In Accounting, you can record the same transaction multiple ways, depending on which accounting method you use.

Weird, right?

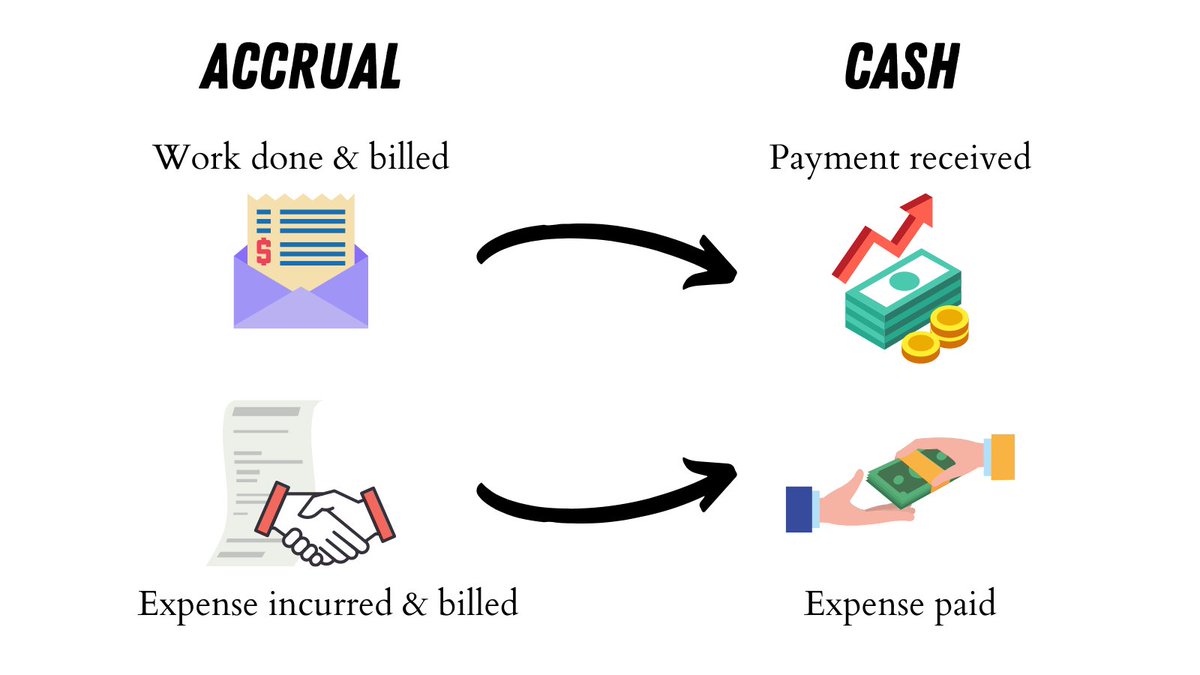

Let me simplify Cash vs Accrual Accounting for you:

Weird, right?

Let me simplify Cash vs Accrual Accounting for you:

Cash = recorded when revenue received & expenses paid

Accrual = recorded when revenue earned (or work done) & expenses incurred

The best way to understand this is through an example:

Accrual = recorded when revenue earned (or work done) & expenses incurred

The best way to understand this is through an example:

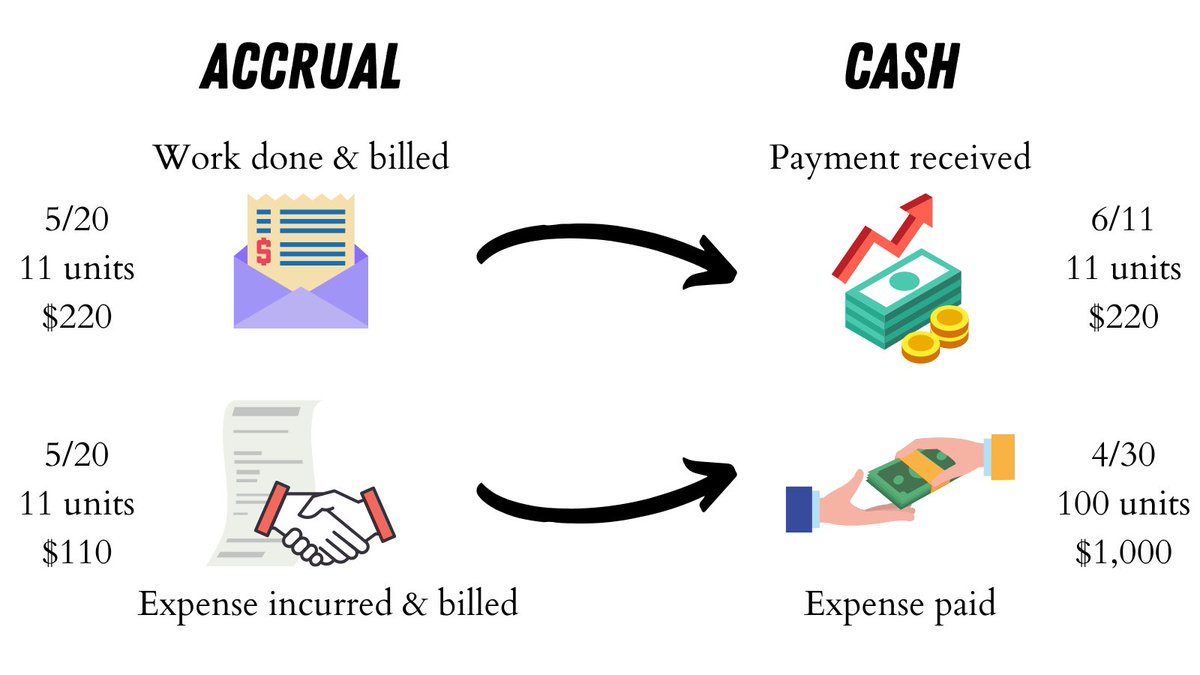

On April 21, ABC Company orders 100 units of Widget A for $1,000 ($10/unit), which they will later sell. They pay for these units on April 30.

Cash: expense is recorded when paid on April 30

Accrual: expense is recorded when sold; until then it’s recorded to inventory

Cash: expense is recorded when paid on April 30

Accrual: expense is recorded when sold; until then it’s recorded to inventory

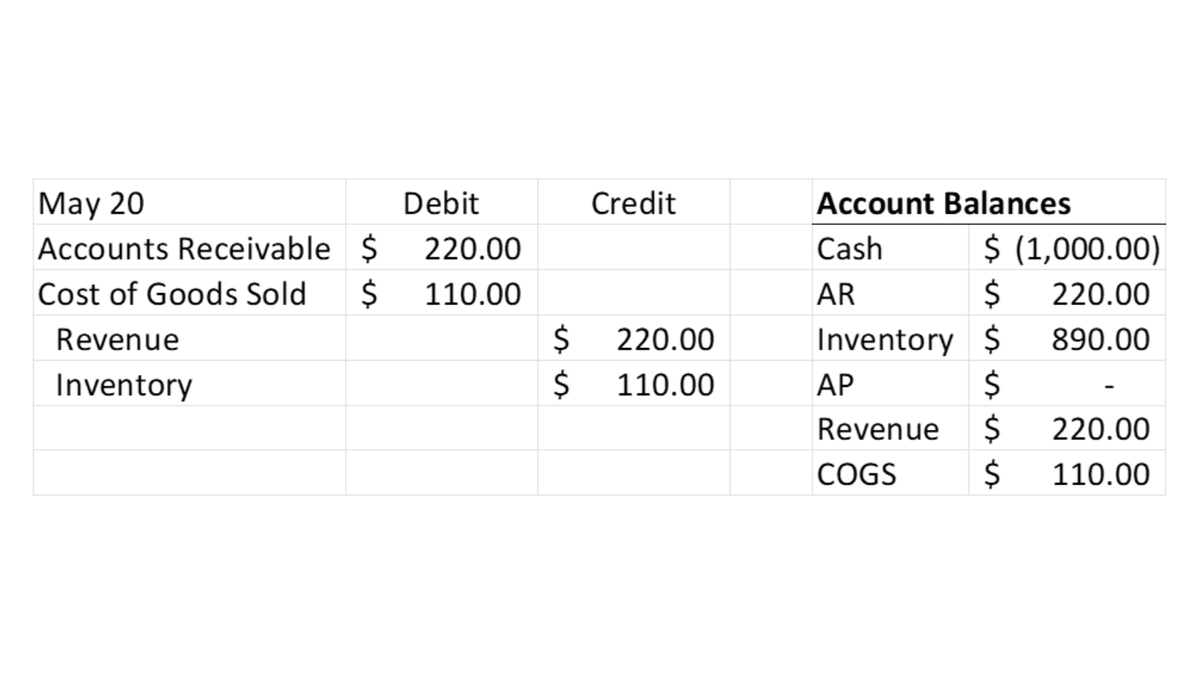

So now, on May 20, ABC sells 11 of those units ($10/unit x 11 units) for $20/unit to XYZ Company.

Cash: no action is needed

Accrual: revenue is recorded for $220 (11 units x $20/unit) and expense for $110 (11 x $10/unit cost)

Cash: no action is needed

Accrual: revenue is recorded for $220 (11 units x $20/unit) and expense for $110 (11 x $10/unit cost)

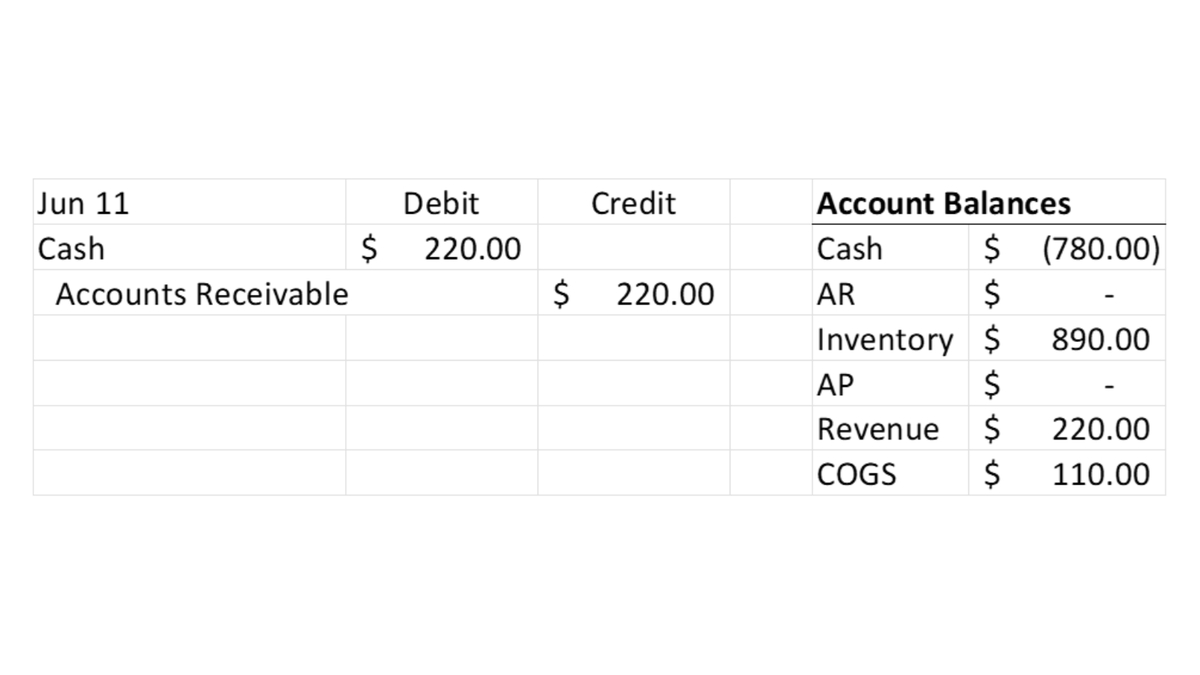

XYZ doesn’t pay for the units until June 11.

Cash: revenue is recorded for $220 (11 units x $20/unit)

Accrual: no action is needed

Cash: revenue is recorded for $220 (11 units x $20/unit)

Accrual: no action is needed

To summarize the transaction:

Cash: revenue is recorded when the money is received (6/11) and expense when Widget A was paid for (4/30)

Accrual: revenue is recorded when earned (5/20) and expense on the same date (5/20)

Cash: revenue is recorded when the money is received (6/11) and expense when Widget A was paid for (4/30)

Accrual: revenue is recorded when earned (5/20) and expense on the same date (5/20)

It’s natural to ask: in Accrual, if the units aren’t recorded immediately, how are they accounted for?

That brings us to the beauty of accounting.

Let me introduce to you some accounts:

• Accounts Receivable

• Accounts Payable

• Inventory

That brings us to the beauty of accounting.

Let me introduce to you some accounts:

• Accounts Receivable

• Accounts Payable

• Inventory

So let’s go through the same transaction again and focus on the Accrual transaction.

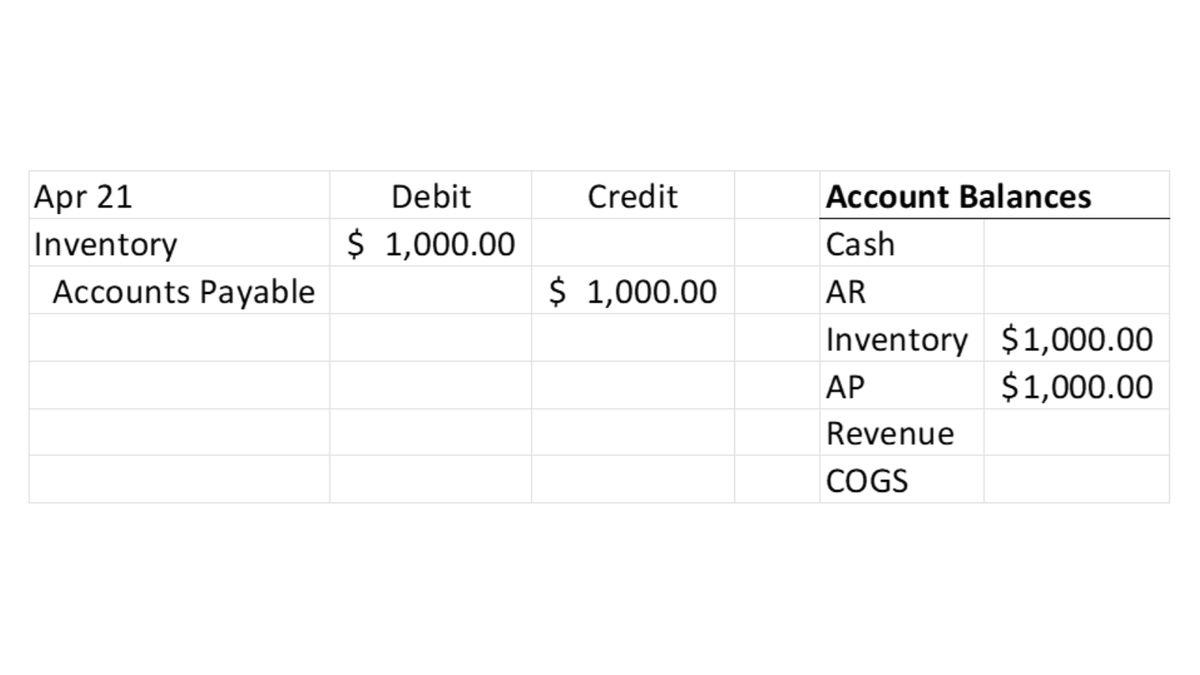

On April 21, ABC orders 100 units of Widget A for $1,000 ($10/unit).

This order is recorded to Inventory (increase) and Accounts Payable (increase).

On April 21, ABC orders 100 units of Widget A for $1,000 ($10/unit).

This order is recorded to Inventory (increase) and Accounts Payable (increase).

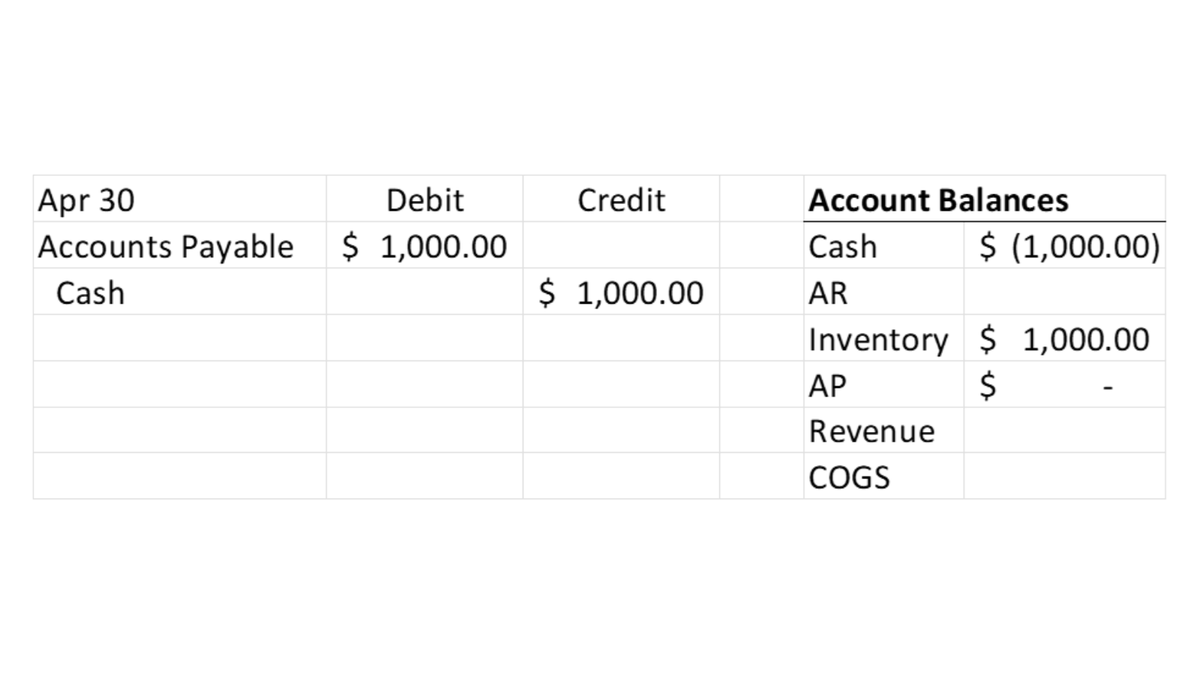

When the 100 units are paid for on April 30, Accounts Payable decreases and Cash decreases.

The units are then sold on May 20, which is when revenue and expenses come into the picture.

BUT, only the units sold are recorded.

Revenue is recorded at the price sold $220 and Expense (COGS) and Inventory is recorded at the COST of $110.

BUT, only the units sold are recorded.

Revenue is recorded at the price sold $220 and Expense (COGS) and Inventory is recorded at the COST of $110.

Finally on June 11, the money is received.

This will increase Cash and move Accounts Receivable to zero.

As you can, you still have less cash than you started with!

This will increase Cash and move Accounts Receivable to zero.

As you can, you still have less cash than you started with!

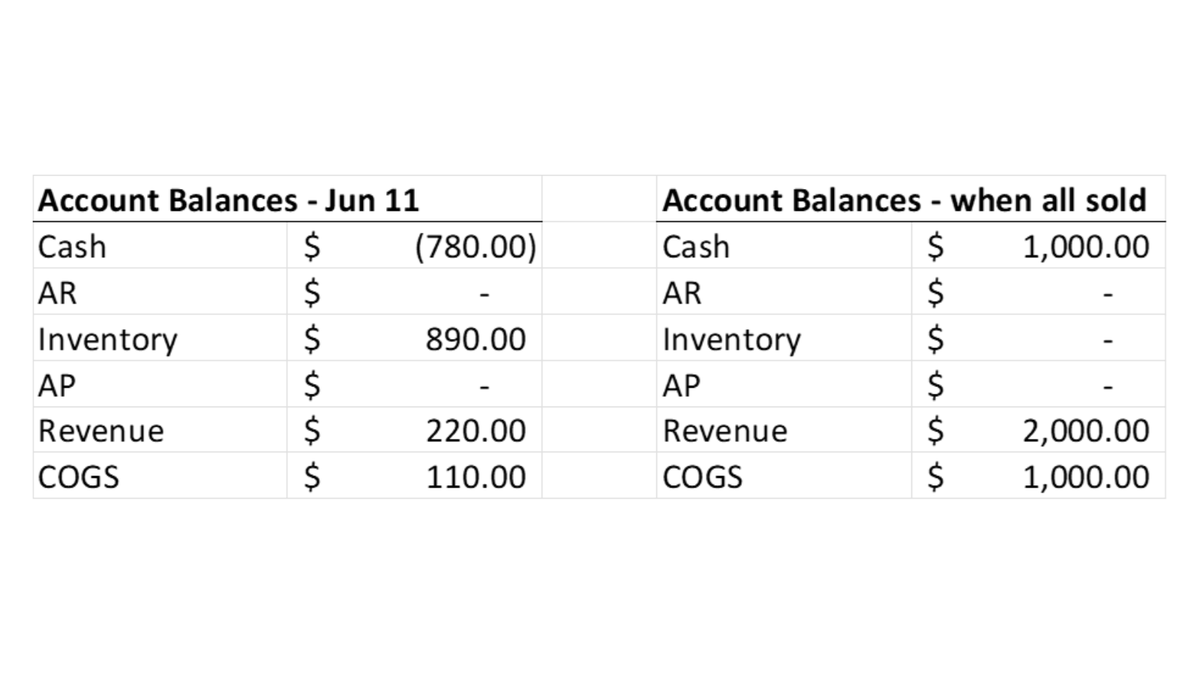

As you sell through, your:

• Cash increases

• Inventory decrease

• Revenue increases

• COGS increases

It's not until you sell everything that we get a full picture (see the image).

• Cash increases

• Inventory decrease

• Revenue increases

• COGS increases

It's not until you sell everything that we get a full picture (see the image).

You've made $1,000 before any General or Administrative expenses are accounted for, which is a 50% Gross Margin.

This is just ONE example and we could talk about many more.

For items that aren’t inventoried, they could be EXPENSED or CAPITALIZED.

Long-term assets (vehicles, furniture, land, etc) are capitalized and then depreciated as the item is used.

For items that aren’t inventoried, they could be EXPENSED or CAPITALIZED.

Long-term assets (vehicles, furniture, land, etc) are capitalized and then depreciated as the item is used.

If you want to dive deeper, join @IAmClintMurphy and me in our upcoming cohort.

In 3 days we’ll help you:

• make numbers-informed decisions

• communicate your numbers with clarity

Join now: maven.com

In 3 days we’ll help you:

• make numbers-informed decisions

• communicate your numbers with clarity

Join now: maven.com

@IAmClintMurphy That’s it for today. We'll tackle the rest later.

If you enjoyed this, follow me so you don’t anything as I decode Accounting for you: @KurtisHanni

I’d appreciate it if you’d retweet the first tweet to support me and spread the knowledge:

If you enjoyed this, follow me so you don’t anything as I decode Accounting for you: @KurtisHanni

I’d appreciate it if you’d retweet the first tweet to support me and spread the knowledge:

Loading suggestions...