Seshasayee Paper & Board Ltd: Detail Analysis

With respect to our previous detailed article on Satia Industry, we kept the second part set aside for the position of other industry players in Paper Industry.

Thread 🧵👇

With respect to our previous detailed article on Satia Industry, we kept the second part set aside for the position of other industry players in Paper Industry.

Thread 🧵👇

About Company (SPBL):

👉 Seshasayee Paper was founded in 1960 by Mr S. Vishwanathan.

👉 Company is engaged in the business of manufacturing Printing & Writing Paper and Paper board.

👉 Seshasayee is the flagship company of ESVIN Group, located in Chennai.

👉 Seshasayee Paper was founded in 1960 by Mr S. Vishwanathan.

👉 Company is engaged in the business of manufacturing Printing & Writing Paper and Paper board.

👉 Seshasayee is the flagship company of ESVIN Group, located in Chennai.

Business Products:

SPBL manufactures variety of papers such as Book Printing, Grade Paper, Color Paper, Cream Woven Paper, Super White, Chromo Paper, Maplitho Paper, Bristol Paper, Kraft Paper, Copier Paper under the brand names of Color Sprint, SPrint Plus, Success, Index etc

SPBL manufactures variety of papers such as Book Printing, Grade Paper, Color Paper, Cream Woven Paper, Super White, Chromo Paper, Maplitho Paper, Bristol Paper, Kraft Paper, Copier Paper under the brand names of Color Sprint, SPrint Plus, Success, Index etc

Production Capacity:

SPBL has 2 manufacturing units in Tamil Nadu:

1. Erode:

👉Plant capacity: 1,32,000 TPA.

👉Integrated pulp plant capacity: 1,45,000 TPA at Erode.

Over the period of time, the capacity of the plant has increased from 20,000TPA to 1,32,000 now.

SPBL has 2 manufacturing units in Tamil Nadu:

1. Erode:

👉Plant capacity: 1,32,000 TPA.

👉Integrated pulp plant capacity: 1,45,000 TPA at Erode.

Over the period of time, the capacity of the plant has increased from 20,000TPA to 1,32,000 now.

2. Tirunelveli:

👉Production Capacity: 78,000 TPA.

In March 2011, SPBL acquired Subburaj Papers Ltd, with capacity of 60,000 TPA. It was then converted into a virgin pulp paper mill.

Water: SPBL sources water from River Cauvery. There is political / legal issue in recent times

👉Production Capacity: 78,000 TPA.

In March 2011, SPBL acquired Subburaj Papers Ltd, with capacity of 60,000 TPA. It was then converted into a virgin pulp paper mill.

Water: SPBL sources water from River Cauvery. There is political / legal issue in recent times

Plantation:

SPBL has planting of nearly 16 crores of Casuarina and Eucalyptus seedlings in about 20,000 acres in Tamil Nadu.

This helps sourcing raw materials for the company. Also, this even helps reducing the pulp demand of the company as no imports are required.

SPBL has planting of nearly 16 crores of Casuarina and Eucalyptus seedlings in about 20,000 acres in Tamil Nadu.

This helps sourcing raw materials for the company. Also, this even helps reducing the pulp demand of the company as no imports are required.

Power Plant: SPBL has 20MW Captive Power Plant at Erode for internal consumption. Company imports coal for its captive power plant.

Chemical Recovery: ~50% of the energy consumed is green power generated from ‘Black Liquor’. 96% of the chemicals is recovered back & is re-cycled.

Chemical Recovery: ~50% of the energy consumed is green power generated from ‘Black Liquor’. 96% of the chemicals is recovered back & is re-cycled.

Subsidiary

SPBL has 2 subsidiary:

🎯 Ponni Sugar: SPBL holds 27.45% market share. It is in business of sugar manufacturing. Current Market Cap of Ponni Sugar is 215 cr.

🎯 Esvi International: Wholly owned subsidiary that holds properties and derives property income.

SPBL has 2 subsidiary:

🎯 Ponni Sugar: SPBL holds 27.45% market share. It is in business of sugar manufacturing. Current Market Cap of Ponni Sugar is 215 cr.

🎯 Esvi International: Wholly owned subsidiary that holds properties and derives property income.

Expansion:

SPBL till now has carried 3 Mill Development Plan (MDP).

MDP III (Ongoing CAPEX):

Project was started in July 2019 with budget of 315 cr

🚀 Upgradation of Erode to 1,65,000 MPTA

🚀Upgradation of RDH Pulp Mill to 1,54,000 TPA

🚀Augmenting Waste Water Treatment Plant

SPBL till now has carried 3 Mill Development Plan (MDP).

MDP III (Ongoing CAPEX):

Project was started in July 2019 with budget of 315 cr

🚀 Upgradation of Erode to 1,65,000 MPTA

🚀Upgradation of RDH Pulp Mill to 1,54,000 TPA

🚀Augmenting Waste Water Treatment Plant

Distribution Reach:

SPBL has a network of 50+ dealers & 1 depot in Bengaluru.

Co. caters to 30 countries in region like US, Africa, Sri Lanka, Nepal, & Europe.

Around 65-70% of the sales in domestic market comes from South Region.

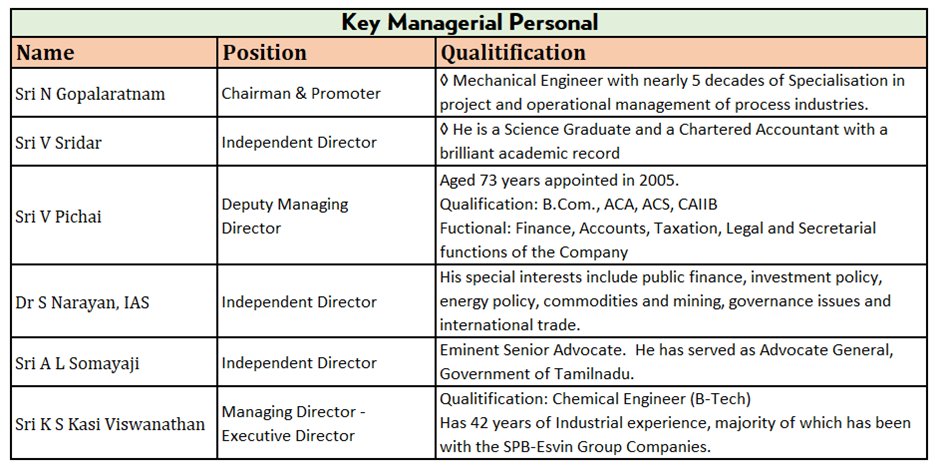

Key Managerial Person

SPBL has a network of 50+ dealers & 1 depot in Bengaluru.

Co. caters to 30 countries in region like US, Africa, Sri Lanka, Nepal, & Europe.

Around 65-70% of the sales in domestic market comes from South Region.

Key Managerial Person

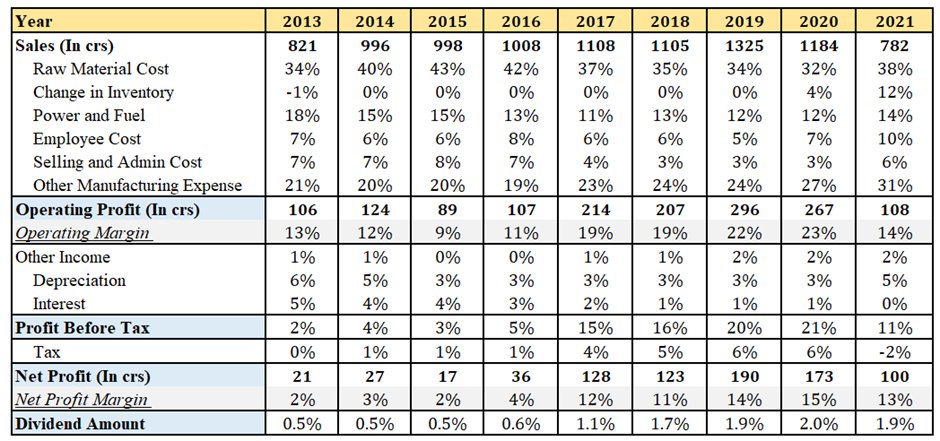

Financial:

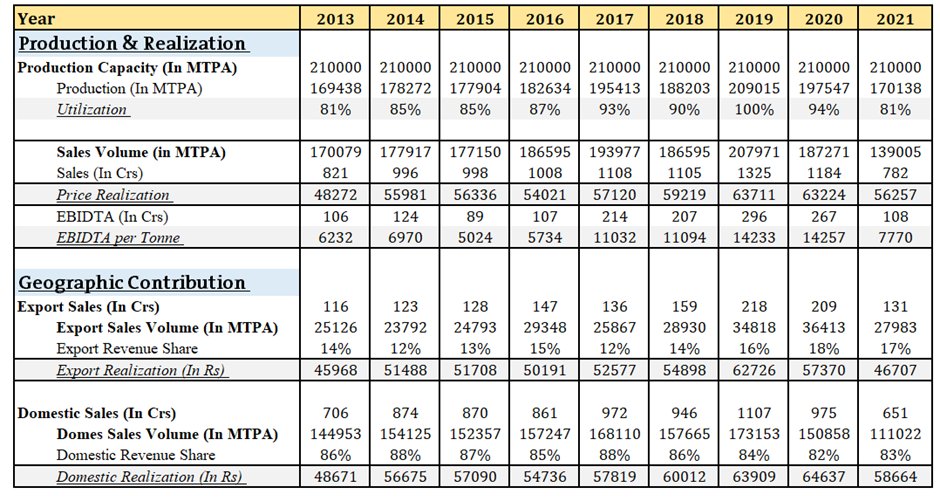

Realization per ton:

SPBL is currently working at almost optimum utilization.

Export revenue share as a percentage of total revenue stand at 18%. Export realization seems lower than that, but this is due to deemed export or the trading export.

Realization per ton:

SPBL is currently working at almost optimum utilization.

Export revenue share as a percentage of total revenue stand at 18%. Export realization seems lower than that, but this is due to deemed export or the trading export.

Over the last decade, there has been no significant capacity expansion, resulted in less than 10% growth in the topline.

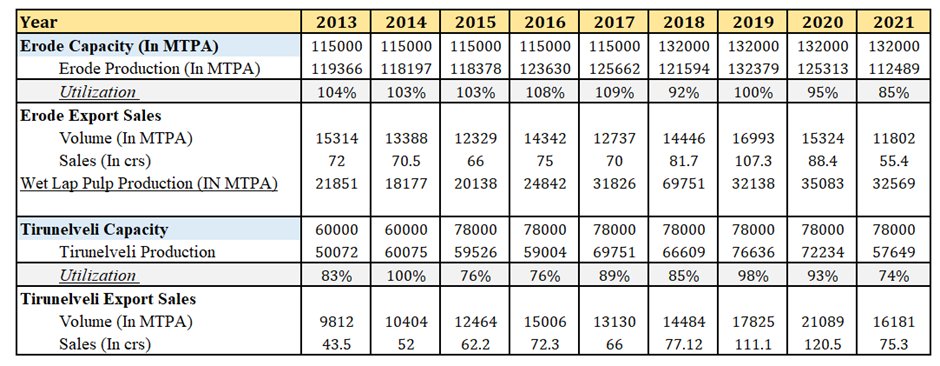

Plant wise capacity & utilization of SPBL.

Sales growth is less than 6% (in a decade)which is because of no increase in significant capacity expansion

Plant wise capacity & utilization of SPBL.

Sales growth is less than 6% (in a decade)which is because of no increase in significant capacity expansion

P&L:

- Usage of integrated pulp

- Purchase of bagasse (from sister co. Ponni Sugars)

- Sourcing waste paper helped decreasing their raw material cost.

This has saved a lot of money for the company, while there has been some hindrance in other expense (water expense overhead)

- Usage of integrated pulp

- Purchase of bagasse (from sister co. Ponni Sugars)

- Sourcing waste paper helped decreasing their raw material cost.

This has saved a lot of money for the company, while there has been some hindrance in other expense (water expense overhead)

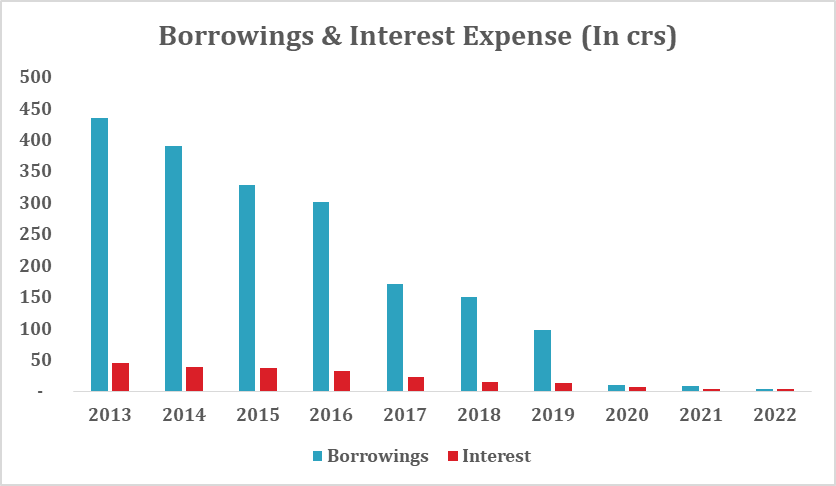

Borrowing:

The company has also spent cash flows on decreasing the borrowing of the company, which resulted in decrease in interest expense and increase in net profit margin by 5% from 2013.

The company has also spent cash flows on decreasing the borrowing of the company, which resulted in decrease in interest expense and increase in net profit margin by 5% from 2013.

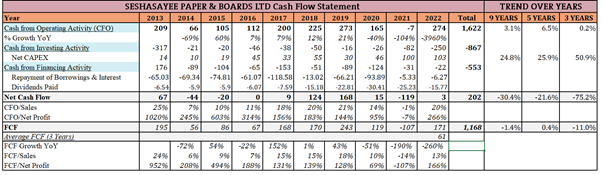

Cash Flow Movement:

SPBL is a net cash positive company except for the last year, where 2021 was impacted majorly due to the Covid (which impacted the industry working capital cycle due to inventory), and increase in expansion taken in 2022.

SPBL is a net cash positive company except for the last year, where 2021 was impacted majorly due to the Covid (which impacted the industry working capital cycle due to inventory), and increase in expansion taken in 2022.

👉Company is free cash flow positive.

👉Last 3 year average FCF: Rs 61 cr, which was impacted due to covid.

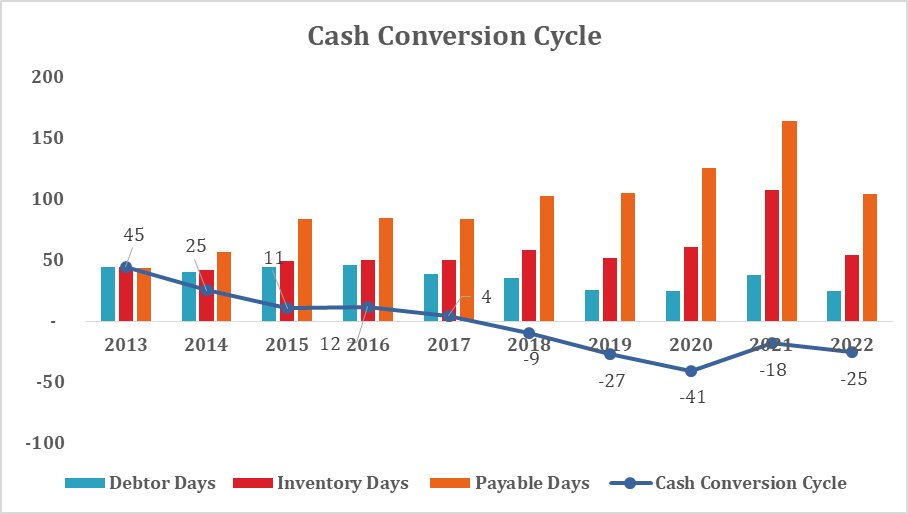

👉Working Capital Cycle is negative, leading to higher CFO than PBT.

👉SPBL has greater edge of managing the payables of the company, while the company has inventory too.

👉Last 3 year average FCF: Rs 61 cr, which was impacted due to covid.

👉Working Capital Cycle is negative, leading to higher CFO than PBT.

👉SPBL has greater edge of managing the payables of the company, while the company has inventory too.

Ratios

ROIC of the company over the period of time is negative, while ROE and ROCE of the company has been improving gradually over the period of time.

ROIC of the company over the period of time is negative, while ROE and ROCE of the company has been improving gradually over the period of time.

Our Key Observation:

1. SPBL topline growth is in line with the industry growth rate, which is very low.

2. Over the last few years, SPBL has focused to increase utilization & operational efficiency. Co. has spent more on the backward integration to increase the profitability

1. SPBL topline growth is in line with the industry growth rate, which is very low.

2. Over the last few years, SPBL has focused to increase utilization & operational efficiency. Co. has spent more on the backward integration to increase the profitability

3. Plant is running at optimum utilization. Hence, there is less volume growth visible until the expansion of Erode plant comes in place.

4.SPBL is a debt free company. Henceforth, if the cycle turns, SPBL will not be bankrupt.

4.SPBL is a debt free company. Henceforth, if the cycle turns, SPBL will not be bankrupt.

5.Looking at the historical valuation of the company, it is currently at more than a fair price valuation.

6.Return ratios over the last few years are negative for the company.

6.Return ratios over the last few years are negative for the company.

Loading suggestions...