Voltamp Transformers: Business Analysis

A Thread 🧵👇 (RT if beneficial)

A Thread 🧵👇 (RT if beneficial)

1/ Okay, they don't make those transformers but something which is much more important than them (until we have to fight space aliens I guess)

They make Transformers, the backbone of a functioning electricity supply chain.

They make Transformers, the backbone of a functioning electricity supply chain.

2/ How do Transformers work?

It's a device that transfers electric energy from one alternating-current circuit to one or more other circuits, either increasing (stepping up) or reducing (stepping down) the voltage.

Confused?

It's a device that transfers electric energy from one alternating-current circuit to one or more other circuits, either increasing (stepping up) or reducing (stepping down) the voltage.

Confused?

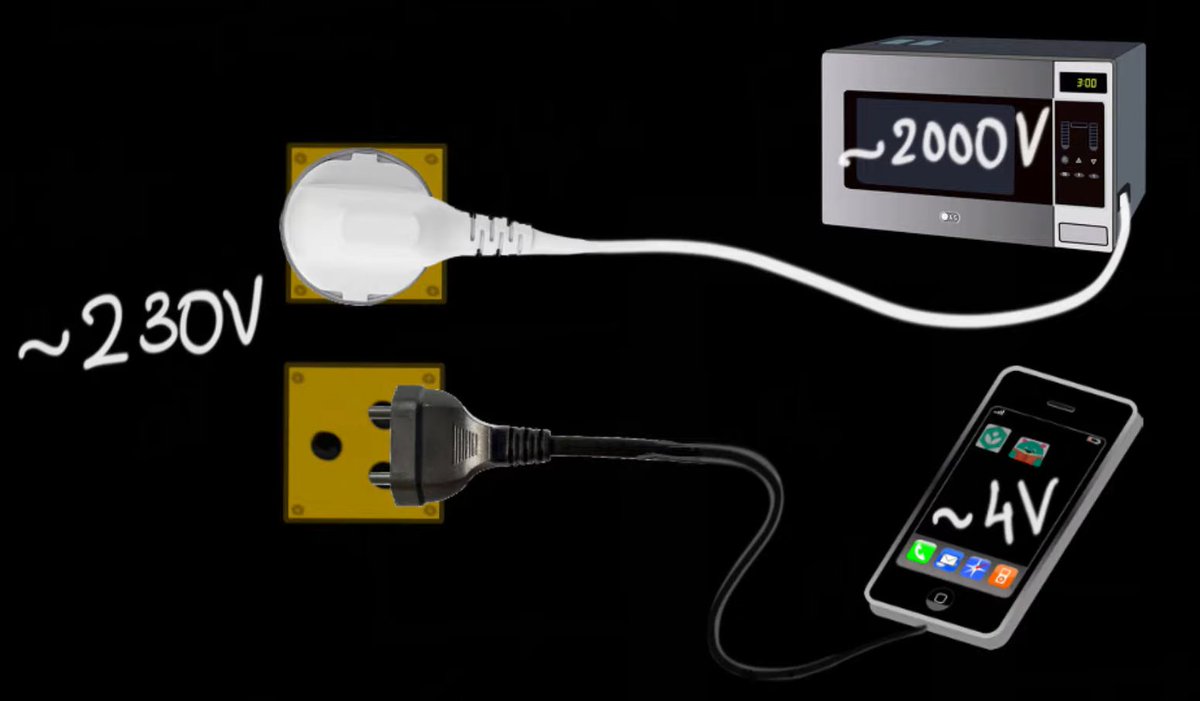

3/ Basically, it's transformers that allow you to charge your phone (which requires ~4V) & cook in a microwave (which requires ~2000V) from the same socket (which is ~230V)

Check out this video if you are curious for more: youtube.com

Check out this video if you are curious for more: youtube.com

4/ Transformers are of 2 types – Power transformers and Distribution transformers.

While both have the same modus operandi, power transformers are designed for high voltage load (33kv to 400kv), are built for 100% efficiency, and are used in nationwide power grids.

While both have the same modus operandi, power transformers are designed for high voltage load (33kv to 400kv), are built for 100% efficiency, and are used in nationwide power grids.

5/ Whereas Distribution transformers, have smaller capacities (less than 33kv) & are used by industries to align their electric equipment (furnaces, Lighting, etc) with the power from the grid.

Voltamp primarily operates here, focused on small industrial transformers up to 22kv.

Voltamp primarily operates here, focused on small industrial transformers up to 22kv.

6/ Opportunity size

In India, power transformers make up 45% of the INR 160-180 bn industry, while distribution transformers (incl. industrial) make up 55%.

Considering the above, companies in the business of transformer manufacturing rely on capex by

In India, power transformers make up 45% of the INR 160-180 bn industry, while distribution transformers (incl. industrial) make up 55%.

Considering the above, companies in the business of transformer manufacturing rely on capex by

7/ State Electricity Boards, State transmission cos., and PGCIL – Power Grid Corporation (for power and distribution transformers) and higher industrial capex (for industrial transformers).

Commoditised business, Industrial business relatively lesser.

Commoditised business, Industrial business relatively lesser.

8/ Competitive scenario: fragmented but consolidating

No new player has entered for 10 years now. Few have gone bankrupt & many others are in no position to take more work.

Some were closing but got a lease of life due to the moratorium.

No new player has entered for 10 years now. Few have gone bankrupt & many others are in no position to take more work.

Some were closing but got a lease of life due to the moratorium.

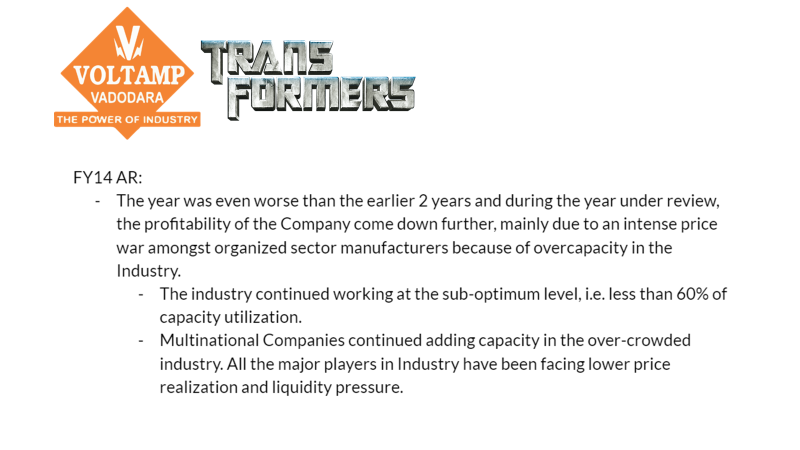

9/ Still, 100s of players remain.

A snippet from Voltamp's FY14 AR where they mentioned how MNCs continue to add capacity even when the demand was not increasing & the industry was working at a suboptimal utilization.

A snippet from Voltamp's FY14 AR where they mentioned how MNCs continue to add capacity even when the demand was not increasing & the industry was working at a suboptimal utilization.

10/ Sales growth is directly proportional to GDP growth (A direct play on private capex)

What interests me about Voltamp?

In the last up-cycle phase of FY03-09, it increased its EPS 21 times (from 5.3 to 114), with a 6-yr CAGR of 66%. Book value 11x.

What interests me about Voltamp?

In the last up-cycle phase of FY03-09, it increased its EPS 21 times (from 5.3 to 114), with a 6-yr CAGR of 66%. Book value 11x.

11/ After the same cycle, the rev hasn't grown in the last 10-12 years.

The last time Voltamp did put capex was in 2009 to increase their installed capacity to 13 GVA, so one can imagine the pain the industry players have gone through here.

The last time Voltamp did put capex was in 2009 to increase their installed capacity to 13 GVA, so one can imagine the pain the industry players have gone through here.

12/ Let's start with the strengths of Voltamp

a. In a commoditized business, brand matters & how does one differentiate? Quality, service, and on-time delivery. Due to this for many companies like L&T, Siemens, etc, Voltamp will always be their 1st supplier of choice.

a. In a commoditized business, brand matters & how does one differentiate? Quality, service, and on-time delivery. Due to this for many companies like L&T, Siemens, etc, Voltamp will always be their 1st supplier of choice.

13/ They boast of their transformers having a life of 30 years (Not verified); which is not given by most of the Chinese players who dump their products in India.

b. They do not bid for the govt. contracts just to increase their revenue, it's a good thing 👇

b. They do not bid for the govt. contracts just to increase their revenue, it's a good thing 👇

14/ c. They have ave been ahead of the curve in terms of technological change owing to technology transfer from MNCs, for which they pay a one-time fee.

15/ d. Very high Asset turnover business: not capital intensive (works for incumbents & entrants- low entry barriers)

Interestingly, players like Indo Tech and IMP Powers only made profits during the upcycle, bleeding red thereafter, Voltamp’s nos. have been relatively steady.

Interestingly, players like Indo Tech and IMP Powers only made profits during the upcycle, bleeding red thereafter, Voltamp’s nos. have been relatively steady.

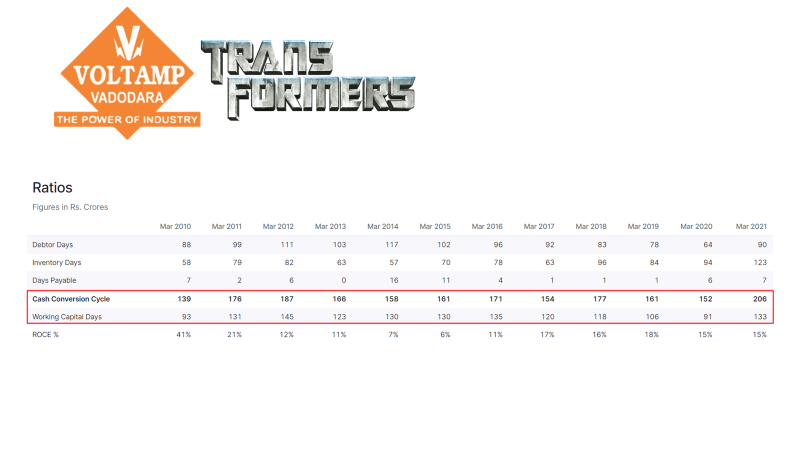

16/ e. Best Working capital management in the industry. Still, very high (3-4 months) due to the nature of the beast. High inventories & high credit periods.

However, Voltamp has been prompt in paying off its creditors in time. Good for relations.

However, Voltamp has been prompt in paying off its creditors in time. Good for relations.

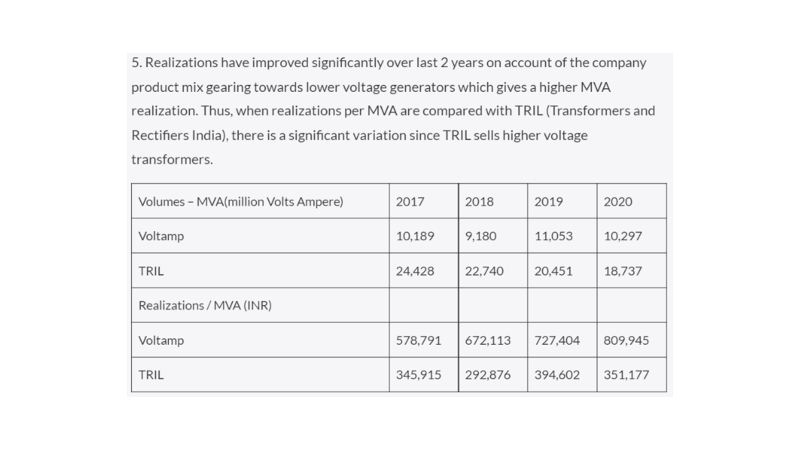

17/ f. During this down period, Voltamp has been able to increase their realizations per MVA (unit they sell); compared to others in the industry. [Source: Valupickr]

18/ Let's come to weaknesses

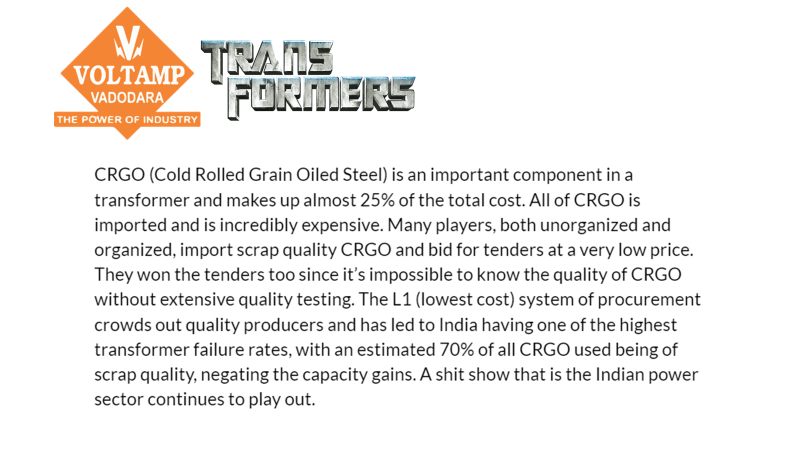

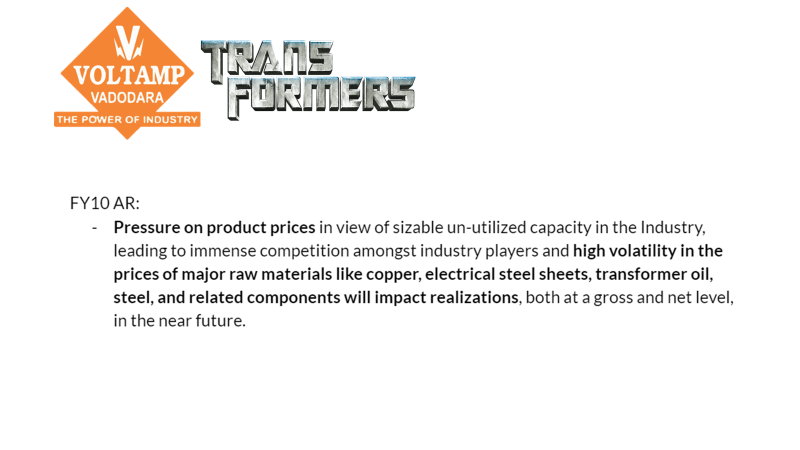

a. Gross margins are b/w 20-30% (expands & contracts as per the cycle)

Raw materials such as copper and cold rolled grain oriented (CRGO) steel (which account for ~60% of total RM cost)

Limited ability to pass on. FY10 anecdote 👇

a. Gross margins are b/w 20-30% (expands & contracts as per the cycle)

Raw materials such as copper and cold rolled grain oriented (CRGO) steel (which account for ~60% of total RM cost)

Limited ability to pass on. FY10 anecdote 👇

19/ b. No entry or exit barriers.

In the last upcycle, capacity increased from 135GVA in FY07 to 400GVA in FY16 (Voltamp transformers still at 13GVA) with the unorganized sector’s proportion increasing from lower single digits to 30%+.

In the last upcycle, capacity increased from 135GVA in FY07 to 400GVA in FY16 (Voltamp transformers still at 13GVA) with the unorganized sector’s proportion increasing from lower single digits to 30%+.

20/ c. Zero Negotiating power with the customers: No pass-through mechanism once the orders are booked in private orders (90%+ of rev)

Additionally, have to pass on all the RM price changes if it goes down (impacting revenues)

Additionally, have to pass on all the RM price changes if it goes down (impacting revenues)

21/ d. The company’s raw materials are primarily imported or international price linked and they don’t hedge the same. So, delayed payments always run a currency risk in case of Rupee devaluation.

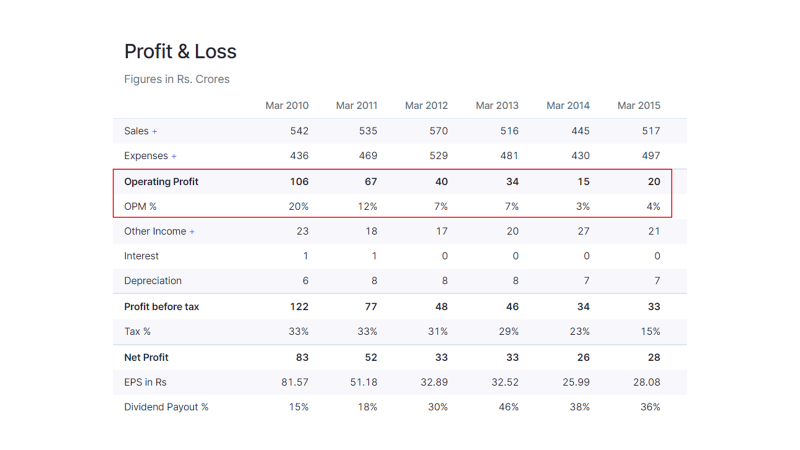

FY14 & FY15 witnessed the same when their margins went from 10-12% to 3-4%.

FY14 & FY15 witnessed the same when their margins went from 10-12% to 3-4%.

22/ e. Huge cash on books invested in mutual funds & PMS: What’s the point of not distributing that to shareholders & why is one taking so much risk with shareholder's capital?

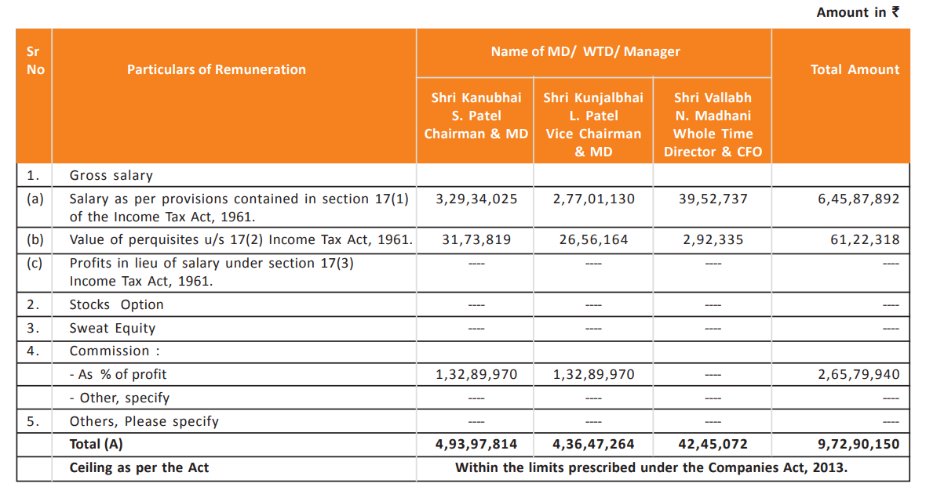

f. High Salaries: The 2 MDs cumulatively take 8-10% of PAT as remuneration which is quite high.

f. High Salaries: The 2 MDs cumulatively take 8-10% of PAT as remuneration which is quite high.

23/ g. Receivables issue if the customer goes bankrupt.

They have been proactive in not getting more than 10% of their revenue from renewables, due to the inherent risk of high fatality there (too many external things to depend on)

90% of the sales have been done to non-govt.

They have been proactive in not getting more than 10% of their revenue from renewables, due to the inherent risk of high fatality there (too many external things to depend on)

90% of the sales have been done to non-govt.

24/ h. Payment by customers is not in a single term. They release in parts like 10% after drawings, 40% after testing, 20% after commissions, etc. 10% of payment will be paid after a successful performance in the guarantee period i.e after 3 years of commission.

25/ Voltamp has to extend bank guarantees (both performance and financial) to its customers; the average tenor of performance bank guarantees (PBGs) extended by it for transformers sold by it ranges from 3-6 years.

This could result in unanticipated liabilities at any time.

This could result in unanticipated liabilities at any time.

26/ More threats:

Macroeconomic challenges like the recent $130 crude, rupee devaluation (have to import a lot of RMs/ components)

The industry is prone to aggressive bidding by incumbents leading to margin contraction from time to time.

Imports from Chinese & Koreans.

Macroeconomic challenges like the recent $130 crude, rupee devaluation (have to import a lot of RMs/ components)

The industry is prone to aggressive bidding by incumbents leading to margin contraction from time to time.

Imports from Chinese & Koreans.

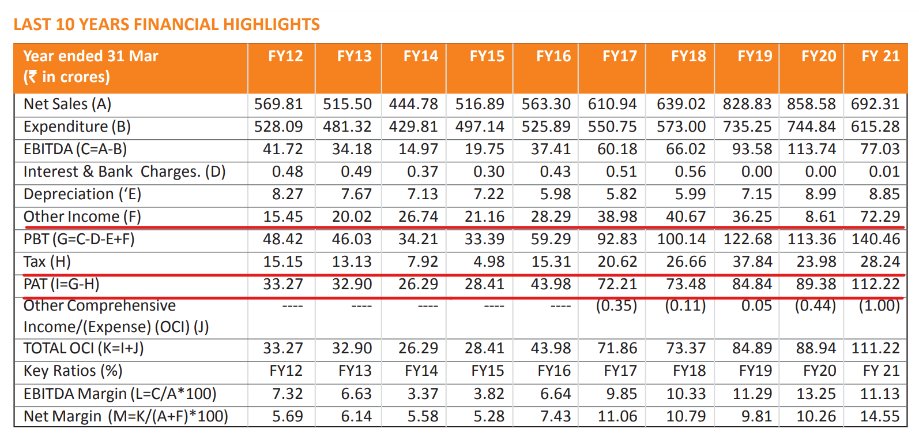

27/ Let's look at financials

- Things are improving finally for the better: Rev growth & subsequent margin expansion (not today, as the cycle picks up) is the key

- Debt-free balance sheet

- OCF conversion has been weak, will it change in an upcycle is a key trackable.

- Things are improving finally for the better: Rev growth & subsequent margin expansion (not today, as the cycle picks up) is the key

- Debt-free balance sheet

- OCF conversion has been weak, will it change in an upcycle is a key trackable.

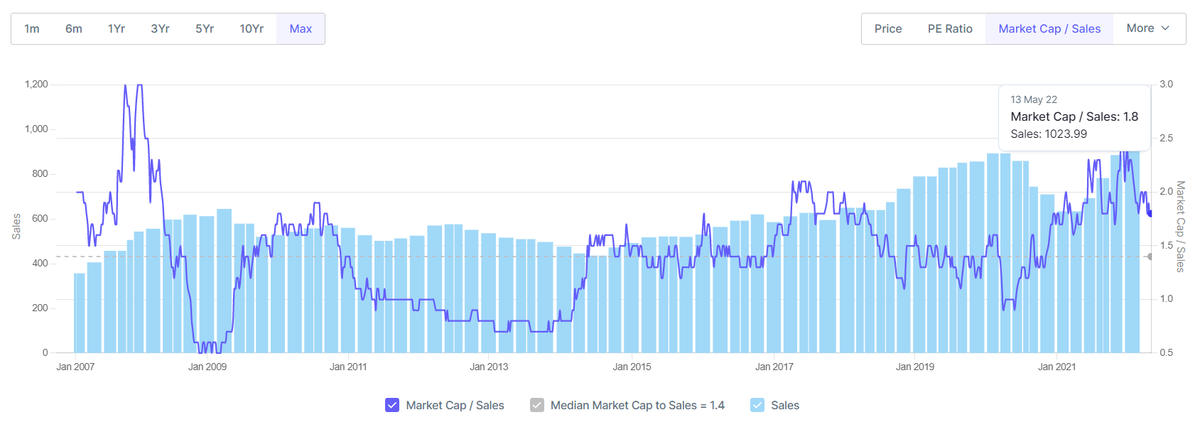

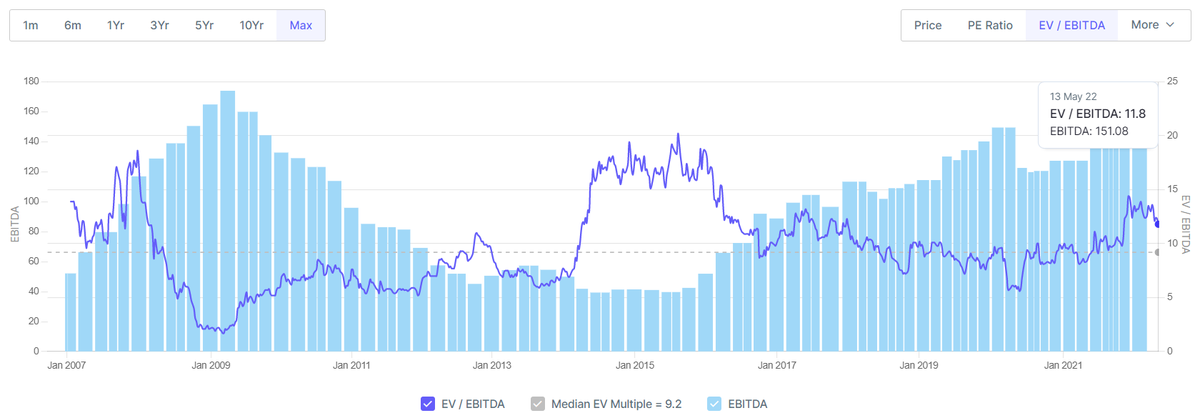

28/ Valuations & Conclusion

At 1.8K cr market cap; The stock is reasonably valued across P/E, P/Sales, or EV/EBITDA if we take a possible upcycle & 500+ crs in investments.

However, due to the weak business quality, I would prefer to buy it only when it's cheap.

End of Thread.

At 1.8K cr market cap; The stock is reasonably valued across P/E, P/Sales, or EV/EBITDA if we take a possible upcycle & 500+ crs in investments.

However, due to the weak business quality, I would prefer to buy it only when it's cheap.

End of Thread.

29/ If someone prefers to read in PDF format 👇

drive.google.com

drive.google.com

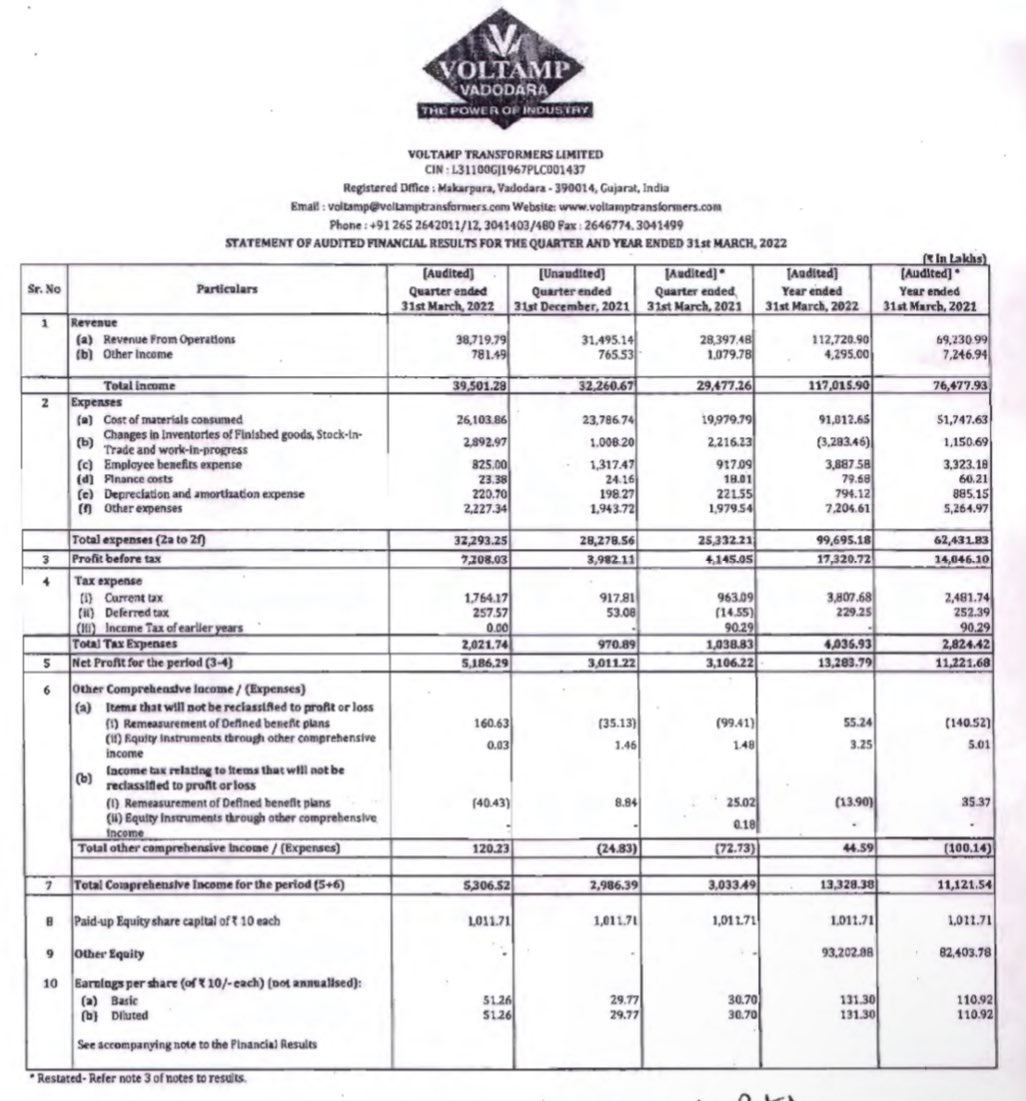

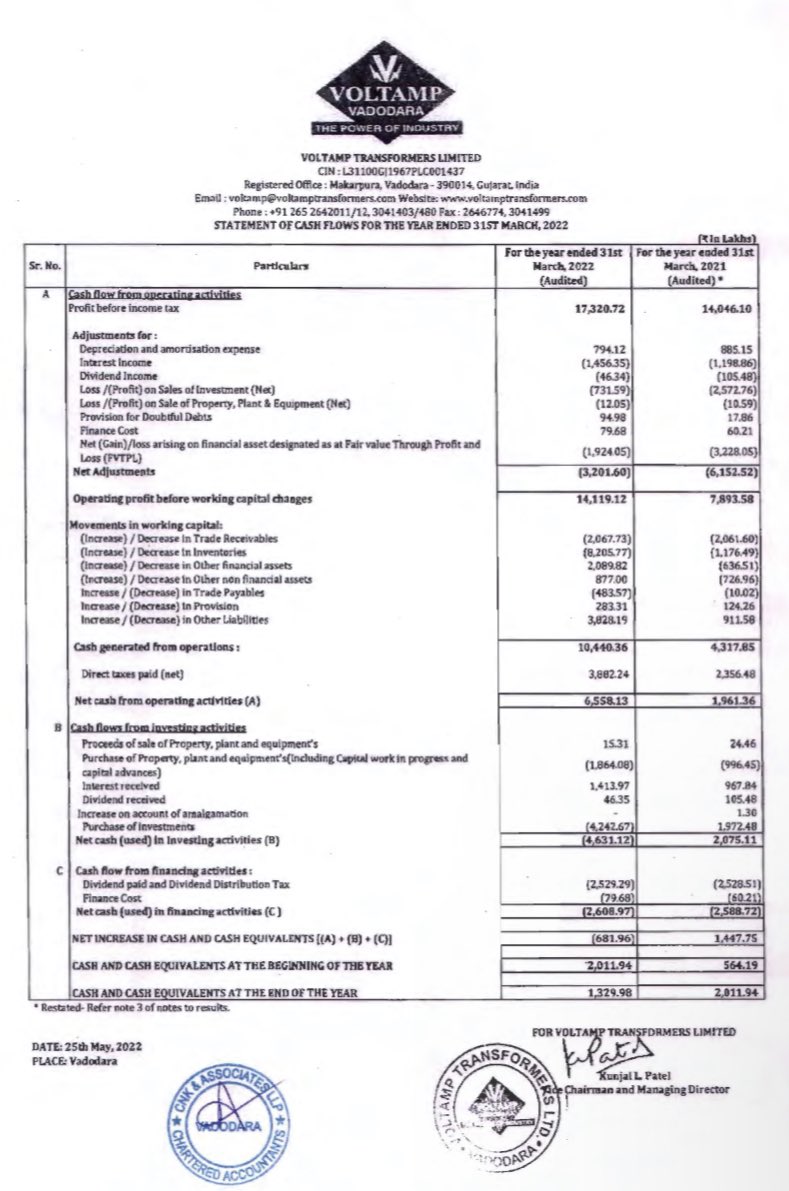

30/ Strong performance by Voltamp Transformers in FY22 (The increasing demand is visible), stable Cashflows.

Loading suggestions...