1/ After $CPRT's highly impressive Q3 results yesterday, where vehicle sales jumped +58% and EBIT +14% y/y despite tough comps, we thought it would be a good time to break this business down. Let's go!

2/ $CPRT was founded back in the early 80s by Willis Johnson, who's still the second largest shareholder and Chairman, after 10+ years in the salvage industry. It was operated like a family business for roughly a decade and then went public in the early 90s.

3/ Who knew selling dinged up cars online would be a gold mine?

As this illustration shows you, for every car accident the car owner's insurance company has to take some kind of action, and basically if the expense of fixing the car is too high they auction it away on Copart.

As this illustration shows you, for every car accident the car owner's insurance company has to take some kind of action, and basically if the expense of fixing the car is too high they auction it away on Copart.

4/ In the early days Copart tried the $IAA model (their largest peer), to buy totalled cars from insurance companies and then auction them out themselves, but soon realized that this wasn't the way to go. They instead became a one-stop-shop middleman.

5/ The switch from owning the cars themselves to instead go for a marketplace model, now with global scale because of the internet, gave both Copart and the insurance companies better unit economics. Win-win. That of course created a huge supply, which in turn increased demand.

6/ And for a marketplace business like this to work, and be competitively advantaged, you need to have both the largest supply and the largest demand. That is a tough position to reach, and exactly why it's such a powerful business once a dominant market position is established.

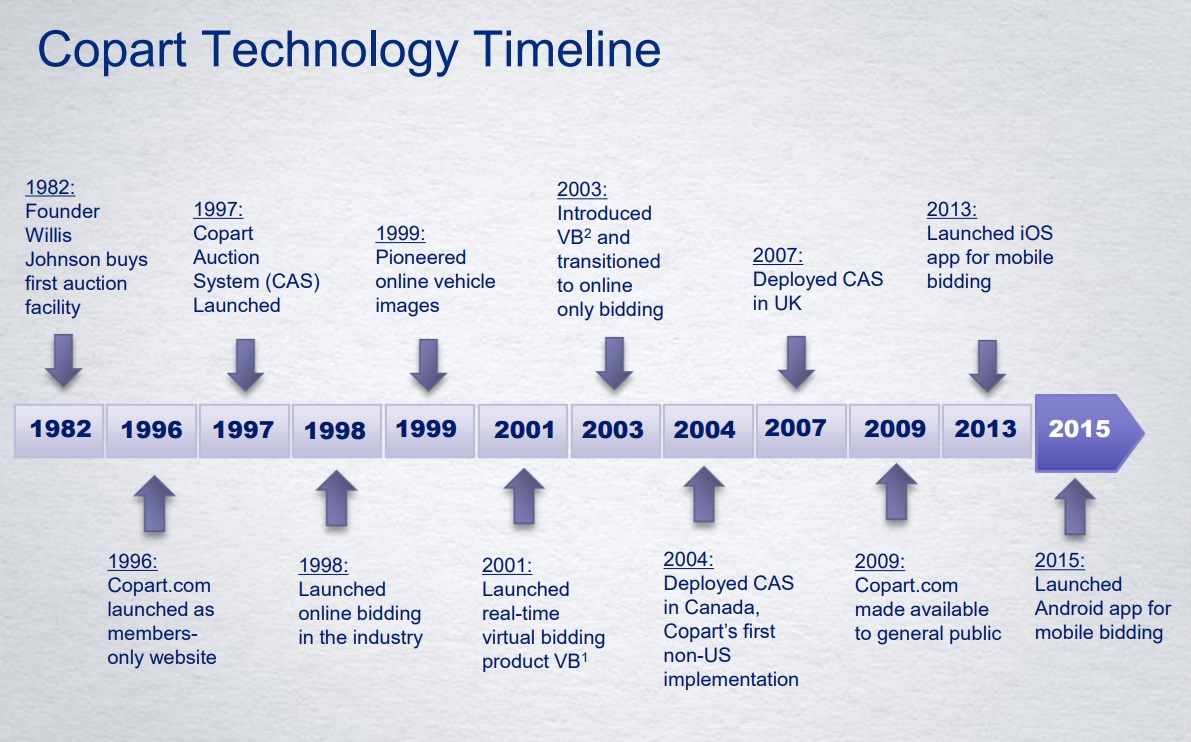

7/ $CPRT is the largest marketplace of its kind globally today, and the second largest player in the space is $IAA. One of the key reasons why Copart quickly gained share initially was early internet/tech adoption. They were for example the first car auction site with images.

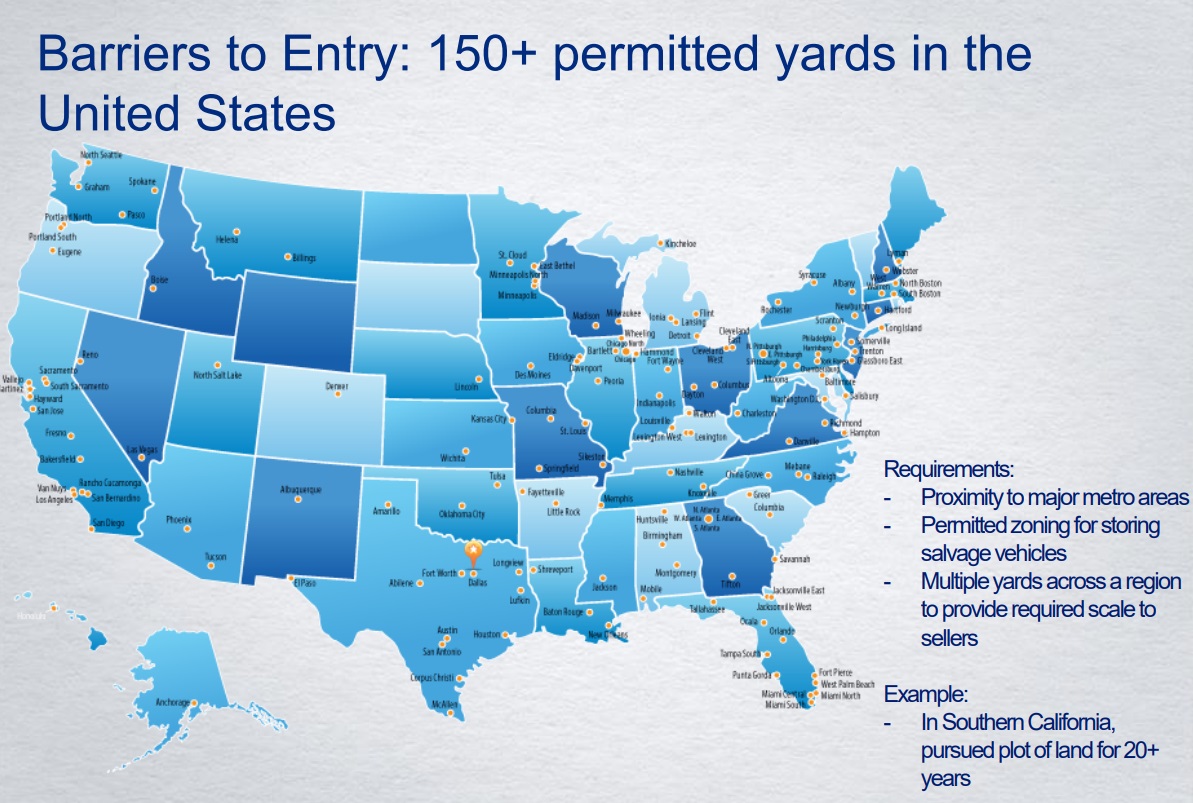

8/ Another key reason obviously is their *huge* investments in physical infrastructure. Copart doesn't just offer a digital marketplace, they offer to take care of everything surrounding the transaction (except transport in some markets, depending on where in the world you live).

9/ Like for $AMZN with their logistics infrastructure, the physical part of $CPRT's business strengthens their digital marketplace. Copart has 200+ massive salvage yards around the world, and handle +175K auctions daily with buyers in 190+ countries.

10/ The complexity and capital intensity of making this physical/digital network work seamlessly together is a huge barrier to entry for competitors. How much $ and time would you need to destroy $CPRT's moat?

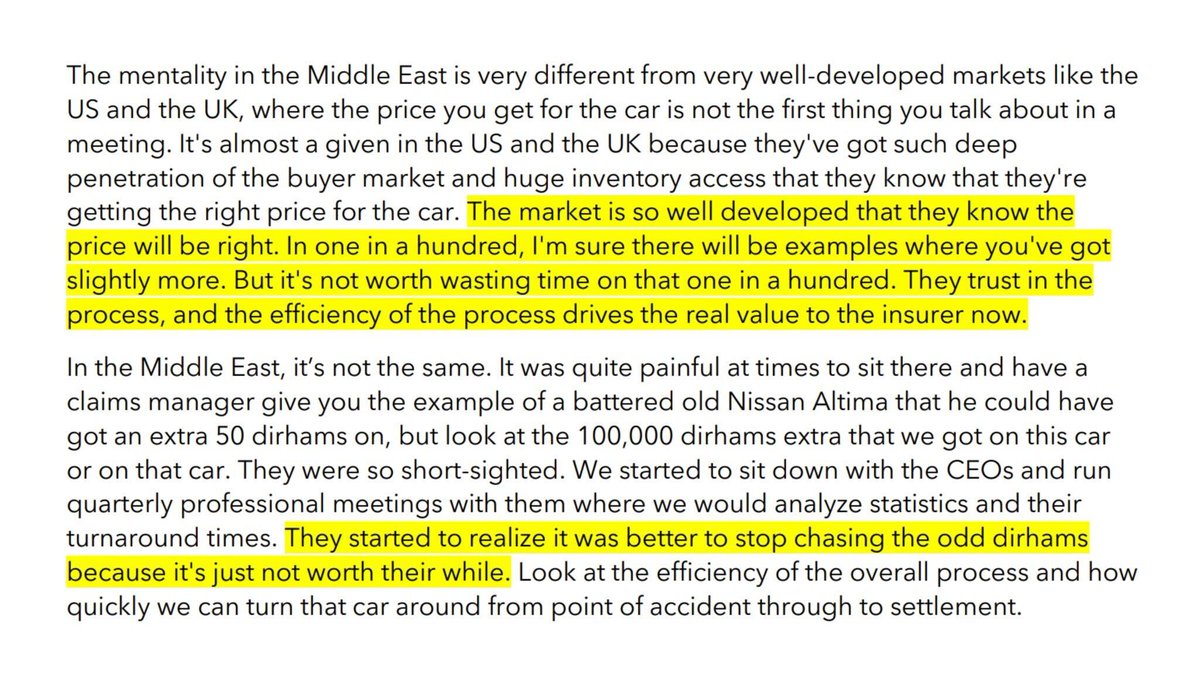

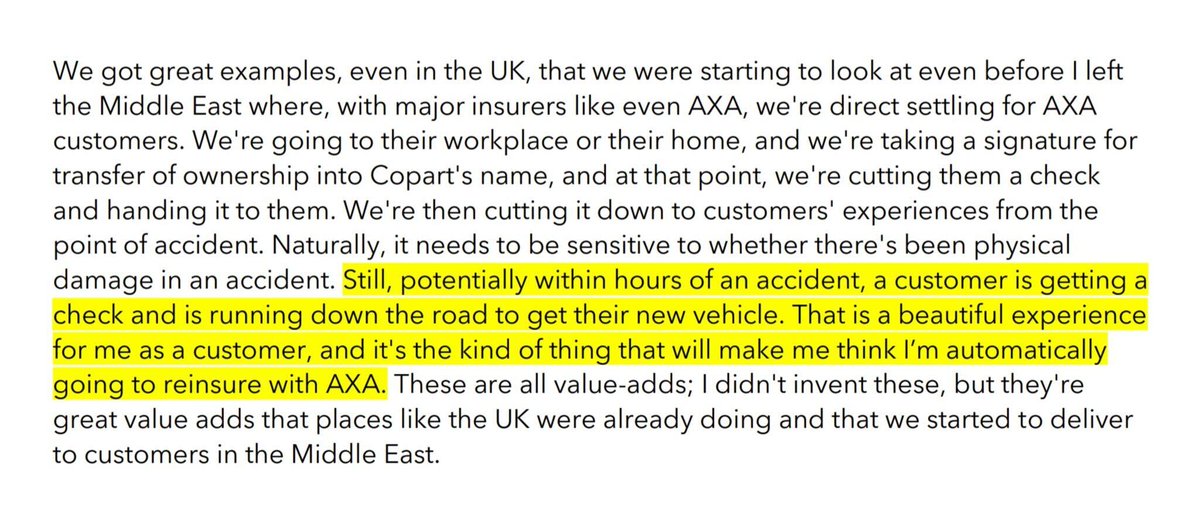

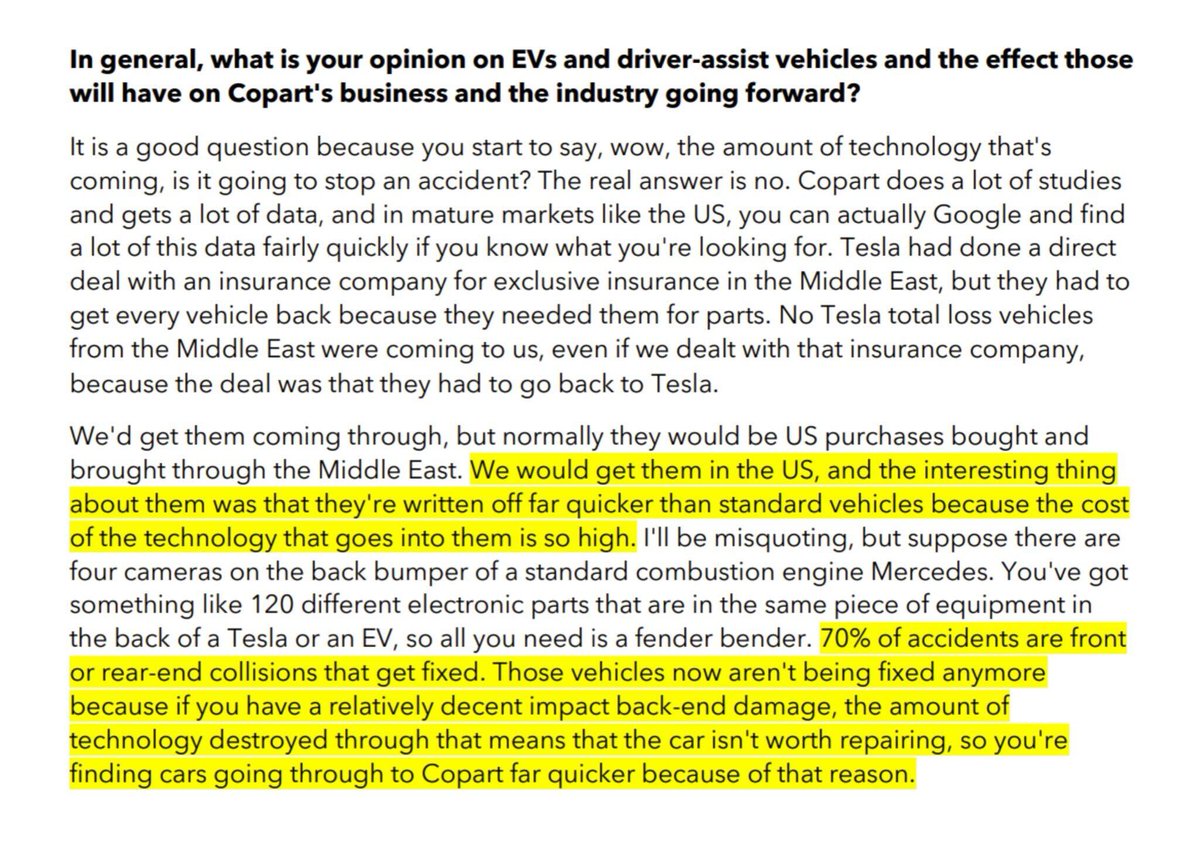

From an @_inpractise interview w/ CPRT's former CEO of Middle East:

From an @_inpractise interview w/ CPRT's former CEO of Middle East:

11/ Much like $COST, Copart started out in the US (and still have the majority of their sales domestically >80%, although this includes exports) but are now leveraging their volume/cost advantage by taking on the world. To date, they have 8500+ acres of land in 11 countries.

12/ And contrary to some people's belief, electric vehicles (well, new cars in general really) seem to be a tailwind rather than a headwind for $CPRT. The more technology that gets put into the cars, the more expensive they are to fix.

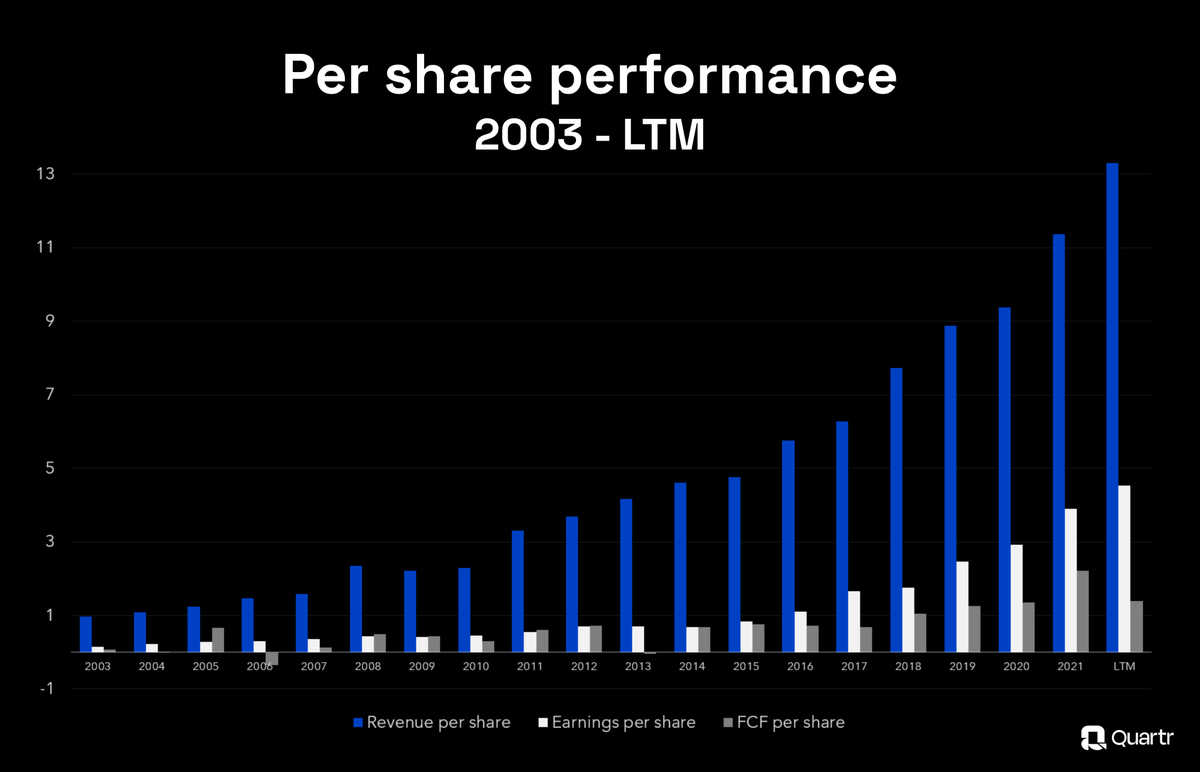

13/ $CPRT's conservative yet long-term oriented capital allocation has led to a fantastic per share performance, with revenues growing 14x and earnings 30x over the last 20 years. The number of shares has decreased ~40% during the period because of repurchases.

Loading suggestions...