There were 2 Friends, Rahul and Samay. Both were trading the same system.

But,

Samay's P&L: +50%

Rahul's P&L: -100%

What happened? Why did Samay make money, but Rahul blew up his account, even though both were trading the exact same system?

But,

Samay's P&L: +50%

Rahul's P&L: -100%

What happened? Why did Samay make money, but Rahul blew up his account, even though both were trading the exact same system?

You, see trading is not just about finding a system with a positive expectancy. You need good risk management and appropriate position sizing to make the best possible returns while avoiding the risk of ruin.

Position sizing decides the "how much" part of your system

Position sizing decides the "how much" part of your system

In this thread, we will cover:

Why position sizing is important?

How to find the correct position sizing for your system?

And, what are the different position sizing techniques?

Why position sizing is important?

How to find the correct position sizing for your system?

And, what are the different position sizing techniques?

As they say:

"A trader with a mediocre system and a great Risk model will become fairly successful.

Whereas, A trader with a great system and a mediocre risk model will become bankrupt"

"A trader with a mediocre system and a great Risk model will become fairly successful.

Whereas, A trader with a great system and a mediocre risk model will become bankrupt"

Okay, but how does position sizing affect a system's performance and why does it matter so much?

Let's understand with help of an example.

Let's understand with help of an example.

Let's play a game of coin toss, heads: you win 100% of your wager, tails: you lose 100%

But, the catch is that the coin is biased, and the probability of heads coming is 52%. So you do have an edge here.

But, the catch is that the coin is biased, and the probability of heads coming is 52%. So you do have an edge here.

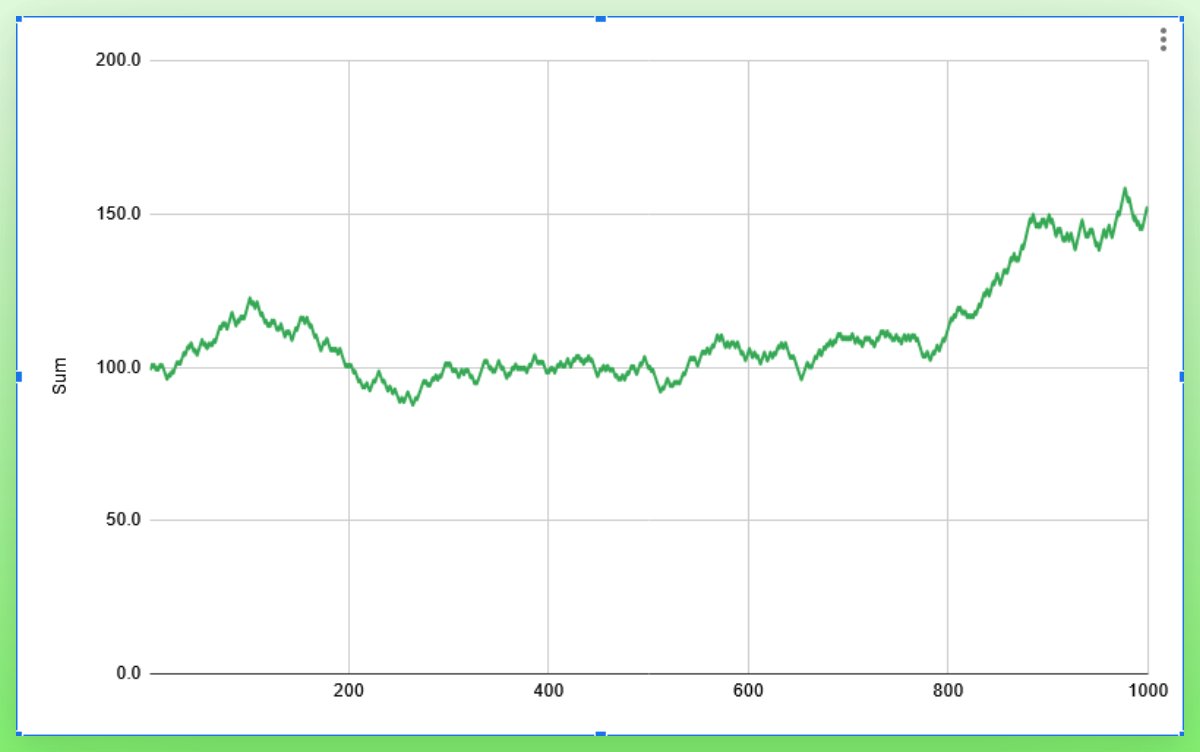

This is what your net worth will look like with different bet sizes.

With 1% risk, and after 1000 simulated coin tosses, you will end up with 150.7$, a 50% return on your net worth.

With 1% risk, and after 1000 simulated coin tosses, you will end up with 150.7$, a 50% return on your net worth.

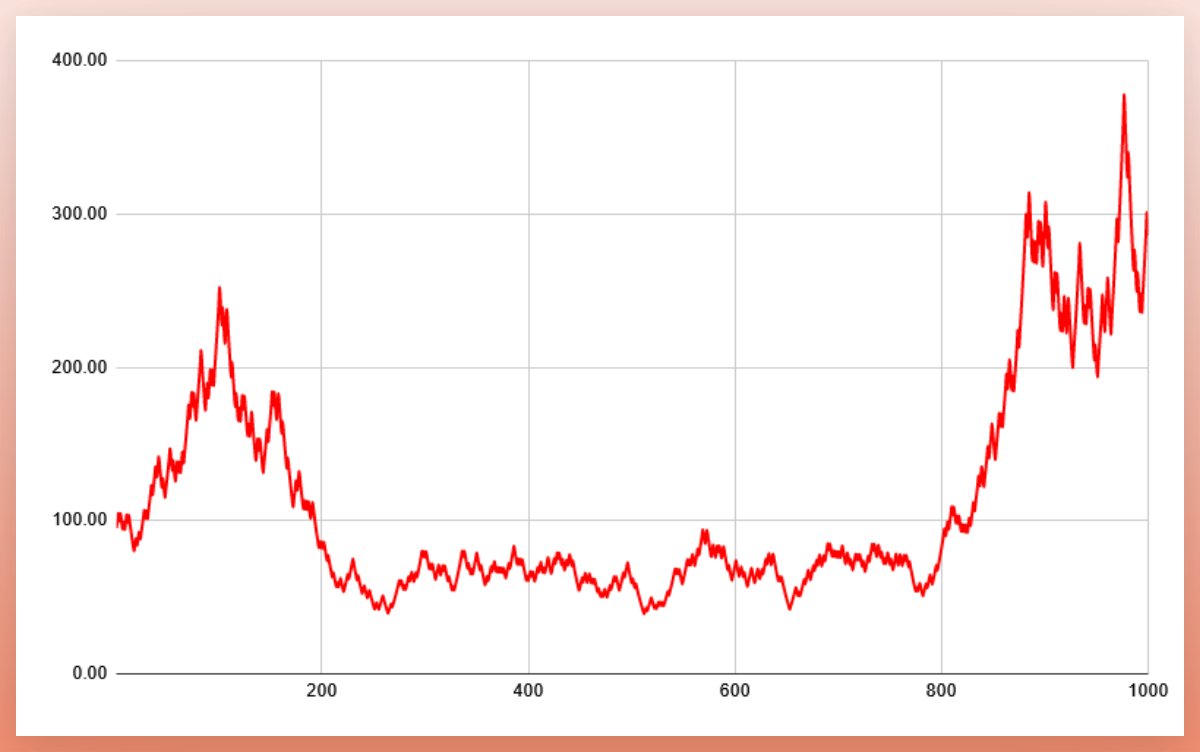

But, what if you risked more, say 5% or 15%?

Of course, as you increase the risk the magnitude of the losses as well as the profits will increase, but once you cross the optimal size, the losses will start hurting the PF, and profits won't be able to compensate for that, and you will eventually end up losing all your money.

With 5% risk, you end up with 286$, with some huge swings in your equity curve, you made about a 180% return on your net worth.

But, if you had increased the risk to 15%, initially you would've made more profits, but in the end, you would've lost all your money.

Now, here we consider ruin when the portfolio value goes to zero, in real life most of us won't be able to trade the system once the dd starts going inching above 10-15%.

So, even if you have a great system, it becomes really important to have robust money management and position sizing plan.

but, now the question is what's the correct risk or position sizing for your trading system?

but, now the question is what's the correct risk or position sizing for your trading system?

As we said earlier, trading is not just about finding a system with an edge, with that, you also need to risk the amount, which will generate your maximum returns without the risk of ruin.

So, how can one know the optimal risk for his trading system? There are various ways to look at it.

The best way is to find the historical drawdowns of the system that you are trading and add some buffer to it, and you'll get an idea of how much your system can lose with different risks.

obviously, the dd can go much higher when you run your system live, but that's why we are adding a buffer to it.

Say, If you are getting a 20% maximum dd on your backtested results, chances are that it will g much higher than this in the future, so if you are a conservative trader you should expect this dd to reach 2x or 40%, and then position sizing accordingly.

Having a systematic approach to the risk that your system possess is probably the best way to know the correct position sizing for your system.

Though you could say that there's one more method, that is the kelly criterion, which is supposed to give you the "optimal" amount that you should bet on every trade.

You can read more about Kelly criterion and Optimal F in detail here,

quantpedia.com

You can read more about Kelly criterion and Optimal F in detail here,

quantpedia.com

Though IMO this works more in theory than in real life, also there's a chance that even if you risk a bit more than the optimal size that kelly generates, you'll end up blowing your account. so it kinda takes you to the edge of the maximum risk that your system can bare.

But, what if you aren't a systematic trader, but a discretionary one, which means that you might not have a good idea about the risk that your system possesses, so how can you position size correctly then?

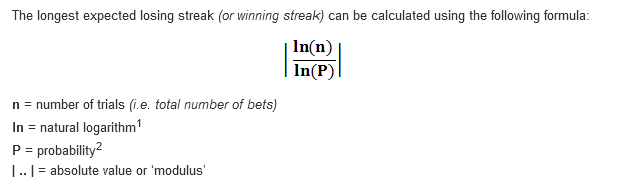

One way could be to look at the maximum losing trades that you can have in a row by looking at the winning % of your historical trades.

The below chart shows how many losing trades you can have in a row, over the next 1000 trades.

The below chart shows how many losing trades you can have in a row, over the next 1000 trades.

You can calculate the same by plugging in different values for win rate, and size of the data set (number of trades) into this formula.

Though it might not give you the "optimal" position sir, it will at least give you a basic idea of how much you can lose if shit hits the fan.

Though it might not give you the "optimal" position sir, it will at least give you a basic idea of how much you can lose if shit hits the fan.

So if you could bear those losing streaks chances are that your position sizing is correct if the dd looks too big, it's time to lower the position sizing, then.

There are many position sizing methods that you can follow:

Percent Risk Position Sizing Method

As the name suggests in this position sizing method we are risking a fixed percentage of our account on every trade, irrespective of the account size.

As the name suggests in this position sizing method we are risking a fixed percentage of our account on every trade, irrespective of the account size.

If the account size says 1 lakh and we are risking 1% on every trade, our risk per trade will be 1000.

Once we take a trade and say it was a winner and, our Capital grows to 1,10,000 then we will riks 1% of it, which will be 1100, and in case we lost money on our first trade and the account goes to 90k, then we'll take a 900 Rs risk on the next trade.

Let's understand this method with help of an example:

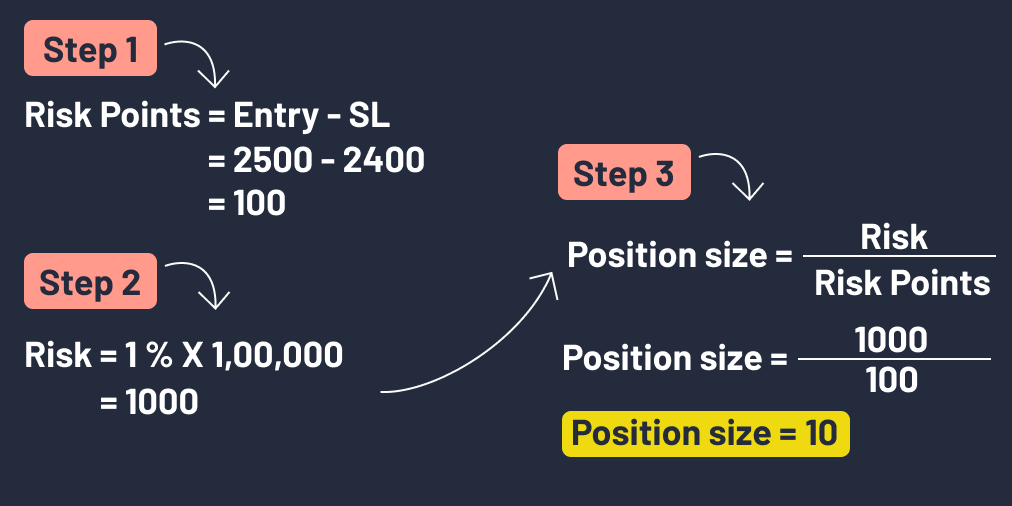

Say you want to buy Reliance at 2500, and according to your method, the Stop-loss level for this trade should be 2400.

And you decide to take 1% risk on every trade that you take and your capital is 1 lakh Rs.

Say you want to buy Reliance at 2500, and according to your method, the Stop-loss level for this trade should be 2400.

And you decide to take 1% risk on every trade that you take and your capital is 1 lakh Rs.

The position size in this example comes to be 10, which means that you have to buy 20 qty of this stock.

Let’s take an example of short selling as well:

Say you want to short a stock at 1000 Rs and your SL for this trade is 1020.

Your risk% per trade is 1% and your account size is 1 lakh.

Say you want to short a stock at 1000 Rs and your SL for this trade is 1020.

Your risk% per trade is 1% and your account size is 1 lakh.

In this trade, you would have to short 50 qty of a stock.

Now let’s move on to the next position sizing method.

Now let’s move on to the next position sizing method.

Equal Units Position sizing method

In this method, we allocate an equal amount of money to each trade, irrespective of our stop loss level.

In this method, we allocate an equal amount of money to each trade, irrespective of our stop loss level.

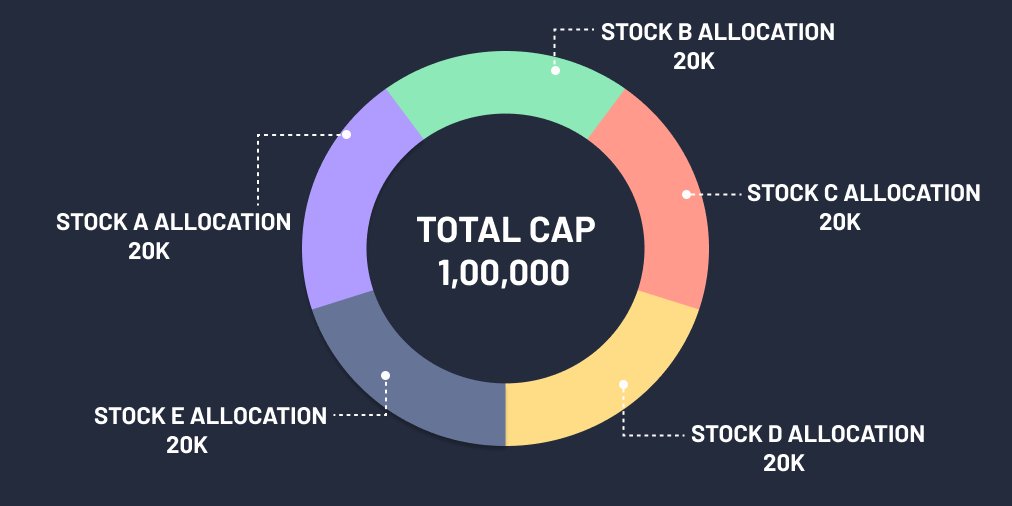

We divide the total equity into parts, say 5, and then we allocate the same amount to the 5 stocks that we buy in our portfolio.

For example, if we have 1,00,000 in our account, and the max position we want to hold at a time is 5, then we can divide the total capital into 5 parts, which will be 20K each.

So, we will allocate 20k of our account on each trade that we get, irrespective of anything else.

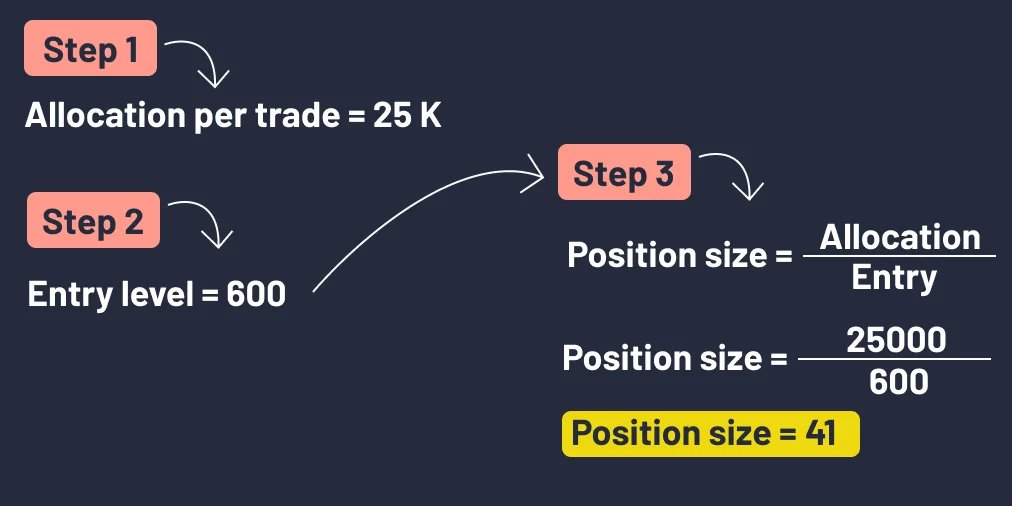

Say we got a signal to buy XYZ stock at 600 Rs, your account value is 1,00,000 and you decided to put 25k in each stock that you Trade.

then, this is how you will decide your position sizing using this method.

then, this is how you will decide your position sizing using this method.

This method is mostly used in investing or portfolio building, where we buy a bunch of stocks, with similar 5-10% below SL levels.

The equal unit approach allows you to give equal weightage to each investment in your portfolio.

Now, let’s move on to the next method.

The equal unit approach allows you to give equal weightage to each investment in your portfolio.

Now, let’s move on to the next method.

Percent Volatility method

This Position sizing method is based upon the Volatility of a stock, By volatility what we mean to say is the daily movement of an instrument.

To calculate the daily movement of a stock we have to subtract the Low of the day from the high of the day.

This Position sizing method is based upon the Volatility of a stock, By volatility what we mean to say is the daily movement of an instrument.

To calculate the daily movement of a stock we have to subtract the Low of the day from the high of the day.

Say, Reliance stock Opened at 2500 and it made a high of 2650 and a low of 2480 and closed in 2550

Then its daily movement is: High – low = 2650 – 2480 = 170

Then its daily movement is: High – low = 2650 – 2480 = 170

So we can calculate the last few day’s volatilities by calculating the average daily movement of the last few days, but we are ignoring the gaps if we use this method.

To counter this we use the "Average true range" indicator to measure the stock’s volatility.

To counter this we use the "Average true range" indicator to measure the stock’s volatility.

This method is used in combination with the percent Risk method that we discussed earlier.

Let’s see how, with the help of an example.

Let’s see how, with the help of an example.

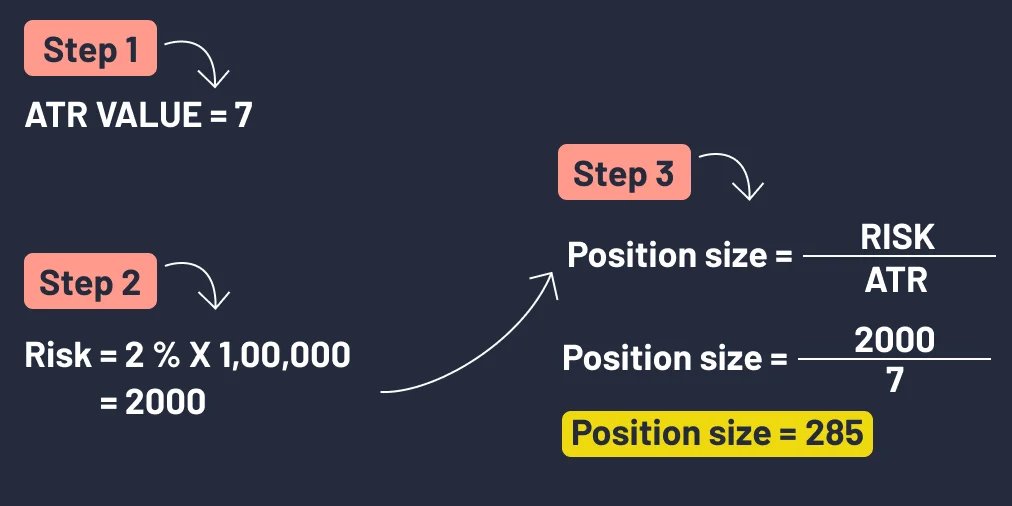

Say, Our Trading account value is 1,00,000 and we don’t want to risk more than 2% on any trade.

Say we get a buying signal at 145 because the stock had found buying in this zone many times in the past.

Say we get a buying signal at 145 because the stock had found buying in this zone many times in the past.

Then we check the ATR indicator value, which is around 7 Rs at the time of entry, so we subtract 7 rs from 145, which is 138, which will be our stop-loss price for this trade.

Calculating the Position sizing

So, you would've to buy 285 Qty of this stock according to this method.

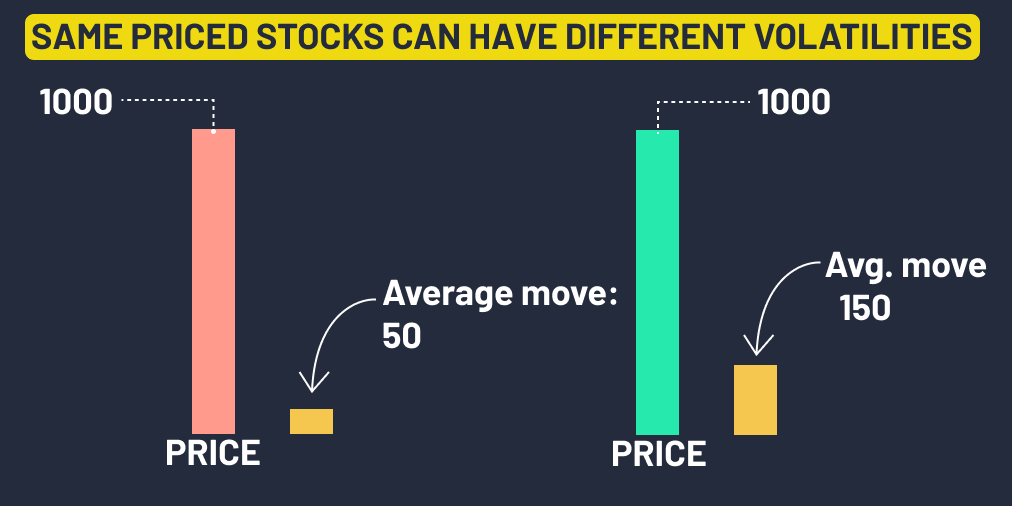

The main merit of using this method is that it takes into account the volatility of the stock, as different stocks have different volatility, and even the same priced stocks can have different volatilities.

The main merit of using this method is that it takes into account the volatility of the stock, as different stocks have different volatility, and even the same priced stocks can have different volatilities.

So, this method gives us an objective way of setting our stop loss according to the daily average move of stock, without any guesswork.

So, that's it for today.

Stay tuned @finkarmaIN for more such writeups in the coming days

If you learned something new, don’t forget to like and retweet this thread.

Thanks for reading

Stay tuned @finkarmaIN for more such writeups in the coming days

If you learned something new, don’t forget to like and retweet this thread.

Thanks for reading

Loading suggestions...