A thread on Krsnaa Q4 results & more importantly the investor presentation. Some really revealing 🔍 details this time.

🧵🧵⤵️

🧵🧵⤵️

To get started, one Can read my good friend @AnishA_Moonka 's thread to know more about biz:

What stands out in that 1 slide summary to you?

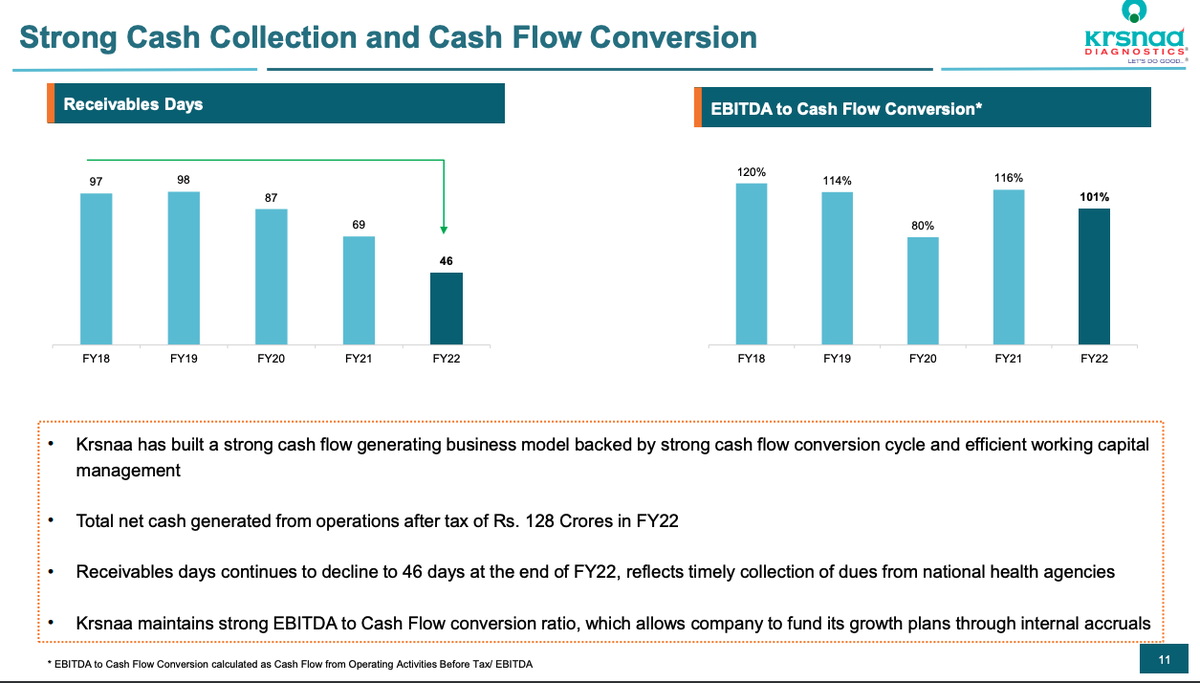

To me personally, it is the receivable days. For a B2G business, their balance sheet strength is commendable.

Another thing which stands out is opportunity size. 70 districts mei hain. India has 773

To me personally, it is the receivable days. For a B2G business, their balance sheet strength is commendable.

Another thing which stands out is opportunity size. 70 districts mei hain. India has 773

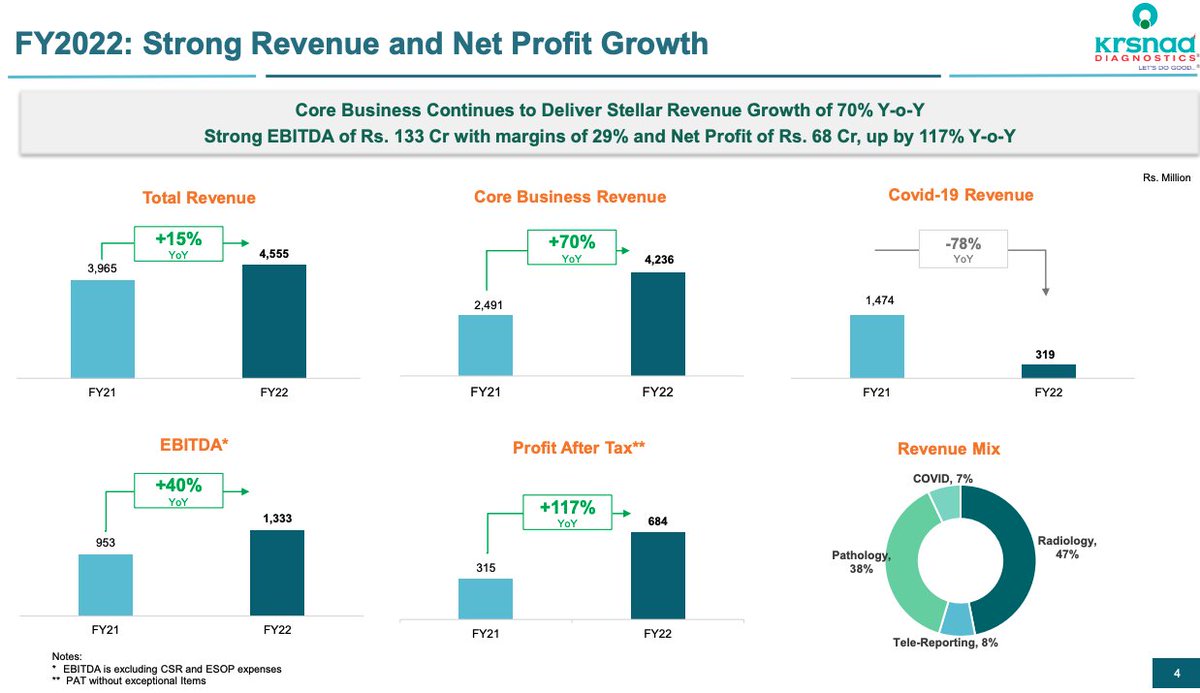

We can see that core revenue growth was masked by covid revenue degrowth. Q4 has 2% covid revenue so going forward base is 'pure' so core biz growth will come out & shine.

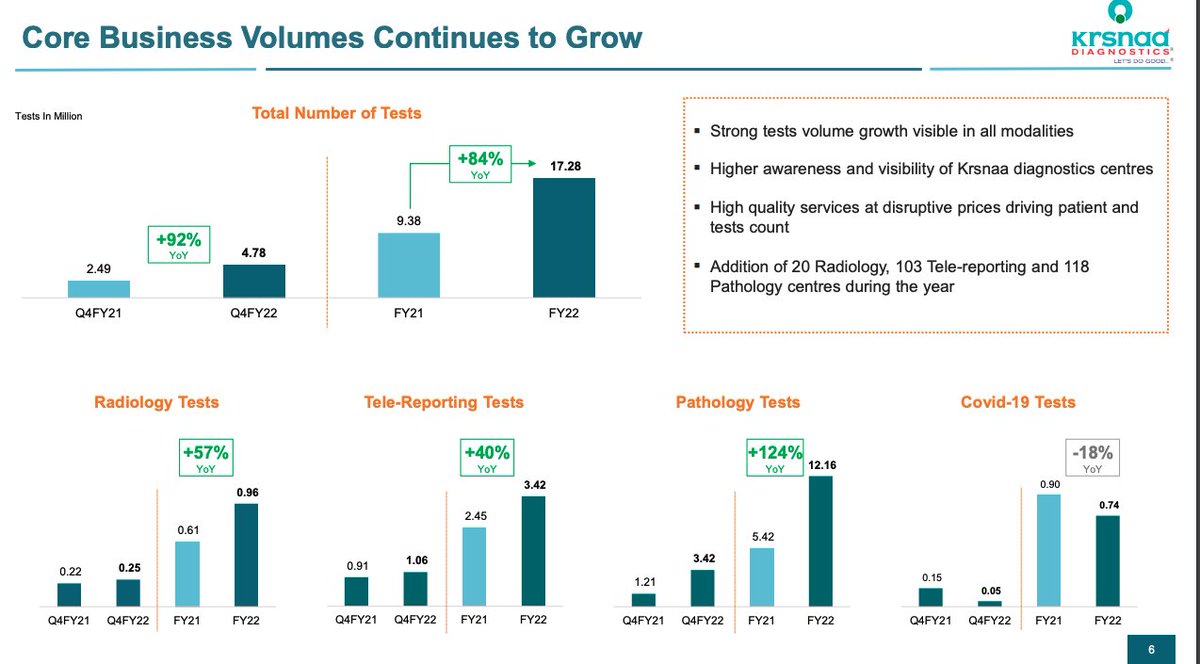

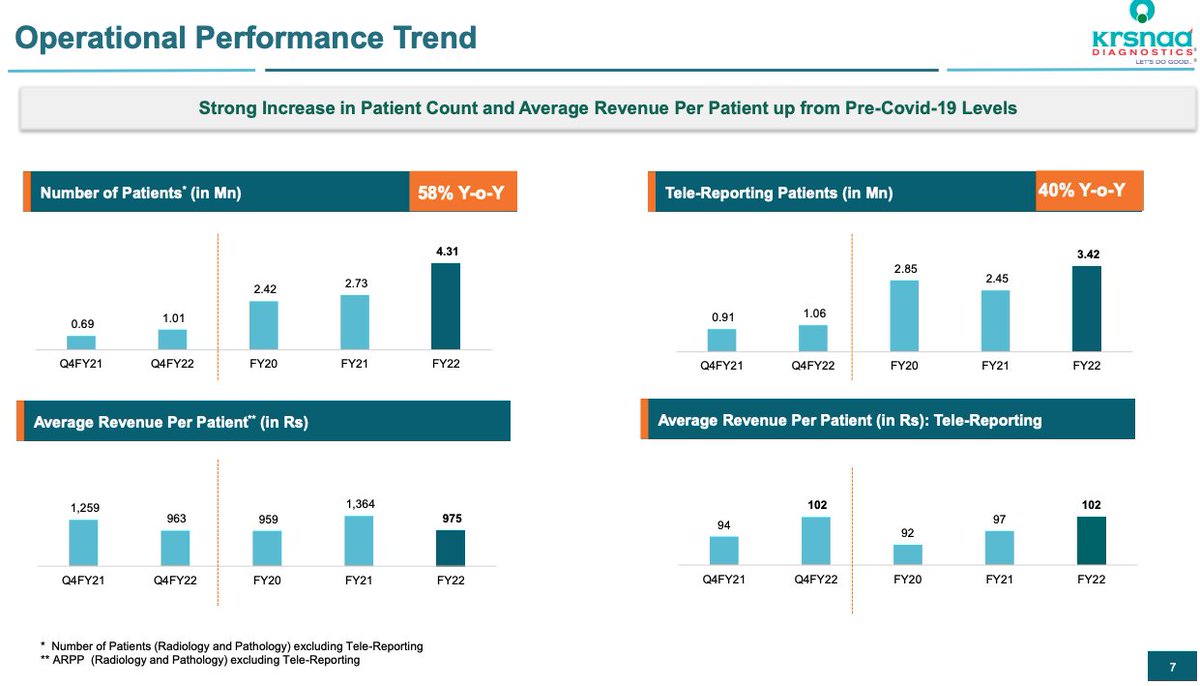

We can see average realisation has gone down.

Average pricing of radiology tests was 2600 in fy21. It was 2200 in FY22. And a bit lower in Q4FY22. THis could very well be due to the product mix being in favor of lower value tests.

Average pricing of radiology tests was 2600 in fy21. It was 2200 in FY22. And a bit lower in Q4FY22. THis could very well be due to the product mix being in favor of lower value tests.

This is also visible in ARPP going down. Need to confirm in concall why product mix has gone to lower value tests.

A lot of anti-thesis for krsnaa is due to B2G nature. However, this has NOT turned up in balance sheet & cashflows which remain healthy. In fact receivable days have gone down. With higher % of mix coming from private in future, this will only improve.

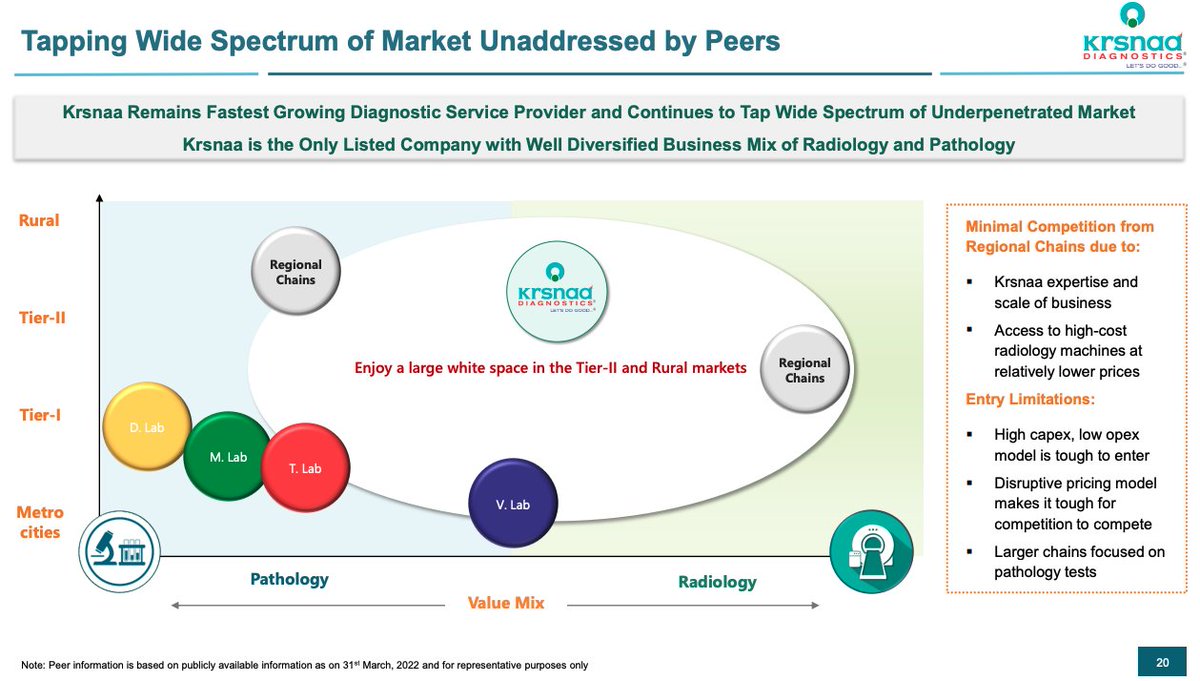

No better way to visually represent krsnaa addressable market than this slide. Well positioned in terms of mix of radiology & pathology. Tier 3/2 remain very under-penetrated.

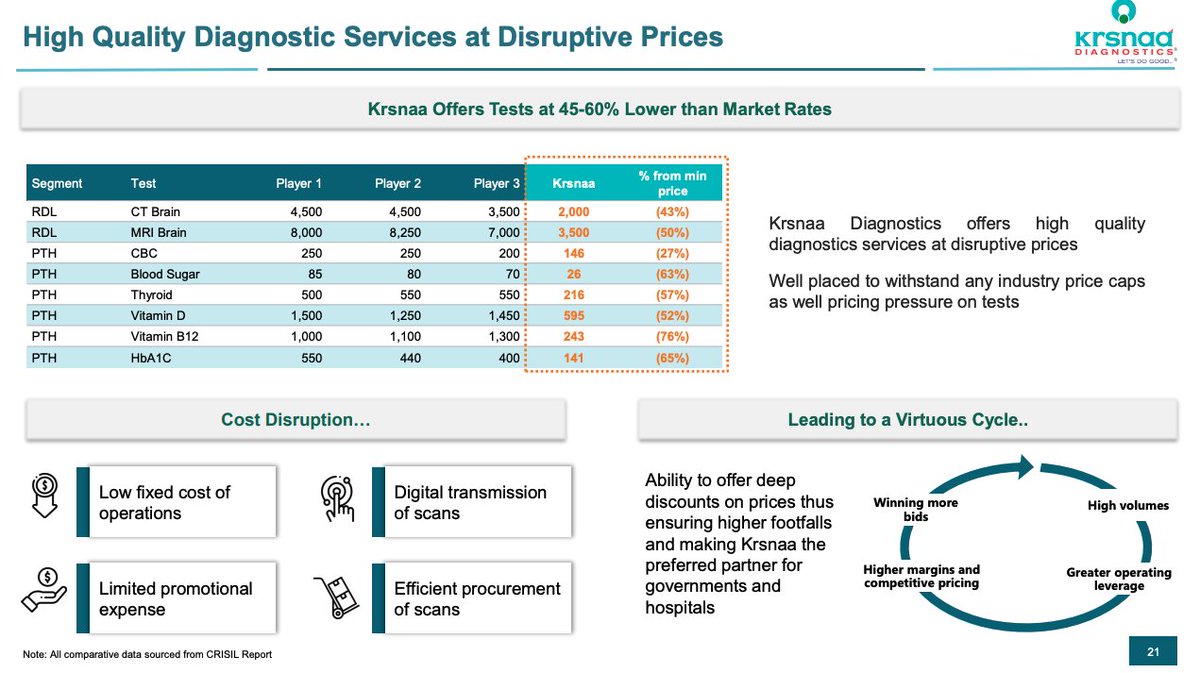

If diagnostics is a commoditised service (Many would debate that) lowest cost producer has a very large advantage. Krsnaa is that player.

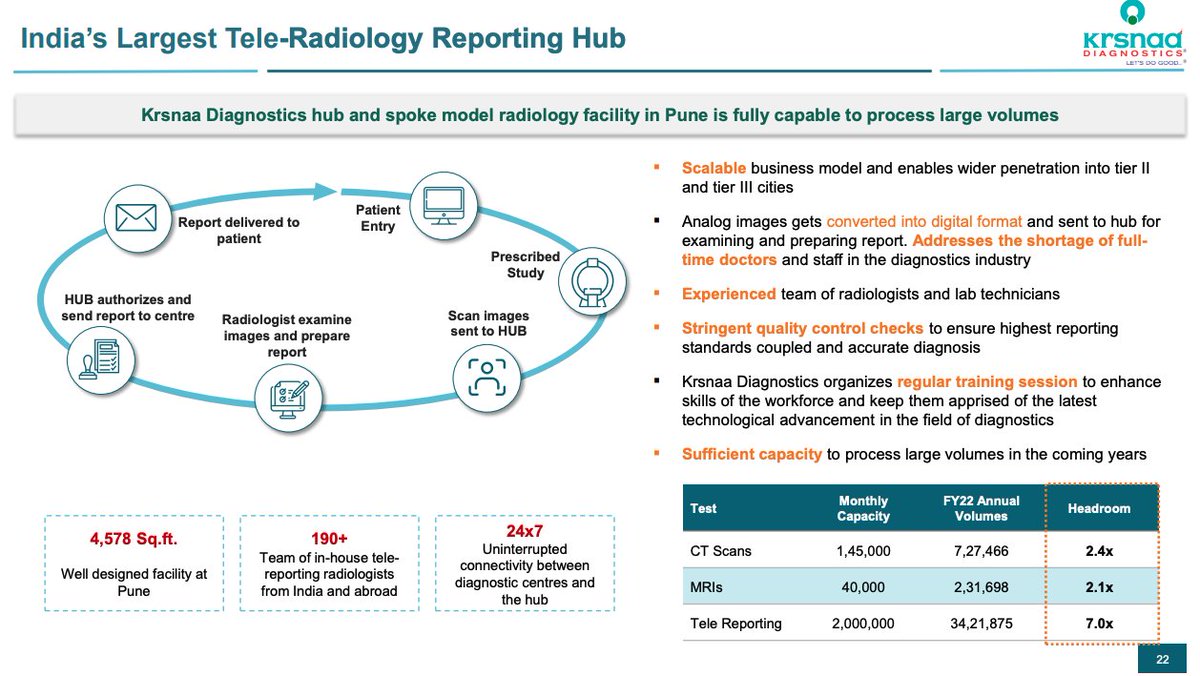

The capacities are significantly under-utilised showing us a fairly large headroom for operating leverage (as capacity utilisation goes up).

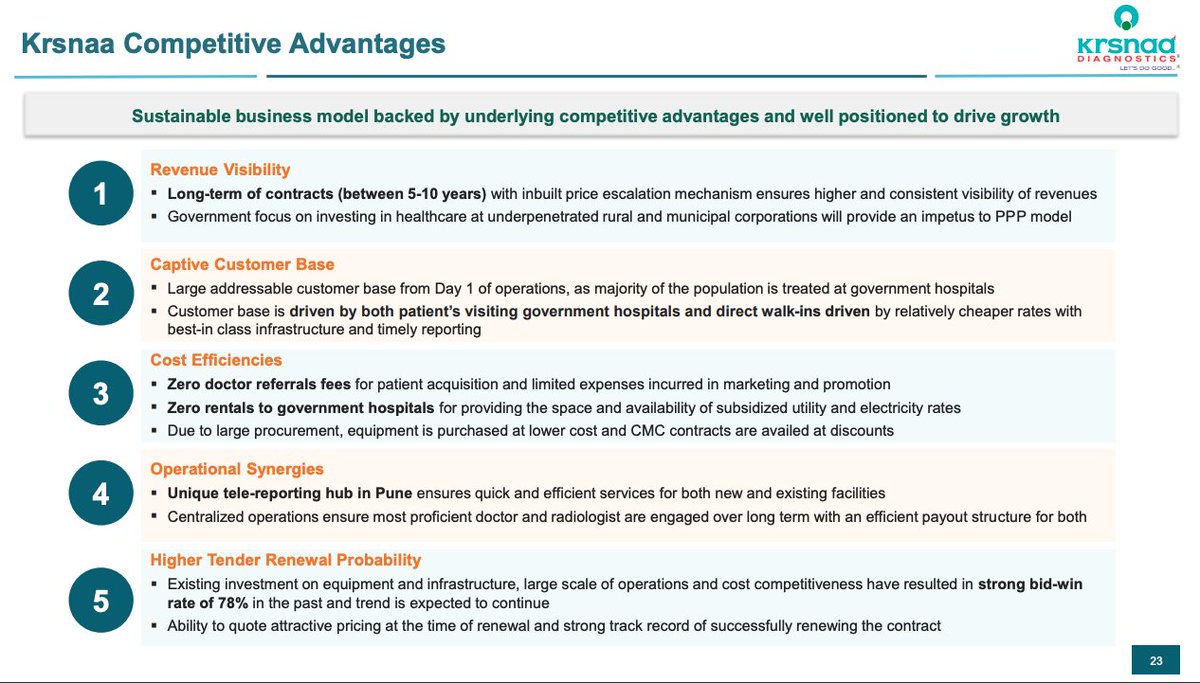

All the competitive advantages summed up in 1 slide. Long term contracts, captive customer base, low cost of ops due to govt labs, economies of scale in procuring equipment. This is text book consolidation of unorganised radiology. High tender renewal rate.

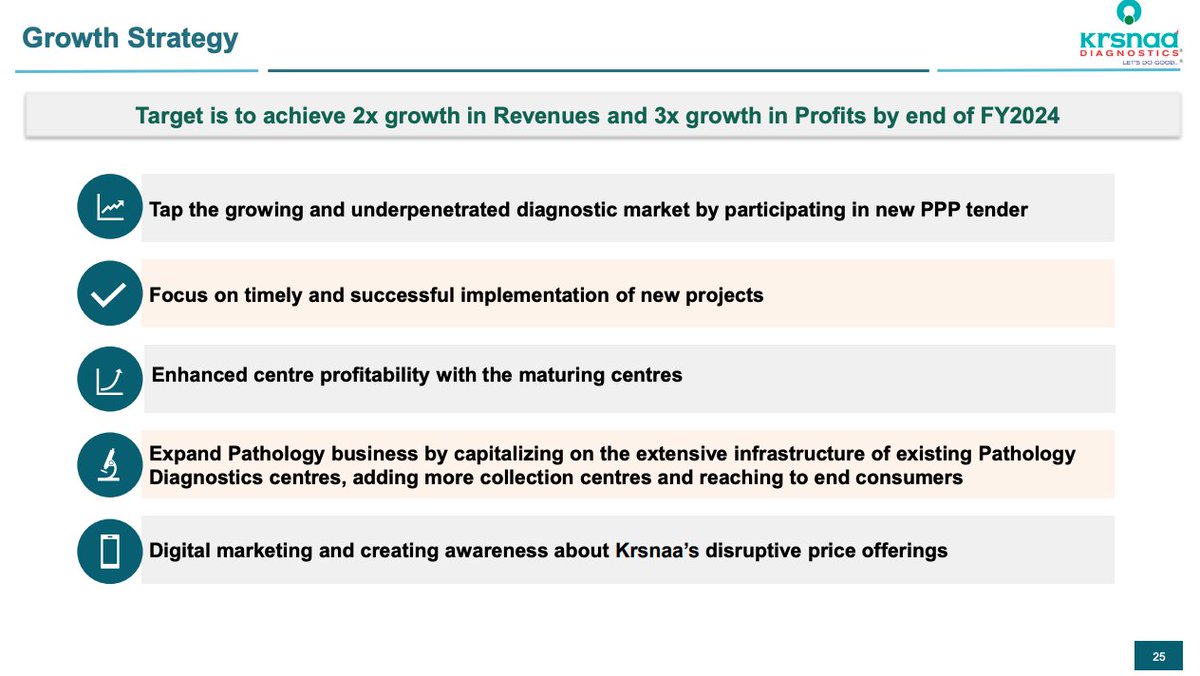

KRSNAA plans to grow revenue 2x & profits 3x in next 2 years (FY23 & FY24). Margin expansion & revenue growth. Sweet.

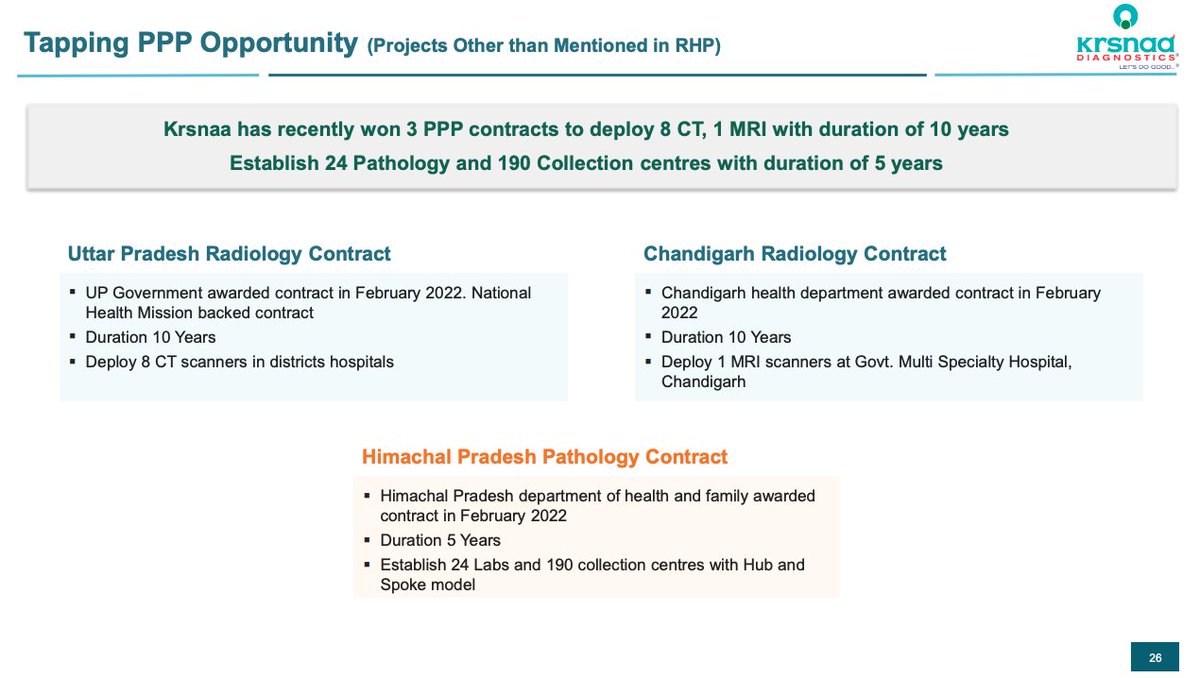

We can see concrete green shoots for how FY24 growth will be realized as well in terms of recent PPP contract wins (older contracts still being executed in punjab)

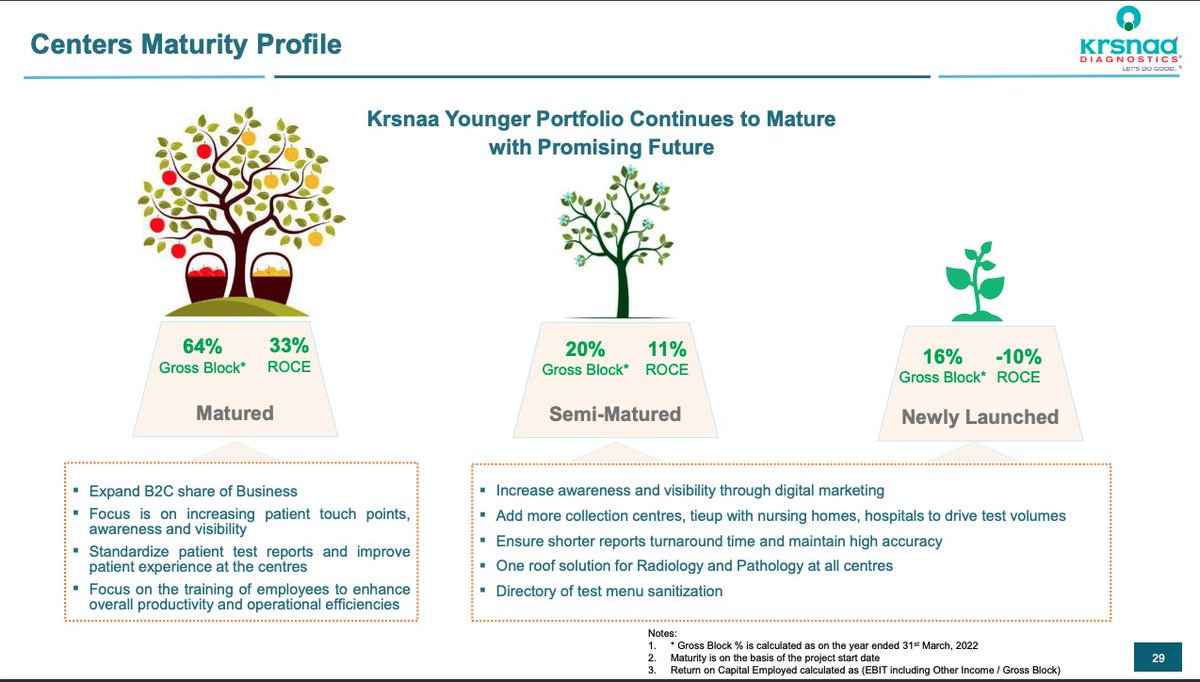

We also get to know the unit economics of the mature centers for 1st time. 33% ROCE is not bad, is it? That is where krsnaa ROCE is headed in medium term (once aggressive growth stops. But who wants it to stop?)

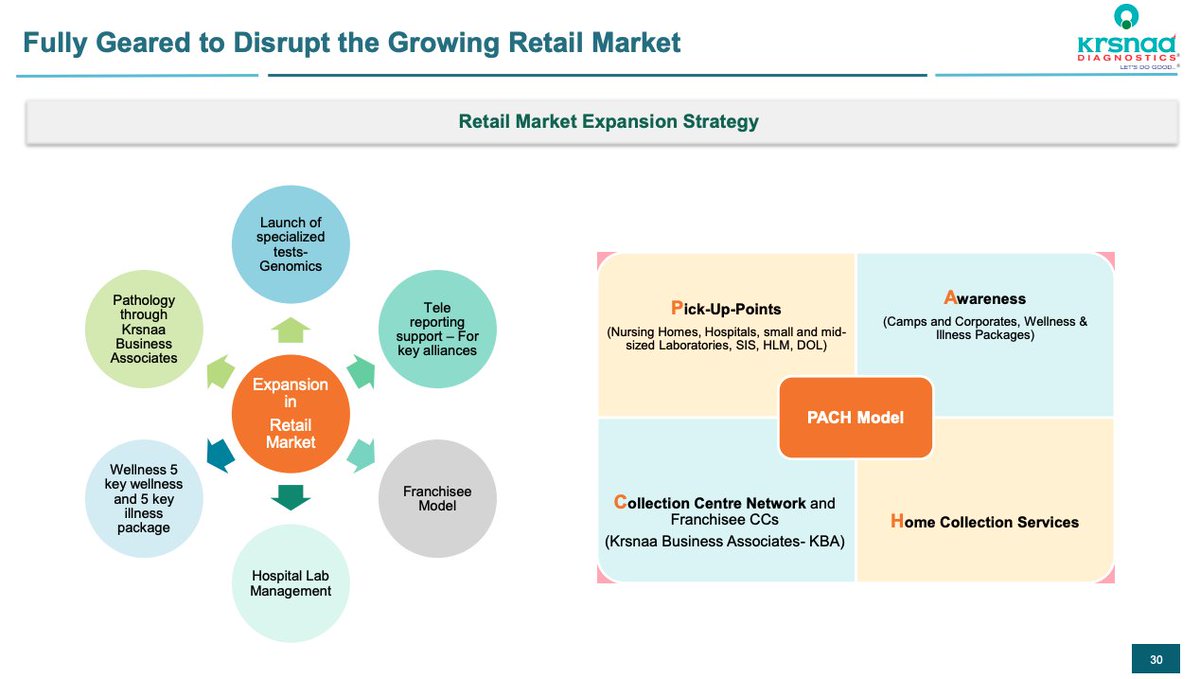

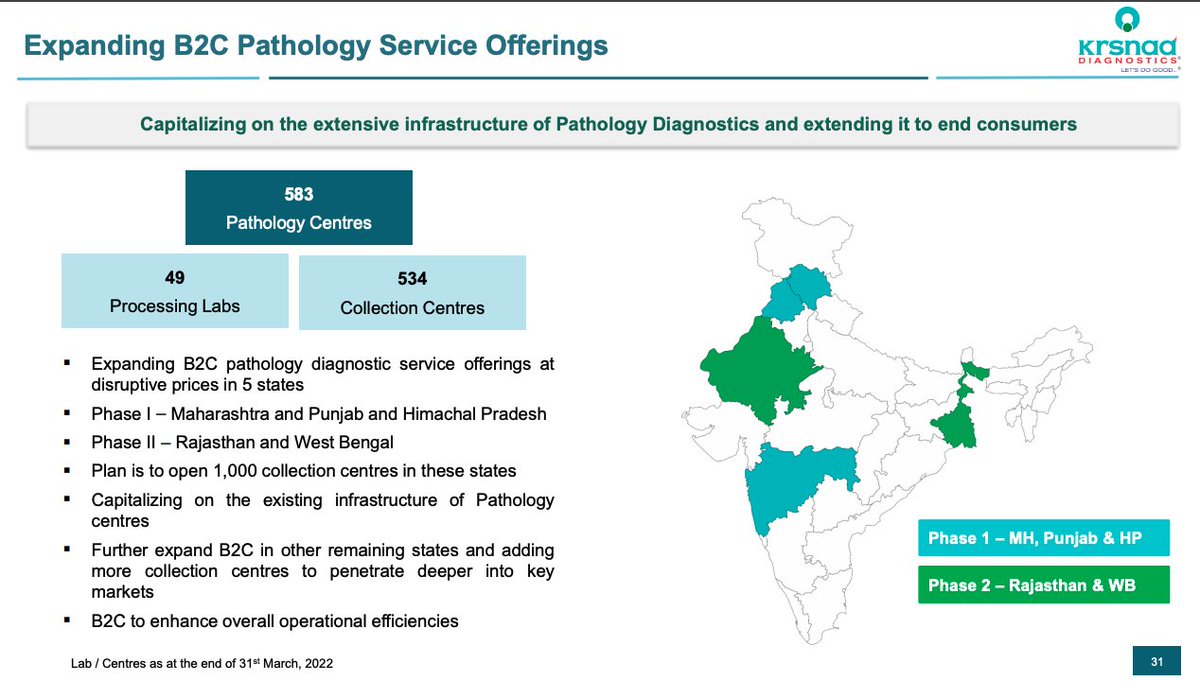

Krsnaa is also planning to leverage its existing pathology lab centers by expanding into B2C. due to the better costing, they will be able to grab market share away from incumbents in many cases.

Since its my thread, also adding some risks (not there in presentation).

1. This is 50% a B2G business so the risks associated with B2G are still there. Bad receivables, delayed receivables. Clear anti-thesis pointer.

1. This is 50% a B2G business so the risks associated with B2G are still there. Bad receivables, delayed receivables. Clear anti-thesis pointer.

2. The tenders awarded by government can be rescinded as well. There is an aspect of variability in B2G businesses due to politics. Will next government continue current tender? Until now, krsnaa has majorly managed to stay out of such trouble. Still something to be aware of.

3. Pathology part of diagnostics is seeing increased competition which can put pressure on prices. However, i believe this could impact krsnaa positively due to lower cost structure.

4. New IPO. COuld there have been any window dressing? We will find out with time.

Do your own due diligence. I am invested so of course biased. this is not a buy or sell reco. Your risk capital. Your gains. Your losses.

Loading suggestions...