Economics

Finance

Banking

Financial Services

Investments

Cross-selling

mortgages

Credit Growth

Balance Sheet

Portfolio Mix

Consumer Durable Loans

Branch Expansion

Unsecured Loans

HDFC Bank analyst day takeaway,

Credit growth outlook healthy; aspires to double the Balance Sheet in four-to-five years:

The bank aspires to double its Balance Sheet over the next four-to-five years, even on a merged basis.

1/25

Credit growth outlook healthy; aspires to double the Balance Sheet in four-to-five years:

The bank aspires to double its Balance Sheet over the next four-to-five years, even on a merged basis.

1/25

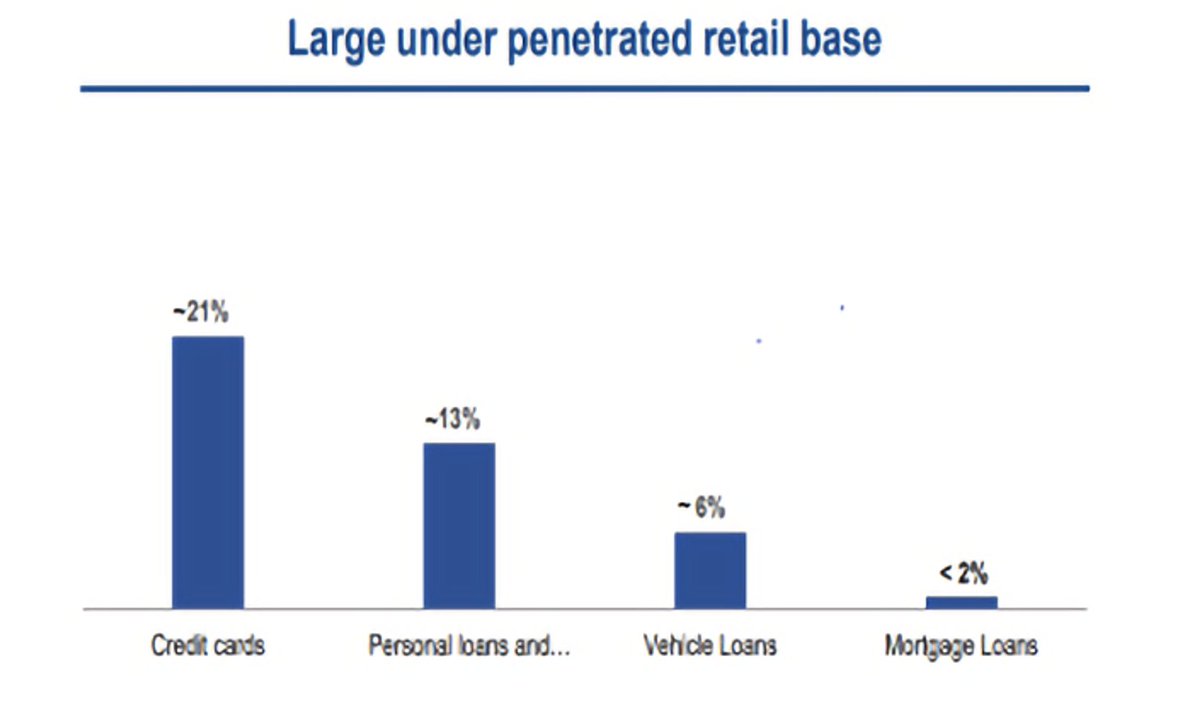

Mortgages to be a key growth driver, improves the portfolio mix:

Mortgages penetration, at 2%, is the lowest v/s 21%/13%/6% penetration for Credit Cards/Personal/Vehicle loans.

Around 70% of HDFC customers do not bank with HDFCB. Undertaking the Mortgage business also

2/25

Mortgages penetration, at 2%, is the lowest v/s 21%/13%/6% penetration for Credit Cards/Personal/Vehicle loans.

Around 70% of HDFC customers do not bank with HDFCB. Undertaking the Mortgage business also

2/25

provides an opportunity to cross-sell Consumer Durable loans.

Currently, ~2k out of 6.3k branches offer mortgages.

The mix of Unsecured loans post-merger is likely to reduce to 22% from ~30% at present, which will increase its appetite to undertake Unsecured loans.

3/25

Currently, ~2k out of 6.3k branches offer mortgages.

The mix of Unsecured loans post-merger is likely to reduce to 22% from ~30% at present, which will increase its appetite to undertake Unsecured loans.

3/25

Branch banking to drive deposit mobilization; C/I ratio to moderate:

The management said that deposit mobilization rose significantly as branches age (10x/25x deposits with 10-15/over 15-years old branches).

Around 60% of branches are less than 10 years old,

4/25

The management said that deposit mobilization rose significantly as branches age (10x/25x deposits with 10-15/over 15-years old branches).

Around 60% of branches are less than 10 years old,

4/25

thus improving vintage will drive deposit growth.

The bank is looking to add 1.5k-2k branches annually & will continue to invest in the business and on its staff.

Despite that, the C/I ratio is likely to moderate to mid-30s (excluding mortgages) over the next 3-to-5 yrs.

5/25

The bank is looking to add 1.5k-2k branches annually & will continue to invest in the business and on its staff.

Despite that, the C/I ratio is likely to moderate to mid-30s (excluding mortgages) over the next 3-to-5 yrs.

5/25

Corporate Banking remains a 2% RoA business:

While the bank went slow on the Retail segment during the COVID-19 pandemic, Corporate asset growth picked up opportunistically.

HDFCB posted a robust growth (16%) in Corporate loans in FY22 as compared to 1% for the system.

6/25

While the bank went slow on the Retail segment during the COVID-19 pandemic, Corporate asset growth picked up opportunistically.

HDFCB posted a robust growth (16%) in Corporate loans in FY22 as compared to 1% for the system.

6/25

The bank looks at the Corporate segment not just from an asset-gathering exercise, but as a segment that helps in increasing liability opportunities and fee income.

7/25

7/25

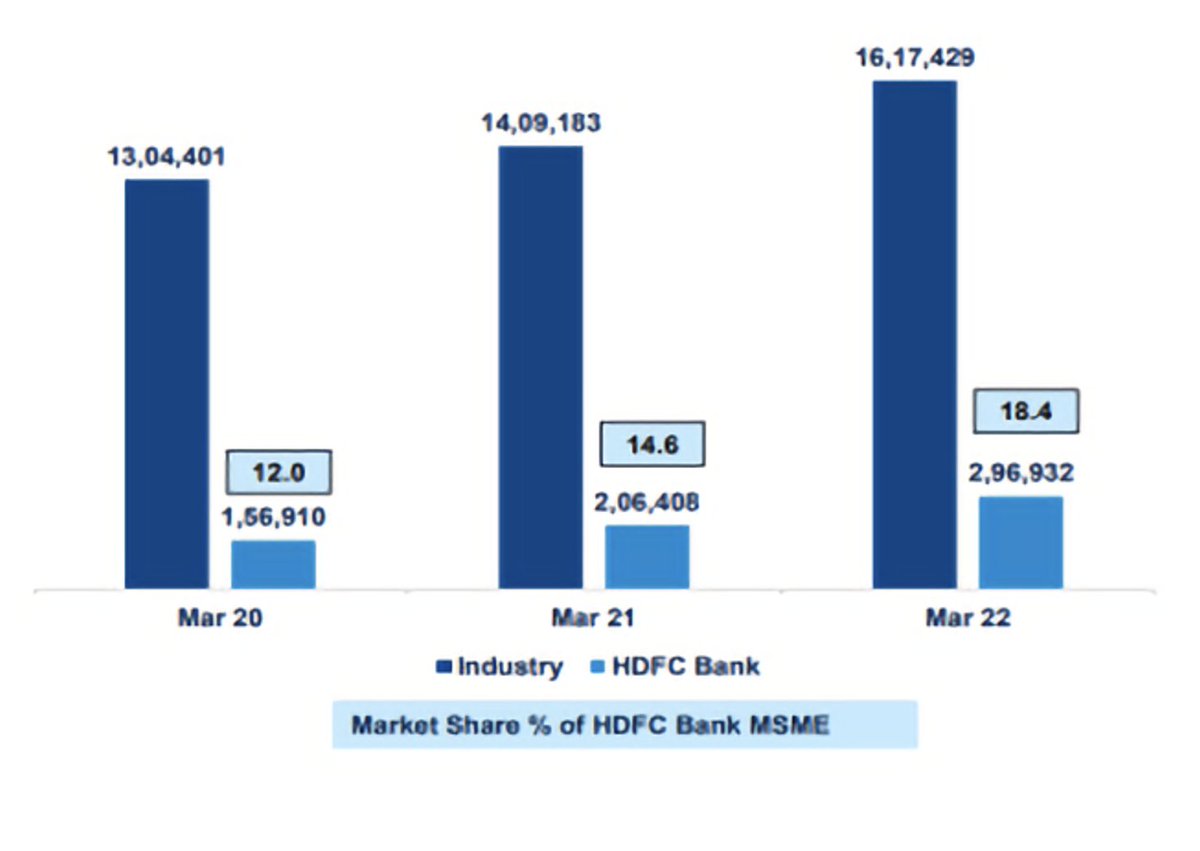

Significant opportunity exists in Commercial and Rural Banking:

Commercial and Rural Banking (CRB) is considered to be the bank’s PSL engine, generating 65-70% of the total PSL for the bank.

The management is confident of growing by 25-30% in this segment, with a

8/25

Commercial and Rural Banking (CRB) is considered to be the bank’s PSL engine, generating 65-70% of the total PSL for the bank.

The management is confident of growing by 25-30% in this segment, with a

8/25

RoA of over 3%

The bank has grown well in this segment & improved its market share by ~600bp over the last 2 yrs to 18.4% in FY22.

On Agri, the bank aims to improve market share by ~300bp to 9% by FY24

The management aims to double its customer base/revenue by FY24/FY25.

9/25

The bank has grown well in this segment & improved its market share by ~600bp over the last 2 yrs to 18.4% in FY22.

On Agri, the bank aims to improve market share by ~300bp to 9% by FY24

The management aims to double its customer base/revenue by FY24/FY25.

9/25

Housing business to drive the Retail portfolio:

The management is bullish on the Housing business and expects the segment to be a primary driver of growth.

The bank plans to increase distribution by 3-4x to improve growth in Gold loans.

10/25

The management is bullish on the Housing business and expects the segment to be a primary driver of growth.

The bank plans to increase distribution by 3-4x to improve growth in Gold loans.

10/25

HDFCB is confident of over 20% growth in Retail assets on a sustained basis.

Focus on building its Retail customer franchise and enhancing cross-selling:

Over the last three years, Retail deposits grew 2x.

The bank aims to double the same over the next 3.5 years.

11/25

Focus on building its Retail customer franchise and enhancing cross-selling:

Over the last three years, Retail deposits grew 2x.

The bank aims to double the same over the next 3.5 years.

11/25

It has gained market share in deposits, with a growth rate of ~2x that of the industry.

Market leadership across payments products; new initiatives to aid growth:

HDFCB offers a whole bouquet of products in payments and consumer financing, and has a

12/25

Market leadership across payments products; new initiatives to aid growth:

HDFCB offers a whole bouquet of products in payments and consumer financing, and has a

12/25

leadership position in both the offline (44%) and online (48%) card acceptance business (POS).

The bank is undertaking various new initiatives, with the launch of PayZapp 2.0 (a comprehensive Mobile commerce payments app) and SmartHub Vyapaar 2.0 (which integrates the

13/25

The bank is undertaking various new initiatives, with the launch of PayZapp 2.0 (a comprehensive Mobile commerce payments app) and SmartHub Vyapaar 2.0 (which integrates the

13/25

entire mobile merchant ecosystem), thus providing a seamless customer experience to drive further growth.

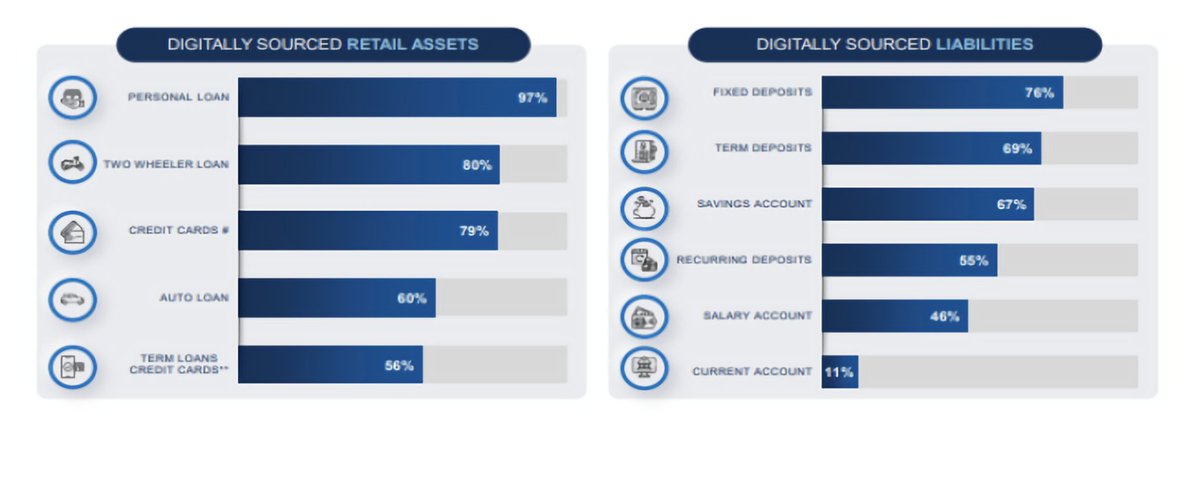

Digital sourcing gaining share, helping improve cross-sell and reduce TAT:

The number of digital transactions rose 3x in FY21-22 from FY18-19 levels.

14/25

Digital sourcing gaining share, helping improve cross-sell and reduce TAT:

The number of digital transactions rose 3x in FY21-22 from FY18-19 levels.

14/25

E-commerce card volumes on the payment gateway saw a 1.75x growth in the past three years, with ~45m UPI transactions being undertaken on a daily basis.

Other key takeaways:

Asset quality ratios remain pristine, the restructured book remains controlled ~1.14% of loans

15/25

Other key takeaways:

Asset quality ratios remain pristine, the restructured book remains controlled ~1.14% of loans

15/25

C/I ratio fell down to 36-37% over FY20-22 v/s 39-40% at pre-COVID levels due to moderation in Retail loans.

As retail lending picks up, C/I ratio is likely to inch up.

Including mortgages, C/I ratio is likely to be early 30s. The aim is to bring it down to below 30%

16/25

As retail lending picks up, C/I ratio is likely to inch up.

Including mortgages, C/I ratio is likely to be early 30s. The aim is to bring it down to below 30%

16/25

over the long term.

Profitability of the Corporate book stands healthy & is still a 2% RoA business. The bank doesn’t do any lending, which is not an 18-20% RoE business during its entire life cycle.

In FY22, the bank grew much faster than industry in corporate banking.

17/25

Profitability of the Corporate book stands healthy & is still a 2% RoA business. The bank doesn’t do any lending, which is not an 18-20% RoE business during its entire life cycle.

In FY22, the bank grew much faster than industry in corporate banking.

17/25

While the system grew 0.9%, Bank posted a strong growth of 15.7% in FY22.

Corporate Banking asset grew at 22% CAGR over last 2 years.

Commercial & Rural Banking:

Opportunity size of segment is huge. Total SME credit demand is of INR50t. Out of this INR20t is serviced

18/25

Corporate Banking asset grew at 22% CAGR over last 2 years.

Commercial & Rural Banking:

Opportunity size of segment is huge. Total SME credit demand is of INR50t. Out of this INR20t is serviced

18/25

by Banks and NBFCs. INR10t is done by the proprietor in his/her own name. Therefore, there is a credit gap of INR20t, which will be funded by organized sector over time.

Market share in MSME segment improved to 18.4% from 12% in the last two years.

19/25

Market share in MSME segment improved to 18.4% from 12% in the last two years.

19/25

Today, the bank is present in more than 600 districts. This has grown from 450 districts, four years ago.

On Agri market share at 6.4% with a target of reaching 9% by FY24.Disbursements in FY23 to be book size of FY22.

20/25

On Agri market share at 6.4% with a target of reaching 9% by FY24.Disbursements in FY23 to be book size of FY22.

20/25

It aims to double its customer base by FY24. It aims to double FY22 revenue by FY25.

Payments Business:

Cards acceptance business (POS): 44% market share in offline cards; 48% market share in online cards acquiring.

Around 13% market share in UPI (P2M);

21/25

Payments Business:

Cards acceptance business (POS): 44% market share in offline cards; 48% market share in online cards acquiring.

Around 13% market share in UPI (P2M);

21/25

25% market share in EPI

Average ticket size stands at INR1,900 with around three transactions per customer.

5.Retail Customer Franchise and Life Cycle Management:

Retail deposits grew 2x in the last three years. The target is to grow another 2x over the next 3.5 years.

22/25

Average ticket size stands at INR1,900 with around three transactions per customer.

5.Retail Customer Franchise and Life Cycle Management:

Retail deposits grew 2x in the last three years. The target is to grow another 2x over the next 3.5 years.

22/25

Customer acquisition grew 1.9x over FY18-22 to 8.3m. The target is to reach 10m over the next 15 months.

Branch breakeven is improving. Vintage branch breakeven was 2-2.5 years. Some branches now break even in nine-to-ten months.

23/25

Branch breakeven is improving. Vintage branch breakeven was 2-2.5 years. Some branches now break even in nine-to-ten months.

23/25

Around 55% of branches breakeven within 12-24 months.

Aiming for a 2x growth in rural in 18-24 months through a differentiated proposition.

Asset quality continued to witness an improvement over 4QFY22, led by lower slippages. GNPA/NNPA moderated to 1.17%/0.32%.

24/25

Aiming for a 2x growth in rural in 18-24 months through a differentiated proposition.

Asset quality continued to witness an improvement over 4QFY22, led by lower slippages. GNPA/NNPA moderated to 1.17%/0.32%.

24/25

Restructuring book declined to ~INR157b (1.14% of total loans). Moreover, PCR improved to ~73%, which, along with a floating provision of INR14.5b and contingent provision of INR96.9b, would keep credit cost in check & limit the impact on profitability

End of the thread.

25/25

End of the thread.

25/25

Loading suggestions...