Ever since 2018, the Auto sector has faced severe challenges.

A short thread🧵 on the state of the auto sector and why we think the cycle is slowly turning

Lets go👇

(1/12)

A short thread🧵 on the state of the auto sector and why we think the cycle is slowly turning

Lets go👇

(1/12)

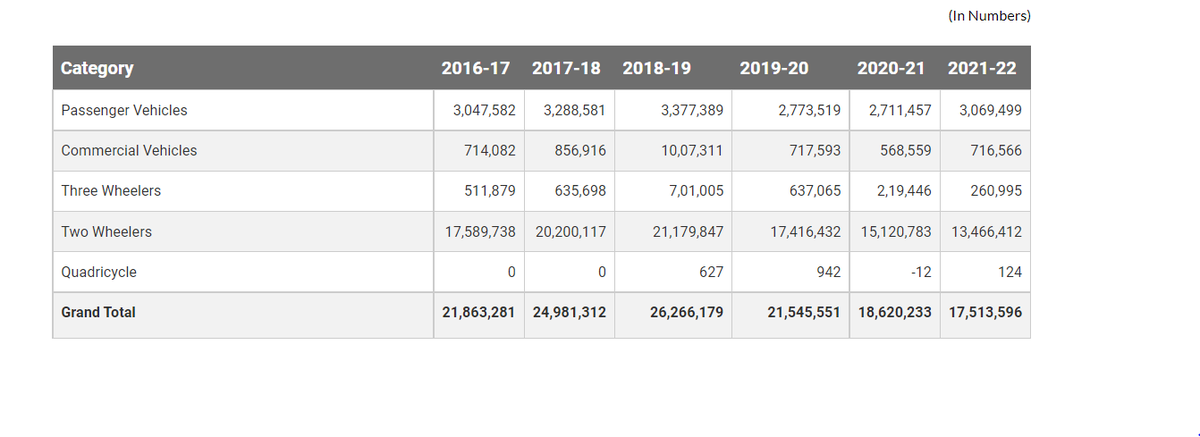

The cyclicality of the Auto sector:-

Sales peaked out across PV,CV and 2Ws in 2018.

Sales have not crossed the 2018 levels in any of the line of Vehicles.

Deep stress was evident when companies went all out to give discounts in 2020.

(2/12)

Sales peaked out across PV,CV and 2Ws in 2018.

Sales have not crossed the 2018 levels in any of the line of Vehicles.

Deep stress was evident when companies went all out to give discounts in 2020.

(2/12)

Deep Stress in the economy since 2018.

Ever since 2018 there has been a freeze in credit flow in the economy.

That led to deep distress in the economy.

Lockdowns induced by COVID-19 further accentuated the deep distress in the economy.

(3/12)

Ever since 2018 there has been a freeze in credit flow in the economy.

That led to deep distress in the economy.

Lockdowns induced by COVID-19 further accentuated the deep distress in the economy.

(3/12)

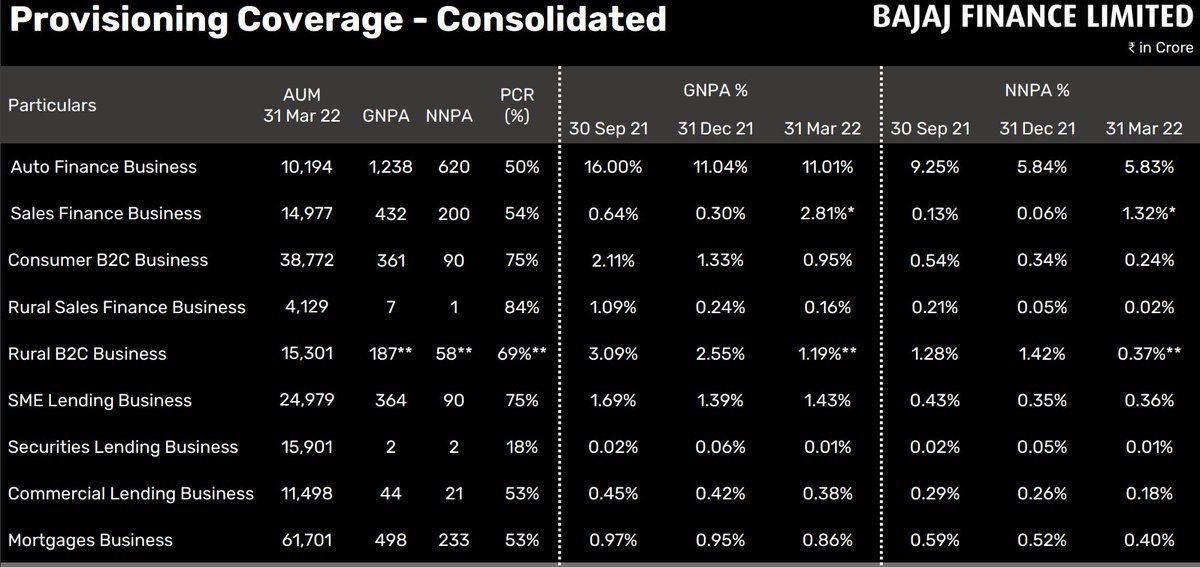

Deep stress for Auto Lenders:-

As the auto sector faced severe headwinds.

The lenders to the sector faced severe NPA pressure.

Lenders like Bajaj Finance saw a rise in NPA to about 11%.

Tata Motors NBFC arm saw a surge in NPAs to about 25%

(4/12)

As the auto sector faced severe headwinds.

The lenders to the sector faced severe NPA pressure.

Lenders like Bajaj Finance saw a rise in NPA to about 11%.

Tata Motors NBFC arm saw a surge in NPAs to about 25%

(4/12)

Semi-Conductor Shortages:-

Semiconductors are an essential part of manufacturing in the auto industry.

Beginning 2021 due to a massive surge in demand, Semi-Conductor shortage was observed.

The situation was so bad,OEMs in India+across the world cut down on production

(5/12)

Semiconductors are an essential part of manufacturing in the auto industry.

Beginning 2021 due to a massive surge in demand, Semi-Conductor shortage was observed.

The situation was so bad,OEMs in India+across the world cut down on production

(5/12)

Surge in input costs for the OEMs

Maruti outlines the commodity price inflation:-

🚘Steel prices from Rs 38000/T to Rs 65000/T

🚘Copper went from $5200/T to $10000/T

🚘Rhodium increased from 18000/gm to 65000/gm

This severly dented the OEM margins

(6/12)

Maruti outlines the commodity price inflation:-

🚘Steel prices from Rs 38000/T to Rs 65000/T

🚘Copper went from $5200/T to $10000/T

🚘Rhodium increased from 18000/gm to 65000/gm

This severly dented the OEM margins

(6/12)

Why do we think the auto sector has bottomed out?

The recovery in the economy:-

As the economy comes out of COVID-19 shock and opens up....credit will start to flow into the economy.

As the recovery continues, this help sustain the auto demand.

(7/12)

The recovery in the economy:-

As the economy comes out of COVID-19 shock and opens up....credit will start to flow into the economy.

As the recovery continues, this help sustain the auto demand.

(7/12)

Easing of Semi-Conductor shortages:-

The shortages on the semiconductor side are expected to ease in 2023.

This will help OEMs revert back to original production plans.

(8/12)

The shortages on the semiconductor side are expected to ease in 2023.

This will help OEMs revert back to original production plans.

(8/12)

Low Inventory:-

Most dealers across India and Europe have run out of inventory for cars.

This will mean OEMs will have to produce more in order to service demand.

(9/12)

Most dealers across India and Europe have run out of inventory for cars.

This will mean OEMs will have to produce more in order to service demand.

(9/12)

Record waiting period:-

With OEMs struggling with chip shortages

Some cars have a waiting period ranging from 6 months to about 1.5 years.

(10/12)

With OEMs struggling with chip shortages

Some cars have a waiting period ranging from 6 months to about 1.5 years.

(10/12)

Valuations:-

While most OEMs may not be cheap..some do offer value.

Many auto ancillaries trade at P/S of less than 1 and are dirt cheap.

(11/12)

While most OEMs may not be cheap..some do offer value.

Many auto ancillaries trade at P/S of less than 1 and are dirt cheap.

(11/12)

Conclusion

Auto sector has undergone a severe downturn over the last 3 years.

Mean Reversion will start to play out.

The next 3 years should see a revival in the fortunes of the sector

(12/12)

Auto sector has undergone a severe downturn over the last 3 years.

Mean Reversion will start to play out.

The next 3 years should see a revival in the fortunes of the sector

(12/12)

Loading suggestions...