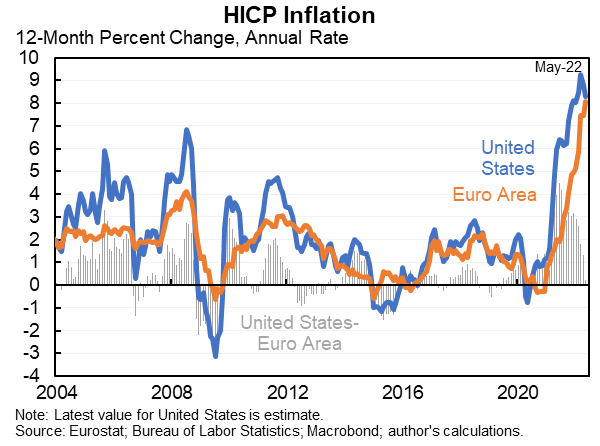

Headline US & Euro area inflation rates have converged.

But, the underlying dynamics of the inflation in the 2 economies is different. More painful in Europe. More persistent in the US.

Calls for different policy responses.

My latest @wsjopinion wsj.com

But, the underlying dynamics of the inflation in the 2 economies is different. More painful in Europe. More persistent in the US.

Calls for different policy responses.

My latest @wsjopinion wsj.com

Here is the opening paragraph of my piece summarizing the argument.

Inflation is a combo of supply and demand everywhere.

But more US inflation is home grown/demand driven. And more European inflation is imported/supply driven.

Makes US inflation less painful than European because Americans got transfer payments & larger nominal wage gains).

But more US inflation is home grown/demand driven. And more European inflation is imported/supply driven.

Makes US inflation less painful than European because Americans got transfer payments & larger nominal wage gains).

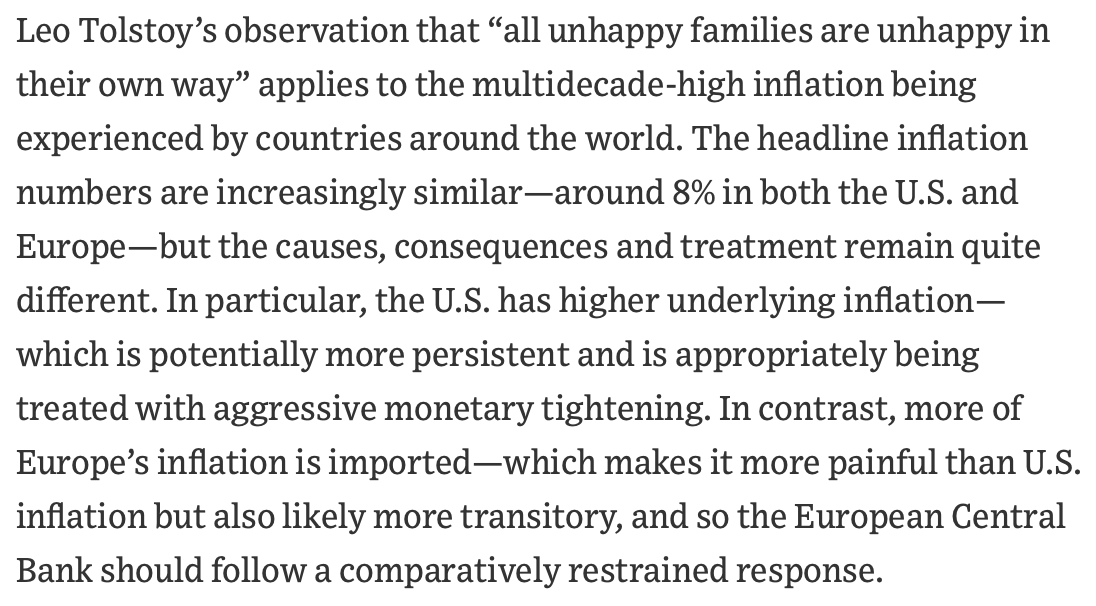

Over the last four months European inflation has actually been faster than U.S. inflation. This is because natural gas prices have skyrocketed to 3X as high in Europe as they are in the United States.

This difference is clearly (and literally) imported.

This difference is clearly (and literally) imported.

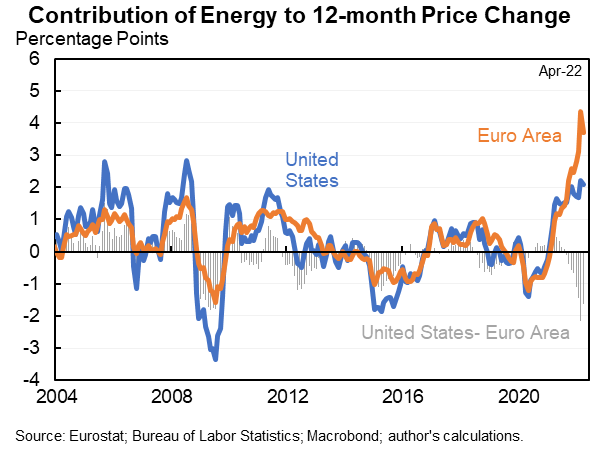

Looking at core inflation (which excludes volatile food and energy) there is still a ~2.7 percentage point difference over the last 12 months. That's a HUGE gap.

High car prices have elevated US core inflation. But European core prices have also been elevated by two imported factors:

1. Passthrough from high natural gas prices

2. US fiscal stimulus driving up goods prices worldwide.

1. Passthrough from high natural gas prices

2. US fiscal stimulus driving up goods prices worldwide.

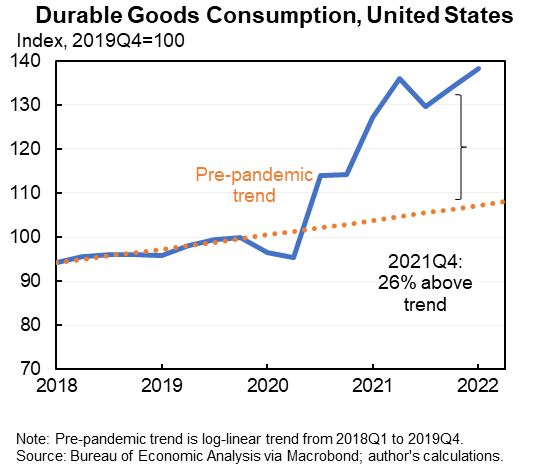

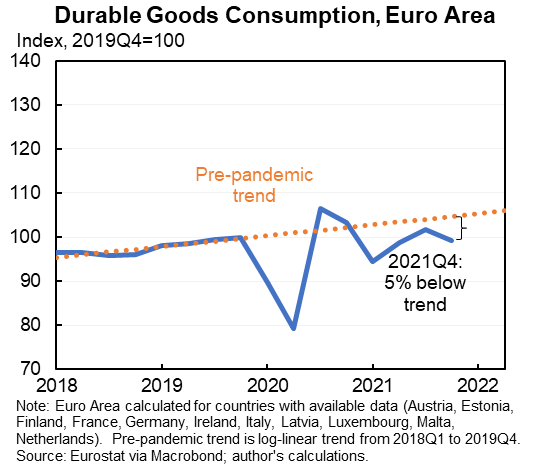

On 2, the difference between the US and Euro area durable goods spending is enormous. The US goods spending was not primarily a COVID-induced shift from services: it happened after the 2021 checks went out and as COVID was rapidly declining. And European services was lower.

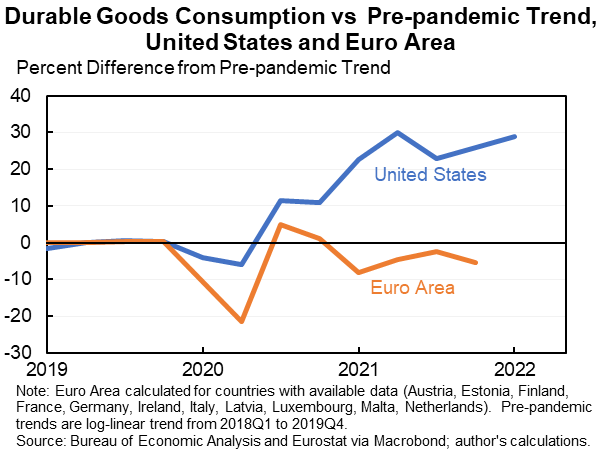

To put this in perspective, this shows the 2 relative to trend. Clearly: (1) more demand in the US (for better or worse, many argue for better which is a coherent view) & (2) US increase was 4% of global durables spending, enough to exacerbate global supply-side price increases.

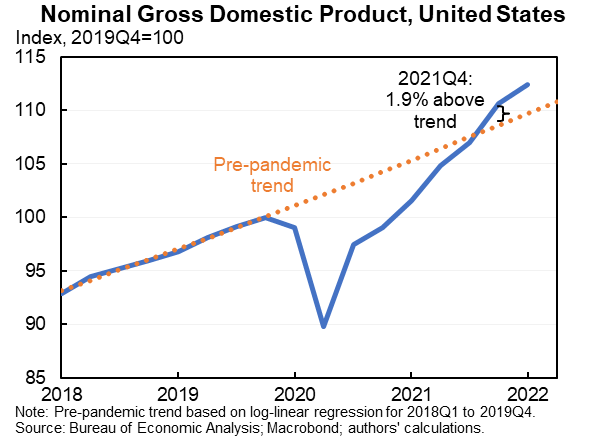

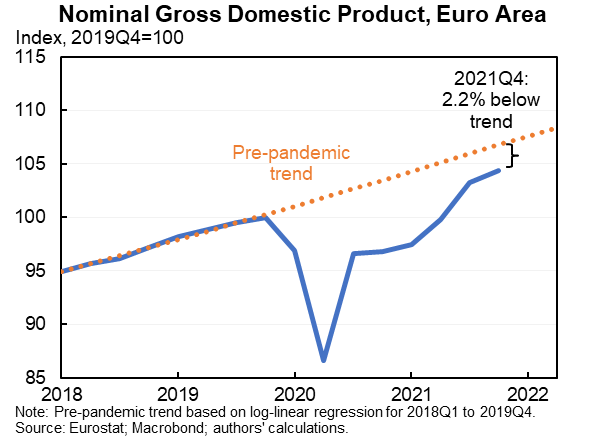

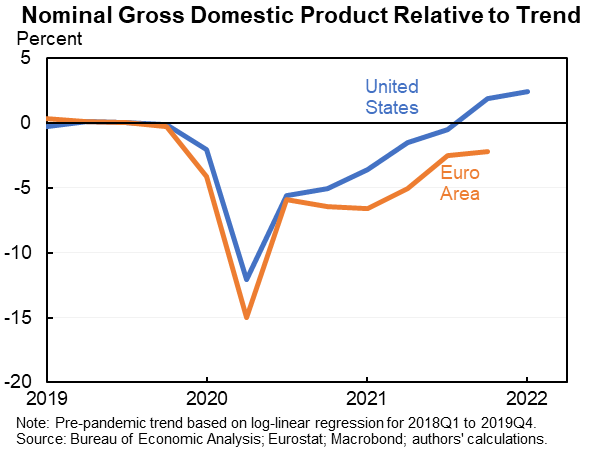

The fact that demand is much higher and playing a bigger role comes out clearly when comparing nominal GDP: The US is well above trend while the Euro area was well below trend in 2021-Q4 (the most recent available data).

Showing that same analysis but comparing the two relative to trend.

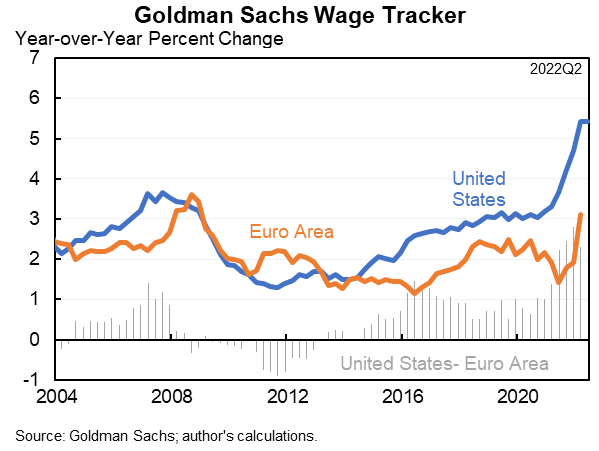

Finally, perhaps most telling is is the differences in nominal wage growth. Nominal wage growth picked up much more in the United States than in the Euro area. And is a bigger driver of inflation here.

(Note, some of the recent rise in Europe is one-time payments in Germany.)

(Note, some of the recent rise in Europe is one-time payments in Germany.)

In Europe this is called a "cost of living crisis" & for good reason. Real wage declines are much larger than they are in the United States. They didn't get anything resembling US transfer payments. Much of the inflation came from abroad and is showing up in prices but not wages.

It's also painful in the United States with real wages falling at the fastest rate they have fallen in forty years. But not nearly as painful as it is in Europe.

My main interest in this issue is forward-looking. I was recently in a number of discussions with European policymakers and I think it is important that the ECB not overreact to the imported inflation. And I don't think the US returning to neutral rates is an overreaction.

P.S. All inflation numbers above are roughly comparable ways of measuring, they use the European concept which is HICP. Basically that is US inflation excluding shelter.

Loading suggestions...