Tata Elxsi should be a business case study in B-Schools

In 2018:-

The company faced massive problems,the stock corrected by 50%

2021:-

The business+the stock have been on a massive up move.

A thread🧵on how the company forged a turnaround in business

Lets go👇

(1/14)

In 2018:-

The company faced massive problems,the stock corrected by 50%

2021:-

The business+the stock have been on a massive up move.

A thread🧵on how the company forged a turnaround in business

Lets go👇

(1/14)

What is the business of Tata Elxsi?

The company operates in the following segments

1. Software Development & Services

Subdivisions here are:-

Embedded Product Design (EPD)

Industrial Design & Visualisation (IDV) division

2. System Integration & Support (SIS)

(2/14)

The company operates in the following segments

1. Software Development & Services

Subdivisions here are:-

Embedded Product Design (EPD)

Industrial Design & Visualisation (IDV) division

2. System Integration & Support (SIS)

(2/14)

The company operates in the following businesses

1. Automotive

2. Broadcast & Communications

3. Healthcare

(3/14)

1. Automotive

2. Broadcast & Communications

3. Healthcare

(3/14)

Problems in 2018:-

The company had nearly 40% of its revenue coming from the JLR business

Due to Brexit and the auto industry slowdown, many discretionary projects were postponed.

This Hurt the company pretty badly in terms of growth.

(4/14)

The company had nearly 40% of its revenue coming from the JLR business

Due to Brexit and the auto industry slowdown, many discretionary projects were postponed.

This Hurt the company pretty badly in terms of growth.

(4/14)

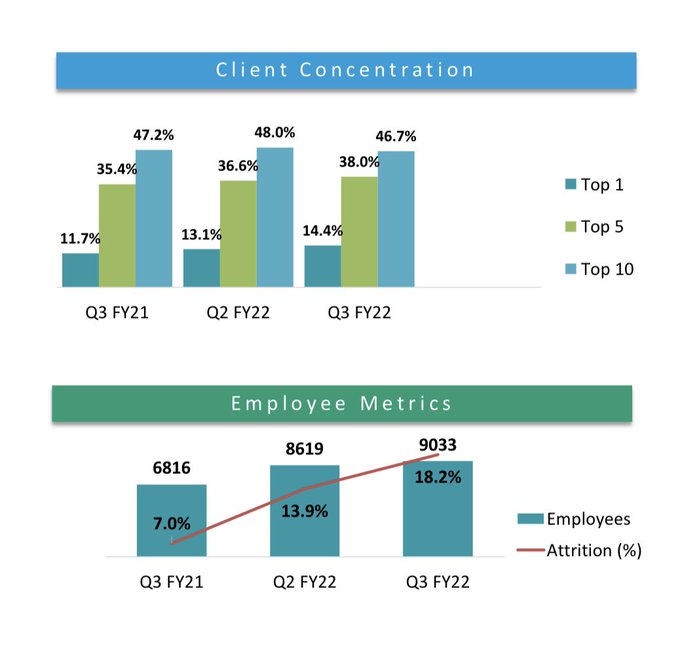

How did the company tackle this?

In 2018 the company decided to diversify away from JLR.

The company began working with other OEMs+ diversifying its business line as well.

As a result of this the client concentration has come down+a more diversified business is seen.

(5/14)

In 2018 the company decided to diversify away from JLR.

The company began working with other OEMs+ diversifying its business line as well.

As a result of this the client concentration has come down+a more diversified business is seen.

(5/14)

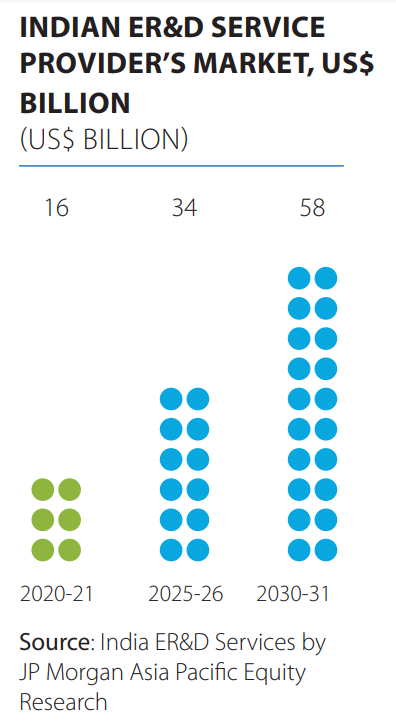

The massive potential of the ER&D business:-

The Engineering Research and Development Business is set to grow nearly 4x in the next 10 years.

Tata Elxsi mainly operates in this business.

(6/14)

The Engineering Research and Development Business is set to grow nearly 4x in the next 10 years.

Tata Elxsi mainly operates in this business.

(6/14)

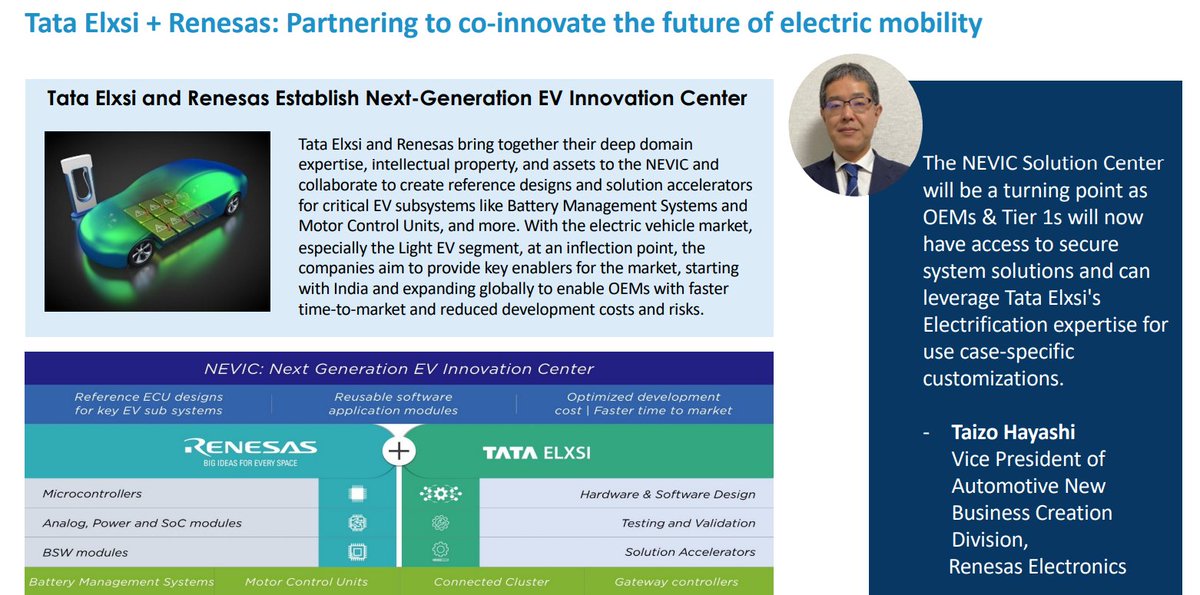

EV centered products:-

Tata Elxsi is developing products for EVs like Battery Management systems and Motor controllers which will be essential to the function of the vehicle.

These avenues have massive potential for the company.

(7/14)

Tata Elxsi is developing products for EVs like Battery Management systems and Motor controllers which will be essential to the function of the vehicle.

These avenues have massive potential for the company.

(7/14)

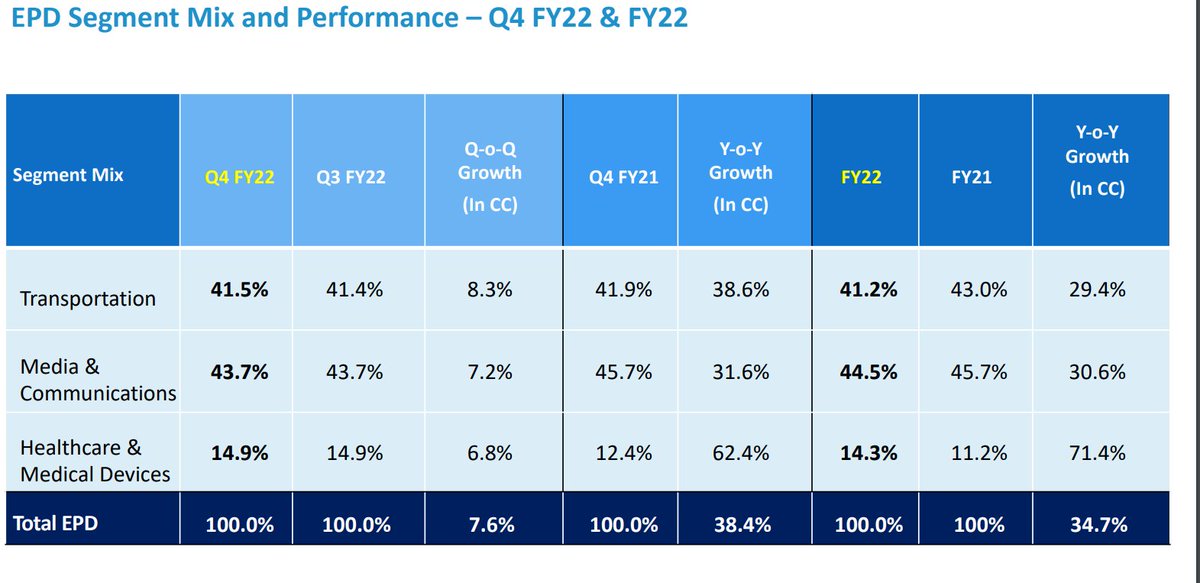

The spectacular rise of the Healthcare division:-

The healthcare business grew upwards of 70% YoY

This was supported by demand for regulatory service offerings and digital and connected health‐related engagements.

(8/14)

The healthcare business grew upwards of 70% YoY

This was supported by demand for regulatory service offerings and digital and connected health‐related engagements.

(8/14)

The good growth in the Media and Communications:-

Tata Elxsi is a strong player in the OTT and the 5G implementation space.

We see strong growth as the company wins new orders from new geographies as well as new players

(9/14)

Tata Elxsi is a strong player in the OTT and the 5G implementation space.

We see strong growth as the company wins new orders from new geographies as well as new players

(9/14)

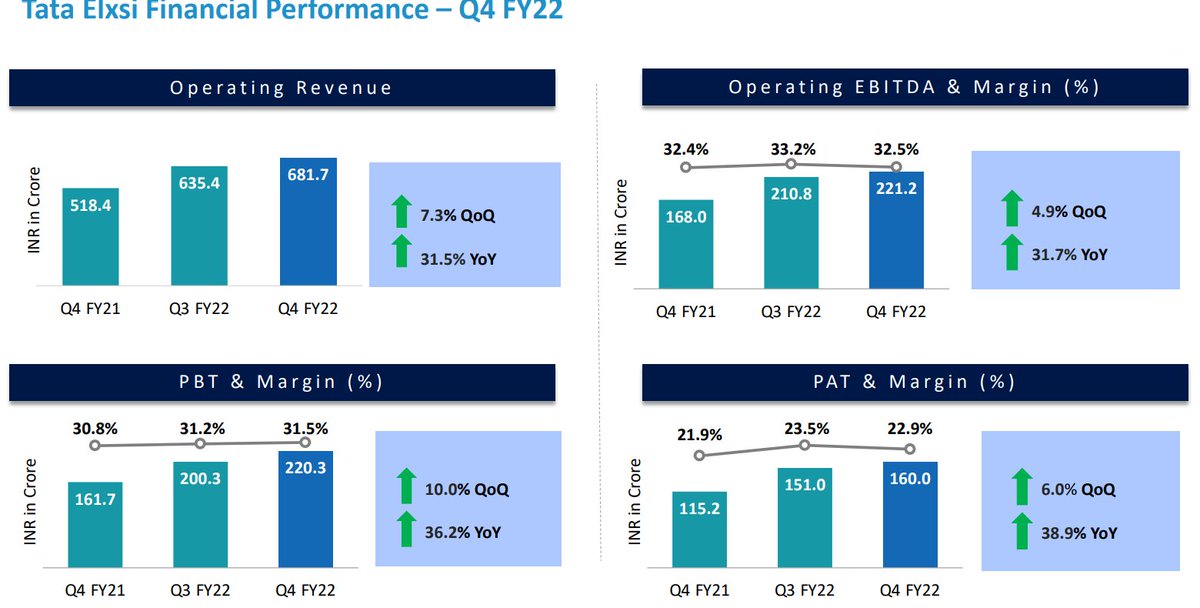

Financials:-

Due to robust demand, the margins have expanded from 24% to 31%.

Full-year 2016 EPS-Rs 25

March 2022 Quarter EPS-Rs 25.

The power of compounding in the business.

The company has a cash rich Balance sheet

(10/14)

Due to robust demand, the margins have expanded from 24% to 31%.

Full-year 2016 EPS-Rs 25

March 2022 Quarter EPS-Rs 25.

The power of compounding in the business.

The company has a cash rich Balance sheet

(10/14)

So what are the risks for the company?

1. Slowdown in the automotive business is a key risk for the company.

2. Rising interest rate scenario may hurt demand.

3. OTT is a very challenging business with cut-throat competition

(11/14)

1. Slowdown in the automotive business is a key risk for the company.

2. Rising interest rate scenario may hurt demand.

3. OTT is a very challenging business with cut-throat competition

(11/14)

Valuations:-

2019:

Price=Rs 622

P/E=15.11

2022

Price:Rs 8000

P/E=90

The massive PE rating has meant the stock has become ultra ultra-expensive with no margin of safety

(12/14)

2019:

Price=Rs 622

P/E=15.11

2022

Price:Rs 8000

P/E=90

The massive PE rating has meant the stock has become ultra ultra-expensive with no margin of safety

(12/14)

Conclusion:-

Tata Elxsi has its business on a strong footing.

There were many problems in 2018.

The company has slowly and steadily overcome those problems and the business has done well in the past 1-2 years

(13/14)

Tata Elxsi has its business on a strong footing.

There were many problems in 2018.

The company has slowly and steadily overcome those problems and the business has done well in the past 1-2 years

(13/14)

The demand momentum for the company is extremely robust.

However, the valuations are extremely expensive and one must be careful on the stock.

One must use the example of Tata Elxsi to understand how the management forged a dramatic turnaround in the business.

(14/14)

However, the valuations are extremely expensive and one must be careful on the stock.

One must use the example of Tata Elxsi to understand how the management forged a dramatic turnaround in the business.

(14/14)

Loading suggestions...