So I'm writing a thread after a very long time and this one is going to be about a small company that is growing fast in a growing sector and is available at reasonable valuations.

And the name of the company is - HARI OM PIPE INDUSTRIES

So let's get started

And the name of the company is - HARI OM PIPE INDUSTRIES

So let's get started

Let's start with the company' business first, what does the company actually do.

So HARI OM INDUSTRIES founded in 2007 is an integrated n integrated manufacturer of Mild Steel (MS) Pipes, Scaffolding, HR Strips, MS Billets, and Sponge Iron.

So HARI OM INDUSTRIES founded in 2007 is an integrated n integrated manufacturer of Mild Steel (MS) Pipes, Scaffolding, HR Strips, MS Billets, and Sponge Iron.

So let's look at the product portfolio one by one.

They manufacture -

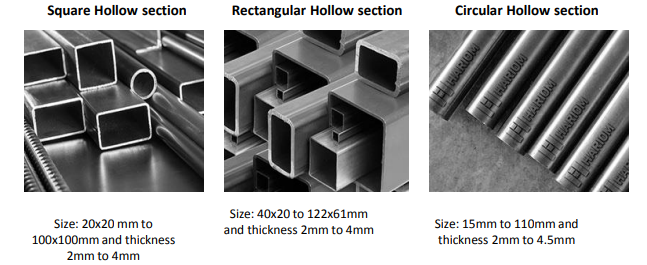

1. MS (Mild steel ) Tubes and Pipes ranging from 19.5mm to 127.5mm outer diameter with thickness ranging from 1 to 3.5mm.

These are mainly used for commercial and residential construction.

They manufacture -

1. MS (Mild steel ) Tubes and Pipes ranging from 19.5mm to 127.5mm outer diameter with thickness ranging from 1 to 3.5mm.

These are mainly used for commercial and residential construction.

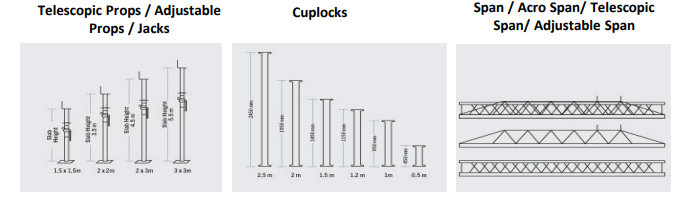

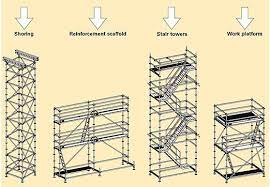

2. Scaffoldings Systems- These are temporary work platform on a construction site. These scaffolding are used for conducting construction activities above the ground level.

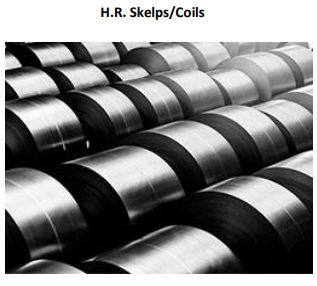

3. HR Strips - The company manufactures H.R Skelps and Coils in various shapes and sizes as per the requirement of customers. It is majorly used in Industrial cable trays and different industrial setups.

4. MILD STEEL BILLETS - The freshly made steel, which is still in the form of a metal bar or rectangle, is called billets.

MS Billets is a key input for rolling mill to product HR trips. These are used to make round bar, flat bar, angle plate, spring steel, wire rod etc.

MS Billets is a key input for rolling mill to product HR trips. These are used to make round bar, flat bar, angle plate, spring steel, wire rod etc.

5. SPONG IRON - Sponge iron is a metallic product produced through direct reduction of iron ore in the solid state It is a substitute for scrap and is mainly used in making steel through the secondary route The process of sponge iron making aims to remove the oxygen from iron ore

The company has two manufacturing units - One at Mahbubnagar, Telangana for Rolling mills, scaffolding, piping mill, Induction Furnace etc.

And 2nd Plant at Anantapur, AP for Sponge Iron which they recently acquired.

And 2nd Plant at Anantapur, AP for Sponge Iron which they recently acquired.

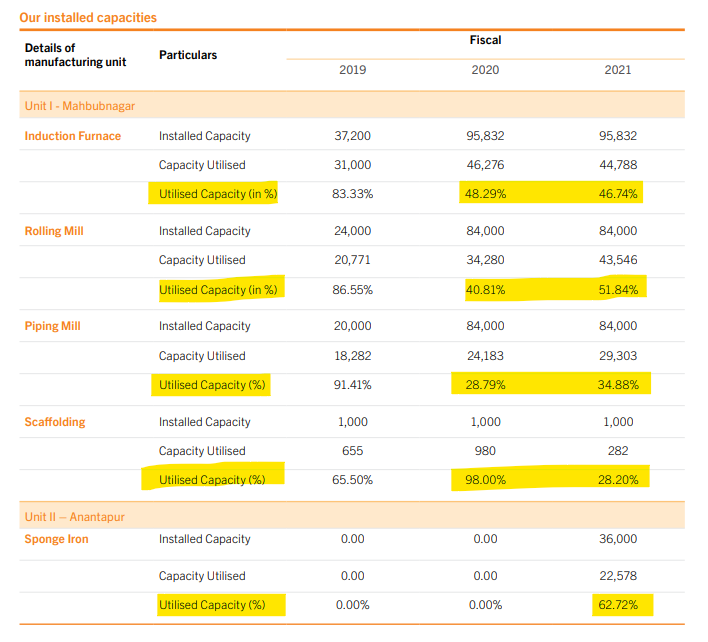

For most of the products, capacity utilization is down to 48-50% from 60-905 in 2019.

The Sponge Iron facility has capacity utilization around 62.72% with total capacity of 36,000 MTPA

The Sponge Iron facility has capacity utilization around 62.72% with total capacity of 36,000 MTPA

Capacity expansion - Company is expanding it's capacity for MS Pipes in Unit - 1 from 84,000 MTPA to 1,32,000 MTPA and Furnace capacity from 95,832 MTPA to 1,04,232 MPTA.

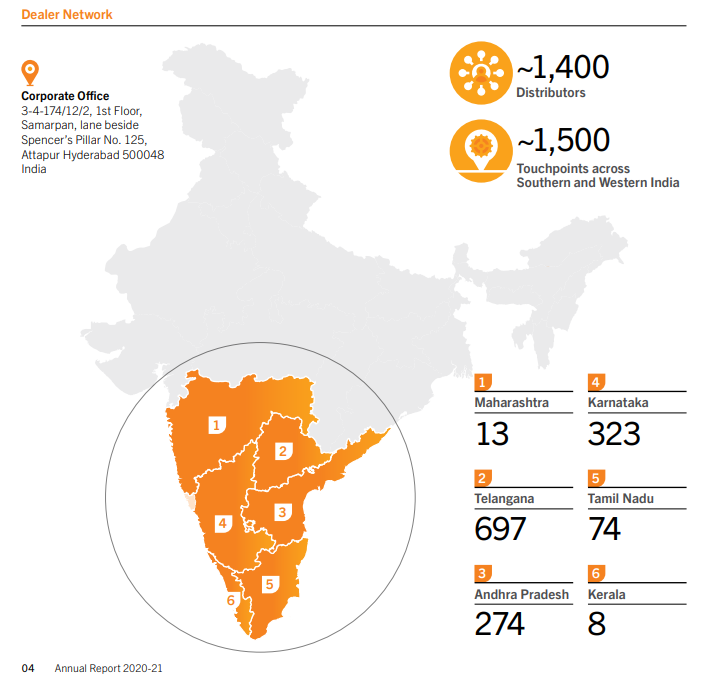

The company mainly has presence in South India with 1,400 distributors and 1,500 touchpoints in 6 states.

What makes them special is that they have integrated operations.

They themselves produce Sponge Iron from Iron Ore which is used to make final products like MS Pipes, Scaffoldings etc.

For example, MS Billets can be sold independently or maybe used as input for rolling mills.

They themselves produce Sponge Iron from Iron Ore which is used to make final products like MS Pipes, Scaffoldings etc.

For example, MS Billets can be sold independently or maybe used as input for rolling mills.

Further the output of Rolling mills i.e. HR Strips can be sold independently and can be used as an input to manufacture MS Pipes.

Both manufacturing plants are at strategic location -

Both manufacturing plants are at strategic location -

The company is eligible for obtaining private power from IEX thorough online bidding process in case of shortage.

They have installed pollution control equipment at their smoke emanating chimney that collects the dust particles which are then sold to cement companies.

They have installed pollution control equipment at their smoke emanating chimney that collects the dust particles which are then sold to cement companies.

The company is expanding their product portfolio and adding more "value-added products" like - Rust Free MS Pipes, End Facing of MS Pipes, Packaging.

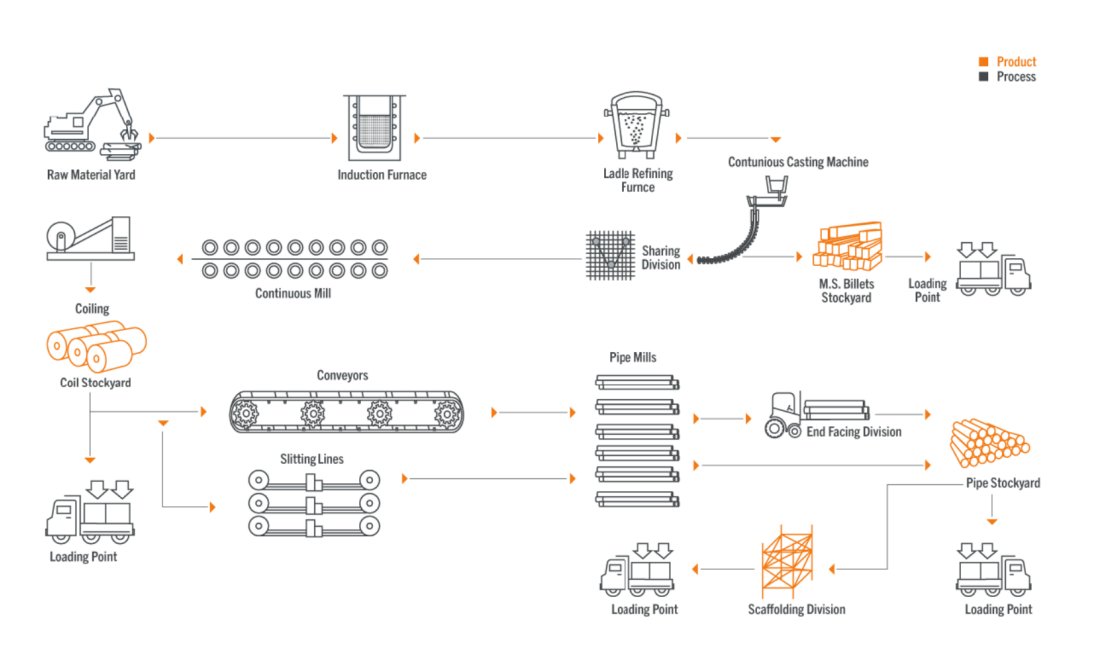

Production process of Unit 1 -

The steel-melting scrap and sponge iron in the ratio of 30/70 are processed in the induction furnace producing MS Billets, which are then used as an input for the rolling mill to produce HR Strips

The steel-melting scrap and sponge iron in the ratio of 30/70 are processed in the induction furnace producing MS Billets, which are then used as an input for the rolling mill to produce HR Strips

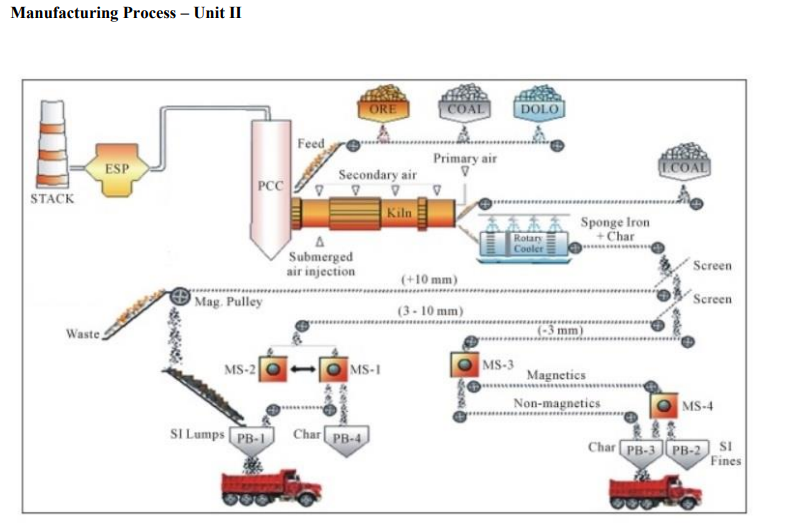

Production Process of Unit 2 -

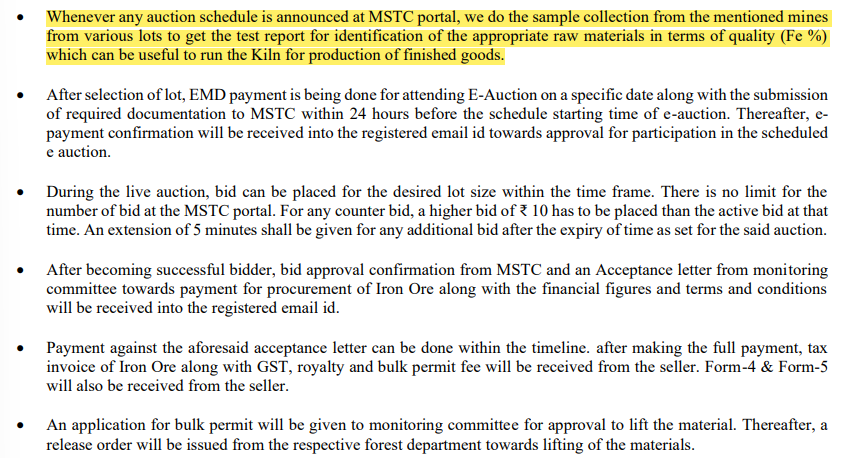

The company has registered on MSTC E-Auction to procure the scrap.

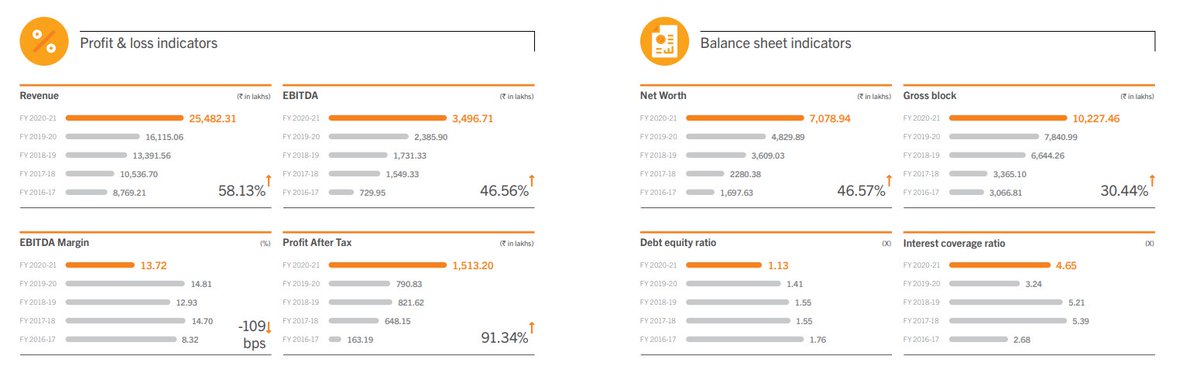

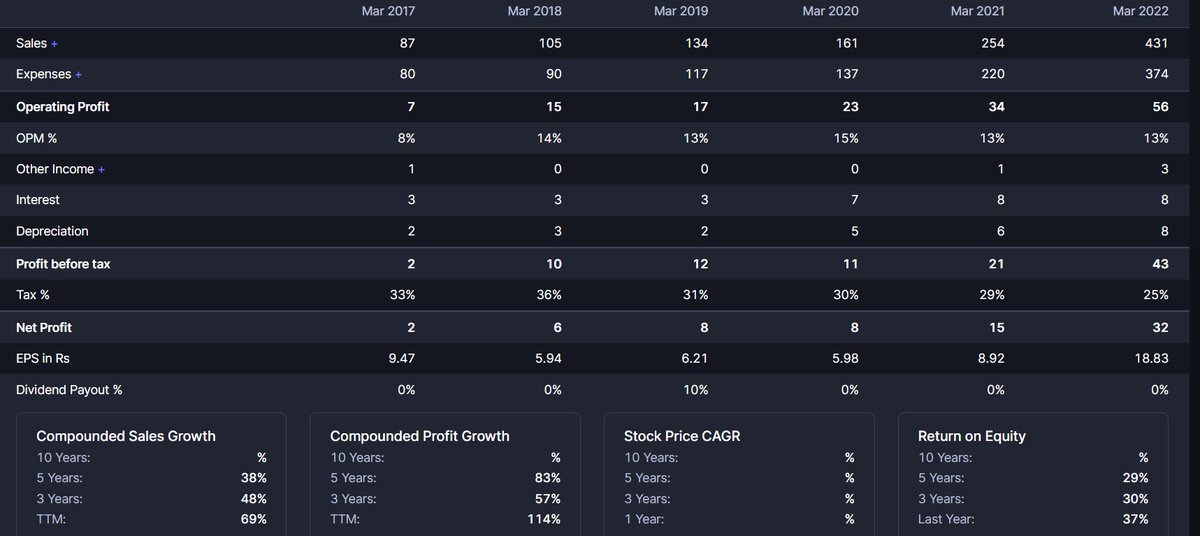

Now let's take a look at numbers -

The Company has consistently growth it's revenue from last 5 years with EBIDTA Margins in the range of 12-14%

Debt to Equity is still high but down from 1.76 to 1.13

Last 5 year sales CAGR is at 38%

The Company has consistently growth it's revenue from last 5 years with EBIDTA Margins in the range of 12-14%

Debt to Equity is still high but down from 1.76 to 1.13

Last 5 year sales CAGR is at 38%

Margins are better as compared to APL Apollo due to the backward integration and different product portfolio.

CCC and WCC are high because they have to maintain inventory as they directly sell to the dealer instead of keeping stockist.

CCC and WCC are high because they have to maintain inventory as they directly sell to the dealer instead of keeping stockist.

Plus they are negatively affected by the steel price fluctuation and have to face inventory losses sometimes.

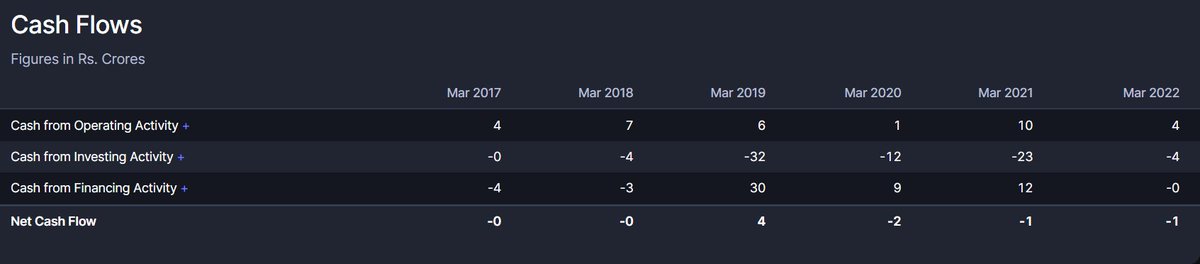

Plus very poor cash flows.

Plus very poor cash flows.

High Dependence on top 10 customers -

Our top 10 customers contributed 60.74% and 49.78% of total sales for the Fiscal 2021 and 2020 respectively.

Our top 10 suppliers contributed 56.32% and 50.35% of total purchases Fiscal 2021 and 2020 respectively.

Our top 10 customers contributed 60.74% and 49.78% of total sales for the Fiscal 2021 and 2020 respectively.

Our top 10 suppliers contributed 56.32% and 50.35% of total purchases Fiscal 2021 and 2020 respectively.

High geographical concentration - Telangana 41%, Karnataka 25%, Tamil Nadu 20%, Andhra 10%,

balance to Maharashtra, Pondicherry, Goa, Kerala, Punjab, etc.

EBIDTA per ton is around 8000 - 8500rs

balance to Maharashtra, Pondicherry, Goa, Kerala, Punjab, etc.

EBIDTA per ton is around 8000 - 8500rs

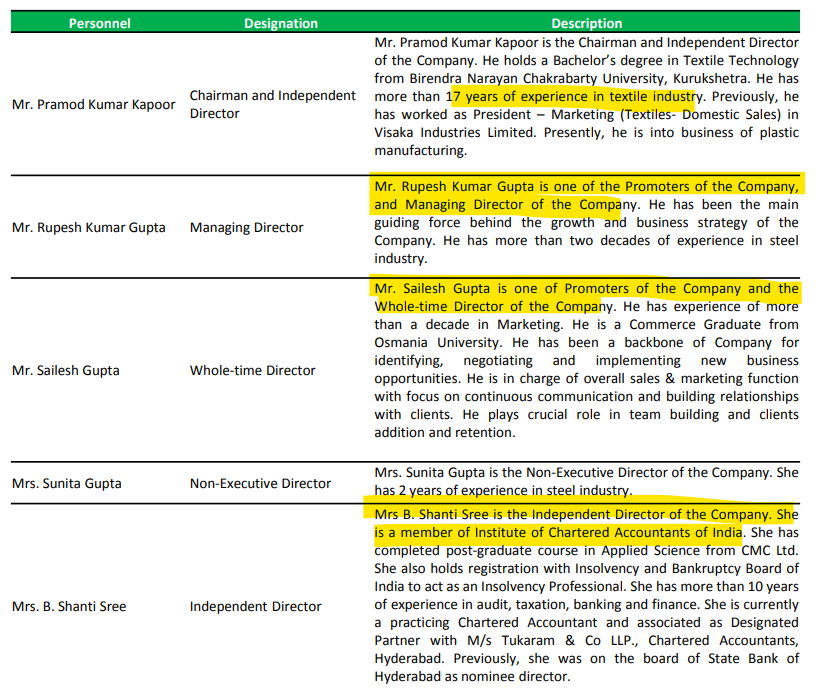

Now let's take a look at the management team -

The business is family run and MD are Directors are related.

The business is family run and MD are Directors are related.

Have already discussed the negative points.

It's a risky business as it is a commodity business which is cyclical in nature.

It's a risky business as it is a commodity business which is cyclical in nature.

Don't forget to like, share and re-tweet

@soicfinance @ishmohit1 @sahil_vi @suru27 @badola_arjun @shubhfin @shivang_ran @abhymurarka

Re-tweet the 1st tweet -

@soicfinance @ishmohit1 @sahil_vi @suru27 @badola_arjun @shubhfin @shivang_ran @abhymurarka

Re-tweet the 1st tweet -

Loading suggestions...