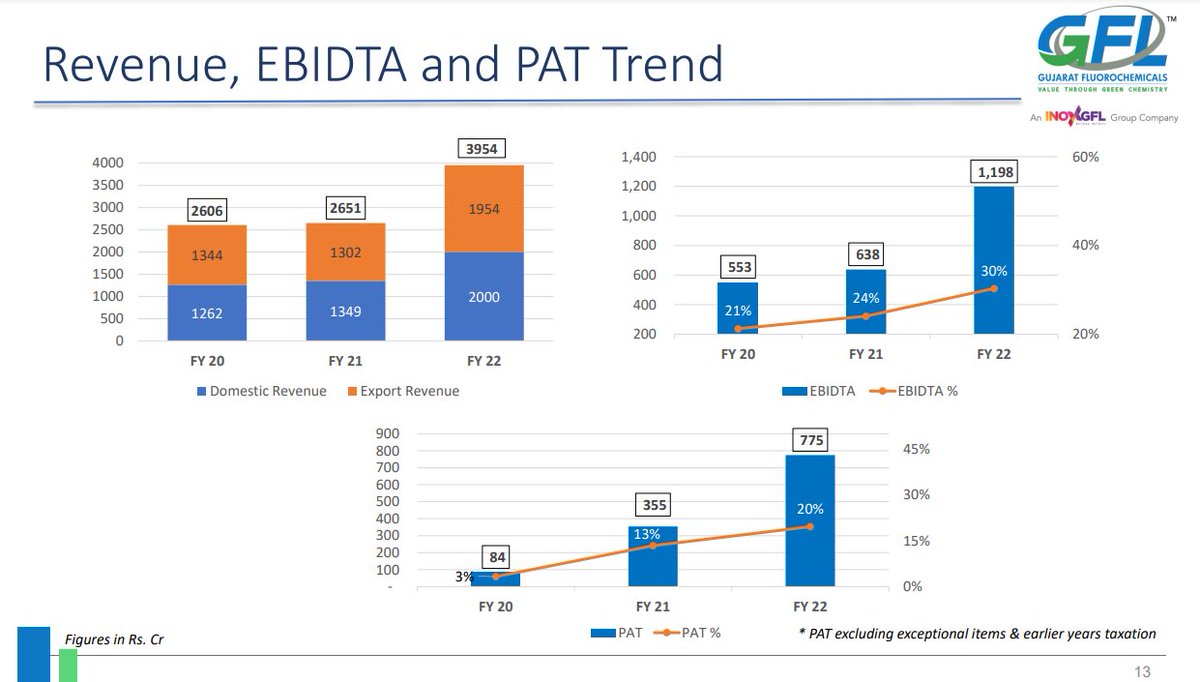

Gujarat Flurochemicals Ltd conducted the conference call for Q4 FY22

"Mgmt targets topline growth of 20-23% of FY23"

Here are the concall highlights

🧵👇

"Mgmt targets topline growth of 20-23% of FY23"

Here are the concall highlights

🧵👇

Business Updates:

• Company has commence the export of R142b and R125.

• Lithium ion battery chemical project is under construction and as per schedule.

• Prices are expected to be impacted as additional domestic capacity is coming up

• Loss of business was 28cr for shutdown

• Company has commence the export of R142b and R125.

• Lithium ion battery chemical project is under construction and as per schedule.

• Prices are expected to be impacted as additional domestic capacity is coming up

• Loss of business was 28cr for shutdown

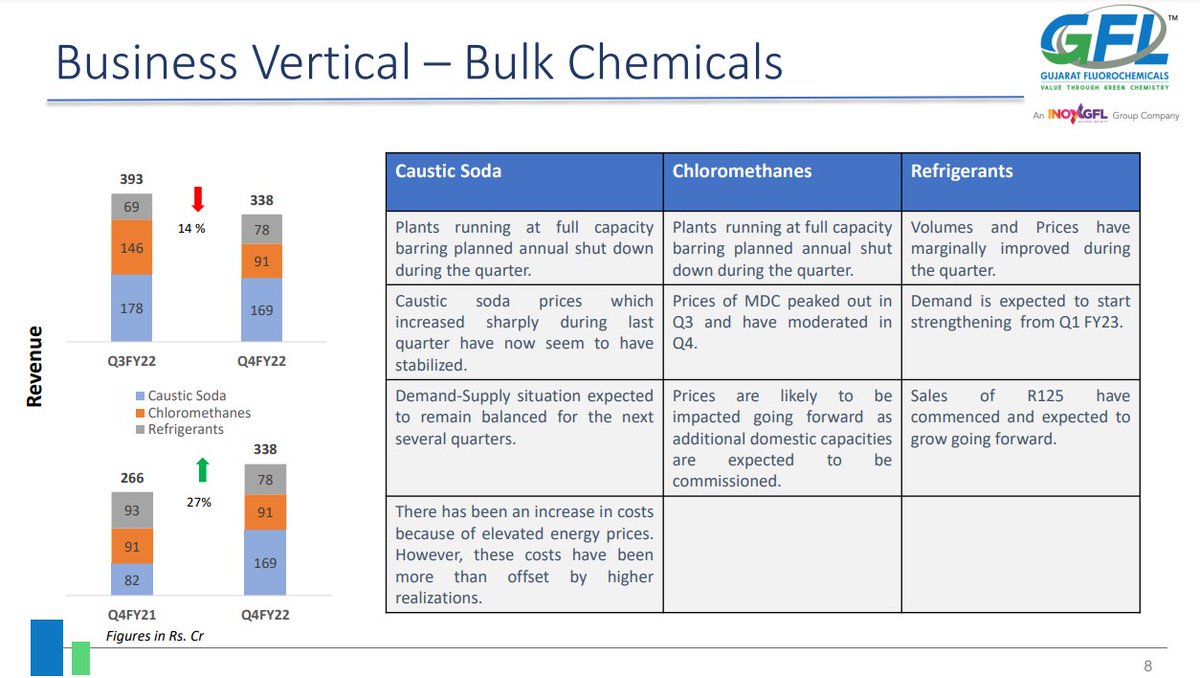

Bulk Chemicals:

(Revenue Mix in Image)

• Caustic soda plant is running at full capacity (except for shut down).

• Price of caustic soda has been stabilized (Rose due to energy price)

• Prices of MDC peaked out in Q3 and have moderated in Q4, resulted decline in Chloromethanes

(Revenue Mix in Image)

• Caustic soda plant is running at full capacity (except for shut down).

• Price of caustic soda has been stabilized (Rose due to energy price)

• Prices of MDC peaked out in Q3 and have moderated in Q4, resulted decline in Chloromethanes

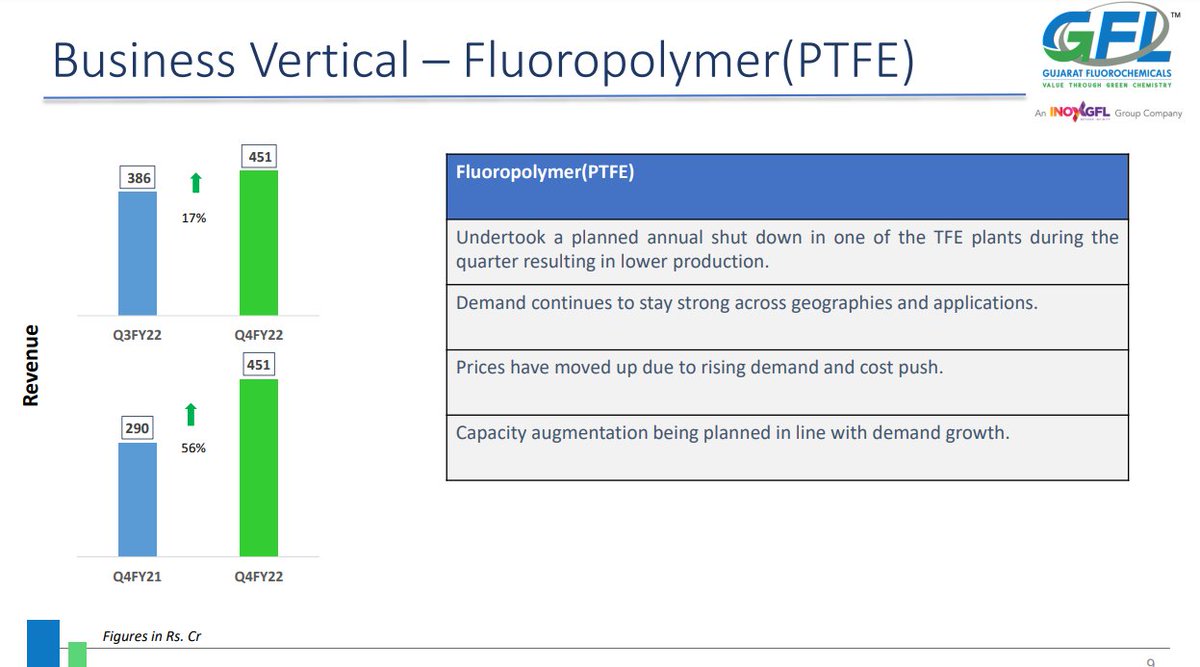

Fluoropolymer:

• Growth came from both rising demand, leading to increase in price of volume both.

• Demand continues to stay strong across geographies and applications.

• De-bottlenecking will take couple of months (with add on of 200-300 PTFE to be available from Q4)

• Growth came from both rising demand, leading to increase in price of volume both.

• Demand continues to stay strong across geographies and applications.

• De-bottlenecking will take couple of months (with add on of 200-300 PTFE to be available from Q4)

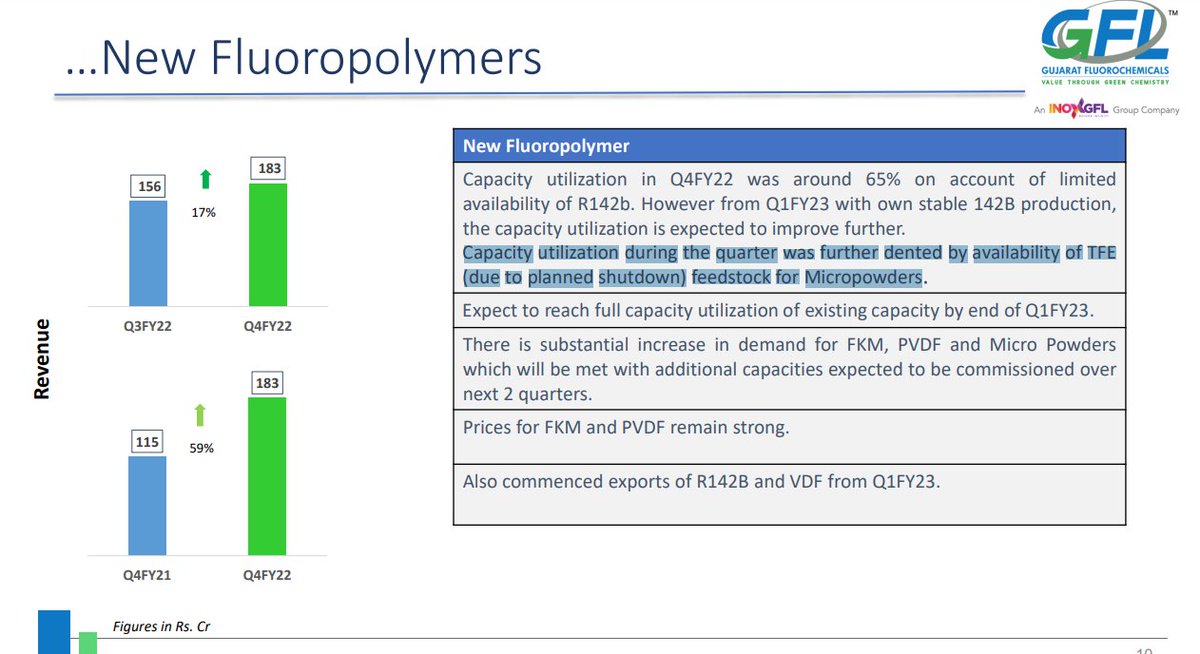

New Fluroropolymer:

(Revenue growth in image)

• Capacity utilization during the quarter was further dented by availability of TFE (due to planned shutdown) feedstock for Micropowders.

• Expect to reach full capacity utilization of existing capacity by end of Q1FY23.

(Revenue growth in image)

• Capacity utilization during the quarter was further dented by availability of TFE (due to planned shutdown) feedstock for Micropowders.

• Expect to reach full capacity utilization of existing capacity by end of Q1FY23.

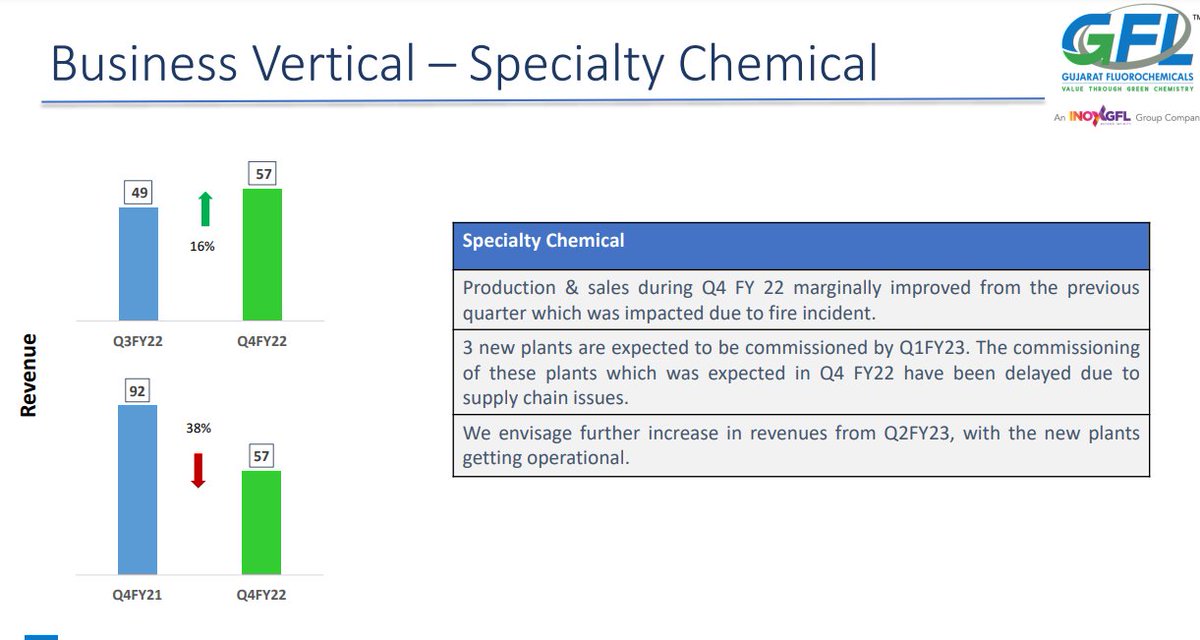

Specialty Chemical:

(Revenue mentioned in image)

• Revenue was hampered due to fire incident is down by 38% YoY.

• Production & sales during Q4 FY 22 marginally improved

• 3 new plants are expected to be commissioned by Q1FY23. It was delayed due to supply chain issue.

(Revenue mentioned in image)

• Revenue was hampered due to fire incident is down by 38% YoY.

• Production & sales during Q4 FY 22 marginally improved

• 3 new plants are expected to be commissioned by Q1FY23. It was delayed due to supply chain issue.

Product Mix:

• Mgmt expect to export R125 of 4K-5K Tons in Fy23.

• PVDF export will depend on internal consumption. As few capex is pre-poned PVDF internal consumption will increase.

• Mgmt expect R142b export of 500Tone next year.

• New products in R&D stage for refrigerant

• Mgmt expect to export R125 of 4K-5K Tons in Fy23.

• PVDF export will depend on internal consumption. As few capex is pre-poned PVDF internal consumption will increase.

• Mgmt expect R142b export of 500Tone next year.

• New products in R&D stage for refrigerant

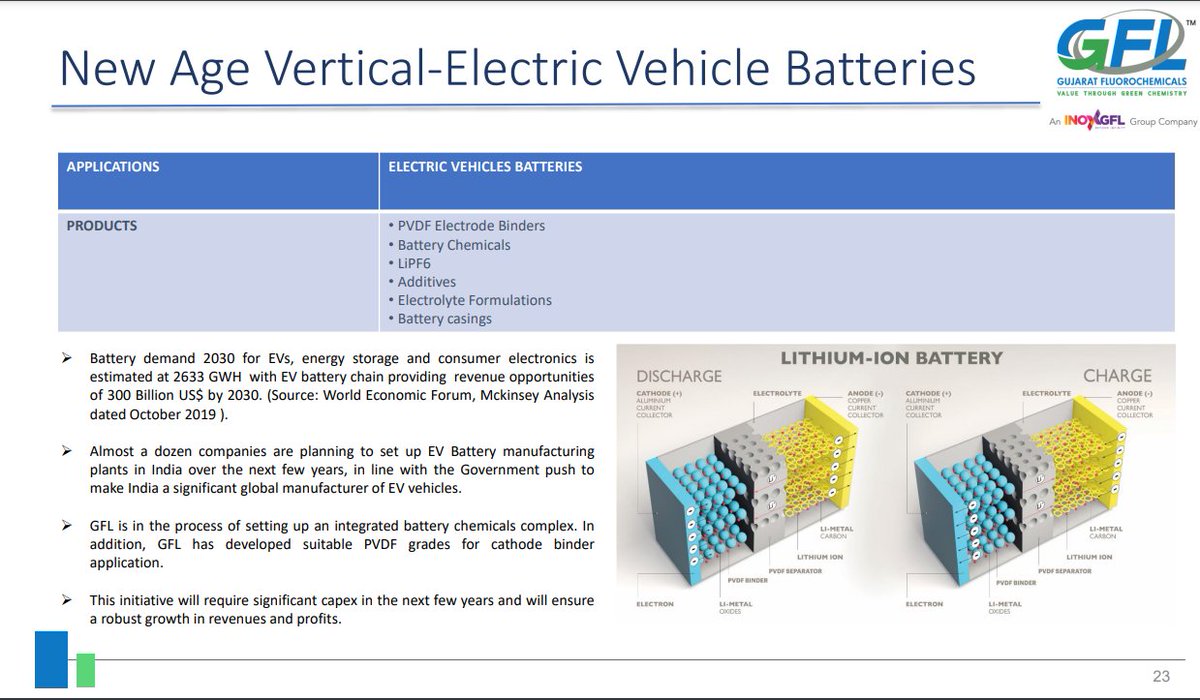

New Age Verticals:

• For batter chemicals, plant for LiPF6 is under construction and should be ready by end of year.

• PVDF product is already available and sampling is in progress and will be for commercial sale in 2 quarters.

• PVDF will commission next year.

• For batter chemicals, plant for LiPF6 is under construction and should be ready by end of year.

• PVDF product is already available and sampling is in progress and will be for commercial sale in 2 quarters.

• PVDF will commission next year.

Battery Chemicals:

• Mgmt is looking for long term contract.

• Plant will commission by end of year and it will take 2 quarters to stabilize the plant.

Customer Application:

- PVDF to Battery manufacturer

- Battery chemical: Company manufacturing of electrolyte in US & Europe

• Mgmt is looking for long term contract.

• Plant will commission by end of year and it will take 2 quarters to stabilize the plant.

Customer Application:

- PVDF to Battery manufacturer

- Battery chemical: Company manufacturing of electrolyte in US & Europe

Capacity:

• Price hike PTFE has been accepted by the customer (In double digit)

• Anti-dumping duties for R125 has also been announced on China

• PTFE capacity is 1550 tons per month

• New Fluoropolymers capacity is 700 tons per month which is extended to 1100 tons per month

• Price hike PTFE has been accepted by the customer (In double digit)

• Anti-dumping duties for R125 has also been announced on China

• PTFE capacity is 1550 tons per month

• New Fluoropolymers capacity is 700 tons per month which is extended to 1100 tons per month

Operational Highlights:

• Gross Flow for specialty intermediates would be 600crs post expansion.

• CAPEX of 300cr for Wind power is for GFL.

• Most of the corporate guarantees will be revoked by the end of the year.

• FKM business potential is 100Mil $.

• Gross Flow for specialty intermediates would be 600crs post expansion.

• CAPEX of 300cr for Wind power is for GFL.

• Most of the corporate guarantees will be revoked by the end of the year.

• FKM business potential is 100Mil $.

Realization:

• PFA: 35$

• FEP: 25$ but it is small compenent for company.

• LiPF: Spot at 70%$ & contract at 50$. But these are subject to change. 30$ would be reasonable price to assume.

• PFA: 35$

• FEP: 25$ but it is small compenent for company.

• LiPF: Spot at 70%$ & contract at 50$. But these are subject to change. 30$ would be reasonable price to assume.

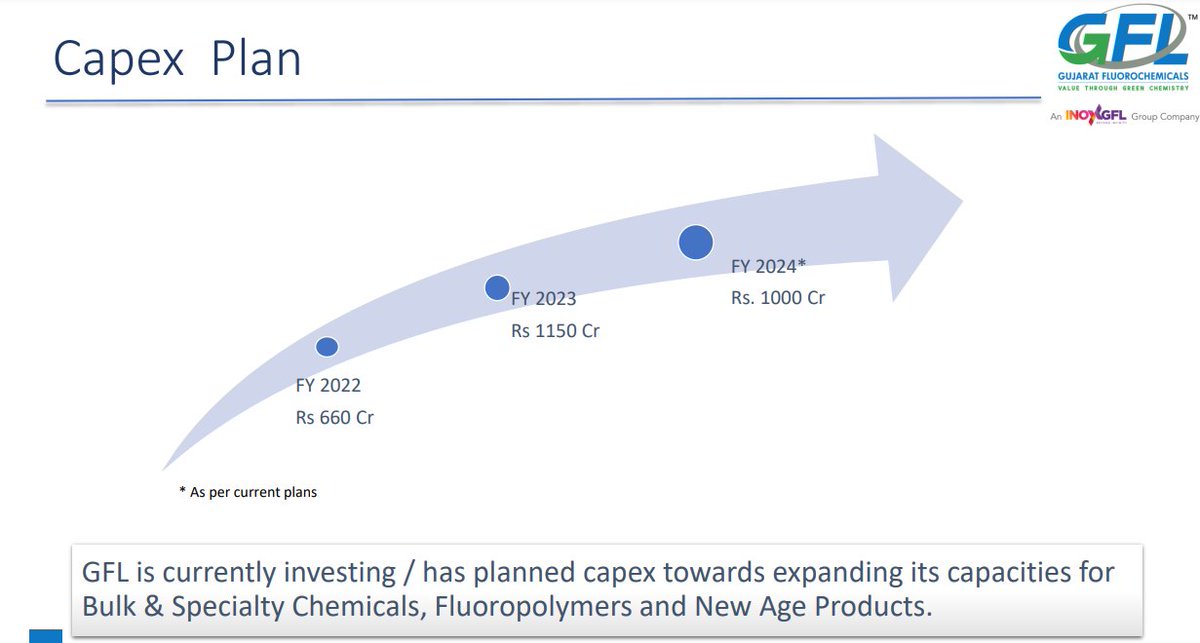

CAPEX:

• CAPEX plan increased from 900cr to 1150cr for FY23.

Breakup:

- Specialty Chemical (Lithium Complex): 300cr

- New Fluoropolymer: 300cr

- Backward integration into PVDF & refirgerants: 250cr. - Balance on wind power and de-bottlenecking (PTFE: increase in 20% capacity).

• CAPEX plan increased from 900cr to 1150cr for FY23.

Breakup:

- Specialty Chemical (Lithium Complex): 300cr

- New Fluoropolymer: 300cr

- Backward integration into PVDF & refirgerants: 250cr. - Balance on wind power and de-bottlenecking (PTFE: increase in 20% capacity).

Other:

• Company is almost debt free, with Net D/E to 0.33. Company intends to be debt free in coming year.

• Working Capital improved to 120 days from 168 days.

• Around 7cr was impacted to fire incident.

• CAPEX budget is on basis of current raw material price.

• Company is almost debt free, with Net D/E to 0.33. Company intends to be debt free in coming year.

• Working Capital improved to 120 days from 168 days.

• Around 7cr was impacted to fire incident.

• CAPEX budget is on basis of current raw material price.

Loading suggestions...