Windlas Biotech conducted the conference call for Q4 FY22

Here are the concall highlights

🧵👇

Here are the concall highlights

🧵👇

Business Updates:

• CDMO service revenue stood at 379cr (4% YoY). Chronic & Sub chronic segment has higher revenue share.

• Received GNP certificate from South Africa which was filed in 2021.

• EU-GMP inspection completed for plant 4at Dehradun with 0 critical observations.

• CDMO service revenue stood at 379cr (4% YoY). Chronic & Sub chronic segment has higher revenue share.

• Received GNP certificate from South Africa which was filed in 2021.

• EU-GMP inspection completed for plant 4at Dehradun with 0 critical observations.

Industry:

• In H1, company did face supply chain issue, while the supply chain issue has now been normalized in H2.

Revenue Target for FY22:

- Domestic: 65-70%

- CDS: 15-20%

- Export: 10%

- Injectables: 5-10%

• In H1, company did face supply chain issue, while the supply chain issue has now been normalized in H2.

Revenue Target for FY22:

- Domestic: 65-70%

- CDS: 15-20%

- Export: 10%

- Injectables: 5-10%

Segmental Revenue:

• Export business was 20.9cr (up 10.2% YoY) contributing 4% of revenue. (9.5cr for Q4)

• Company will expand in new geographies and new product will drive export market.

• Export business was 20.9cr (up 10.2% YoY) contributing 4% of revenue. (9.5cr for Q4)

• Company will expand in new geographies and new product will drive export market.

CDMO:

• Revenue for Q4 was 96.9cr (up 11.4% YoY). Contributed 79% of revenue.

- New patent expiry launches

- Increasing wallet share from existing customer

- Foray into injectables

- New customer additon

will drive growth.

• Chronic segment is expected to show higher growth.

• Revenue for Q4 was 96.9cr (up 11.4% YoY). Contributed 79% of revenue.

- New patent expiry launches

- Increasing wallet share from existing customer

- Foray into injectables

- New customer additon

will drive growth.

• Chronic segment is expected to show higher growth.

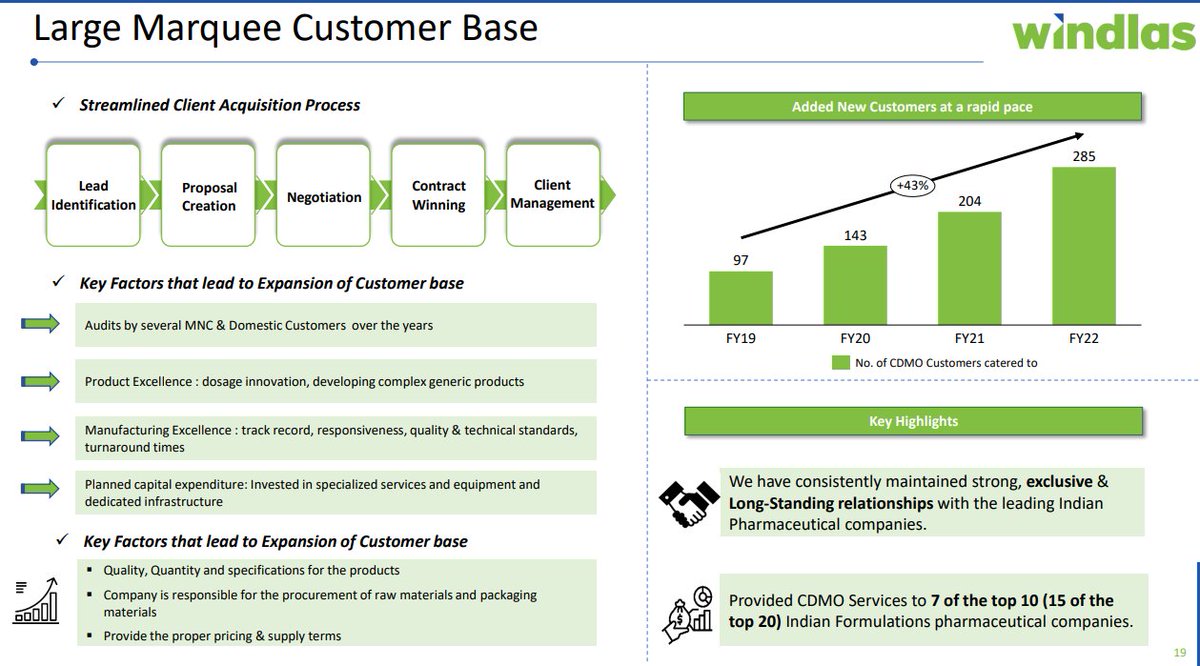

Customer:

• Co. is looking to reduce the dependency on single customer.

• CDMO growth was resulted from new customer.

• With increase in wider range of services, slowly revenue per customer will increase. For short-term company is looking to add on more customer.

• Co. is looking to reduce the dependency on single customer.

• CDMO growth was resulted from new customer.

• With increase in wider range of services, slowly revenue per customer will increase. For short-term company is looking to add on more customer.

Trade Generics:

• Revenue for Q4: 14.7cr (up 30.8% YoY). Contributed 13% of consol revenue.

• Chanel, product & geographic expansion will drive growth for growth. While government policy will help as well.

• Revenue for Q4: 14.7cr (up 30.8% YoY). Contributed 13% of consol revenue.

• Chanel, product & geographic expansion will drive growth for growth. While government policy will help as well.

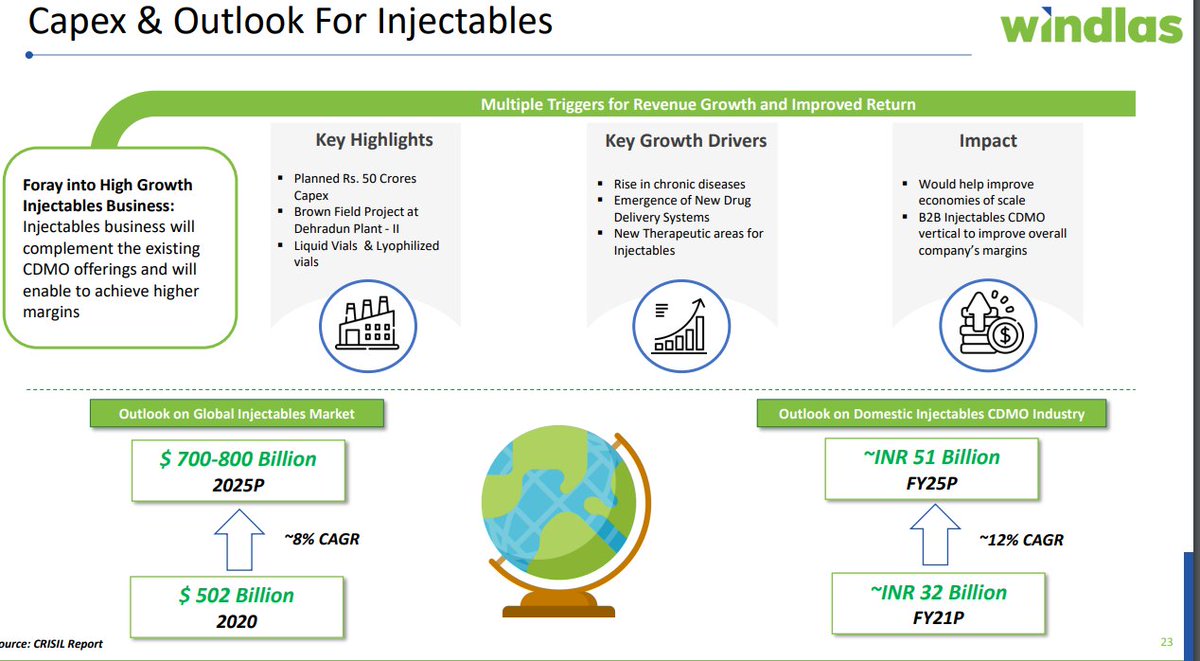

Injectables:

• Injectable business will be a higher margin business.

• Sales is expected to begn by end of year, & there may be losses for 1 year or so.

• Mgmt expect by FY25-26, injectables to deliver its growth

• Asset Turn: 1.25

Conti.

• Injectable business will be a higher margin business.

• Sales is expected to begn by end of year, & there may be losses for 1 year or so.

• Mgmt expect by FY25-26, injectables to deliver its growth

• Asset Turn: 1.25

Conti.

• With investment of 70cr, revenue potential is 175cr with 18-19% of EBIDTA, for injectables business.

Inorganic Business:

• For inorganic expansion company has criteria of

- Company should be well growing business

- Value addition of company with respect to Windlas.

Inorganic Business:

• For inorganic expansion company has criteria of

- Company should be well growing business

- Value addition of company with respect to Windlas.

R&D:

• R&D cost have grown at 16% since 2019, & is expected to reap its benefits in coming years.

• R&D expense increased by 2.9cr & product registration cost has increased by 1cr, which had drag margin down for CDMO.

• R&D cost have grown at 16% since 2019, & is expected to reap its benefits in coming years.

• R&D expense increased by 2.9cr & product registration cost has increased by 1cr, which had drag margin down for CDMO.

Loading suggestions...