The Statement of Cash Flows answers one simple question:

Where is cash going?

Let's dive in:

Where is cash going?

Let's dive in:

In business, there is a hyperfocus on profit, but profits aren't actually CASH in the business.

Let's me introduce Cash versus Accrual Financials:

Cash = recorded when revenue received & expenses paid

Accrual = recorded when revenue earned (or work done) & expenses incurred

Let's me introduce Cash versus Accrual Financials:

Cash = recorded when revenue received & expenses paid

Accrual = recorded when revenue earned (or work done) & expenses incurred

In Accrual Accounting, showing a profit doesn't mean you received cash.

Revenue can be recorded for work done (or product sold), but if they go to Tahiti, you never receive CASH.

Also, growing quickly can create high profits, but the CASH required for inventory could be higher.

Revenue can be recorded for work done (or product sold), but if they go to Tahiti, you never receive CASH.

Also, growing quickly can create high profits, but the CASH required for inventory could be higher.

The Statement of Cash Flows solved these problems.

It answers:

1. Was cash flow positive or negative?

2. Why was it positive or negative?

It answers:

1. Was cash flow positive or negative?

2. Why was it positive or negative?

The formula:

Net Increase/Decrease of cash during period + Cash at beginning of period = Cash at end of period

The net increase/decrease is broken down into 3 categories:

• Operating Activities

• Investing Activities

• Financing Activities

Net Increase/Decrease of cash during period + Cash at beginning of period = Cash at end of period

The net increase/decrease is broken down into 3 categories:

• Operating Activities

• Investing Activities

• Financing Activities

• Operating Activities

Cash that changes hands related to the operations of the business goes in this section.

Net Income +/- non-cash adjustments from Income Statement +/- changes in operating assets and liabilities

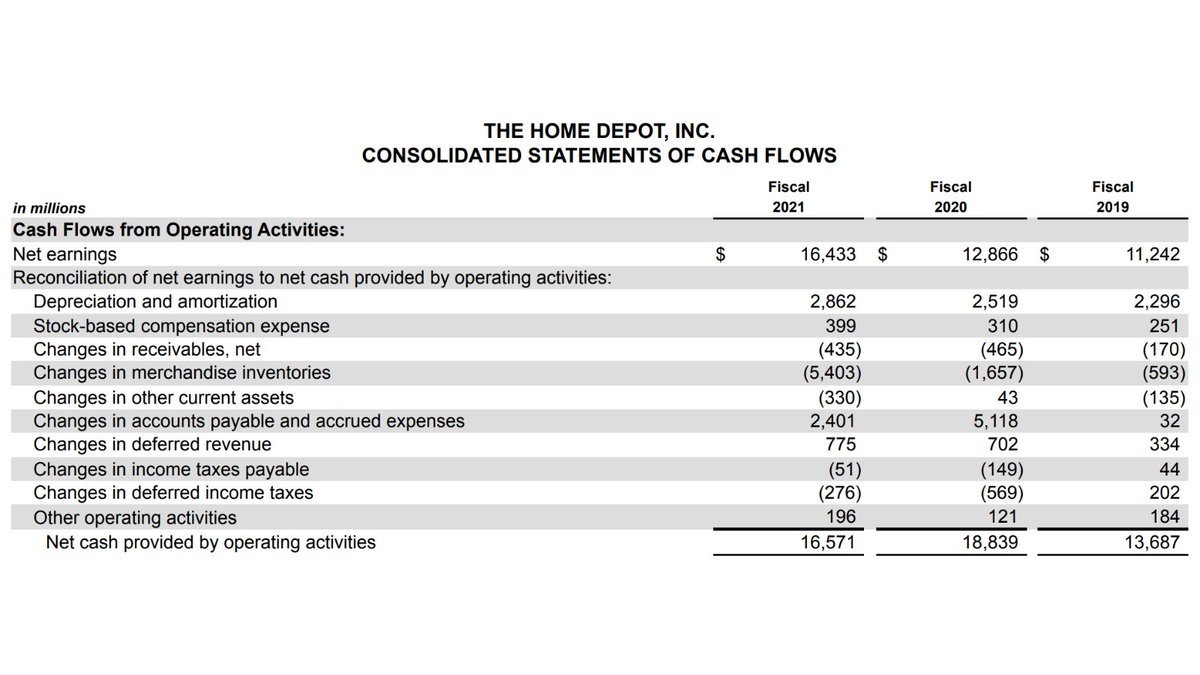

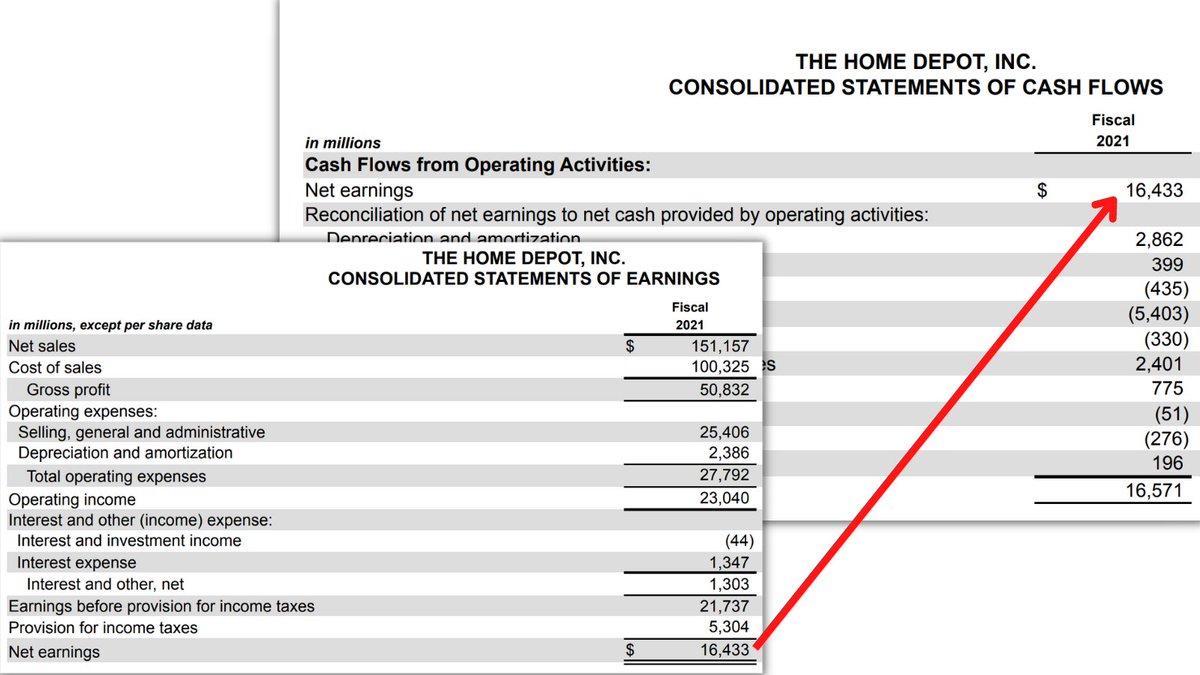

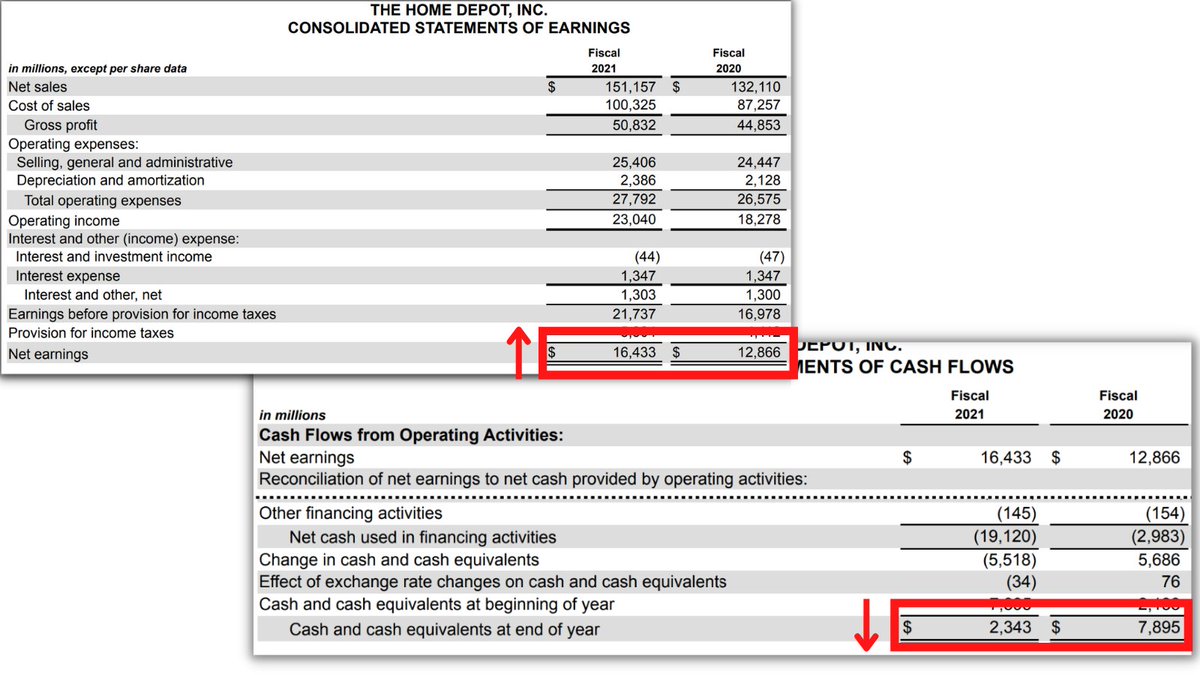

(We’ll be using Home Depot’s financials for this thread)

Cash that changes hands related to the operations of the business goes in this section.

Net Income +/- non-cash adjustments from Income Statement +/- changes in operating assets and liabilities

(We’ll be using Home Depot’s financials for this thread)

Non-cash adjustments from the Income Statement include:

• Depreciation & Amortization

• Any deferred expense

Changes in assets or liabilities include:

• AR & AP

• Inventory

• Deferred Revenue or taxes

• Depreciation & Amortization

• Any deferred expense

Changes in assets or liabilities include:

• AR & AP

• Inventory

• Deferred Revenue or taxes

When looking at the Operating Activities section, the goal is to determine if you're negative or positive cash flow and WHY.

Notice that Profit is ONE line within this section.

There are a lot of factors that determine your cash flow from operations.

Notice that Profit is ONE line within this section.

There are a lot of factors that determine your cash flow from operations.

If cash flow is negative cash flow from operations, you have to make up the difference from:

• Investing Activities

• Financing Activities

• Previous cash balances

• Owner funding the business

• Investing Activities

• Financing Activities

• Previous cash balances

• Owner funding the business

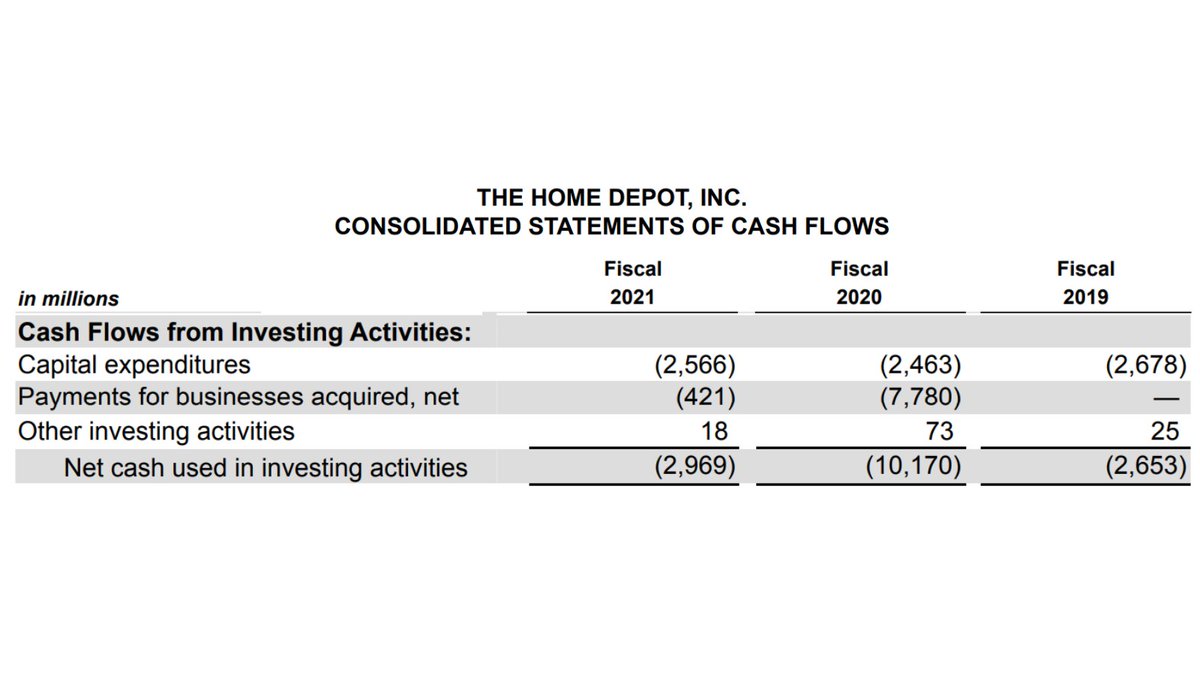

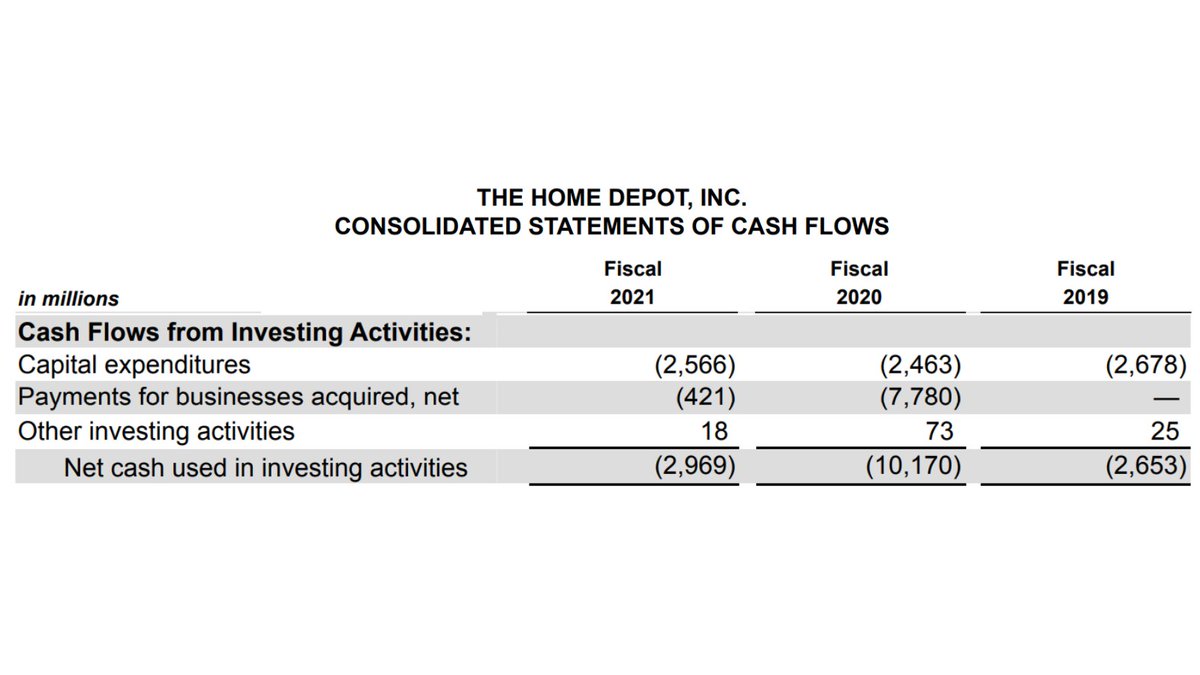

• Investing Activities

This reflects the purchase and sale of assets such as vehicles, equipment, or sale/purchase of a company.

This reflects the purchase and sale of assets such as vehicles, equipment, or sale/purchase of a company.

Negative cash flow from investing could mean you’re:

• buying assets

• buying businesses

• investing via research and development

Positive cash flow from investing could mean:

• selling assets

• getting returns on marketable securities

• buying assets

• buying businesses

• investing via research and development

Positive cash flow from investing could mean:

• selling assets

• getting returns on marketable securities

Negative or positive in investing isn't inherently good or bad. It’s based on the context of the whole statement.

Positive cash flow in investing from selling equipment or securities to cover operating losses is bad.

Positive cash flow in investing from selling equipment or securities to cover operating losses is bad.

Negative cash flow in investing from purchasing equipment because of company growth is good.

As a rule, negative cash from investing activities is GOOD if you’re trading short-term for long-term.

As a rule, negative cash from investing activities is GOOD if you’re trading short-term for long-term.

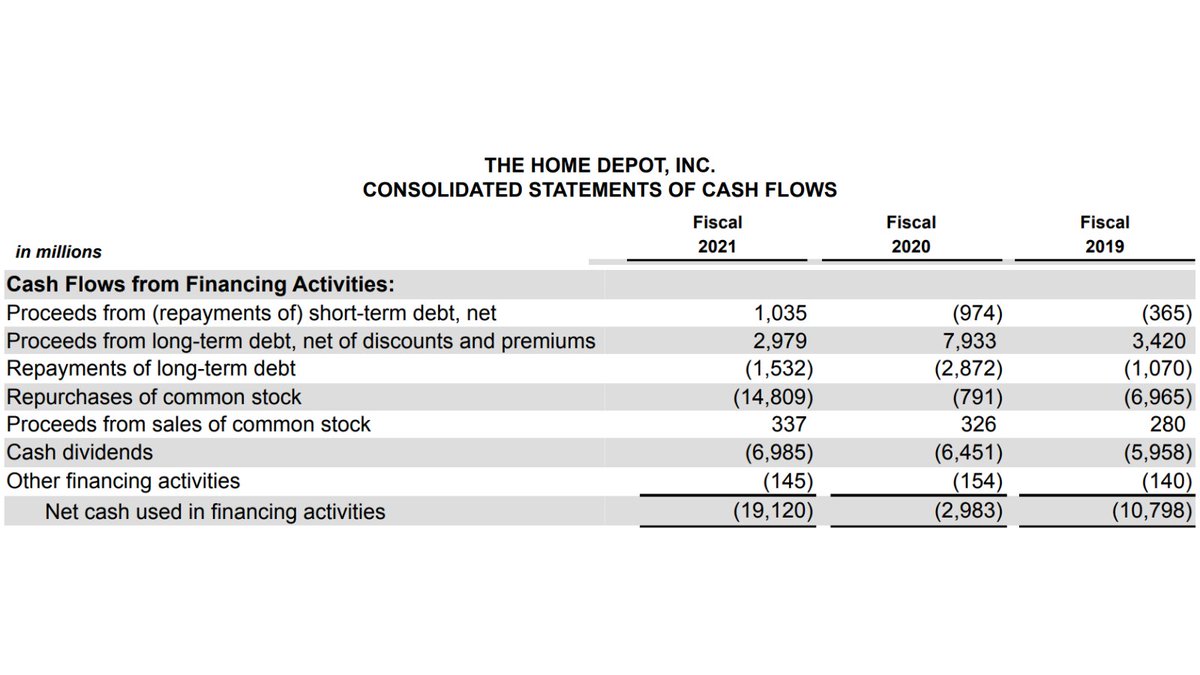

• Financing Activities

This reflects changes in debt and equity.

It can include:

• Stock sale or repurchases

• Issuance or repayment of debt

• Distribution or dividend to owner

This reflects changes in debt and equity.

It can include:

• Stock sale or repurchases

• Issuance or repayment of debt

• Distribution or dividend to owner

Positive cash flow in financing indicates that cash has come into the company (increasing assets).

Negative cash flow in financing indicates the company has paid out capital.

Negative cash flow in financing indicates the company has paid out capital.

Just as with Investing, either can be a good or bad sign depending on context.

If a company is returning money to investors or owners, it is a sign they don’t have a way to deploy it in investments.

If a company is returning money to investors or owners, it is a sign they don’t have a way to deploy it in investments.

If a company has positive cash flow from financing, it could indicate they’re taking on more debt.

If it’s because of growth, good.

If it’s because enough cash isn’t being generated by operations, it could be bad.

If it’s because of growth, good.

If it’s because enough cash isn’t being generated by operations, it could be bad.

The Statement of Cash Flows is one of the more complex and confusing concepts.

To reiterate: cash flow is what matters, not profits.

As you can see from Home Depot, they had higher profits in 2021 but cash went down.

To reiterate: cash flow is what matters, not profits.

As you can see from Home Depot, they had higher profits in 2021 but cash went down.

Why would that be?

Cash flow from Investing went from -$10.2B to -$3.0B (not it)

Cash flow from Financing went from -$3.0B to -$19.1B (found it)

You can see this was from repurchasing stock and dividends.

Good or bad? We’ll let you decide.

Cash flow from Investing went from -$10.2B to -$3.0B (not it)

Cash flow from Financing went from -$3.0B to -$19.1B (found it)

You can see this was from repurchasing stock and dividends.

Good or bad? We’ll let you decide.

If you want to dive deeper, join @IAmClintMurphy and me in our upcoming cohort.

In 3 days we’ll help you:

• make numbers-informed decisions

• communicate your numbers with clarity

Join now: maven.com

In 3 days we’ll help you:

• make numbers-informed decisions

• communicate your numbers with clarity

Join now: maven.com

I hope this was helpful!

Tomorrow I’ll be diving into the Cash versus Accrual Accounting, so follow me so you don’t miss it: @KurtisHanni

If you enjoyed this thread, retweeting the first tweet helps support me and spread the knowledge:

Tomorrow I’ll be diving into the Cash versus Accrual Accounting, so follow me so you don’t miss it: @KurtisHanni

If you enjoyed this thread, retweeting the first tweet helps support me and spread the knowledge:

Loading suggestions...