The basics of income statement explained from scratch 🧮➕

In this thread we will talk about:-

1.What is a Profit & Loss Statement

2.Accrual principle of accounting

3.Profit & Loss line items

Let's dive in 🧵🧵🧵🧵🧵🧵🧵

Retweet for educating max investors!!

In this thread we will talk about:-

1.What is a Profit & Loss Statement

2.Accrual principle of accounting

3.Profit & Loss line items

Let's dive in 🧵🧵🧵🧵🧵🧵🧵

Retweet for educating max investors!!

What is a Profit & Loss Statement?

Statement of Profit & Loss is one of the most important part of financial statements which shows a company's revenue, expenses and the amount of Profit earned or Loss incurred by the company. It is also known as Income Statement.

Statement of Profit & Loss is one of the most important part of financial statements which shows a company's revenue, expenses and the amount of Profit earned or Loss incurred by the company. It is also known as Income Statement.

Normally P&L statements are prepared quarterly or annually. Quarterly means a period of 3 months of a financial year.

Annually means for the whole financial year i.e, April to March.

These are the 4 Quarters in a year🔽🔽

Annually means for the whole financial year i.e, April to March.

These are the 4 Quarters in a year🔽🔽

P&L Statement is prepared on the basis of accrual principle of accounting. Accrual principle means recording revenues and expenses as and when it is incurred. It doesn’t matter whether cash is received or not.

Let's look at an example👇

Let's look at an example👇

For example, You have an electronics shop and one of your friend came to purchase a TV. You sold it to him and asked him to pay after installation so here you haven't received the cash but you will record the sales in your P&L as and when TV is out for delivery.

The P&L Statement normally consist of following line items

1⃣Revenue:

Revenue from Operations

Other Income

2⃣Expenses:

Cost of goods sold

Employee Benefit Expenses

Finance Cost

Depreciation

Other expenses

3⃣Exceptional Items

4⃣Profit Before Tax

5⃣Tax Expense

6⃣PAT

1⃣Revenue:

Revenue from Operations

Other Income

2⃣Expenses:

Cost of goods sold

Employee Benefit Expenses

Finance Cost

Depreciation

Other expenses

3⃣Exceptional Items

4⃣Profit Before Tax

5⃣Tax Expense

6⃣PAT

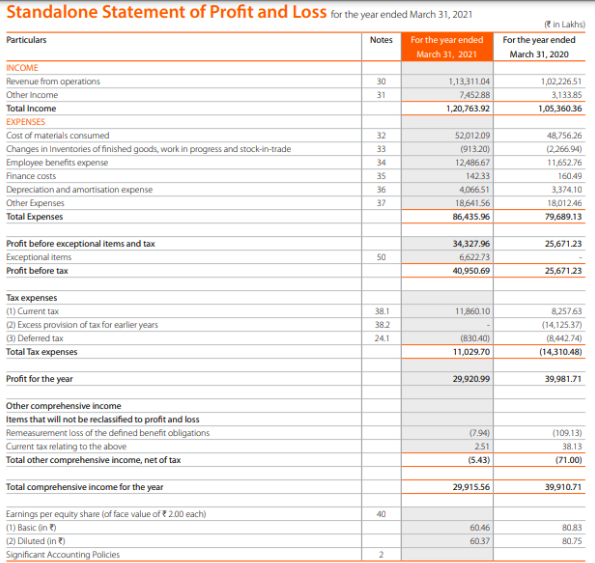

This is how the Profit and Loss statement looks like 👇

Now let’s dig into each and every line item of P&L Statement:

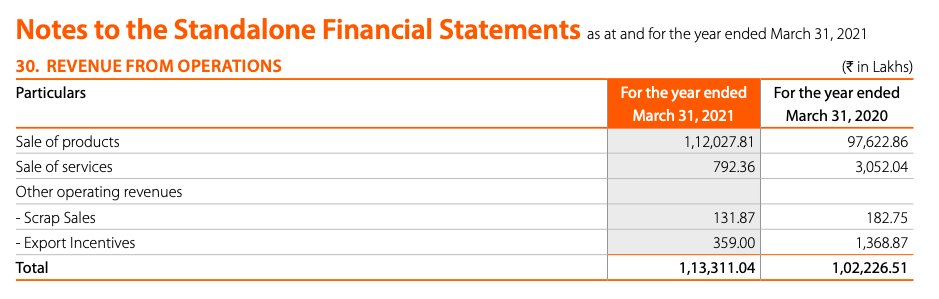

Revenue: The P&L Statement starts with Revenue from Operations, it is the total amount of sales done by the company. It is also termed as the top line of the company.

Revenue: The P&L Statement starts with Revenue from Operations, it is the total amount of sales done by the company. It is also termed as the top line of the company.

Revenue consists of 2 parts i.e revenue from core operating activities which is my normal business activity and other is revenue from other operating activities which may include scrap sales, export incentives.

Here we need to track the growth in revenue in CY as compared to PY

Here we need to track the growth in revenue in CY as compared to PY

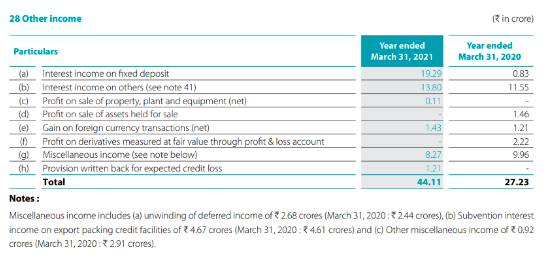

Other Income:

The next part in revenue will be Other Income, it means income from activities other than business activities like interest or dividend income on investments, profit or loss on sale of investments, foreign exchange gain or loss, insurance claims received.

The next part in revenue will be Other Income, it means income from activities other than business activities like interest or dividend income on investments, profit or loss on sale of investments, foreign exchange gain or loss, insurance claims received.

So these were the 2 line items for Incomes, now lets come to the expenses.

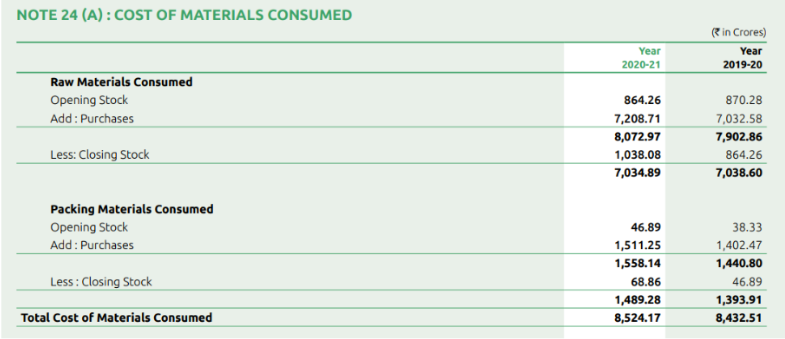

The first line item in expenses is Cost of material consumed, it is the raw material cost that the company requires to manufacture finished goods. It is calculated as opening stock + Purchases - Closing stock

Closing stock of previous year will always be the opening stock of CY

Closing stock of previous year will always be the opening stock of CY

Purchases of Stock in trade: It refers to all the purchases of finished goods that the company buys towards conducting its business.

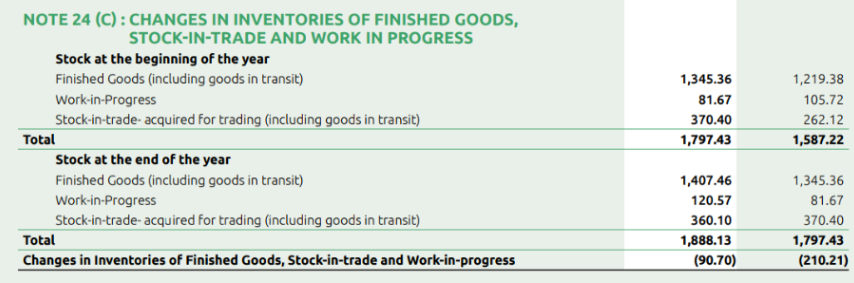

Changes in inventories of Finished Goods, Stock in Trade and Work in Progress: It is the cost that is incurred in manufacturing finished goods.

Changes in inventories of Finished Goods, Stock in Trade and Work in Progress: It is the cost that is incurred in manufacturing finished goods.

Change in inventory of finished goods refers to the costs incurred in the past on the goods which are sold in the current year.

The negative amount indicates that the company produced more items in the current year than it managed to sell.

The negative amount indicates that the company produced more items in the current year than it managed to sell.

So for example, you manufactured 100 units in CY but were able to sell 80 units only so while preparing the P&L statement the cost charged should be of 80 units only so we will reduce the cost of remaining 20 units in the CY and add back whenever these 20 units are sold.

So till now we have discussed 3⃣ costs i.e, cost of material consumed, purchases & change in inventories. If we add all these 3 we get the Cost of Goods Sold and if we reduce it from Revenue from Operations we will get the Gross Profit.

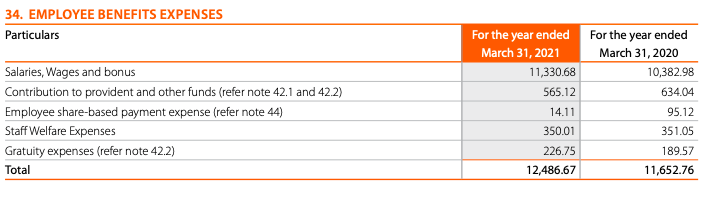

Employee Benefits Expenses

This is the next line items in expenses and includes all expenses incurred on employees like salaries paid to employees, remuneration to directors, ESOP costs, contribution towards provident funds, gratuity and staff welfare expenses.

Check this ⤵️⤵️

This is the next line items in expenses and includes all expenses incurred on employees like salaries paid to employees, remuneration to directors, ESOP costs, contribution towards provident funds, gratuity and staff welfare expenses.

Check this ⤵️⤵️

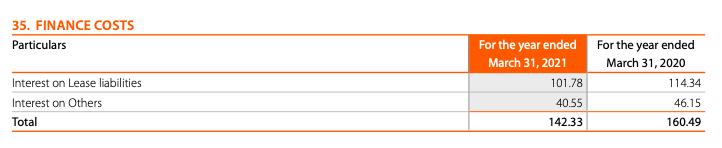

Finance Costs ➕➗

Finance cost is the interest & other related payments that company is paying on its borrowings. Companies can borrow from anyone like banks, private lenders, directors or from related parties. It also includes interest on lease liabilities.

Finance cost is the interest & other related payments that company is paying on its borrowings. Companies can borrow from anyone like banks, private lenders, directors or from related parties. It also includes interest on lease liabilities.

Here investors should track 2 things:

1⃣Average borrowing rate: Investors can compute it as Interest cost / Borrowings shown in the balance sheet. This needs to be checked whether it is as per normal banking rates.

1⃣Average borrowing rate: Investors can compute it as Interest cost / Borrowings shown in the balance sheet. This needs to be checked whether it is as per normal banking rates.

2⃣Interest cost on loan from directors or related parties: Directors may charge very high interest on their loans to get the cash out from the company, so as an investor we should check it very carefully.

Coming to the most important expense items:- Depreciation and Amortisation

For example, suppose you are a manufacturer of T-shirts and during the year you earned a profit of Rs. 10,00,000.

For example, suppose you are a manufacturer of T-shirts and during the year you earned a profit of Rs. 10,00,000.

For example, suppose you are a manufacturer of T-shirts and during the year you earned a profit of Rs. 10,00,000.

Now to expand your business you thought to manufacture Jeans as well along with T-shirts and for that you need to purchase new machinery costing Rs. 6,00,000.

Now to expand your business you thought to manufacture Jeans as well along with T-shirts and for that you need to purchase new machinery costing Rs. 6,00,000.

You are expecting that you will be using this machine for the next 5 years.

Now if you charge the cost of the machine directly in P&L then profit will be reduced to just 4,00,000 (10 lakhs - 6 lakhs) which is not correct because you will be using this machine for next 5 years.

Now if you charge the cost of the machine directly in P&L then profit will be reduced to just 4,00,000 (10 lakhs - 6 lakhs) which is not correct because you will be using this machine for next 5 years.

Hence it makes sense to spread the cost of the asset over its useful life. This is called depreciation.

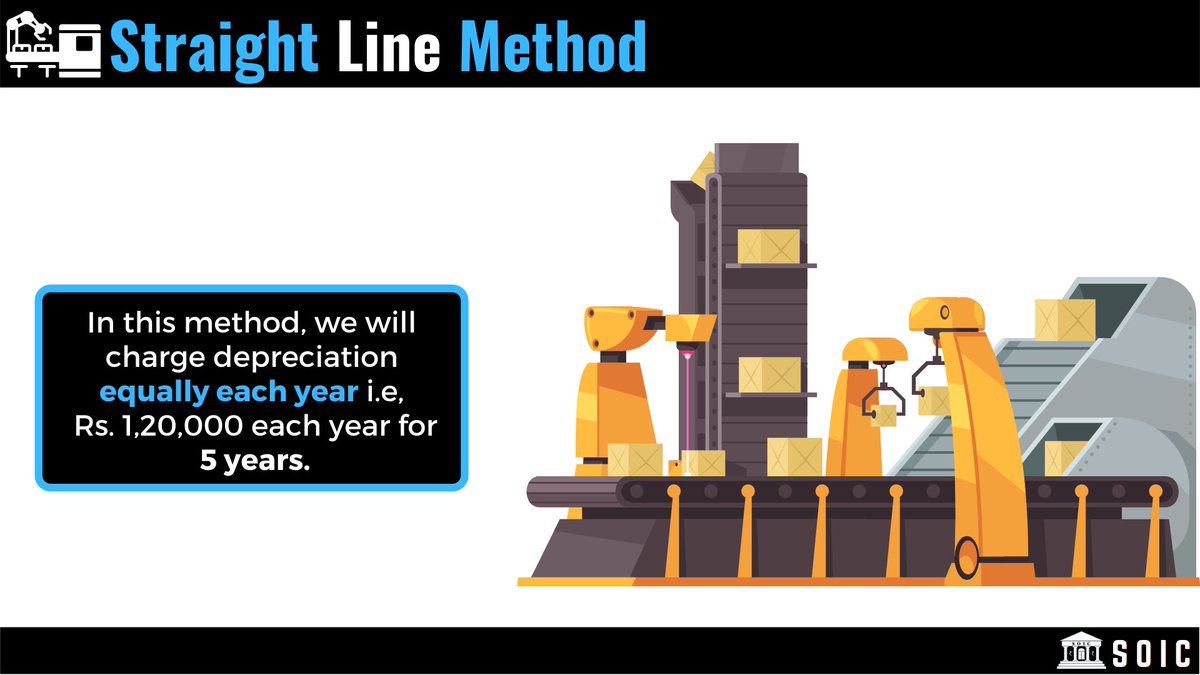

Here rather than charging Rs. 6,00,000 in year 1 you can charge Rs. 1,20,000 each year for next 5 years (6,00,000 / 5 Years).

Here rather than charging Rs. 6,00,000 in year 1 you can charge Rs. 1,20,000 each year for next 5 years (6,00,000 / 5 Years).

Depreciation can be charged only on tangible assets except land. Tangible assets means assets which you can touch like buildings, machines, computers, etc.

In the same way when we charge depreciation on intangible assets like brands, goodwill then it is known as amortization.

In the same way when we charge depreciation on intangible assets like brands, goodwill then it is known as amortization.

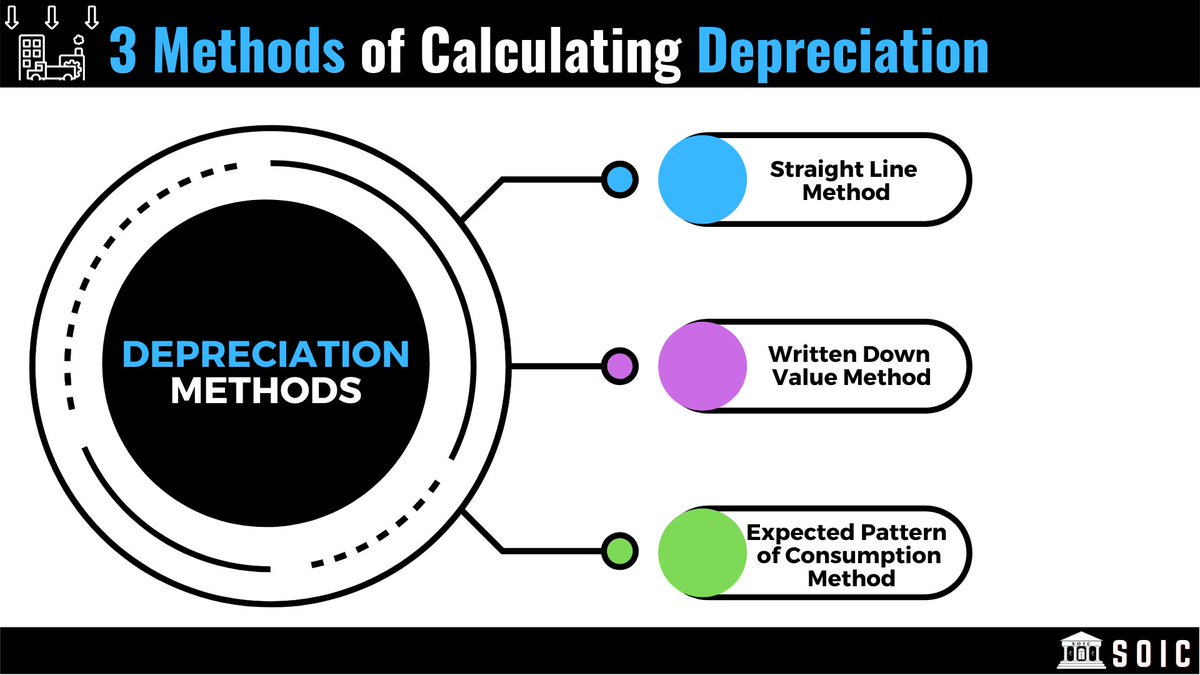

There are 3 methods to calculate depreciation

🔽🔽🔽

🔽🔽🔽

1⃣ Straight line method: In this method as discussed above we will charge depreciation equally in each year i.e, Rs. 1,20,000 each year for 5 years.

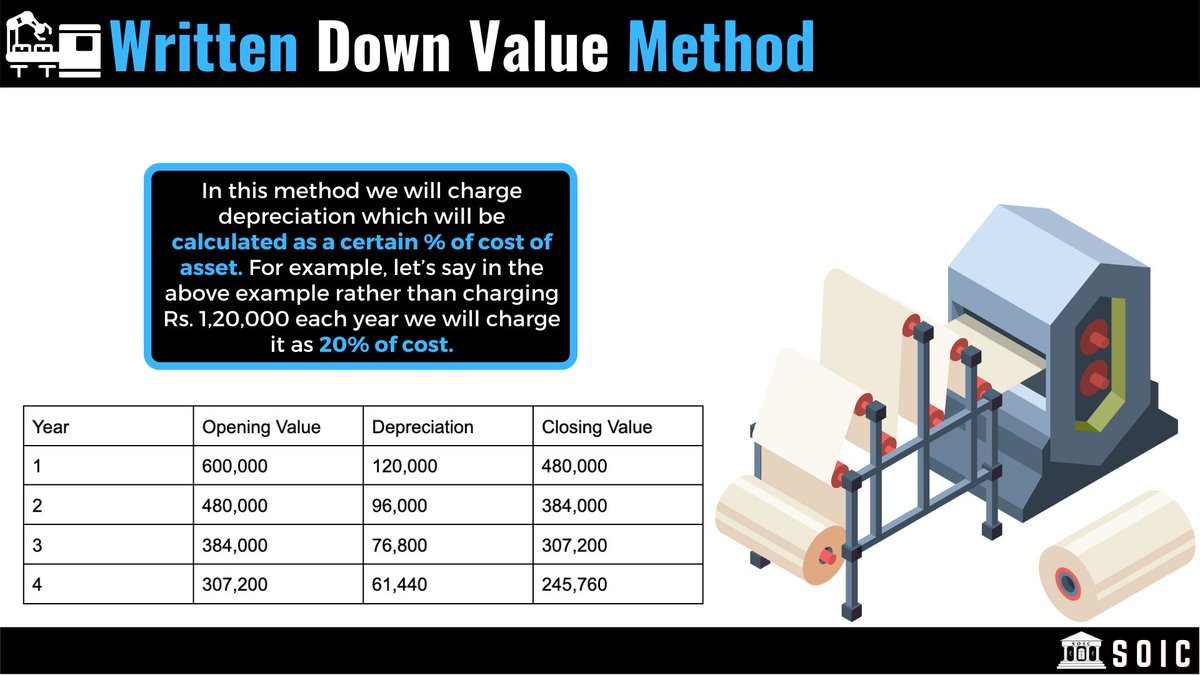

Written Down Value method: In this method we will charge depreciation which will be calculated as a certain % of cost of asset.

In WDV depreciation is higher in year 1 and then reduces every year.

In WDV depreciation is higher in year 1 and then reduces every year.

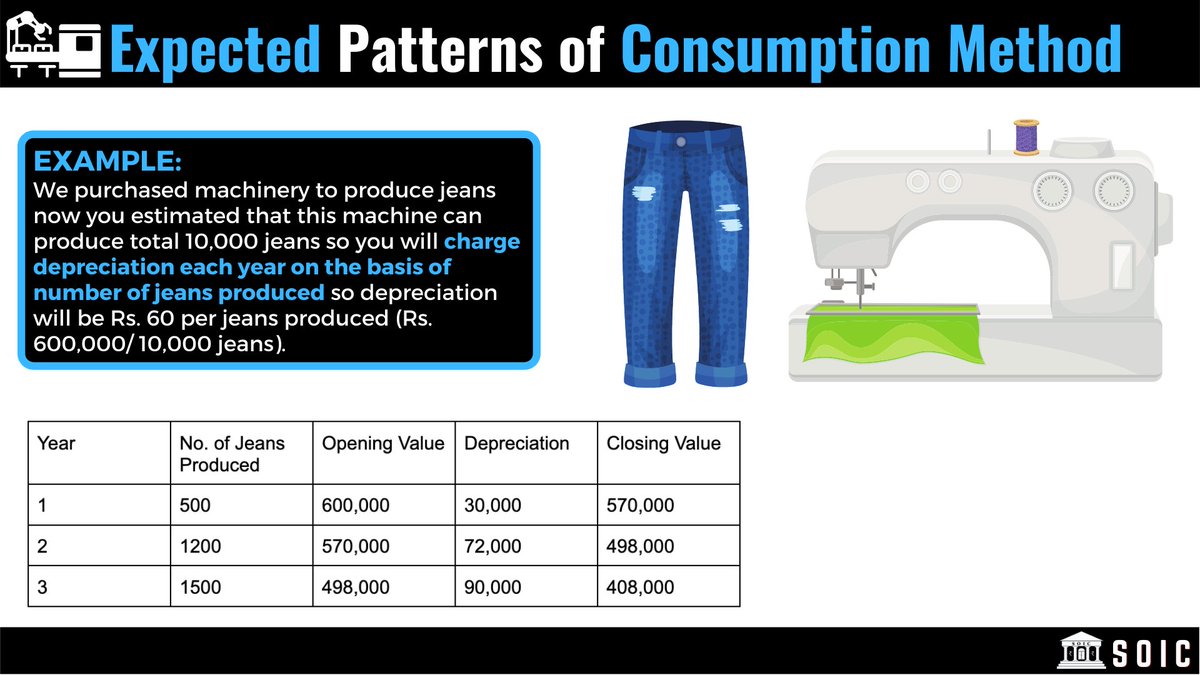

Expected pattern of consumption: In this method depreciation is charged on the basis of the number of units produced from that asset.

This is very aggressive accounting because under this companies show more profits in initial years when production is low.

This is very aggressive accounting because under this companies show more profits in initial years when production is low.

Investor must track the method of depreciation the company is using and check it with the players in the industry.

Also track the change in useful life of assets, many companies change the asset life and increase it so they can charge lower dep in books and show more profits.

Also track the change in useful life of assets, many companies change the asset life and increase it so they can charge lower dep in books and show more profits.

For example, if we change the life of an asset in our example from 5 yrs to 10 yrs then it will reduce my depreciation amount from 120,000 to 60,000 in Straight line method.

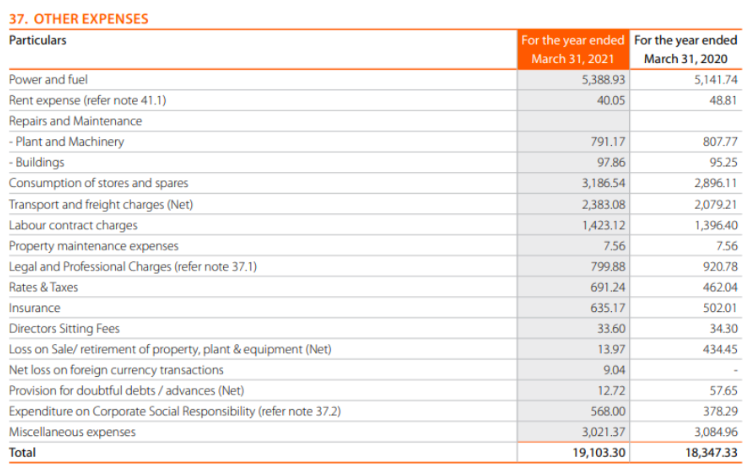

Now comes to last line item in expenses which is Other Expenses: ⤵️

Other expenses are all those expenses which are not covered in above line items.

It includes expenses like selling, general & administrative expenses, audit fees, advertisement expenses, legal & professional fees, travel expenses, repairs, insurance, other miscellaneous exp etc.

It includes expenses like selling, general & administrative expenses, audit fees, advertisement expenses, legal & professional fees, travel expenses, repairs, insurance, other miscellaneous exp etc.

Here investors should track the amount of miscellaneous expenses as a % of sales and compare with other players in industry because management doesn't provide the break-up of these expenses so there may be chances of siphoning off money from the company.

Now we will see the Exceptional gains & losses

Exceptional gain or loss can arise due to any transaction which is not in the ordinary course of business, which company see as one time thing and not recurring in future like sale of subsidiary company, impairment of investments.

Exceptional gain or loss can arise due to any transaction which is not in the ordinary course of business, which company see as one time thing and not recurring in future like sale of subsidiary company, impairment of investments.

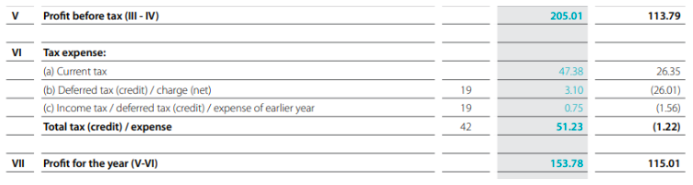

After exceptional items we get the amount of Profit before Tax, which can be calculated as

Total Income - Total Expense +/- Exceptional gain / loss.

=Profit Before Tax

Total Income - Total Expense +/- Exceptional gain / loss.

=Profit Before Tax

After this we deduct the tax amount from PBT. There are 3 types of Tax:

1.Current Tax: It is corporate tax applicable in the current year.

2.Deferred Tax: It is the adjusted tax amount due to change in profit computation as per Income Tax Act & as per Companies Act.

1.Current Tax: It is corporate tax applicable in the current year.

2.Deferred Tax: It is the adjusted tax amount due to change in profit computation as per Income Tax Act & as per Companies Act.

3. Income tax expense of earlier year: It is the amount of tax which is paid in the current year but relating to the previous year like any demand raised by the income tax department for previous year

This is how it looks:-

This is how it looks:-

Finally after reducing all the taxes. We come to

PAT which also known as Profit after tax or Bottomline of the company.

PAT which also known as Profit after tax or Bottomline of the company.

If you enjoyed this tweet, consider retweeting to educate the maximum investors!

I am also doing a master class on how to value a company on the coming Sunday from 1pm onwards!

Link to register:-pages.razorpay.com

I am also doing a master class on how to value a company on the coming Sunday from 1pm onwards!

Link to register:-pages.razorpay.com

Thank you for reading!

------The End-----

------The End-----

Loading suggestions...