Notes on @7Innovator's interview with @saxena_puru:

"Investing in the Stock Market in 2022"

Watch: youtube.com youtube.com

Topics:

- Slowing Economy

- Inflation Peaking

- Yield Curve

- Index Bottom

- Comparisons to '08 and Dot-com

// THREAD

"Investing in the Stock Market in 2022"

Watch: youtube.com youtube.com

Topics:

- Slowing Economy

- Inflation Peaking

- Yield Curve

- Index Bottom

- Comparisons to '08 and Dot-com

// THREAD

@7Innovator @saxena_puru Puru Saxena is an investor in the high-growth technology space.

Late last year, he forecasted the ongoing sell-off in equities when the Fed abruptly reversed their policies.

He argues that monetary policy and liquidity drives booms and busts.

Late last year, he forecasted the ongoing sell-off in equities when the Fed abruptly reversed their policies.

He argues that monetary policy and liquidity drives booms and busts.

@7Innovator @saxena_puru What caused the boom/bubble in financial markets?

Huge amounts of fiscal and monetary stimulus starting in 2020 caused an enormous boom but unsustainable boom in the economy.

Many stocks went up 4-6x in a year. This almost never happens!

Huge amounts of fiscal and monetary stimulus starting in 2020 caused an enormous boom but unsustainable boom in the economy.

Many stocks went up 4-6x in a year. This almost never happens!

@7Innovator @saxena_puru Inflation and Growth.

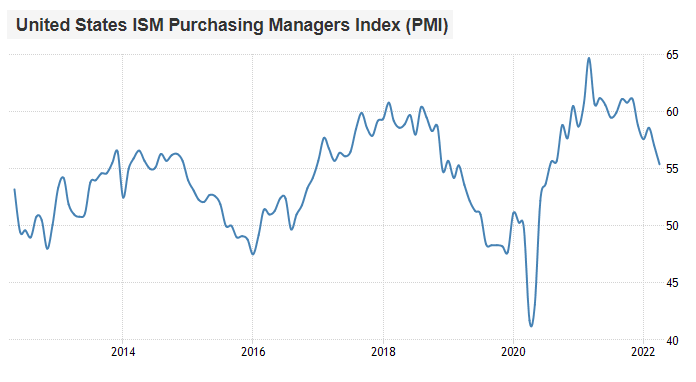

Saxena expects PMI Index to come down to 51-53, suggesting a sharp economic slowdown.

He also believes CPI is peaking and should start to roll-over due to the Fed's tightening. Monetary policy works with a lag.

Saxena expects PMI Index to come down to 51-53, suggesting a sharp economic slowdown.

He also believes CPI is peaking and should start to roll-over due to the Fed's tightening. Monetary policy works with a lag.

@7Innovator @saxena_puru When economy decelerates and inflation rolls over, long-term bond yields should start sliding.

This would be good for long duration secular growth stocks.

As economy slows and cyclical companies, secular compounders should outperform as they depend less on the economy.

This would be good for long duration secular growth stocks.

As economy slows and cyclical companies, secular compounders should outperform as they depend less on the economy.

@7Innovator @saxena_puru What's most vulnerable now?

- Defensive

- Dividend stocks

- Energy

- Commodities

These have all seen sharp rallies.

- Defensive

- Dividend stocks

- Energy

- Commodities

These have all seen sharp rallies.

@7Innovator @saxena_puru Erickson asks: will growth style investing continue in the same form (past 12-13 years) when money was cheap and managers could be more aggressive?

Puru: The time to be negative on growth stocks was last year. Not now when outstanding businesses are down 50-60% or more.

Puru: The time to be negative on growth stocks was last year. Not now when outstanding businesses are down 50-60% or more.

@7Innovator @saxena_puru Investors that bought high-quality names after massive drawdowns in the Dot-com bubble made a fortune.

There were huge discounts on names like Amazon, Apple and Google.

Though there are many rubbish businesses, those who can identify top companies at discounts can do very well.

There were huge discounts on names like Amazon, Apple and Google.

Though there are many rubbish businesses, those who can identify top companies at discounts can do very well.

@7Innovator @saxena_puru Great businesses have:

Strong cash-flows

Great leadership

High margins

Revenue growth

Solid market positioning

Low competition

Outstanding businesses may take 4-5 years to reach new ATHs.

IRR would still be great: a 3x gain in 4-5 years corresponds to a 15-20% annual return.

Strong cash-flows

Great leadership

High margins

Revenue growth

Solid market positioning

Low competition

Outstanding businesses may take 4-5 years to reach new ATHs.

IRR would still be great: a 3x gain in 4-5 years corresponds to a 15-20% annual return.

@7Innovator @saxena_puru Erickson: Who are the winners and losers from inflation?

Puru says:

Winners: Companies or industries that benefit from rising commodity prices and supply chain bottlenecks.

Losers: Companies with no pricing power and dependent on consumer discretionary spending.

Puru says:

Winners: Companies or industries that benefit from rising commodity prices and supply chain bottlenecks.

Losers: Companies with no pricing power and dependent on consumer discretionary spending.

@7Innovator @saxena_puru Puru does not play the macro game of jumping in and out of sectors.

Very few people get it right consistently.

It is very hard to know when to get in and out trades.

He does expect to see commodity prices and producers come under severe pressure, especially as economy slows.

Very few people get it right consistently.

It is very hard to know when to get in and out trades.

He does expect to see commodity prices and producers come under severe pressure, especially as economy slows.

@7Innovator @saxena_puru Interest Rates and Yield Curve Inversion

Simon mentions the Yield Curve Inversion from April 1st, where the yield on the 2Yr Treasury exceeded that of the 10Yr.

This has only happened 4 times in the past 25 years:

1988, 1998, 2005, 2019.

Recessions followed every time.

Simon mentions the Yield Curve Inversion from April 1st, where the yield on the 2Yr Treasury exceeded that of the 10Yr.

This has only happened 4 times in the past 25 years:

1988, 1998, 2005, 2019.

Recessions followed every time.

@7Innovator @saxena_puru Puru argues that the inversion is not a valid recession signal yet.

He looks for a persistent inversion of 60-90 consecutive days.

As soon as the inversion happened, the Fed sent Bullard and other hawks to talk about QT.

Consequently, long-term yields rose and curve steepened.

He looks for a persistent inversion of 60-90 consecutive days.

As soon as the inversion happened, the Fed sent Bullard and other hawks to talk about QT.

Consequently, long-term yields rose and curve steepened.

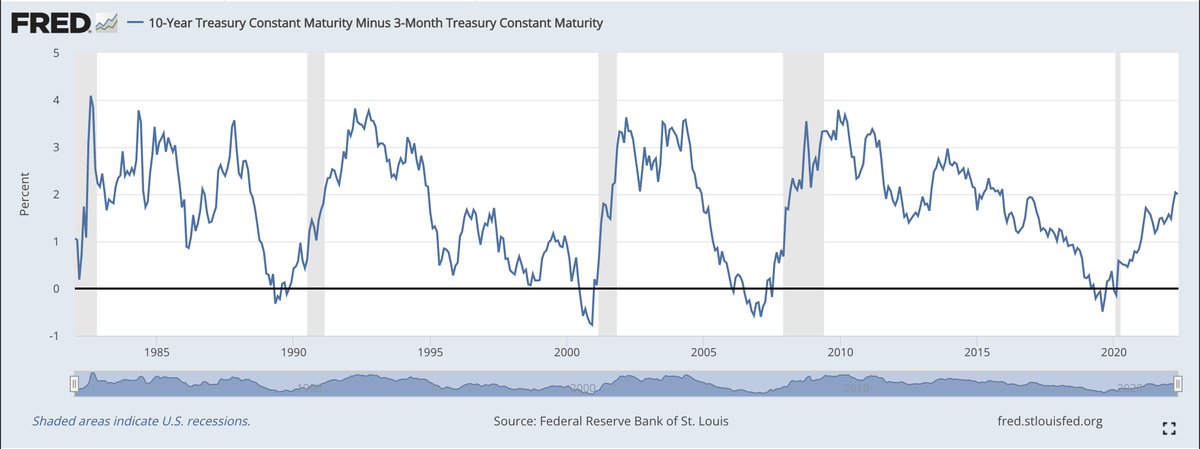

@7Innovator @saxena_puru Saxena also looks at the spread between the 10Yr Treasury and the 3 Month Treasury.

This hasn't inverted in this cycle.

He also notes that a persistent inversion doesn't mean a recession is coming right away. In many cases, it takes 12-18 months after inversion.

This hasn't inverted in this cycle.

He also notes that a persistent inversion doesn't mean a recession is coming right away. In many cases, it takes 12-18 months after inversion.

@7Innovator @saxena_puru Simon: Recession doesn't mean doom and gloom for the stock market.

Stock market is predictive of the future state of the economy. Stocks fall first before recession takes place.

Data from LPL Research shows that the S&P tends to perform well after an inversion.

Stock market is predictive of the future state of the economy. Stocks fall first before recession takes place.

Data from LPL Research shows that the S&P tends to perform well after an inversion.

@7Innovator @saxena_puru Puru: Stock market looks ahead.

It tops when the best has been discounted and bottoms when the worst has been discounted.

News trails financial markets.

Stocks bottom when the news is absolutely scary, frightening and dire.

It tops when the best has been discounted and bottoms when the worst has been discounted.

News trails financial markets.

Stocks bottom when the news is absolutely scary, frightening and dire.

@7Innovator @saxena_puru Puru does not think the current situation is similar to the 2008/2009 cycle.

We've had excesses in the equity market but that is being corrected.

Saxena expects another 7-10% decline in indices (from time of recording) but does not expect a 40-50% crack from here.

We've had excesses in the equity market but that is being corrected.

Saxena expects another 7-10% decline in indices (from time of recording) but does not expect a 40-50% crack from here.

@7Innovator @saxena_puru Valuations at the index level are still elevated:

S&P Forward P/E is at ~17.5x

Nasdaq Forward P/E is at ~20x

If we look at 2011, 2015, 2016, 2018 and COVID crash:

The S&P bottomed around 14x - 15x FPE.

Nasdaq bottomed around 18x - 19x FPE.

S&P Forward P/E is at ~17.5x

Nasdaq Forward P/E is at ~20x

If we look at 2011, 2015, 2016, 2018 and COVID crash:

The S&P bottomed around 14x - 15x FPE.

Nasdaq bottomed around 18x - 19x FPE.

@7Innovator @saxena_puru Simon: What is a good rule of thumb to value tech companies?

Puru: Depends on whether the company is profitable or not.

Currently, everyone hates unprofitable companies but many are unprofitable by design - reinvesting for growth instead of prioritizing profitability.

Puru: Depends on whether the company is profitable or not.

Currently, everyone hates unprofitable companies but many are unprofitable by design - reinvesting for growth instead of prioritizing profitability.

@7Innovator @saxena_puru Valuing profitable companies: EPS, EPS growth, P/E Ratio, Free Cash Flow.

Valuing unprofitable companies: Sales multiple, EV to Revenue, estimate earnings and cashflows 4-5 years into the future. Analyze historical multiples to see what average has been over the last ~5 years.

Valuing unprofitable companies: Sales multiple, EV to Revenue, estimate earnings and cashflows 4-5 years into the future. Analyze historical multiples to see what average has been over the last ~5 years.

@7Innovator @saxena_puru There are no perfect signs or metrics to use. Need to use your best judgment.

These are just some metrics that Puru looks at.

For all businesses - need to know the competitive positioning.

Warren Buffet refers to this as "Moat."

These are just some metrics that Puru looks at.

For all businesses - need to know the competitive positioning.

Warren Buffet refers to this as "Moat."

@7Innovator @saxena_puru How many positions to hold in your portfolio?

Puru likes holding 18-20 companies in his portfolio.

Good diversification benefits without watering down your returns.

Holding too many different positions leads to "diworsification."

Puru likes holding 18-20 companies in his portfolio.

Good diversification benefits without watering down your returns.

Holding too many different positions leads to "diworsification."

@7Innovator @saxena_puru Puru on Big Tech / FAANG stocks.

Much of S&P's returns over the last decade came from mega-cap tech.

Growth rates for these companies are slowing because they've become so big.

Puru doesn't see them as market leaders over the next decade.

Much of S&P's returns over the last decade came from mega-cap tech.

Growth rates for these companies are slowing because they've become so big.

Puru doesn't see them as market leaders over the next decade.

@7Innovator @saxena_puru Growth investing doesn't mean tech investing.

Last 40-50 years - biggest winners have been companies that have been able to grow rapidly for a long period of time.

Examples: Starbucks, McD, Nike, etc.

Industry doesn’t matter. Just need growth, profitability and free cash flow.

Last 40-50 years - biggest winners have been companies that have been able to grow rapidly for a long period of time.

Examples: Starbucks, McD, Nike, etc.

Industry doesn’t matter. Just need growth, profitability and free cash flow.

@7Innovator @saxena_puru Puru on QuantumScape $QS

This is Puru's play on clean energy and EVs.

Developing solid-state lithium batteries.

Management team is all Stanford grads.

Prominent shareholders (like Volkswagen).

Speculative investment:

Pre-revenue.

No commercial cell yet.

This is Puru's play on clean energy and EVs.

Developing solid-state lithium batteries.

Management team is all Stanford grads.

Prominent shareholders (like Volkswagen).

Speculative investment:

Pre-revenue.

No commercial cell yet.

@7Innovator @saxena_puru Dr. Stan Wittingham, inventor of the lithium-ion battery and Nobel Prize recipient, mentions that QuantumScape's advances with solid-state batteries are a "major breakthrough."

Puru's $QS holding is just about 3% of his total portfolio.

Puru's $QS holding is just about 3% of his total portfolio.

@7Innovator @saxena_puru Puru on Tesla $TSLA

Main concern is competition in EV space.

Saxena doesn't expect Tesla will lose its lead, but he doesn't like the high CapEx, cyclical nature of it.

He prefers battery makers - they provide the picks and shovels. Also less competition due to patents.

Main concern is competition in EV space.

Saxena doesn't expect Tesla will lose its lead, but he doesn't like the high CapEx, cyclical nature of it.

He prefers battery makers - they provide the picks and shovels. Also less competition due to patents.

@7Innovator @saxena_puru Saxena on Nu Holdings $NU

Latin American digital bank competing with big legacy banks.

Primarily in Brazil but also in other LatAm countries.

One stop shop - banking, credit, investing.

As a digital bank, costs are lower and they can offer better interest rates to customers.

Latin American digital bank competing with big legacy banks.

Primarily in Brazil but also in other LatAm countries.

One stop shop - banking, credit, investing.

As a digital bank, costs are lower and they can offer better interest rates to customers.

@7Innovator @saxena_puru Nu Holdings cont'd.

Saxena notes the fantastic revenue growth in the last few years.

Analyst estimates expect revenue to compound at 30-40% over the next 4-5 years.

Simon mentions digital banking is a natural winner as Latin America increases access to high-speed internet.

Saxena notes the fantastic revenue growth in the last few years.

Analyst estimates expect revenue to compound at 30-40% over the next 4-5 years.

Simon mentions digital banking is a natural winner as Latin America increases access to high-speed internet.

@7Innovator @saxena_puru Saxena on Mercado Libre $MELI

Puru was a shareholder for the last ~10 years.

E-commerce isn't the big growth segment anymore, now it's payments and FinTech.

Competition in LatAm is increasing.

Forward revenue growth estimates are below 30% YoY - signal for Puru to exit.

Puru was a shareholder for the last ~10 years.

E-commerce isn't the big growth segment anymore, now it's payments and FinTech.

Competition in LatAm is increasing.

Forward revenue growth estimates are below 30% YoY - signal for Puru to exit.

@7Innovator @saxena_puru $MELI is reaching a maturing stage.

Saxena tries to get in early in the S curve cycle. This is how you enjoy the effects of compounding.

Since growth is slowing, Puru sold out and moved to new holdings.

Saxena tries to get in early in the S curve cycle. This is how you enjoy the effects of compounding.

Since growth is slowing, Puru sold out and moved to new holdings.

@7Innovator @saxena_puru Saxena on South East Asia (SEA)

SEA has the toughest COVID restrictions in the world.

Vaccination rates have been low, countries have been slow to re-open and economies have taken a hit.

Puru is invested in US, Latin America or Europe companies. No exposure to Asian companies.

SEA has the toughest COVID restrictions in the world.

Vaccination rates have been low, countries have been slow to re-open and economies have taken a hit.

Puru is invested in US, Latin America or Europe companies. No exposure to Asian companies.

@7Innovator @saxena_puru Puru on position sizing.

High conviction: 6 or 7% at the outset.

Doesn’t necessarily trim if business is operating well, unless there’s a crazy mania like in 2020/2021.

He was getting years worth of returns in a few months, so it made sense to sell and take profits.

High conviction: 6 or 7% at the outset.

Doesn’t necessarily trim if business is operating well, unless there’s a crazy mania like in 2020/2021.

He was getting years worth of returns in a few months, so it made sense to sell and take profits.

@7Innovator @saxena_puru Trim/sell if the excessive returns are so glaringly obvious where you know future returns are going to be poor and there is not much upside left for these companies.

These instances are very rare.

These instances are very rare.

@7Innovator @saxena_puru Puru's hedging method.

Find an ETF or index futures that correlate with the holdings in your portfolio.

For Puru, it's $ARKK.

Puru places hedges during a downtrend.

He shorts with a 1:1 ratio - short exposure matches long exposure.

Find an ETF or index futures that correlate with the holdings in your portfolio.

For Puru, it's $ARKK.

Puru places hedges during a downtrend.

He shorts with a 1:1 ratio - short exposure matches long exposure.

@7Innovator @saxena_puru What classifies as a downtrend?

Look at medium term moving averages. Could be a 50day to 150day.

When the ETF or index future goes below that MA, he places the hedge.

In certain instances, he shorts Nasdaq Index Futures if he's particularly negative near-term.

Look at medium term moving averages. Could be a 50day to 150day.

When the ETF or index future goes below that MA, he places the hedge.

In certain instances, he shorts Nasdaq Index Futures if he's particularly negative near-term.

@7Innovator @saxena_puru In downtrends, the path of least resistance is downwards. He basically gets himself out of the market by being market neutral.

Typical growth portfolio this year would be down about 40-50%.

At the time of recording, Puru was down about ~15% due to the hedges.

Typical growth portfolio this year would be down about 40-50%.

At the time of recording, Puru was down about ~15% due to the hedges.

@7Innovator @saxena_puru Final Thoughts

Bulk of carnage in the high growth space is now behind us.

Puru expects that we'll see a pause from the Fed in the next few months as the economy slows down and inflation cools.

Risk assets will take off if this happens.

Bulk of carnage in the high growth space is now behind us.

Puru expects that we'll see a pause from the Fed in the next few months as the economy slows down and inflation cools.

Risk assets will take off if this happens.

@7Innovator @saxena_puru 2nd half of this year is likely to be better than the first half.

Beaten down, long duration stocks likely to take off over the next 12-15 months.

Lower the price, lower the risk. Many companies are trading at reasonable valuations.

Beaten down, long duration stocks likely to take off over the next 12-15 months.

Lower the price, lower the risk. Many companies are trading at reasonable valuations.

@7Innovator @saxena_puru Thanks for reading!

Special thanks to @7Innovator and @saxena_puru for the insights and analysis.

Thanks to @7investing for producing.

The full video is worth watching!

youtube.com

Special thanks to @7Innovator and @saxena_puru for the insights and analysis.

Thanks to @7investing for producing.

The full video is worth watching!

youtube.com

We'll be regularly sharing our notes and research across various topics in finance.

The financial world is complex, and we aim to produce content that is valuable to readers of all levels.

A follow, like and retweet 👇is greatly appreciated!

The financial world is complex, and we aim to produce content that is valuable to readers of all levels.

A follow, like and retweet 👇is greatly appreciated!

Loading suggestions...