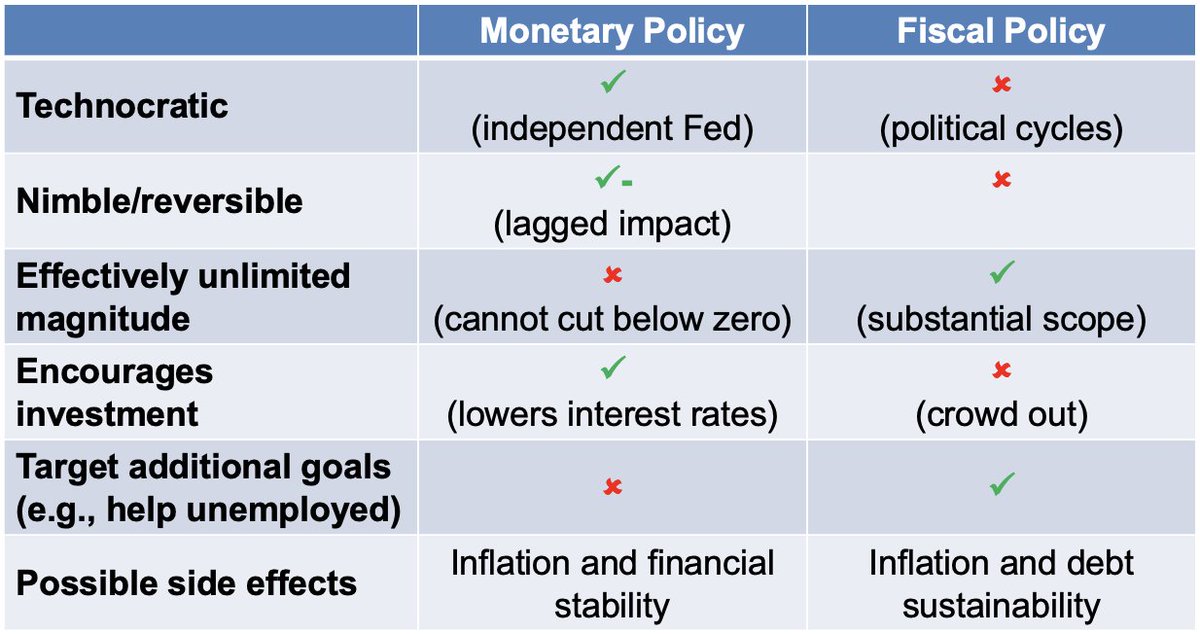

What are the arguments for using monetary policy vs. fiscal policy for stabilization? In theory they can accomplish the same thing (as noted by @pmichaillat among others in discussion w/ @mioana yesterday). In practice some big differences.

To get more granular on fiscal, choice of tax vs. spend (@mioana's original question). In practice one downside of tax is that it functions in annual increments whereas spending programs can be adjusted more frequently (e.g., UI or SNAP eligibility rules, Medicaid transfers).

So while adjusting a wealth tax or transfer payments in theory could mimic interest rates (& could better achieve other goals too), in practice it is hard to see them being adjusted every six weeks like rates.

Finally, @mioana's interesting question was not about discretionary policy but *automatic* fiscal policy. I would not set monetary policy in an automatic way through a Taylor Rule, NGDP targeting or any other rule. So why use a rule for fiscal policy where it is even harder?

First let's distinguish between:

*Normal* automatic stabilizers (e.g., a benefit for the jobless that automatically spends out more when more people lose jobs)

*Algorithmic* automatic stabilizers (e.g., a jobless person gets more when unemployment is higher).

*Normal* automatic stabilizers (e.g., a benefit for the jobless that automatically spends out more when more people lose jobs)

*Algorithmic* automatic stabilizers (e.g., a jobless person gets more when unemployment is higher).

Three considerations on algorithmic auto stabilizers:

1. A better default than the current one. Congress already makes changes in recessions, And it still can/will then make discretionary adjustments even if we had algorithmic stabilizers because it wants to be seen as acting.

1. A better default than the current one. Congress already makes changes in recessions, And it still can/will then make discretionary adjustments even if we had algorithmic stabilizers because it wants to be seen as acting.

2. Not something that we should expect to fully rely on, will still need a discretionary Fed (including amplifying or undoing the automatic stabilizers in a discretionary manner). Can't fully automate to end recessions--just like Taylor/NGDP/etc. rule should not be automated.

3. Most appealing when there is an additional non-macro argument for them.

Higher benefits for a family at $30K and higher taxes for a family at $3m is a *normal* stabilizer with a strong distributional rationale (in my view). But policy parameters do not vary with the economy.

Higher benefits for a family at $30K and higher taxes for a family at $3m is a *normal* stabilizer with a strong distributional rationale (in my view). But policy parameters do not vary with the economy.

(Con't) The *algorithmic* version, eg varying the parameters so someone at $30K gets more when there is higher unemployment has less non-macro rationale--their need doesn't go up just because others are in difficulty.

My two favorite algorithmic automatic stabilizers that vary the parameters based on the economy both have a rationale beyond just macro:

1. unemployment insurance levels and duration (optimal depends on UR)

2. State/local transfers (undoes balanced budget cuts)

1. unemployment insurance levels and duration (optimal depends on UR)

2. State/local transfers (undoes balanced budget cuts)

Finally, the best automatic stabilizer is a a normal one: a larger government & a more progressive fiscal system without time varying parameters. Of course raises bigger values etc. issues than the technocratic algorithmic approaches so no surprise lack of universal agreement.

Loading suggestions...