Sandhar Technologies: Business Analysis.

The Mutual Fund of Auto Ancillaries? Let's find out.

A Thread 🧵👇 (RT if beneficial)

The Mutual Fund of Auto Ancillaries? Let's find out.

A Thread 🧵👇 (RT if beneficial)

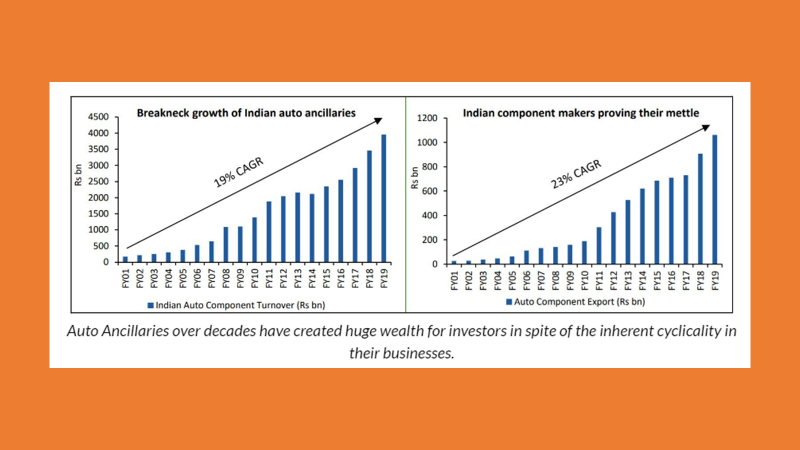

1/ Automotive is a cyclical industry, due to a 4W/2W being a high-cost ticket item vs an average consumer’s salary (think booms & busts 👇)

What makes me interested currently? It’s the tough times (FY18-present), one of the longest downcycle in its post-liberalization history.

What makes me interested currently? It’s the tough times (FY18-present), one of the longest downcycle in its post-liberalization history.

2/ What this means is that we might be very near an upcycle as long-term secular demographic trends continue to trend upwards.

One can never predict the exact timelines, just position themselves to benefit from events of high probability.

Historical performance of this sector👇

One can never predict the exact timelines, just position themselves to benefit from events of high probability.

Historical performance of this sector👇

3/ So, What is an Auto Ancillary?

A modern car requires thousands of parts; the OEMs (for ex. Maruti) that produce these cars doesn't make most of the components in-house.

Sandhar Tech is one such Tier-1 components supplier to these OEMs; known as an auto ancillary.

A modern car requires thousands of parts; the OEMs (for ex. Maruti) that produce these cars doesn't make most of the components in-house.

Sandhar Tech is one such Tier-1 components supplier to these OEMs; known as an auto ancillary.

4/ They are a sort of a mutual fund of auto components as they have developed the capabilities to produce & scale multiple segments of components, vs most of their competitors who are focused on one or two segment.

Through in-house R&D, global tie-ups, & tech acquisitions.

Through in-house R&D, global tie-ups, & tech acquisitions.

5/ "Not a specialized company, but a generalized company."

What do I mean by that? visible in the breadth of products they do.

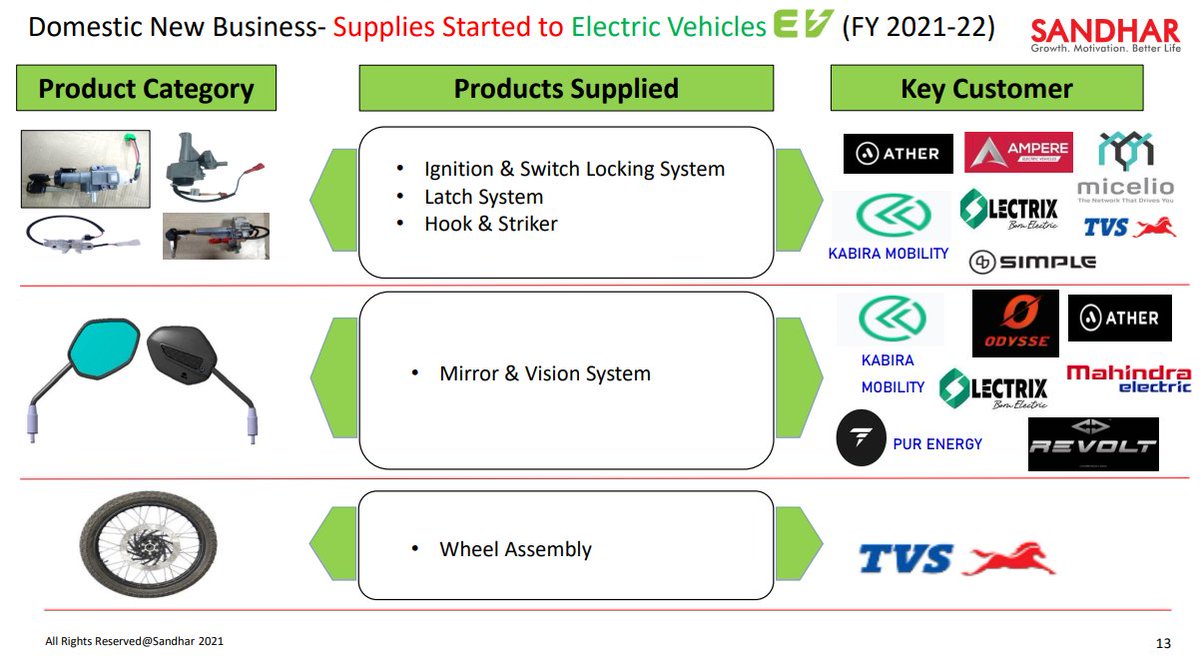

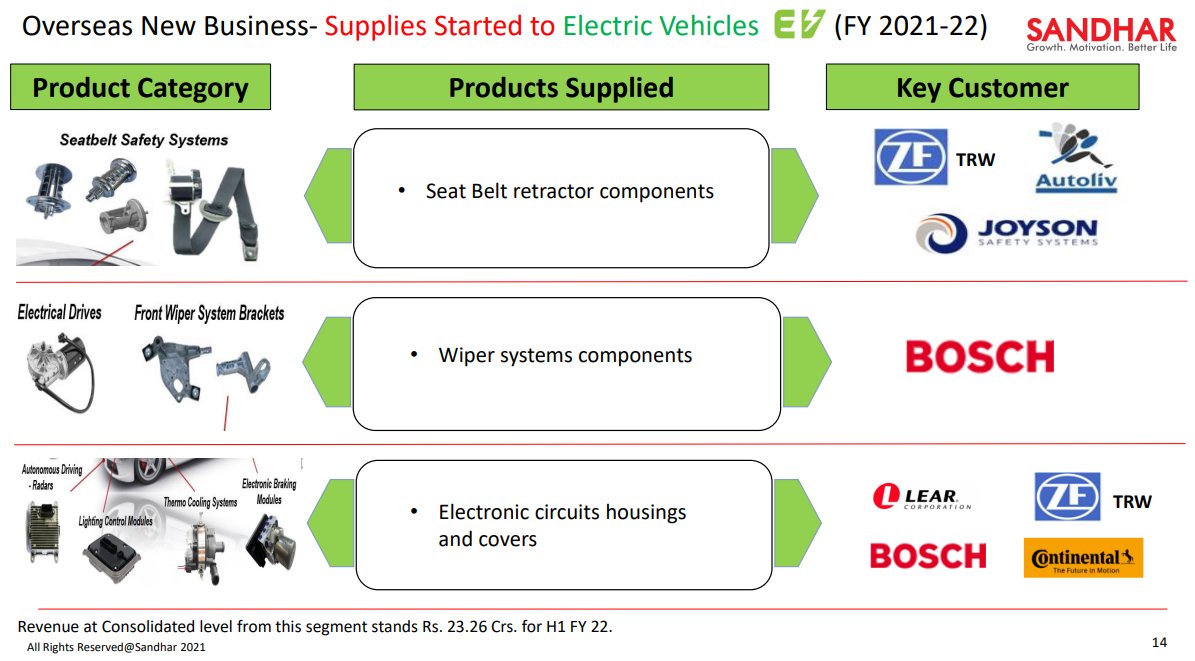

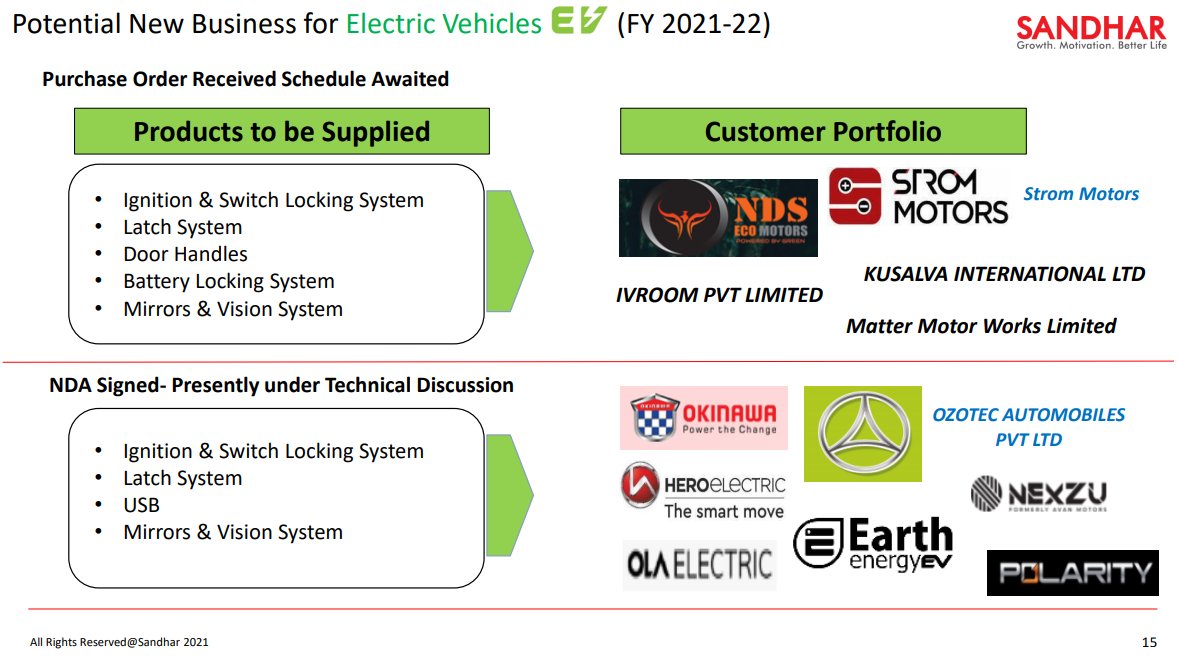

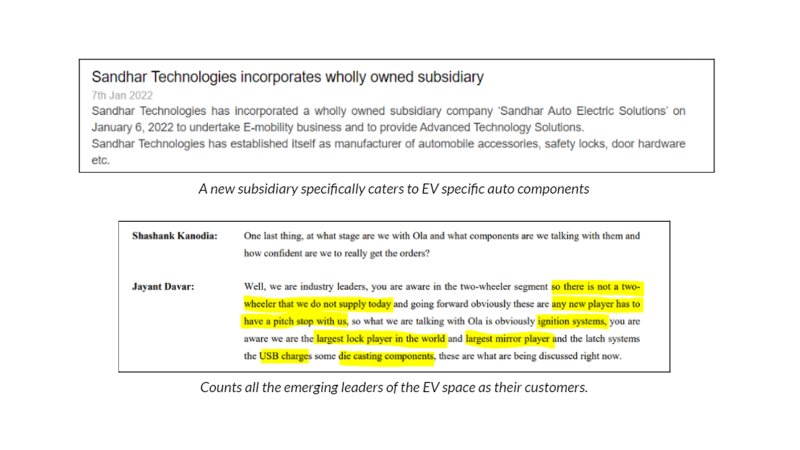

Just look at their initiatives in EV-related parts (they supply to almost all EV OEMs in India), & also have set up a new subsidiary for the same.

What do I mean by that? visible in the breadth of products they do.

Just look at their initiatives in EV-related parts (they supply to almost all EV OEMs in India), & also have set up a new subsidiary for the same.

6/ You should ask: Are they spreading themselves too thin? Their target is to become the best or second-best in all products they sell; demonstrated from time to time.

Largest suppliers of Lock (largest globally), Mirrors, and OHV cabins in India and Aluminum spools in Europe.

Largest suppliers of Lock (largest globally), Mirrors, and OHV cabins in India and Aluminum spools in Europe.

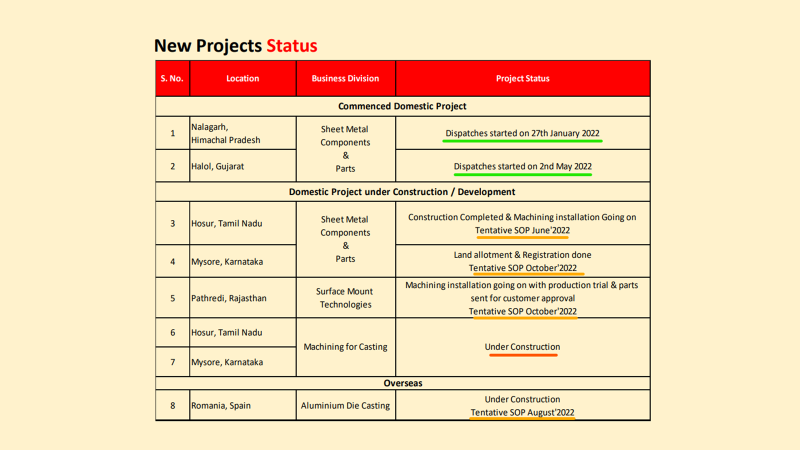

7/ They’ve gone from having 5 manufacturing plants in 2005 to 32 in 2017, and 43 in 2021 & plan to add 7 more (~50 in total) in 2022.

5 of which will go online by Q2FY23 & the last 2 being from the latest machining contract won from TVS (online by Q4FY23)

5 of which will go online by Q2FY23 & the last 2 being from the latest machining contract won from TVS (online by Q4FY23)

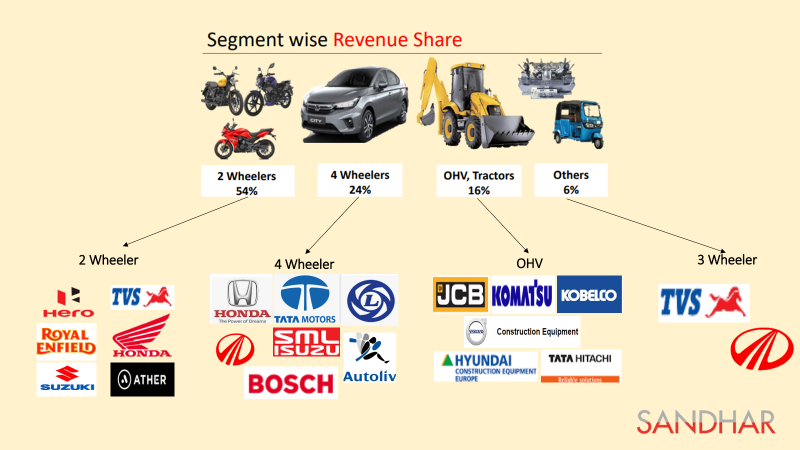

8/ Which OEMs do they get their rev from?

2Ws, 4Ws & Off-Highway Vehicles (OHVs) make up the majority.

Do they cater to most of the OEMs & are diversified in terms of revenue? tick.

2Ws, 4Ws & Off-Highway Vehicles (OHVs) make up the majority.

Do they cater to most of the OEMs & are diversified in terms of revenue? tick.

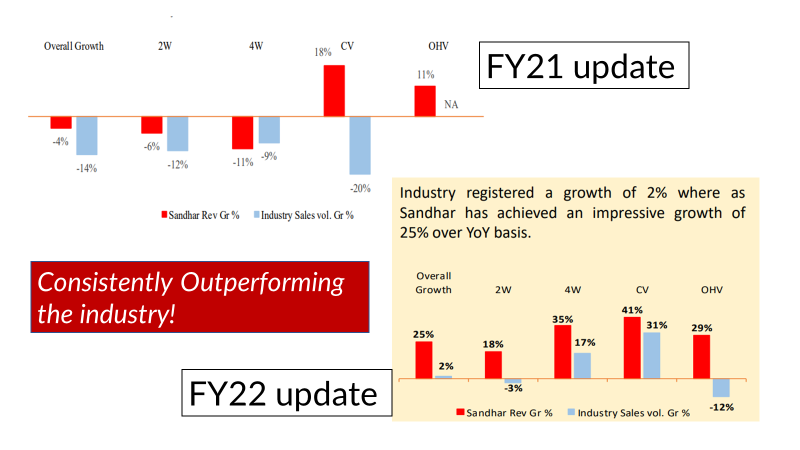

9/ How have they fared against the industry downturn? It is visible in their FY21 & FY22 updates that Sandhar has been consistently outperforming the industry

How? they reported the highest ever quarterly sales in Q4FY22 while industry volumes are down 30-40% from highs.

How? they reported the highest ever quarterly sales in Q4FY22 while industry volumes are down 30-40% from highs.

10/ Why am I interested in Sandhar specifically? Operating leverage.

The majority of the plants after 2017 are running at low utilization, which can be picked up with a reinvigoration of the auto cycle.

Capacity doubled in the last 4 years & capabilities improved multifold.

The majority of the plants after 2017 are running at low utilization, which can be picked up with a reinvigoration of the auto cycle.

Capacity doubled in the last 4 years & capabilities improved multifold.

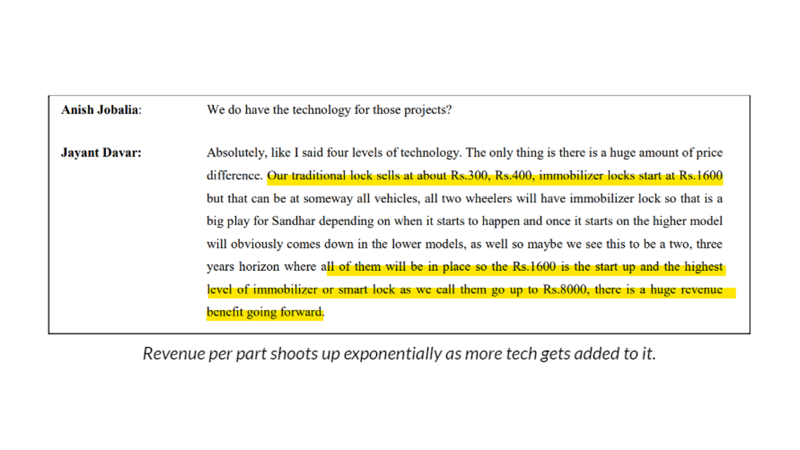

11/ Value add business: Increasing tech & content per vehicle (as they continue to win deals for newer products from existing customers)

The margins (the latest machining business has a 27% EBITDA margin) & ROCE of the value-added products are better.

The margins (the latest machining business has a 27% EBITDA margin) & ROCE of the value-added products are better.

12/ International business scaling up from the current 15% of rev (rest revenue from India)

“The EBITDA margins are in fact now higher than that of the Indian business and with the new plant in Romania those numbers will accentuate and grow even faster.” ~Management.

“The EBITDA margins are in fact now higher than that of the Indian business and with the new plant in Romania those numbers will accentuate and grow even faster.” ~Management.

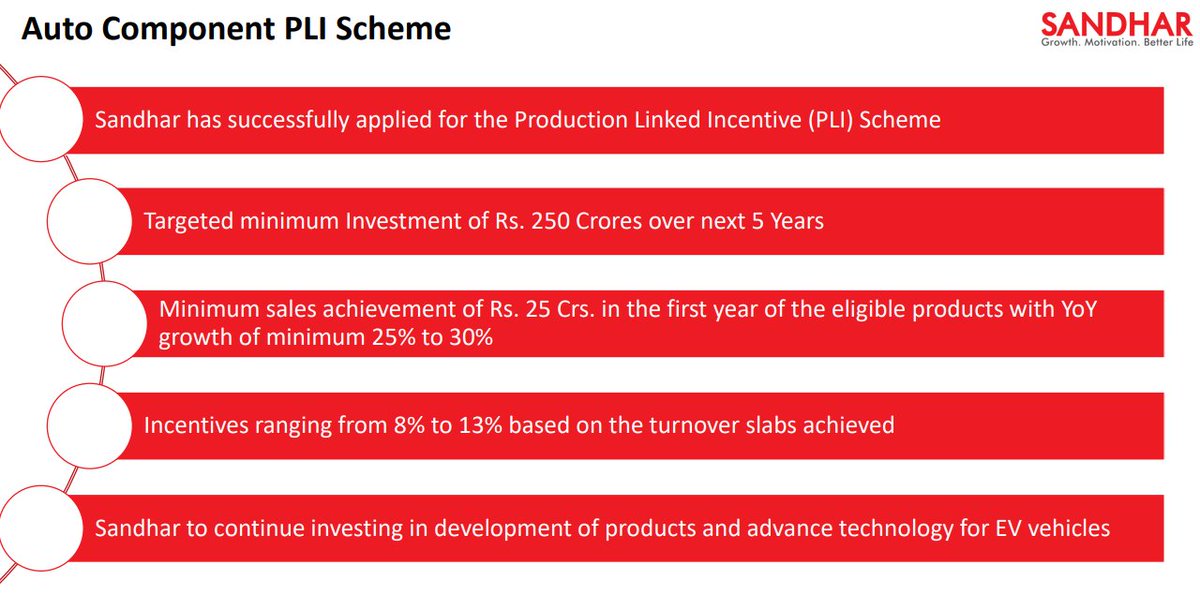

13/ A beneficiary of the PLI scheme (already approved): this positions themselves for the next leg of hi-tech products for which specifically has PLI been allotted.

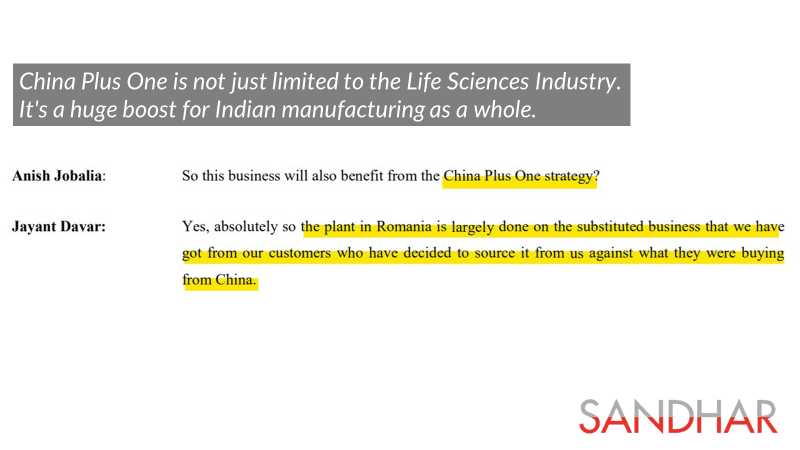

Also a beneficiary of the China+1 story.

Also a beneficiary of the China+1 story.

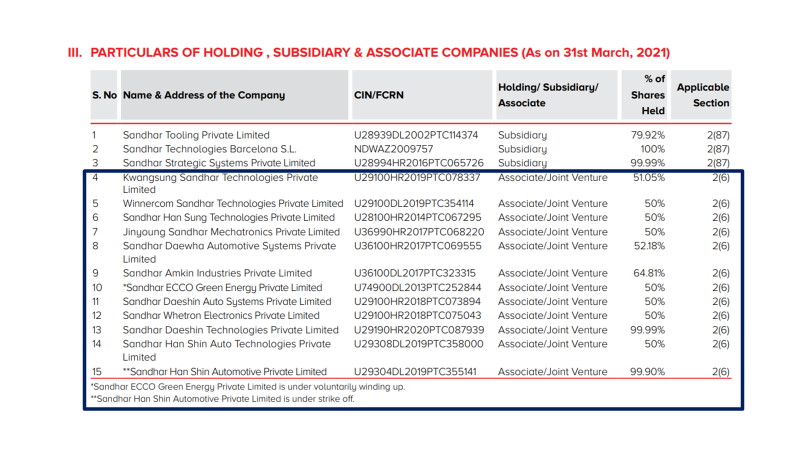

14/ Not to forget that Sandhar has 11 JVs with MNCs across the world & that has been cumulatively losing 8-10 crores yearly today.

Due to disruptions from COVID; should come back & showcase +ve net margins once they scale.

Targetting 500crs/yr sales (10% of rev) in 3 years

Due to disruptions from COVID; should come back & showcase +ve net margins once they scale.

Targetting 500crs/yr sales (10% of rev) in 3 years

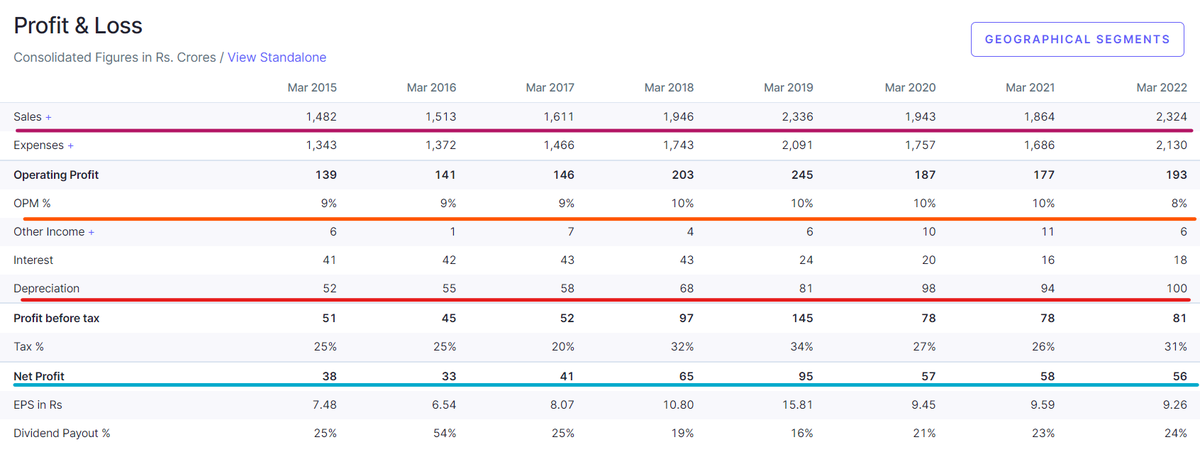

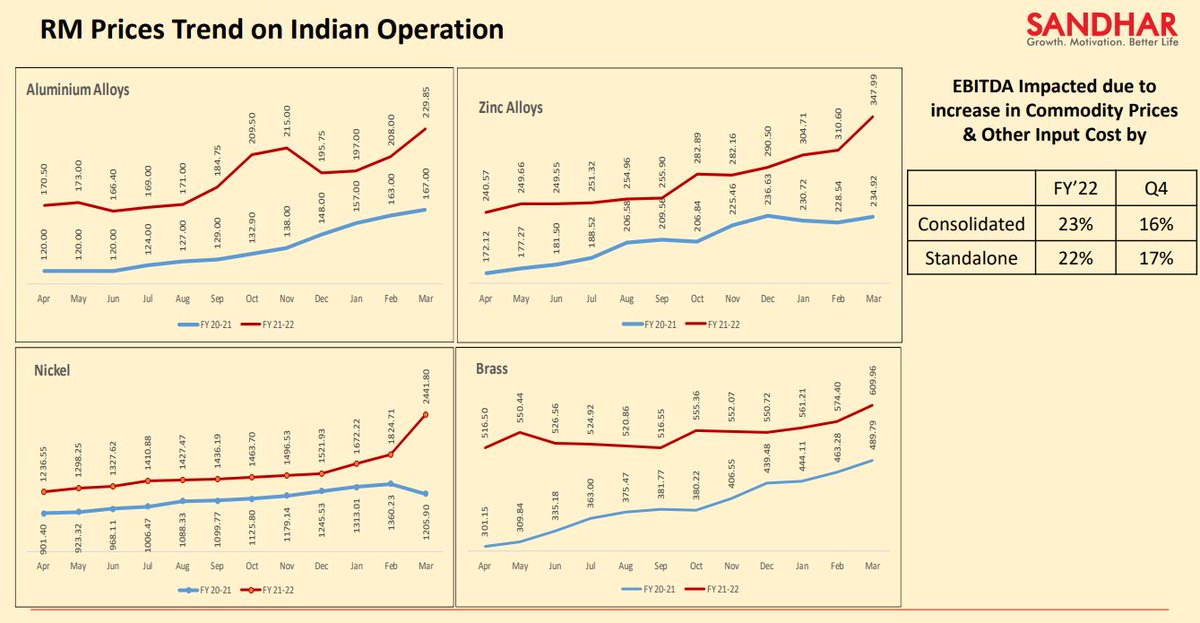

15/ Financials: Profit & Loss

All-time high quarterly revenue run rate with temporarily low margins due to RM inflation (passing on takes 1-2 quarters; different metal prices across the year👇)

All-time high quarterly revenue run rate with temporarily low margins due to RM inflation (passing on takes 1-2 quarters; different metal prices across the year👇)

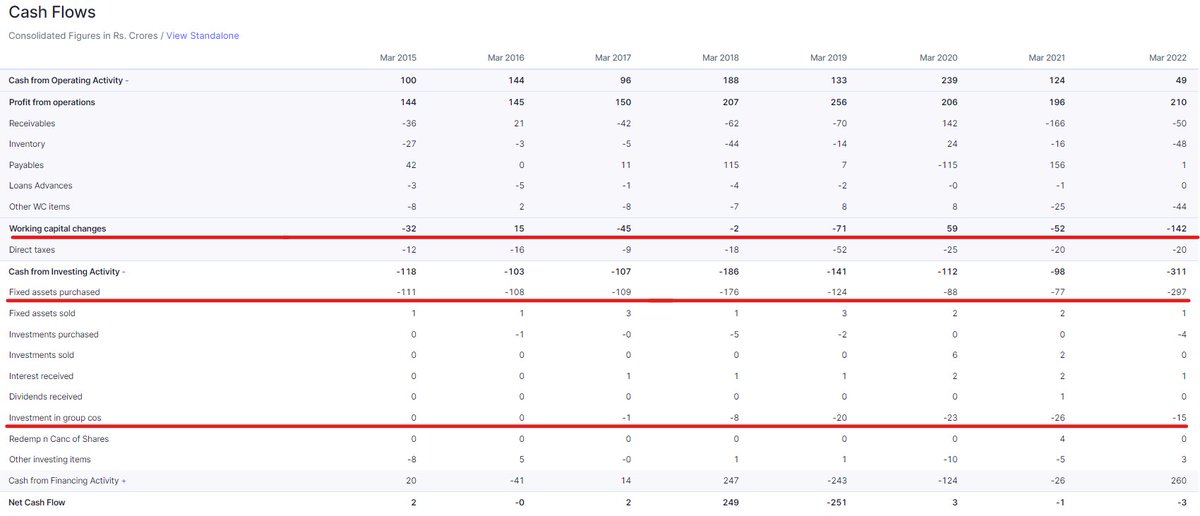

16/ Financials:

Debt might look a lot higher. however, only 250crs is LT while the other is ST at a 4.5% interest rate due to a stretched working capital (should normalise)

Cashflows have been strong historically+ Huge capex investments over the last many years.

Debt might look a lot higher. however, only 250crs is LT while the other is ST at a 4.5% interest rate due to a stretched working capital (should normalise)

Cashflows have been strong historically+ Huge capex investments over the last many years.

17/ Guidance is strong going forward as new plants (most of which are 100% booked from day 1) start contributing.

Capex for FY23 at 350crs & projecting a rev growth of 35-40% with improved margins.

Seems a bit aggressive no, let's talk about the management.

Capex for FY23 at 350crs & projecting a rev growth of 35-40% with improved margins.

Seems a bit aggressive no, let's talk about the management.

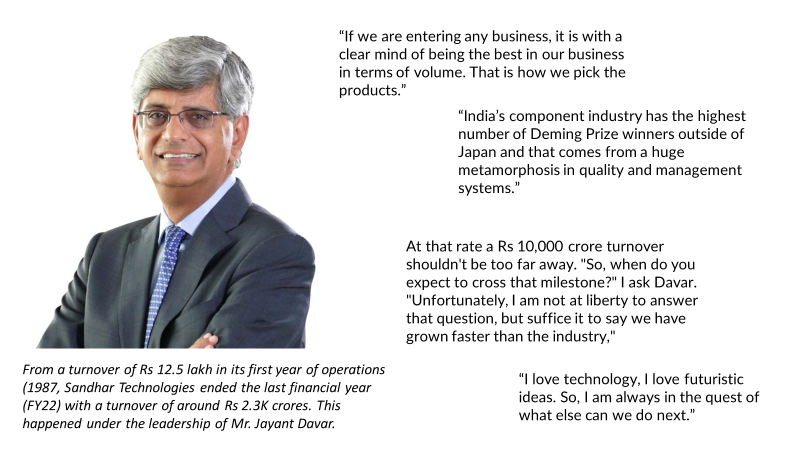

18/ Enter Mr. Jayant Davar, some videos to understand his mindset (other than the delightful concalls)

1. m.youtube.com

During COVID lockdowns:

2. m.youtube.com

3. bit.ly

1. m.youtube.com

During COVID lockdowns:

2. m.youtube.com

3. bit.ly

19/ Remuneration: under control & rightly incentivized: Mr. Davar takes 80-90% of their salary as a % commission of the profits (4% in that particular case which is reasonable from my point of view)

20/ Rational capital allocation philosophy:

Would not invest in brownfield, greenfield, or M&A until & unless they see a min of 2.5-3x asset turns & 20-25% ROCEs in that project

While this has not been visible in the numbers till now, should do as utilization increases.

Would not invest in brownfield, greenfield, or M&A until & unless they see a min of 2.5-3x asset turns & 20-25% ROCEs in that project

While this has not been visible in the numbers till now, should do as utilization increases.

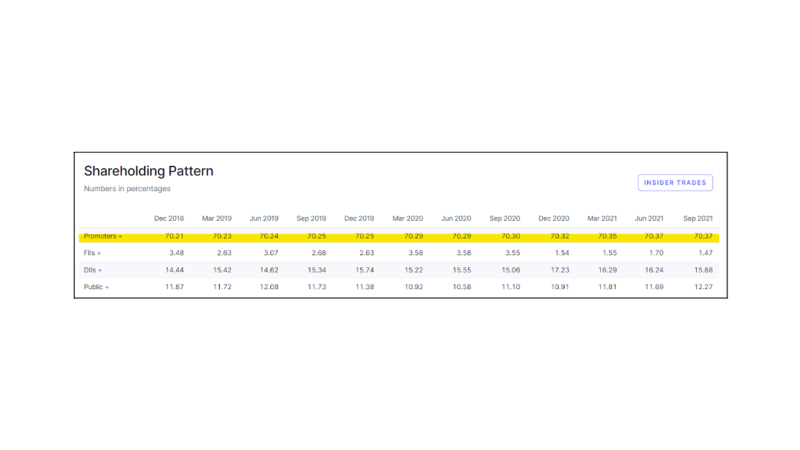

21/ Promoter’s holding is at 70.4% & the same has been continuously buying from the market since the IPO even at prices that are much higher than the CMP.

Mr. Davar has added shares b/w prices of 350-195 over the last 4 years (CMP at 240)

Mr. Davar has added shares b/w prices of 350-195 over the last 4 years (CMP at 240)

22/ Let's come to the risks

a. Complex capital structure (however, RPT is not an issue as of now)

b. High dependence on the recovery & growth of 2W Industry (50%+ rev as of FY22) which has seen a massive 35-40% drop in sales from FY19 highs. (should recover, no one knows when)

a. Complex capital structure (however, RPT is not an issue as of now)

b. High dependence on the recovery & growth of 2W Industry (50%+ rev as of FY22) which has seen a massive 35-40% drop in sales from FY19 highs. (should recover, no one knows when)

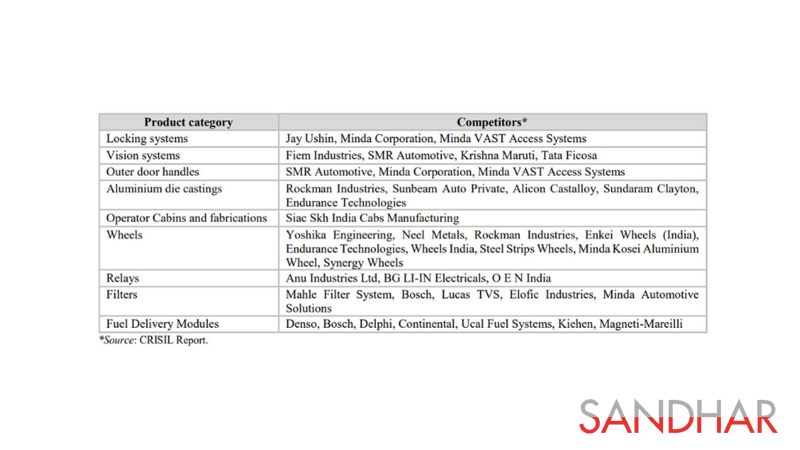

23/ c. Too diversified in terms of products: should require humongous amounts of management bandwidth to grow all.

d. Inflationary pressure on huge incremental capex should hurt ROCEs.

e. Humongous competition in every segment 👇

d. Inflationary pressure on huge incremental capex should hurt ROCEs.

e. Humongous competition in every segment 👇

24/ Conclusion

Current valuations at 0.6x TTM P/S & 6x EV/EBITDA (This is after normalizing for COVID impact in Q1FY22 & the recent RM inflation, as it is a pass on) are reasonable or cheap depending on how they deliver on the targeted growth of 30% over the next 3 years.

End.

Current valuations at 0.6x TTM P/S & 6x EV/EBITDA (This is after normalizing for COVID impact in Q1FY22 & the recent RM inflation, as it is a pass on) are reasonable or cheap depending on how they deliver on the targeted growth of 30% over the next 3 years.

End.

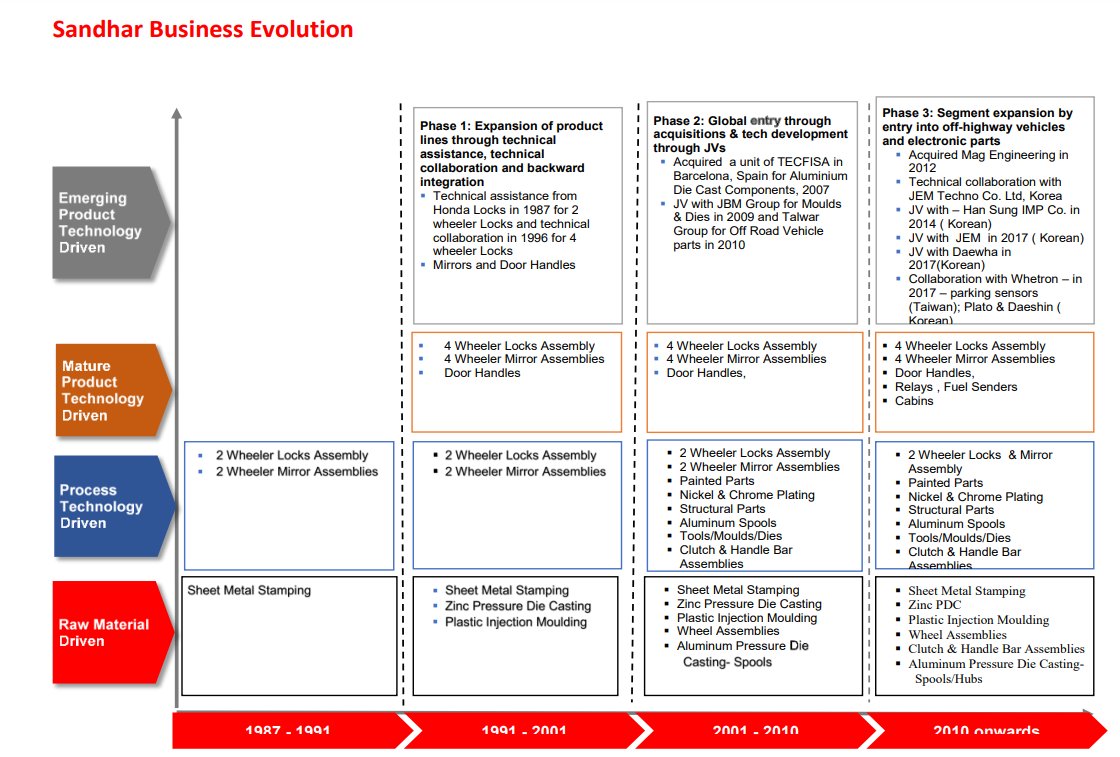

25/ Sandhar's business evolution over the past 35 years.

From a single product to a multi-product, from a single OEM to over 100 OEMs, from a single segment (2W) to almost every segment of vehicles.

Do they have what it takes to take the next leap of conviction?

From a single product to a multi-product, from a single OEM to over 100 OEMs, from a single segment (2W) to almost every segment of vehicles.

Do they have what it takes to take the next leap of conviction?

26/ A risk that is not talked about enough 🚨🚨🚨

It is a cyclical bet at best & if one is interested in the idea, they need to time their entry & exit with utmost precision otherwise they will get trapped until the next upcycle.

Proceed with caution, I am invested & biased.

It is a cyclical bet at best & if one is interested in the idea, they need to time their entry & exit with utmost precision otherwise they will get trapped until the next upcycle.

Proceed with caution, I am invested & biased.

27/ Another important risk for such stocks: Very low float in the market.

70% held by promoters

15% held by mutual funds

Rest by public

Personally have seen the stock move 4-5% (60-75crs in terms of market cap) with 10-20 lakhs of trading volume 🤷♂️

A double edged sword.

70% held by promoters

15% held by mutual funds

Rest by public

Personally have seen the stock move 4-5% (60-75crs in terms of market cap) with 10-20 lakhs of trading volume 🤷♂️

A double edged sword.

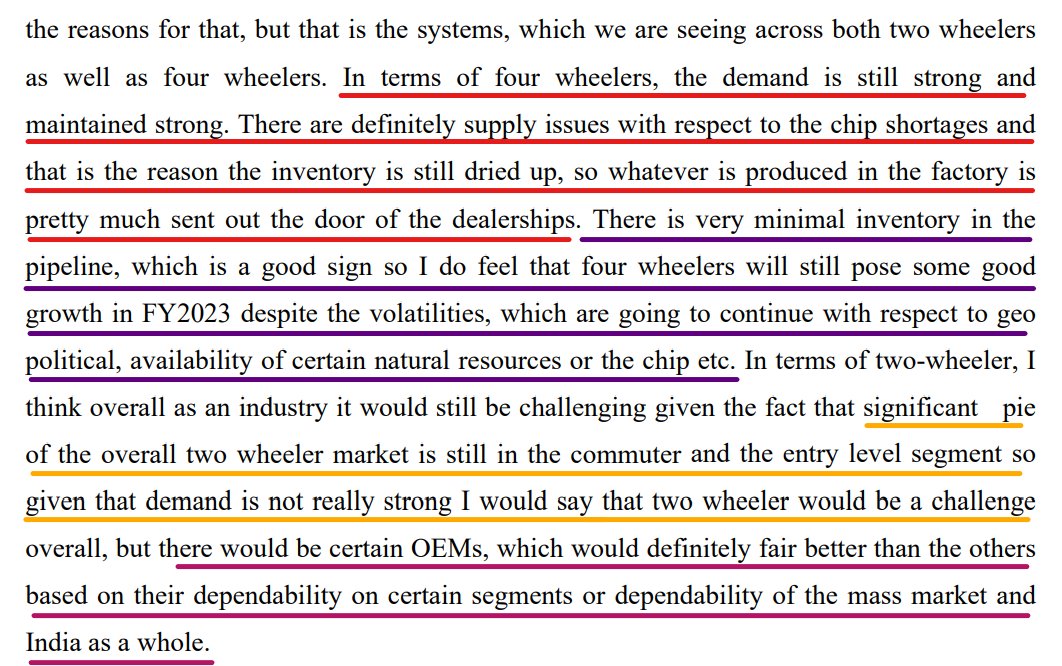

28/ From the Q4FY22 concall of another auto ancillary (Lumax Auto Tech)

4Ws demand is robust & inventories are at an all-time low & will benefit as soon as the supply chain normalizes; similarly in premium 2Ws, the commuter 2W segment still needs to see a sustained recovery 🚀

4Ws demand is robust & inventories are at an all-time low & will benefit as soon as the supply chain normalizes; similarly in premium 2Ws, the commuter 2W segment still needs to see a sustained recovery 🚀

29/ An inspiring speech by Mr. Jayant Davar on his journey, entrepreneurship, importance of practical experience & how they formed the strategy in the initial days of Sandhar. (Recommended at 1.5x)

m.youtube.com

m.youtube.com

Loading suggestions...