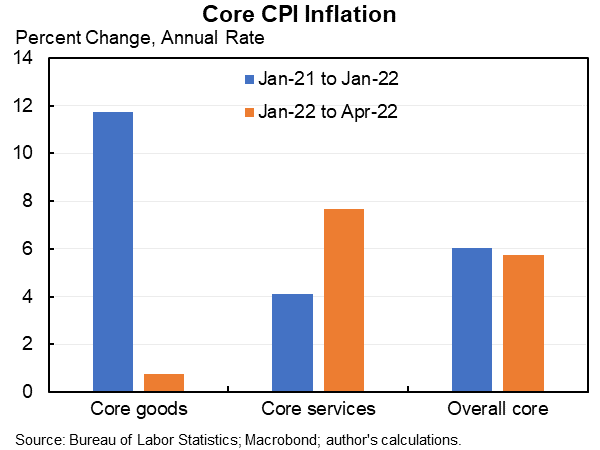

In the last 4 months core goods inflation has nearly disappeared. But core services has picked up—leaving core inflation roughly unchanged (because core services have 2.7X the weight of core goods).

Raises questions about the supply chain & pandemic explanations of inflation.

Raises questions about the supply chain & pandemic explanations of inflation.

This is also a big reason to be worried about the persistence of inflation: services are more cyclically sensitive than goods & less volatile.

@jimstockmetrics & Mark Watson’s “cyclically sensitive inflation” is mostly services & does is not moderating. atlantafed.org

@jimstockmetrics & Mark Watson’s “cyclically sensitive inflation” is mostly services & does is not moderating. atlantafed.org

Overall, however, the easing of the pandemic (in terms of the economy/behavior) has more likely *increased* inflation than reduced it, eg rapid increases in airfares recently. So some services inflation is likely transitorily high & will fall. (And goods should become negative.)

On balance my modal expectation is core PCE inflation of 4% this year and 3.75% in 2023 (Q4/Q4). My mean expectation is more like 3.5% core PCE for 2023 (averaging in the possibility of a recession).

Loading suggestions...