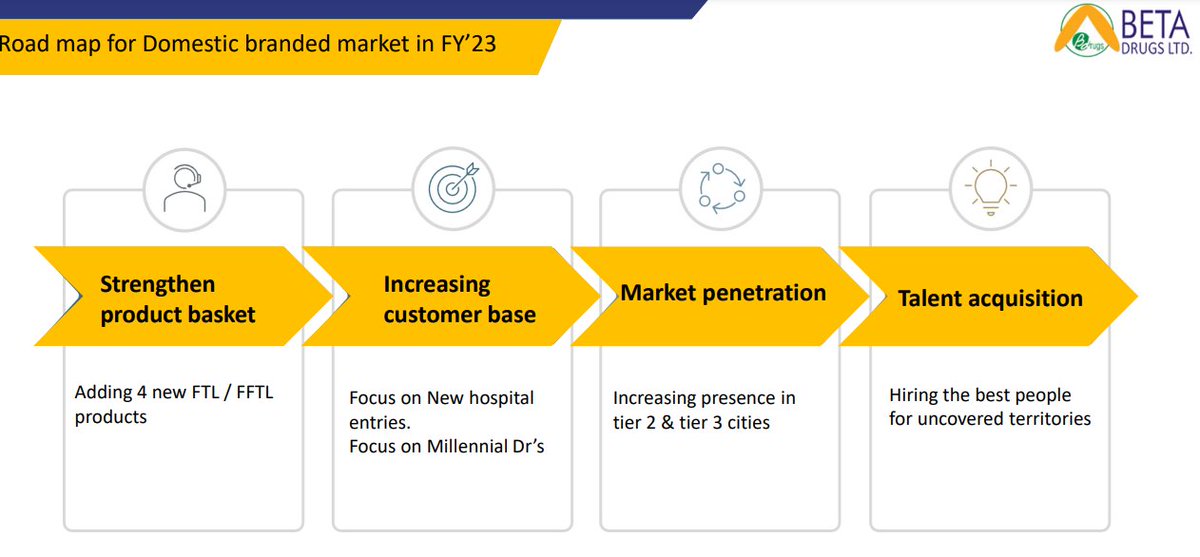

• Co. is expecting for more approval of drug in coming quarter.

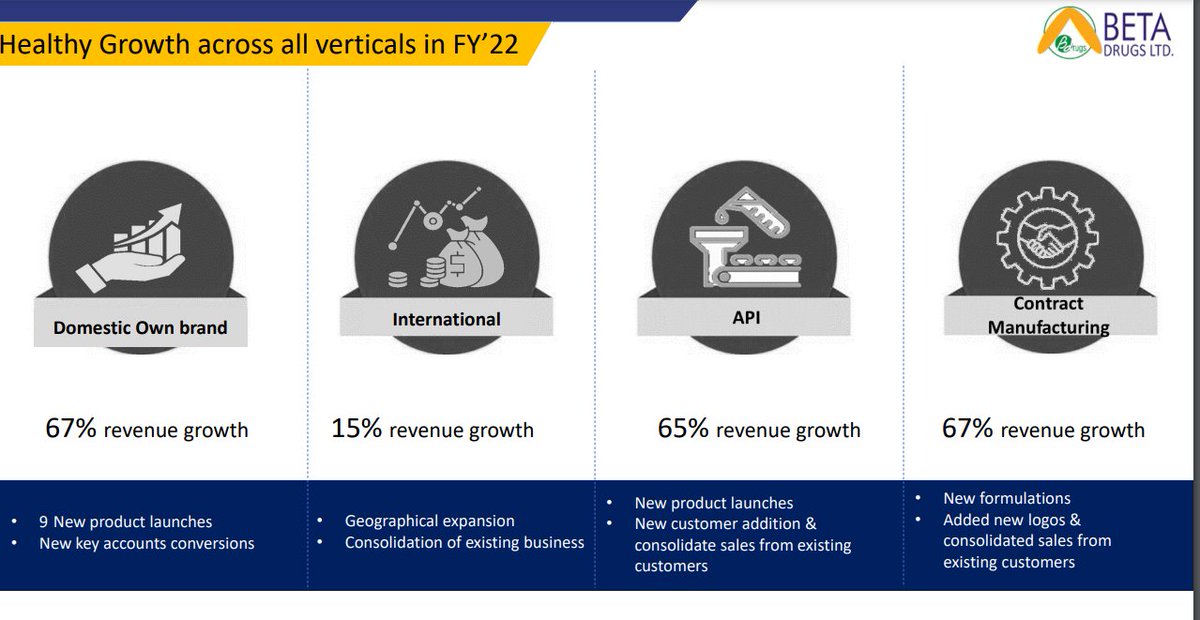

• Beta's own brand grew about 67%, and 2 brands have occupied no 1 position in India.

• International business has grew by 15%.

• API & Cram business has grew 60+% over last year.

• Co. is expecting for more approval of drug in coming quarter.

• Beta's own brand grew about 67%, and 2 brands have occupied no 1 position in India.

• International business has grew by 15%.

• API & Cram business has grew 60+% over last year.

Revenue Mix:

- 21cr for export market, with 18% growth.

- Domestic Business has 55cr of contribution.

Expected Revenue share

Domestic : Export : CRAMS - 35:30:35

Margin Share:

- Own Brand: 30-31%

- Export: 27-30%

- API: 24-26%

- 21cr for export market, with 18% growth.

- Domestic Business has 55cr of contribution.

Expected Revenue share

Domestic : Export : CRAMS - 35:30:35

Margin Share:

- Own Brand: 30-31%

- Export: 27-30%

- API: 24-26%

API:

• Received WHO for the API facility. It will help for both domestic and international market.

• Co. has launched 13 products.

• Expansion will drive growth for the company, with filing of new molecules.

• Received WHO for the API facility. It will help for both domestic and international market.

• Co. has launched 13 products.

• Expansion will drive growth for the company, with filing of new molecules.

CRAMS:

• Beta has participated with 50+ companies till now and plans to add 5-7 new companies for Fy23. (In Fy 22 co. added 7 new cos.)

• Beta has participated with 50+ companies till now and plans to add 5-7 new companies for Fy23. (In Fy 22 co. added 7 new cos.)

Oncology:

• Current market size of Onco is 4750cr and Beta market share is 3.75% only.

• Co. had started to in all the semi-regulated market & will shift to regulated market.

• Co. targets for 14-15% market share.

Zydus, Dr Reddy, Natco, Cipla

• Current market size of Onco is 4750cr and Beta market share is 3.75% only.

• Co. had started to in all the semi-regulated market & will shift to regulated market.

• Co. targets for 14-15% market share.

Zydus, Dr Reddy, Natco, Cipla

CAPEX:

• Lypholizer capacity increased to 3 folds in Beta drugs plant.

• Separate lypholized injectable manufacturing facility for general inject able in Adley formulations plant has been made.

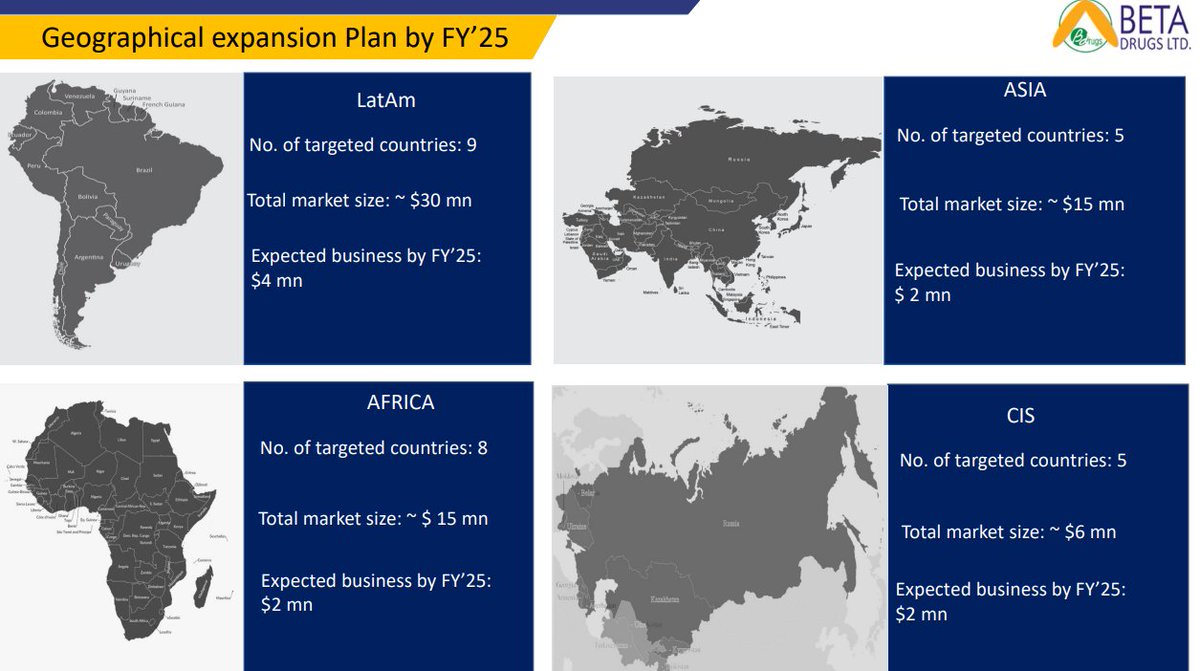

(Geographic expansion in image).

• Lypholizer capacity increased to 3 folds in Beta drugs plant.

• Separate lypholized injectable manufacturing facility for general inject able in Adley formulations plant has been made.

(Geographic expansion in image).

• Installed 2 new Lypholizer and the. Co. will be focusing on OEM parts and non-regulated market.

Plant is expected to commence by June end and all the license has been procured.

• Co. will focusing on anti-fungal & immunosuppressant segment.

Plant is expected to commence by June end and all the license has been procured.

• Co. will focusing on anti-fungal & immunosuppressant segment.

Growth Strategy:

Capacity utilization:

- Oral: 67%

- Injectables: 45%

- API: 30-40% (including recent plant addition.)

With optimum utilization revenuer potential is 300cr+, excluding the current capacity plants.

Capacity utilization:

- Oral: 67%

- Injectables: 45%

- API: 30-40% (including recent plant addition.)

With optimum utilization revenuer potential is 300cr+, excluding the current capacity plants.

Margins:

• EBIDTA margins is expected to grow by 1% and in 3-4 years mgmt expect margins to be ~26-27%.

• Dependency on RM sourcing from China has reduced from 42-45% to ~35% & co. is planning for backward integration for reducing permanent dependency

This will be one in FY25

• EBIDTA margins is expected to grow by 1% and in 3-4 years mgmt expect margins to be ~26-27%.

• Dependency on RM sourcing from China has reduced from 42-45% to ~35% & co. is planning for backward integration for reducing permanent dependency

This will be one in FY25

Other:

• Company has reduced the debtor days to 90 days from 110 days, due to better realization and continue follow-ups.

• Beta is now net debt free.

• Working Capital days has been improved a lot.

• Post MAT credit tax rate will shift to 22%.

• Company has reduced the debtor days to 90 days from 110 days, due to better realization and continue follow-ups.

• Beta is now net debt free.

• Working Capital days has been improved a lot.

• Post MAT credit tax rate will shift to 22%.

Loading suggestions...