QT starts today a 101 thread.

QT is simply the Fed reducing its balance sheet. They accomplish this in two ways. 1. They let their existing maturities payoff and they don't reinvest the proceeds and burn the cash (called runoff)

2. They sell bonds and mortgages into the private

QT is simply the Fed reducing its balance sheet. They accomplish this in two ways. 1. They let their existing maturities payoff and they don't reinvest the proceeds and burn the cash (called runoff)

2. They sell bonds and mortgages into the private

market. (Called outright sales)

In June they will receive 128Bn in proceeds from their treasuries and bills maturities and only reinvest 98BN in treasuries and bills. That means they will buy 30BN fewer bonds. All else being equal that means the market ex fed will have to

In June they will receive 128Bn in proceeds from their treasuries and bills maturities and only reinvest 98BN in treasuries and bills. That means they will buy 30BN fewer bonds. All else being equal that means the market ex fed will have to

Absorb the bond the fed doesn't buy. BUT all else isn't equal 5 principal factors will impact the markets during this period

1. The Fed QT mentioned above

2. The supply of treasury bonds to refinance maturing bonds and fiscal deficits

3. The demand from the global private sector

1. The Fed QT mentioned above

2. The supply of treasury bonds to refinance maturing bonds and fiscal deficits

3. The demand from the global private sector

4. The demand or supply from official sector of the rest of the world for reserve and currency management

5. The impact of market pricing that discounts future events on both 3. And 4. Above

5. The impact of market pricing that discounts future events on both 3. And 4. Above

I have written a Damped spring report in May called "Who will sell Bonds" that goes into each of these factors in some depth and it is free at dampedspring.com in the past DSR section of the site. But Tl;dr here anyway

Stepping back to the goal of QT. It is a weak but still useful lever to reduce inflation it operates by causing all assets to weaken as the fed lack of buying has to be absorbed by the market. That impact inflation by making asset holders less wealthy and decreasing demand for

goods and services. That's why the fed is doing it. Clearly the administration has inflation reduction as a priority and they can use there composition of treasury issuance as a lever. We will come back to that. But the administration also may care more about avoiding a stock

market crash than the Fed. Not saying whether they care or not. Just saying that they have a broader and political mandate than the Fed's two factor mandate. Let's go back to the factors that matter

1. The Feds plan is now well known. I happened to predict it on January 24th both in quantity and timing which you can read in "The path forward and QT" also free. But the point is that we know exactly what the fed is going to do for at least 2022

2. The supply from treasury is key to how QT works. Supply has two dimensions

- Quantity of issuance

- Composition of issuance

Quantity depends on a few things. Tax receipts, spending, and how much they keep in their checking account (called the TGA).

Over the last few months

- Quantity of issuance

- Composition of issuance

Quantity depends on a few things. Tax receipts, spending, and how much they keep in their checking account (called the TGA).

Over the last few months

The federal budget deficit has been trending down. That is primarily due to an underestimate of tax receipts and a clear gridlock for additional spending bills. Tax receipts have been impacted by a sharp rise in wages earned in aggregate. This is partly due to inflation and

Partly due to more workers. The spending side does not increase with Inflation much at all so the deficit is falling rapidly. Make your own assumption on this but notice that over 2022 the fed QT will reduce bond demand by 330BN if the budget deficit falls by that amount the

Drop in bond issuance supply offsets completely QT demand drops and the private sector is by and large unaffected. The treasury can't really do anything about the tax receipts or the spending in 2022 but they hold two additional levers. Staying with Quantity for now the treasury

Has a bank account called the TGA. They can either spend from that instead of issuing (thus reducing supply) or borrow more from the market and add to their bank account. In Q1 they raised 650BN to replenish their checking account which had dropped close to zero given the Debt

Ceiling issue in Q4. Then the tax receipts flooded in and the TGA peaked at 1TN. It's now 817BN

Here's a picture. Notice that prior to COVID a huge checking account was 400BN.

Here's a picture. Notice that prior to COVID a huge checking account was 400BN.

So here we are at 817BN. If the Treasury simply reduced that back to 500BN that would mean 317BN less issuance in quantity. Or offset to QT. So two serious tailwinds to offset QT 1. Declining budget deficit and 2. Historically high checking account balance. Let's move to

Composition. This is the second lever the Treasury has to impact QT. I have written a ton about this and explained it on many podcasts but simply put. If the treasury issues coupons that helps QT do its job.If they issue bills that neutralizes QT's effect. So what have they done

They have significantly reduced the quantity of issuance as mentioned before as the TGA is full and the deficit is falling. AND within the reduced quantity they have increased the percent of coupons issued. Read that again. Because actual coupon issuance had fallen! But bills

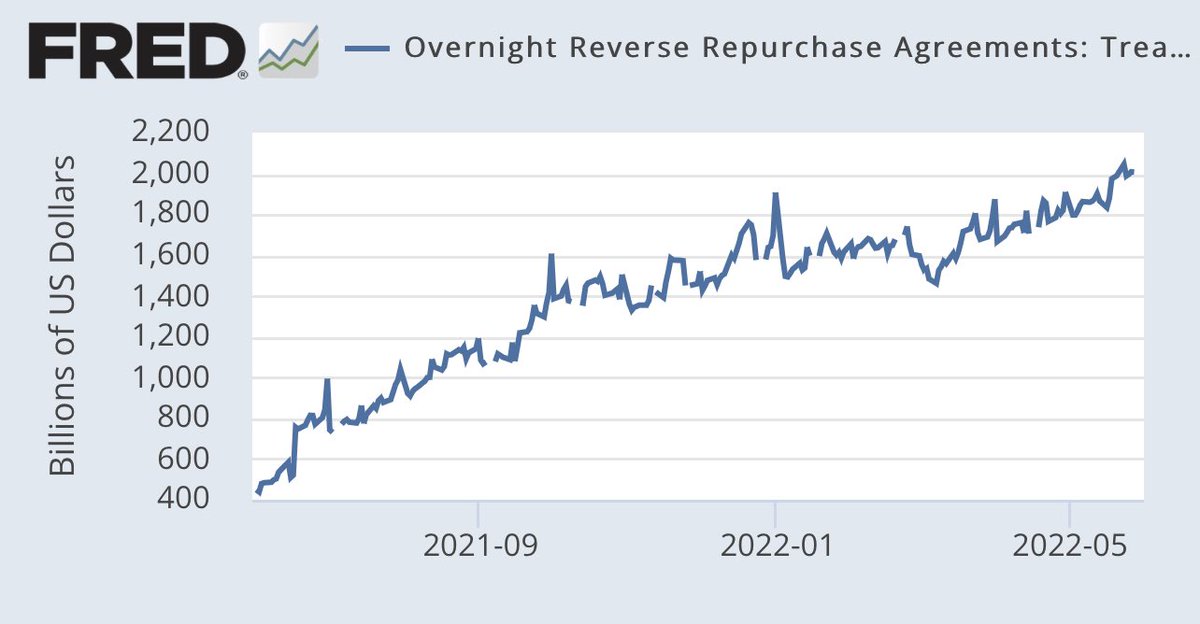

Issuance has cratered going deeply negative in Q2 and Q3 and starving the money markets for investments and have been forced to go to the RRP. Demand for bills is enormous as measured by RRP growing 1/2 a trillion since March.

Why is treasury starving the bills market. I speak to Treasury officials as part of their investor outreach and they are concerned about reducing supply of coupon paper too rapidly because there are real investor needs for duration, a too rapid supply deduction causes squeezes.

But the financing quantity is collapsing so the bills is a plug. Reduce coupons as rapidly as possible but as needs fall reduce bills to get to the number results in both going down a lot but bills much more so. This matters because coupons are falling which offsets QT

So that's the supply.

3. End investor demand. I have lots of graphs in my DSR so will only summarize. Unlevered investors have been large net sellers of duration. Since year end. Banks have stopped buying duration. Levered buyers have modestly increased given more attractive

3. End investor demand. I have lots of graphs in my DSR so will only summarize. Unlevered investors have been large net sellers of duration. Since year end. Banks have stopped buying duration. Levered buyers have modestly increased given more attractive

Levels. Mutual funds have been net sellers. We have seen the outcome in bond yields of all this flow. It's up to you to judge current investor flows and pricing to make your own view of private sector supply and demand. I would call it modestly negative for bond prices here

4. ROW central banks are aggressively weakening their currencies to stimulate economies particularly China. This makes them a seller of CNY and a buyer of USD. They then have to buy a USD asset. They love the belly. We know they have a long term desire to diversify out of USD

Reserves but a short term priority of weakening the currency overrides that desire. We won't know for two months when the TIC data comes up but the currency markets and the blowout directs on the most recent 7 year auction indicates China buying which offset Fed not buying.

*indirects doh

Loading suggestions...