QSR Wars: Devyani vs Sapphire - A mini thread

We know that Devyani & Sapphire operate KFC & Pizza Hut in India & couple of Intl sites.

This thread aims to give a perspective of how they stack up against each other.

1/n

We know that Devyani & Sapphire operate KFC & Pizza Hut in India & couple of Intl sites.

This thread aims to give a perspective of how they stack up against each other.

1/n

Of course, additionally, Devyani operates Coasta & Vaango and Sapphire operates Taco Bell.

As I was studying different reports, I did see data discrepancies & I did my best to present as accurate picture as I can but if you find any discrepancies, my apologies upfront.

2/n

As I was studying different reports, I did see data discrepancies & I did my best to present as accurate picture as I can but if you find any discrepancies, my apologies upfront.

2/n

In this thread, we will compare Devyani and Sapphire

By Location

By Revenue & Margins trend

By Stores (Store growth, SSSG, Sales/store & EBITDA/store)

By Valuations

By Management capability

and also visualize how the future journey could be

3/n

By Location

By Revenue & Margins trend

By Stores (Store growth, SSSG, Sales/store & EBITDA/store)

By Valuations

By Management capability

and also visualize how the future journey could be

3/n

QSR Wars: Devyani vs Sapphire - A mini thread

Please don't forget to like and retweet if you enjoyed the presentation and the content

@soicfinance , @MeyyappanPl1, @suru27 - I understand you track QSR, so please do share any additional points that I may have missed.

4/n

Please don't forget to like and retweet if you enjoyed the presentation and the content

@soicfinance , @MeyyappanPl1, @suru27 - I understand you track QSR, so please do share any additional points that I may have missed.

4/n

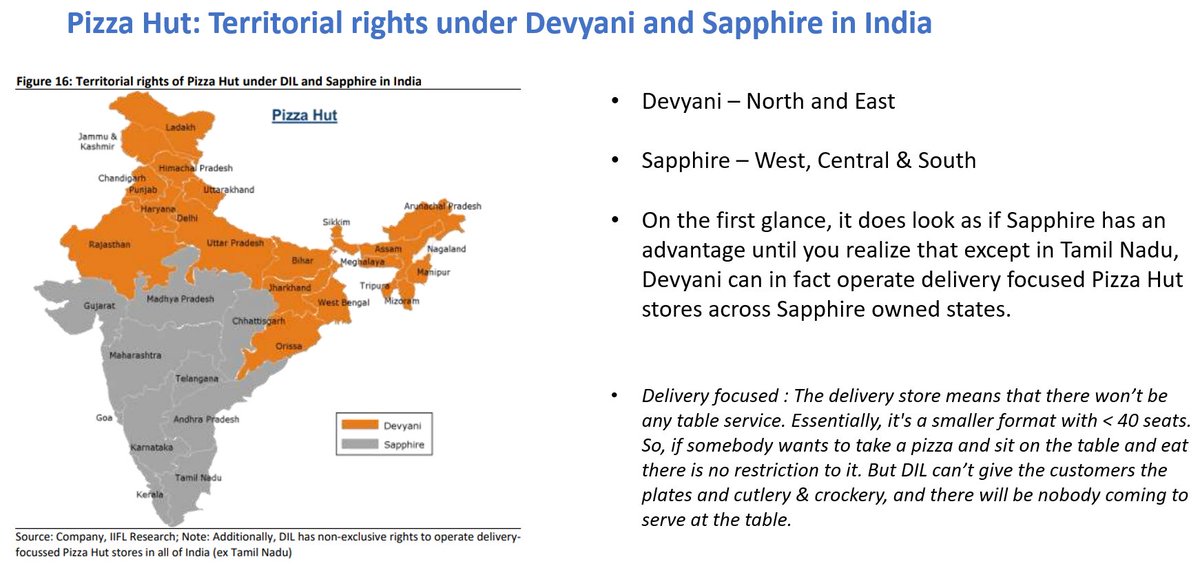

Location: Lets look at territorial rights of Pizza Hut under Devyani and Sapphire in India.

On the first glance, it does look as if Sapphire has an advantage but...look at the graphic

5/n

On the first glance, it does look as if Sapphire has an advantage but...look at the graphic

5/n

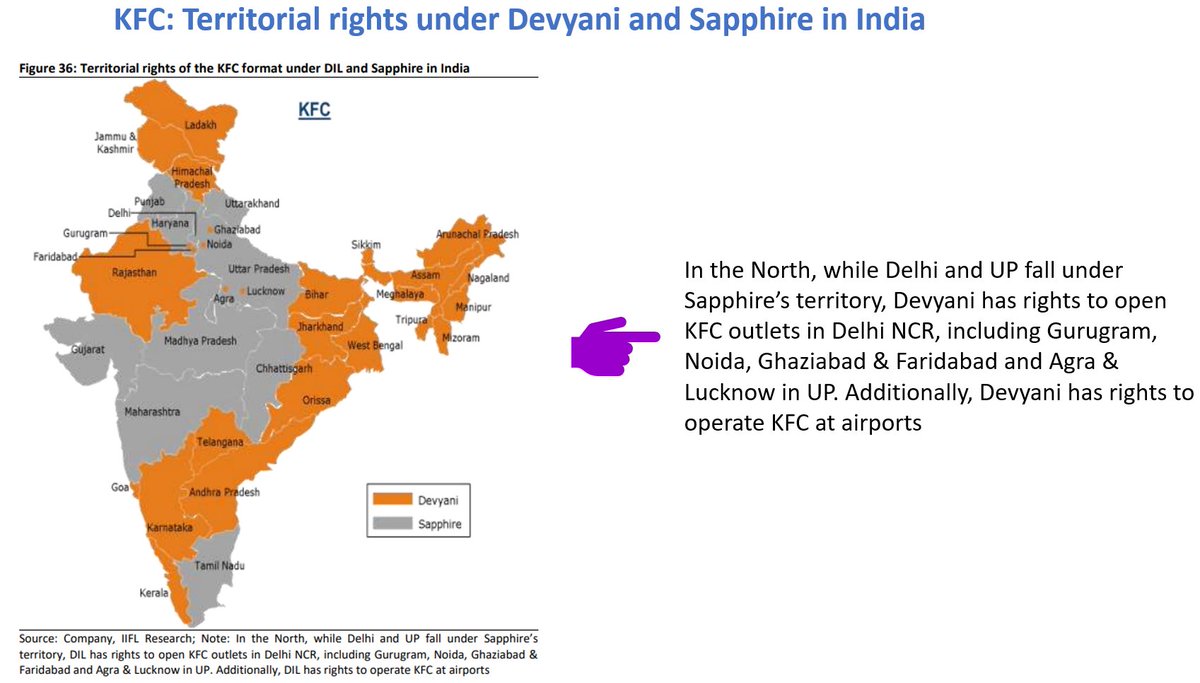

Location: Lets look at territorial rights of KFC under Devyani and Sapphire in India.

Sapphire does have an edge when it comes to metro cities

6/n

Sapphire does have an edge when it comes to metro cities

6/n

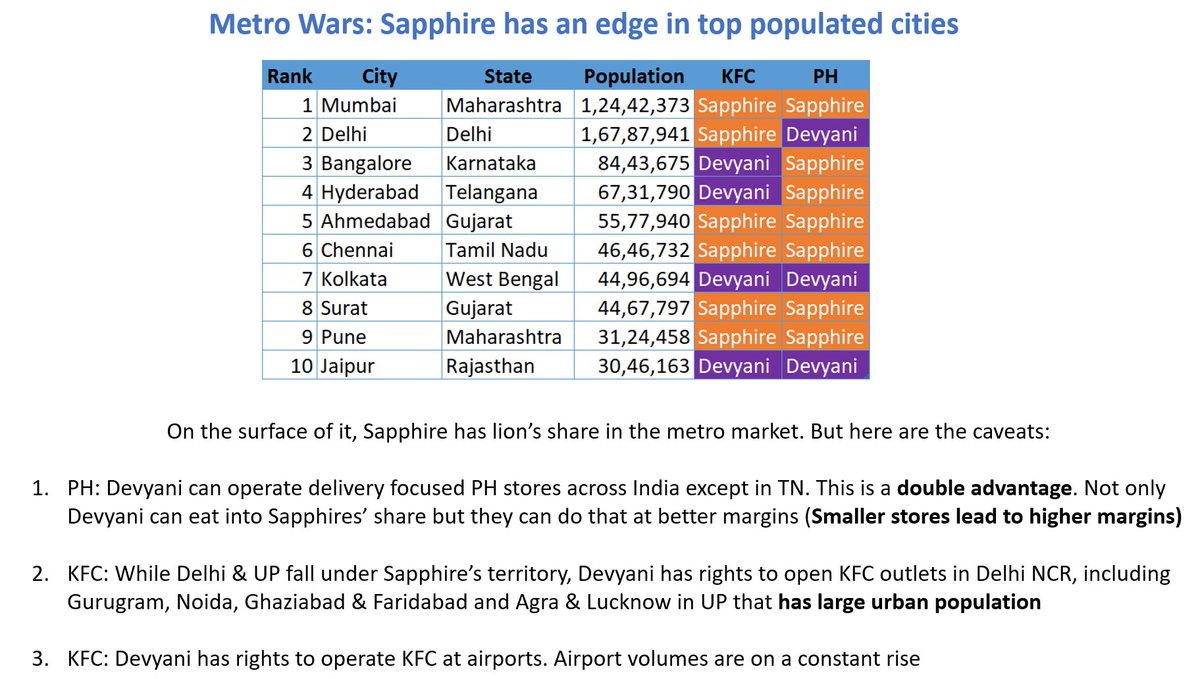

Location: Lets look at how Devyani and Sapphire control the top 10 populated cities.

Overall, Sapphire does have an edge with caveats

7/n

Overall, Sapphire does have an edge with caveats

7/n

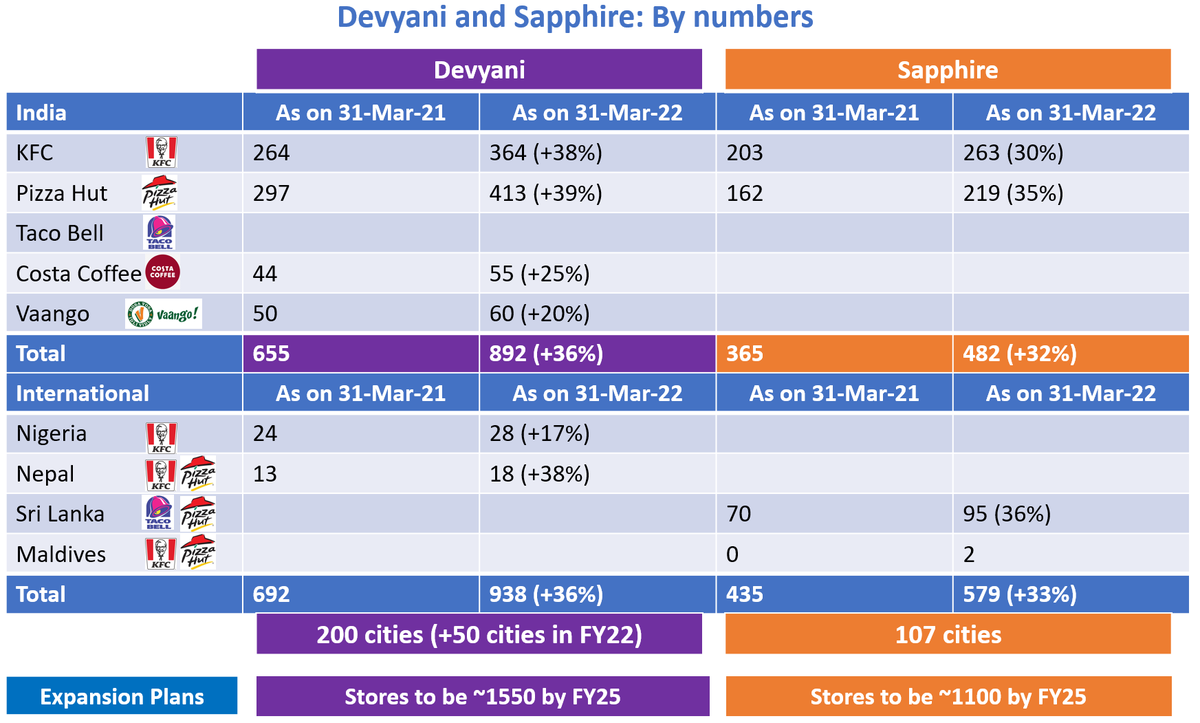

Location and growth: Lets look at the total picture.

Devyani is expanding much faster than Sapphire and they do have plans to open delivery focused PH stores in Sapphire territories

8/n

Devyani is expanding much faster than Sapphire and they do have plans to open delivery focused PH stores in Sapphire territories

8/n

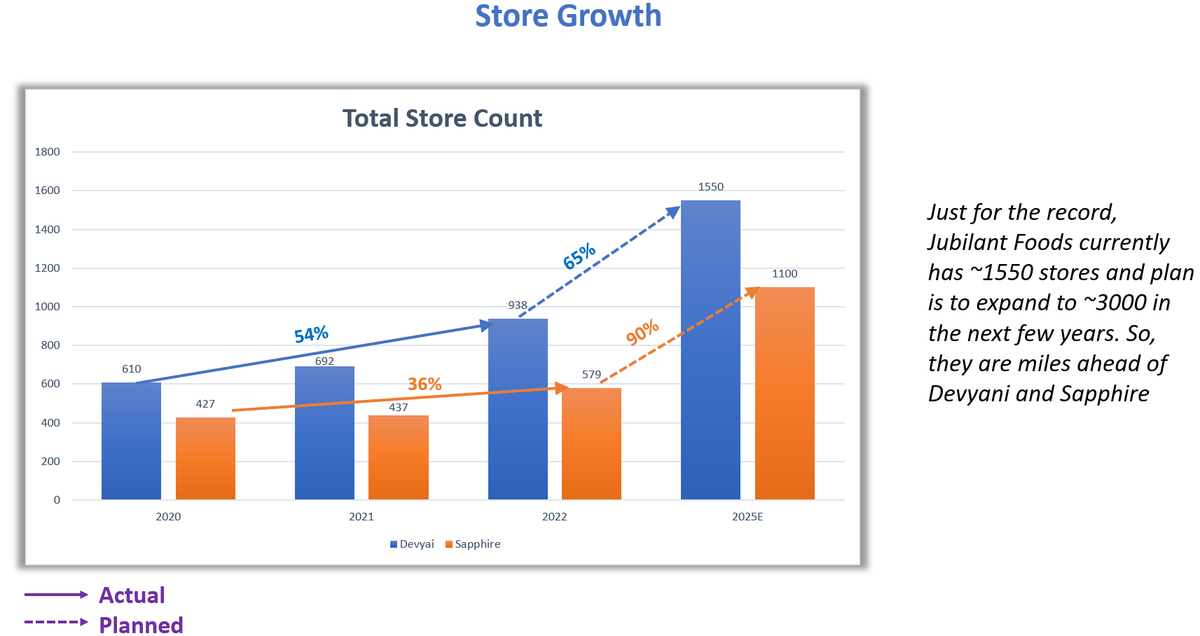

Store Growth: Lets see how the store growth has been taking place

Devyani: Plans to add 200 to 250 stores per year Sapphire: Be around 1100 in next 3-4 years

BTW, Jubilant Foods is way ahead of them!

9/n

Devyani: Plans to add 200 to 250 stores per year Sapphire: Be around 1100 in next 3-4 years

BTW, Jubilant Foods is way ahead of them!

9/n

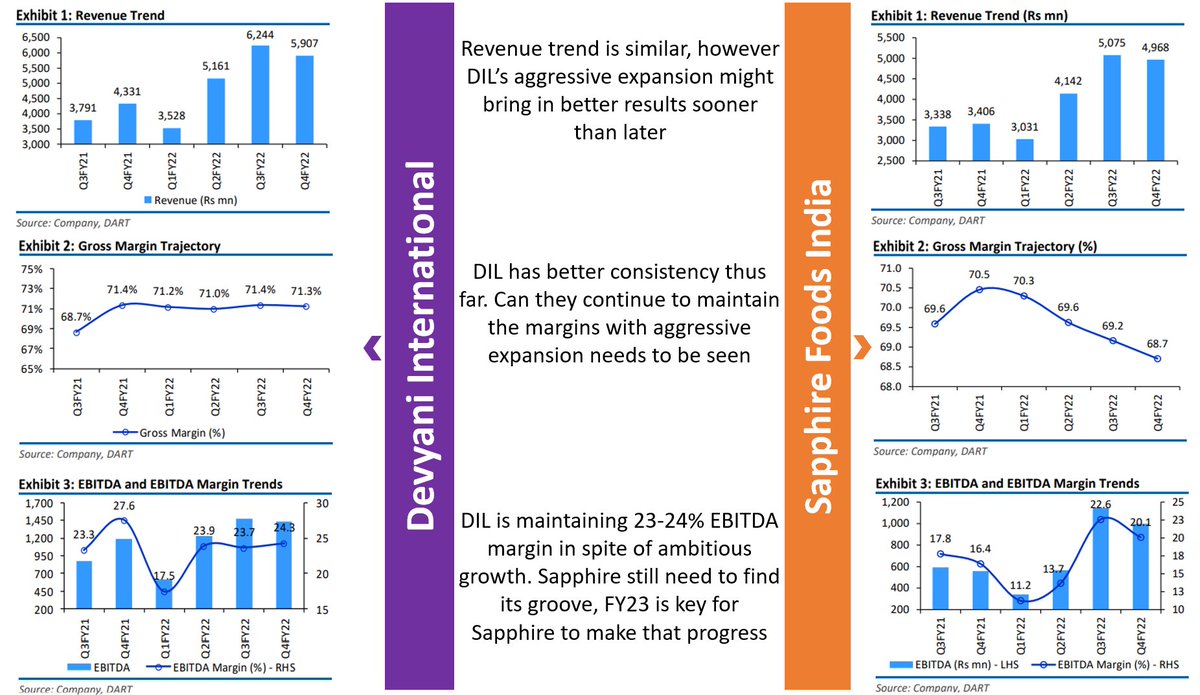

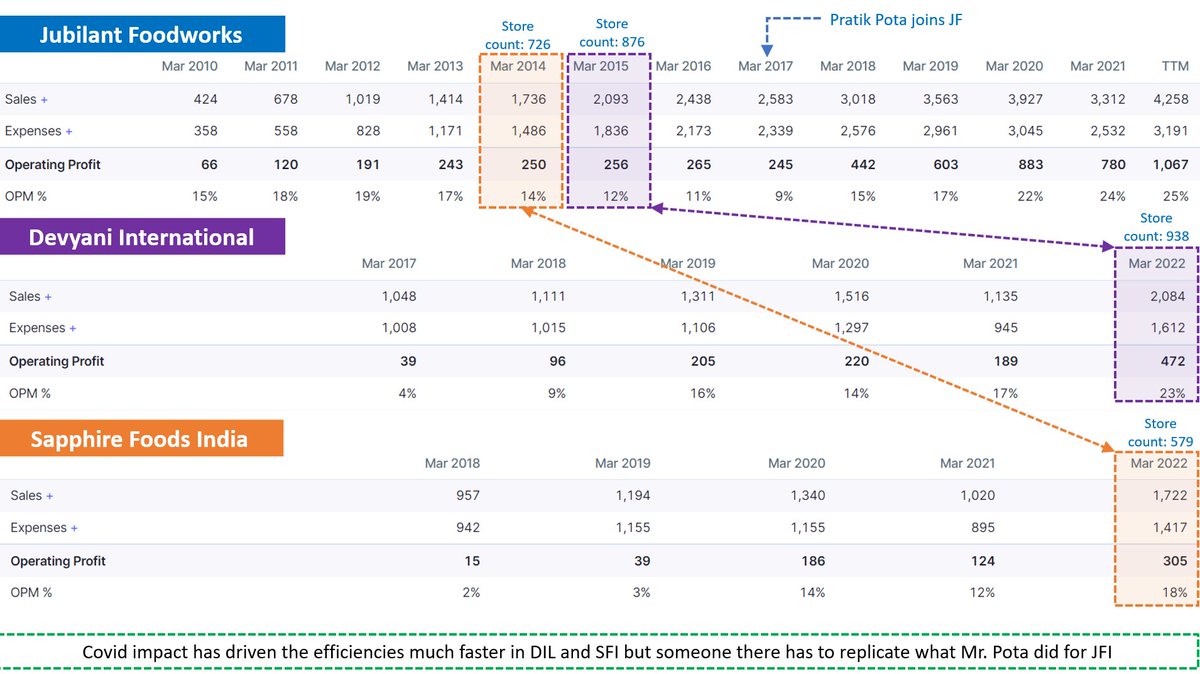

This graphic gives the trend of revenues, gross margins and EBITDA

As of now, Devyani has better consistency in margins than Sapphire even though both are opening the net new stores rapidly

10/n

As of now, Devyani has better consistency in margins than Sapphire even though both are opening the net new stores rapidly

10/n

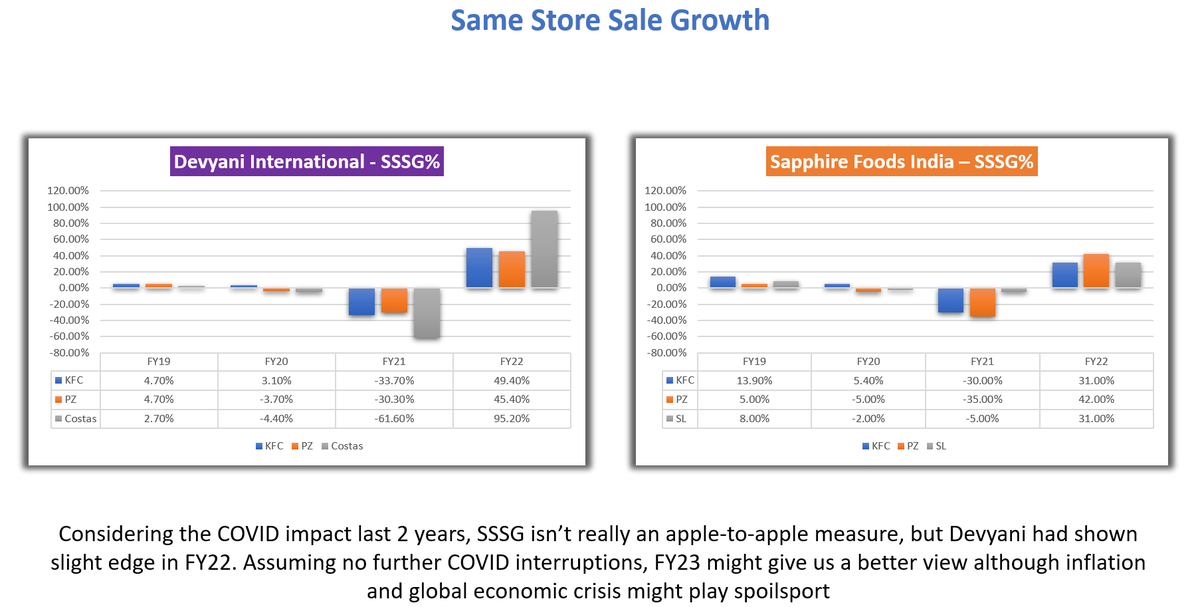

SSSG%: With COVID spoiling the party for QSRs, SSSG isn’t really an apple-to-apple metric but the graphic below can give you some perspective.

Devyani seems to be doing better but FY23 might present us better picture to compare with a good base now

11/n

Devyani seems to be doing better but FY23 might present us better picture to compare with a good base now

11/n

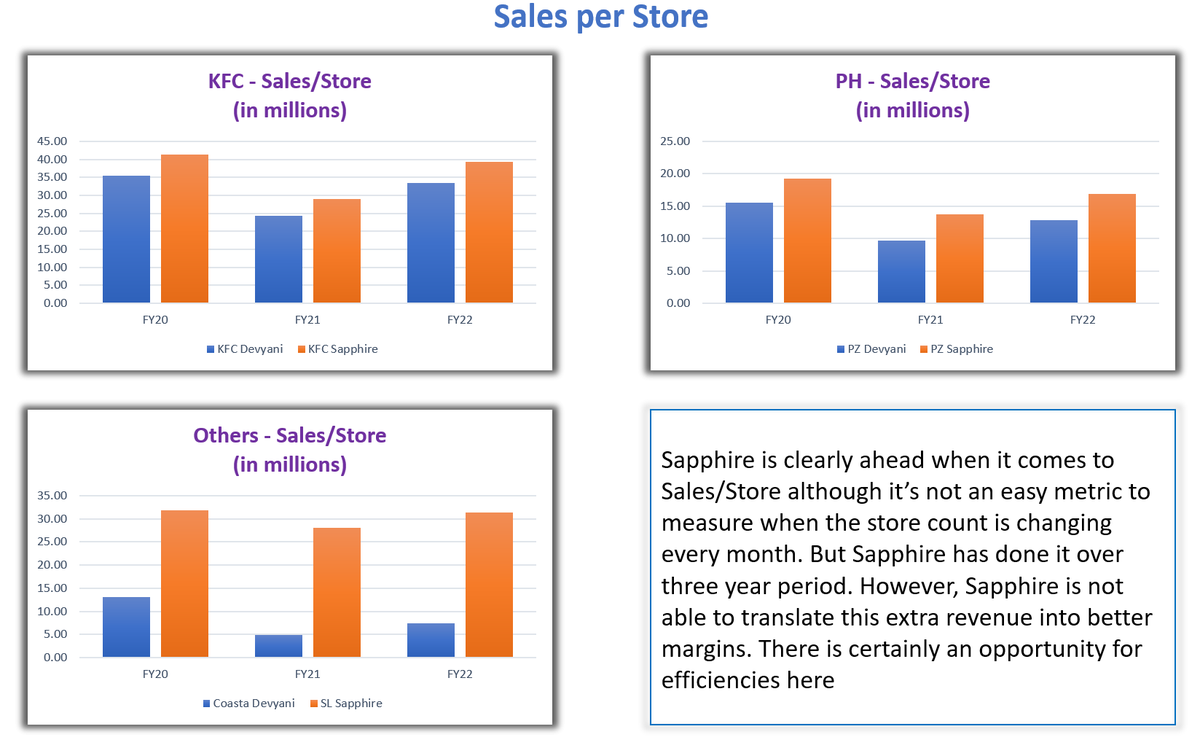

Sales per Store: Sapphire is clearly ahead of Devyani but somewhere it’s also taking a toll on expenses and thus not translating into higher OPM

12/n

12/n

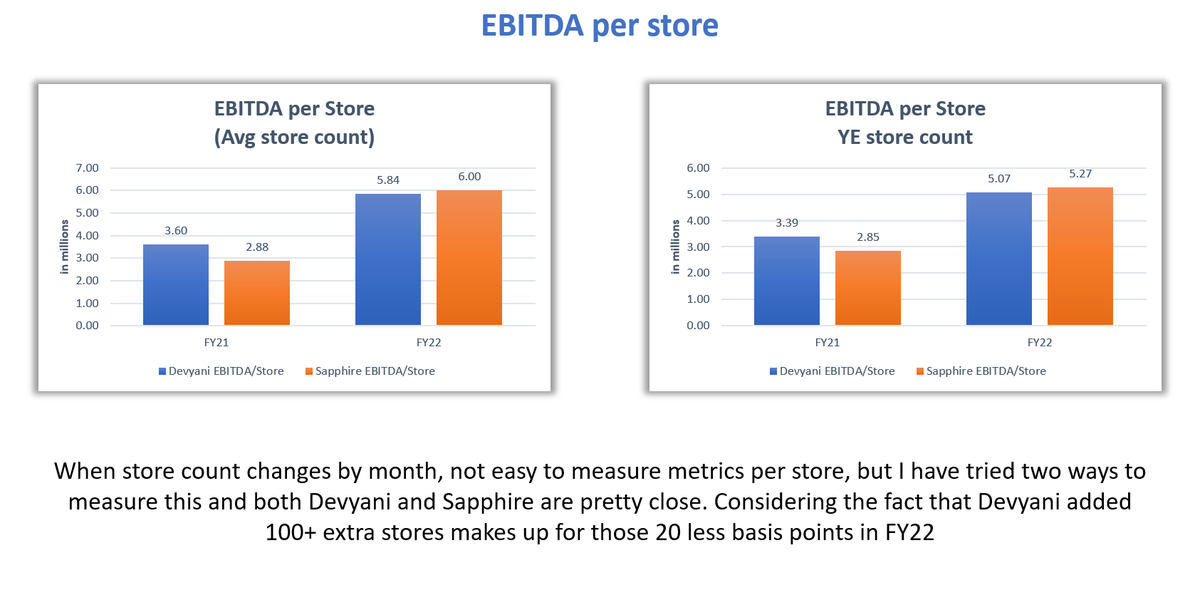

EBITDA per Store: They are in similar neighborhood but the reality is, calculating any per store metric isn’t easy when # of stores keep changing each month.

Hence, pls take this data with a pinch of salt

13/n

Hence, pls take this data with a pinch of salt

13/n

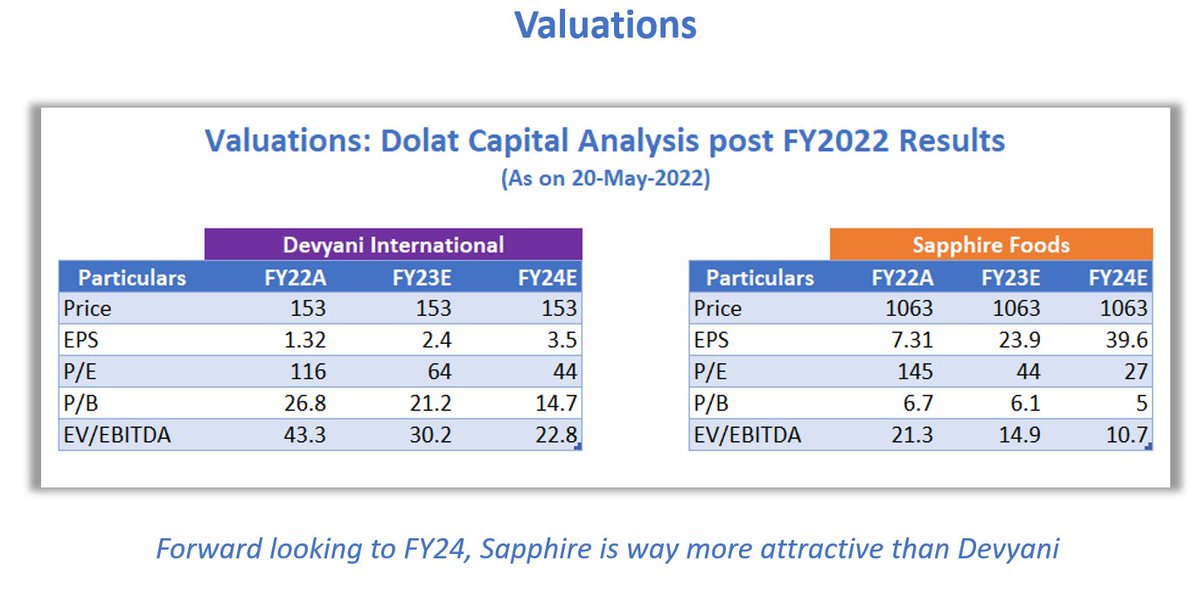

Valuations: Sapphire is clearly more attractive than Devyani at FY24 valuations.

Sri Lankas has given better margins than Indian businesses for Sapphire & if SL takes any hit in FY23, that might spoil the valuations for Sapphire but otherwise Sapphire clearly offers value

14/n

Sri Lankas has given better margins than Indian businesses for Sapphire & if SL takes any hit in FY23, that might spoil the valuations for Sapphire but otherwise Sapphire clearly offers value

14/n

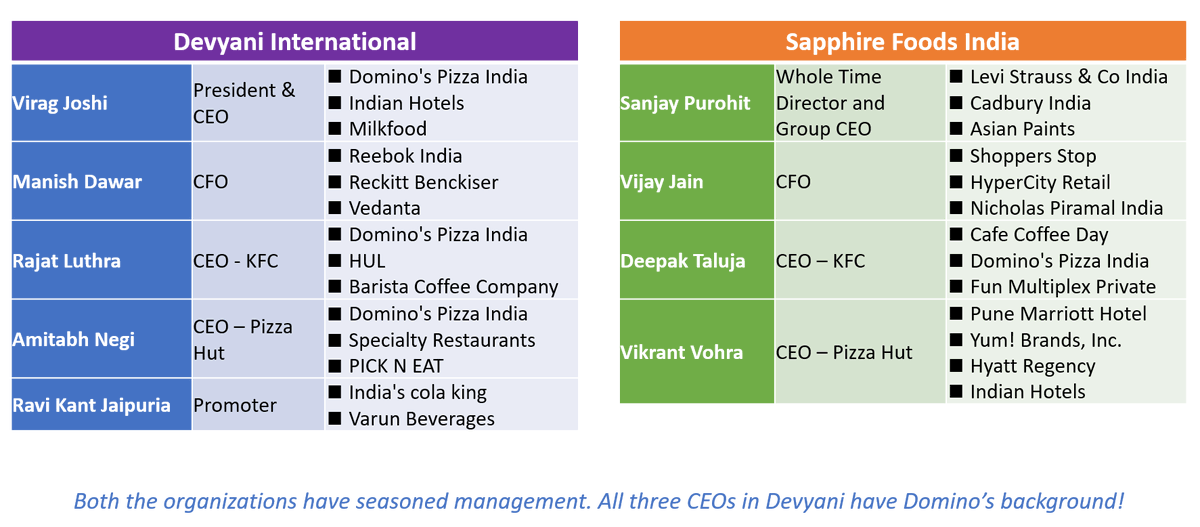

Management: Both the organizations have seasoned management. All three CEOs in Devyani have Domino’s background!

Mr. Jaipuria might offer slight edge to Devyani.

15/n

Mr. Jaipuria might offer slight edge to Devyani.

15/n

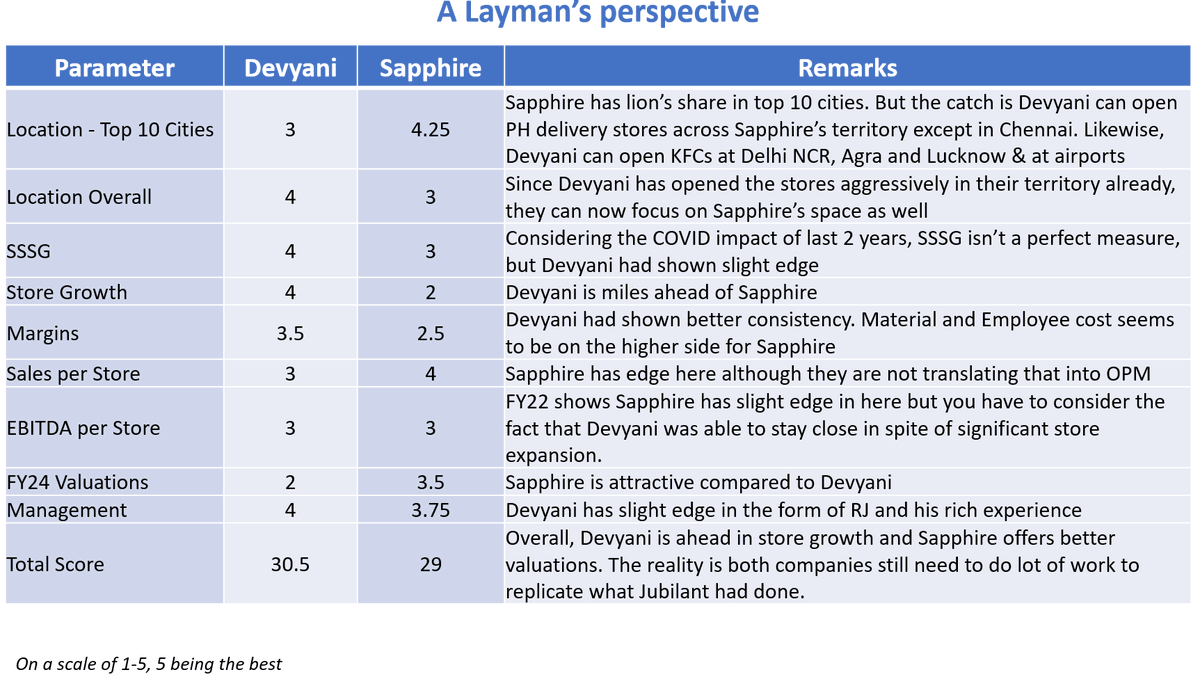

Lets look at the summary of these data points in a single view. I am not an expert so, just treat this as a layman’s view!

16/n

16/n

QSR has a huge runway, the graphic below can help you understand what could be the road ahead for both Devyani & Sapphire.

IMO, both have great opportunities but at the same time Jubilant is still continuing it’s expansion so competition won't be easy

17/n

IMO, both have great opportunities but at the same time Jubilant is still continuing it’s expansion so competition won't be easy

17/n

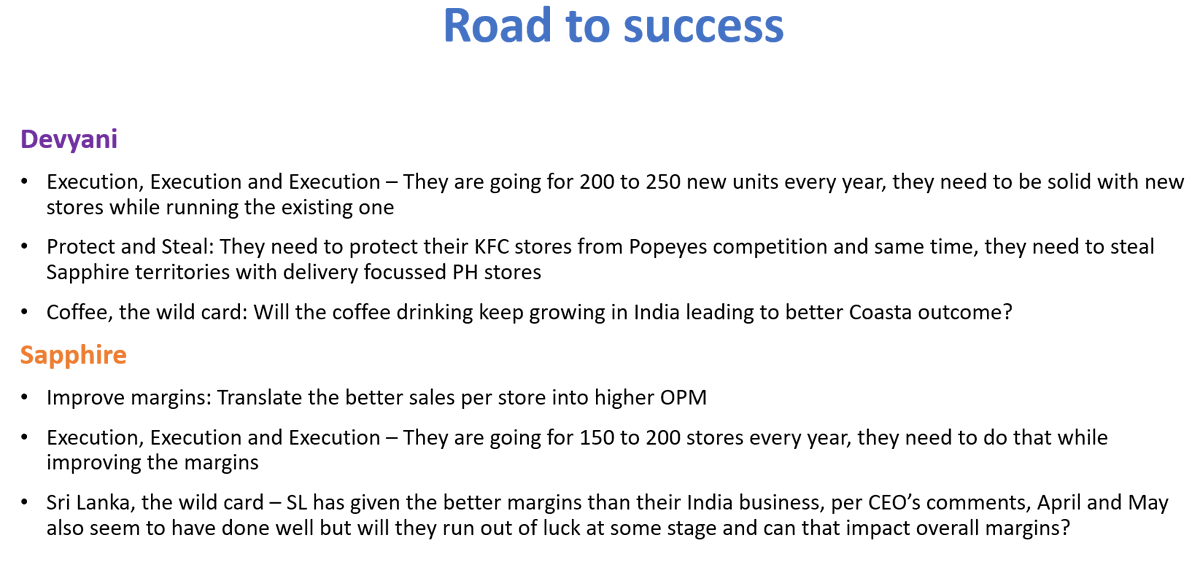

Road to Success: See the graphic for detailed commentary

Devyani

1. Execution

2. Protect and Steal

3. Coffee, the wild card

Sapphire

1. Improve OPM:

2. Execution

3. Sri Lanka, the wild card

18/n

Devyani

1. Execution

2. Protect and Steal

3. Coffee, the wild card

Sapphire

1. Improve OPM:

2. Execution

3. Sri Lanka, the wild card

18/n

At the end, I like both of them, they are ambitious, have manageable debt & have similar rental expenses.

I see them as young Tata Elxsi & LTTS of QSR. Barring a terrible recession, both should do well over the next few years

19/the end

Thank you for reading🙏

I see them as young Tata Elxsi & LTTS of QSR. Barring a terrible recession, both should do well over the next few years

19/the end

Thank you for reading🙏

Loading suggestions...