Motilal Oswal has identified 0.5 PEG as one of possible wealth creation indicators.

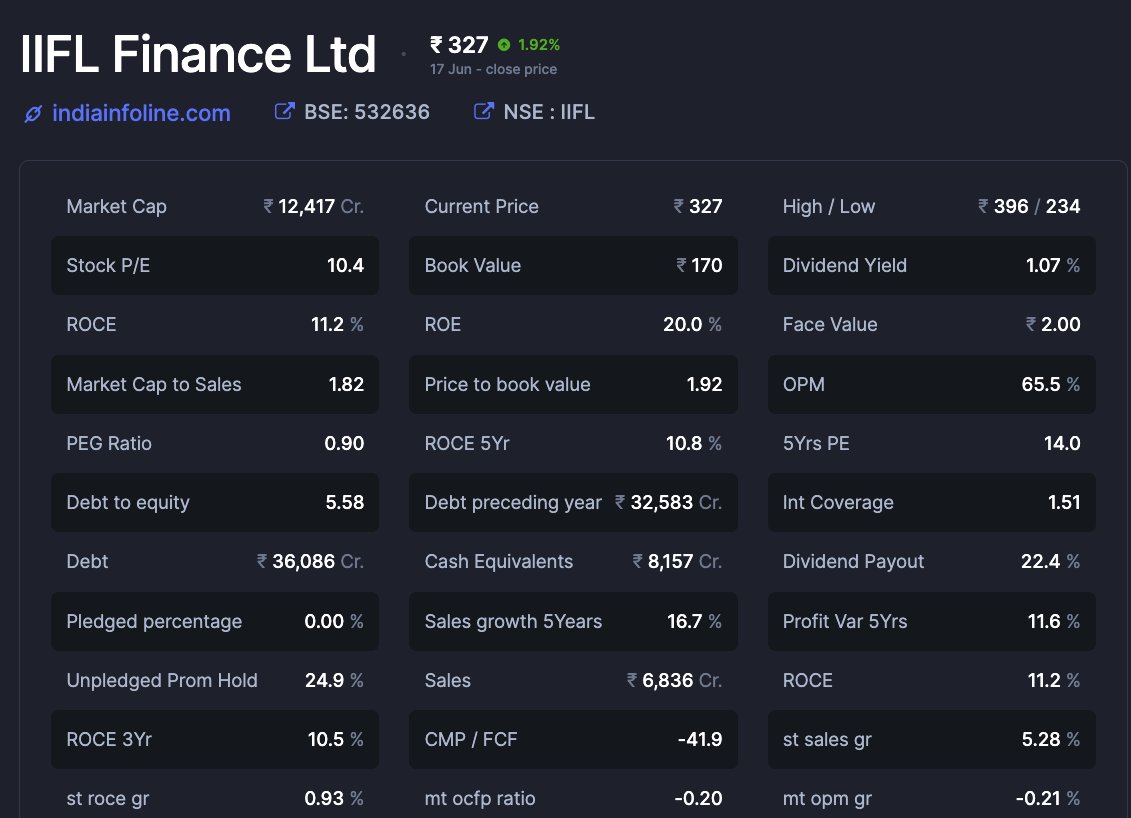

IIFL Finance is at a P/E of 9-10. Can grow 20-25% in next 3 years. Do the math. 🙏

IIFL Finance 2022 AR 🧵🧵⤵️

IIFL Finance is at a P/E of 9-10. Can grow 20-25% in next 3 years. Do the math. 🙏

IIFL Finance 2022 AR 🧵🧵⤵️

If you haven't consider reading this thread as a primer to IIFL Finance:

Let's dive into the AR then.

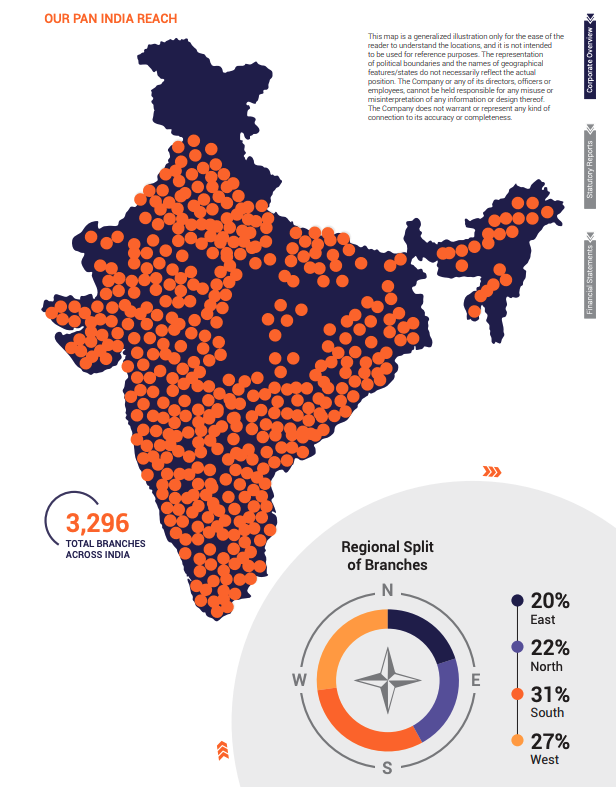

Scale - 1

3,296 branches

in 1,260 towns/cities

22% of those branches added in FY22. Imagine the operating leverage built in.

Scale - 1

3,296 branches

in 1,260 towns/cities

22% of those branches added in FY22. Imagine the operating leverage built in.

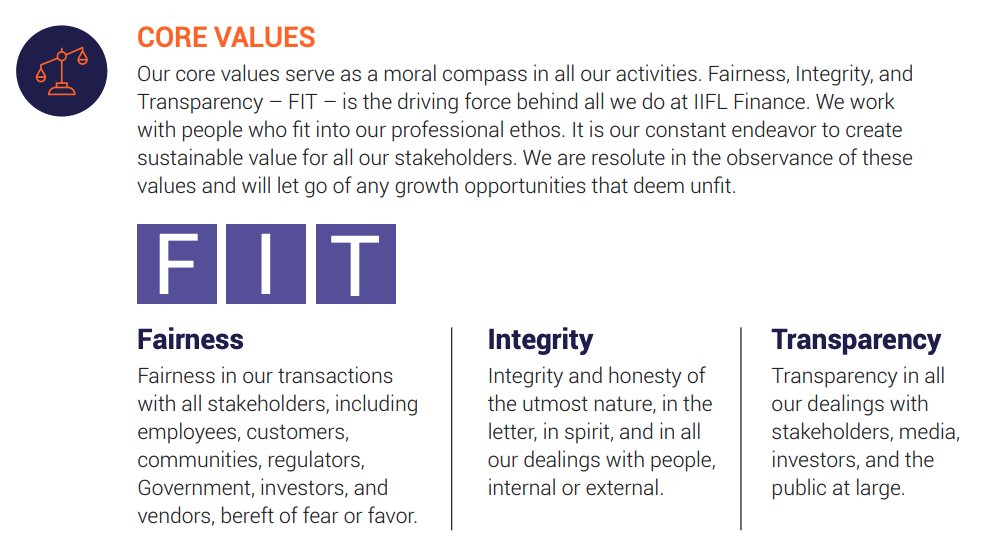

There seems to be a fair amount of focus on MQ & creating value for all stakeholders in this year AR.

FIT: Fairness, Integrity, Transparency

Willing to let go of growth which does not 'fit'. If they can walk the talk on this, can be huge.

FIT: Fairness, Integrity, Transparency

Willing to let go of growth which does not 'fit'. If they can walk the talk on this, can be huge.

Scale - 2

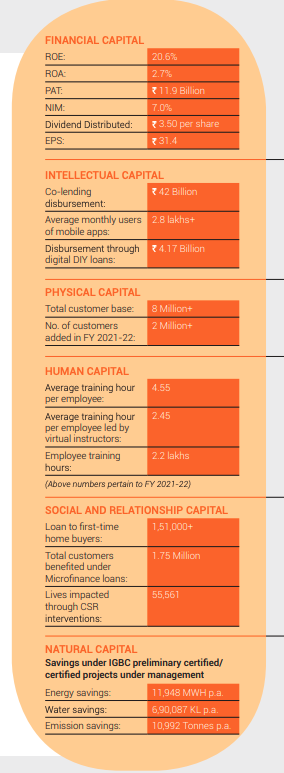

8 mill customers (25% growth).

51,000 cr AUM

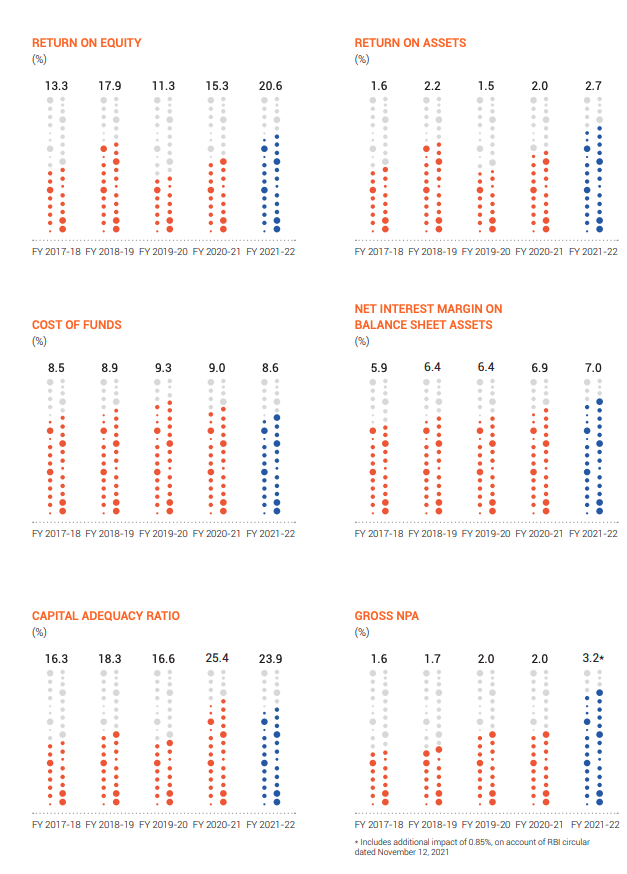

20% ROE

165 Rs BV/share

87% Branches in Tier 2/3 (lending to the underserved)

8 mill customers (25% growth).

51,000 cr AUM

20% ROE

165 Rs BV/share

87% Branches in Tier 2/3 (lending to the underserved)

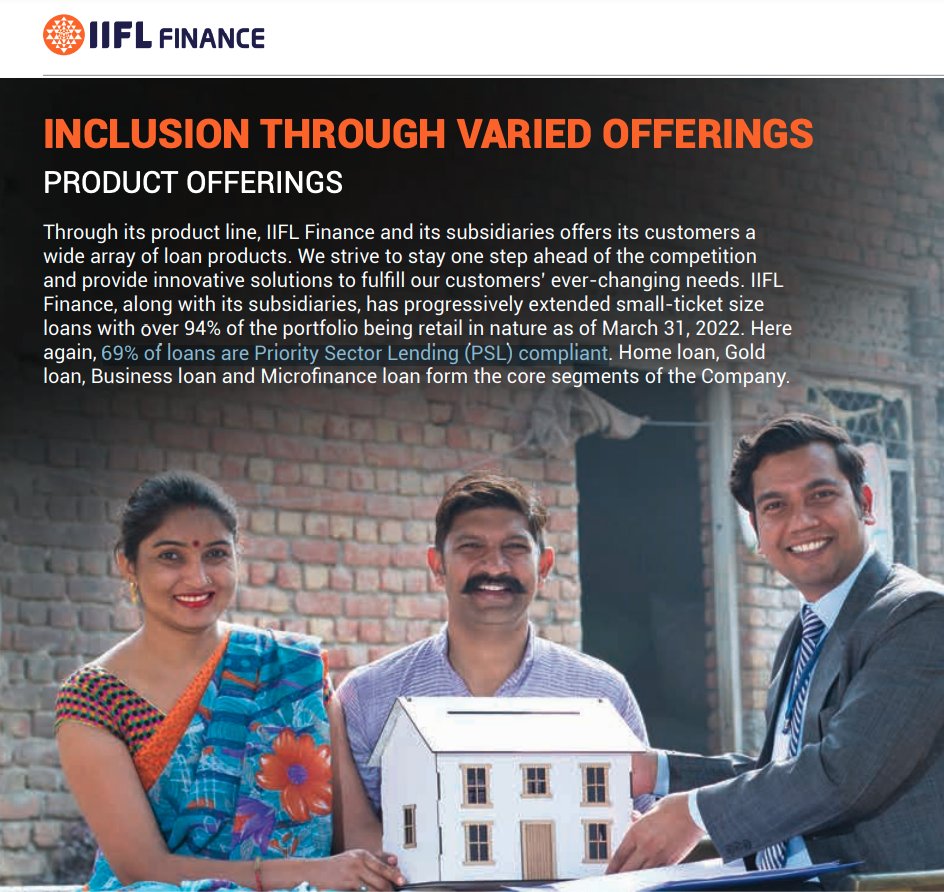

With 94% of loans being retail in nature & 69% loans being PSL compliant, the risk associated with blowup of large corporates has been largely handled in IIFL now.

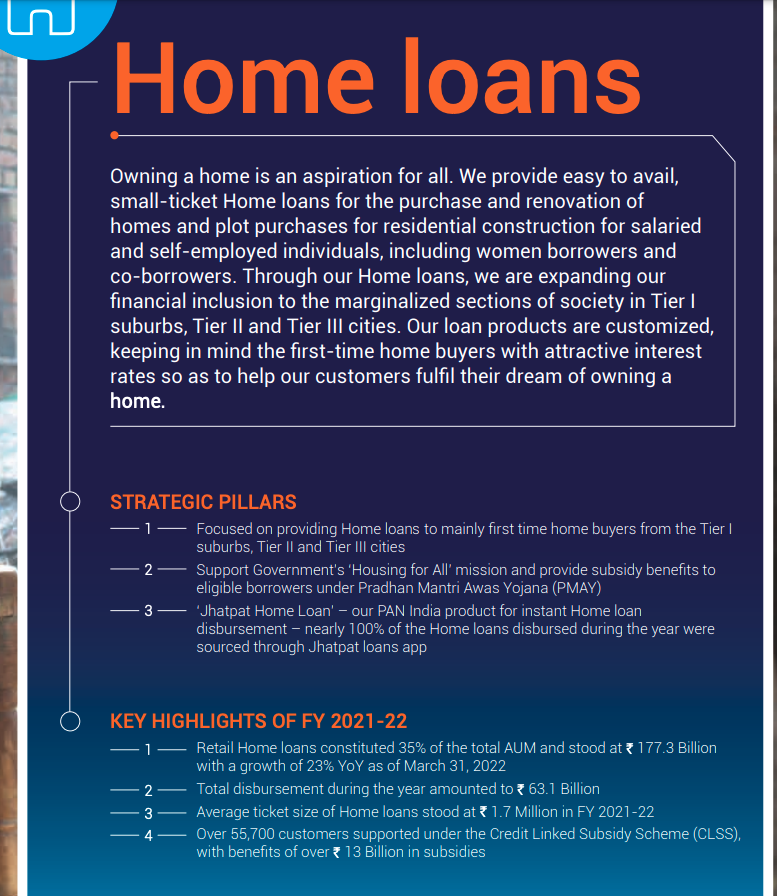

The size of affordable housing market is 13 lakh crore rupees in 2025. Even today it is 9 lakh crores. The opportunity size is huge.

So How will IIFL win the home loan market? By focussing on digital, focussing on 1st time home buyer, by focussing on tier 2/3, 1 suburbs

Apparently the ADIA investment will be key in helping IIFL penetrate deeper into affordable housing

moneycontrol.com

moneycontrol.com

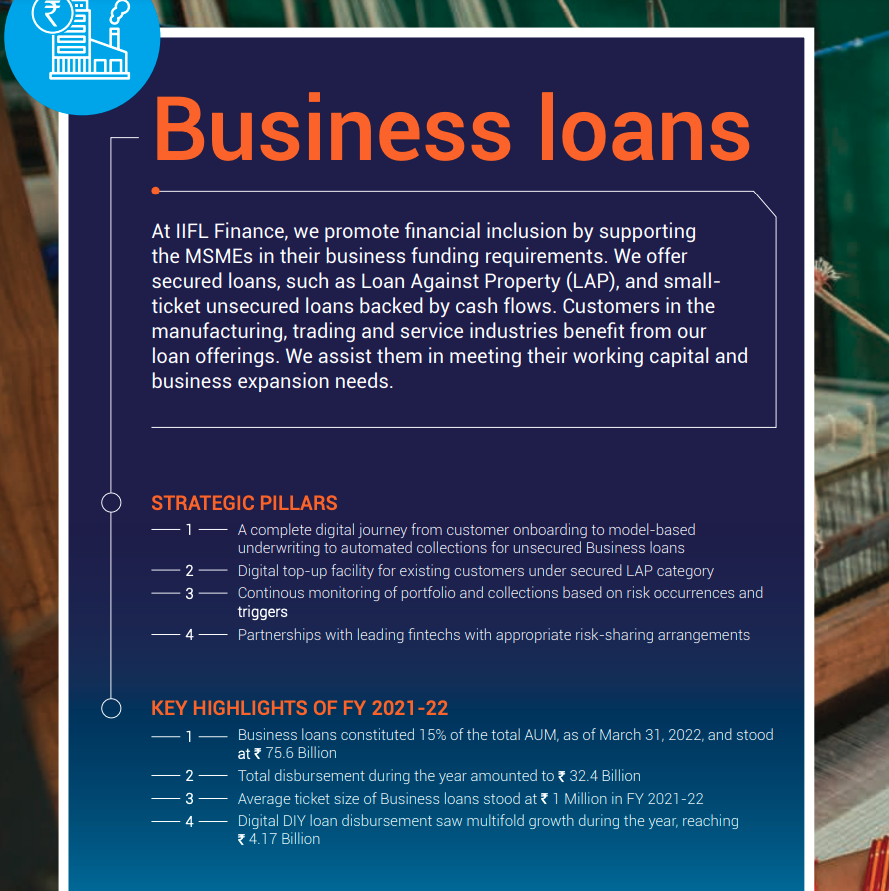

On the business loan side, their strategy is to use LAP to fund capex & WC for manufacturing, trading, services. Want to do customer onboarding, underwriting & collections using digital means.

Currently 15% of AUM.

Currently 15% of AUM.

The TAM for MSME finance is huge. Only 16% of MSME receive formal credit. There is a 25 lakh cr funding gap in MSME sector.

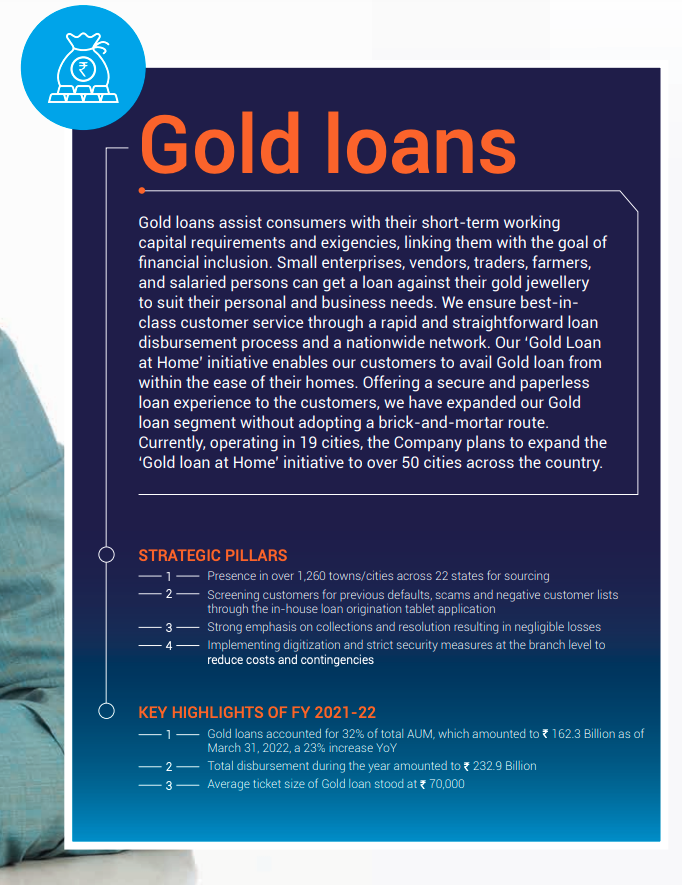

Gold loan market by comparison, seems more mature. Would probably grow slower.

The strategy in this biz unit is to focus on screening customers for previous defaults, scams, & strict security measures to reduce loan losses.

Even the gold loan AUM has grown 23% YoY.

Even the gold loan AUM has grown 23% YoY.

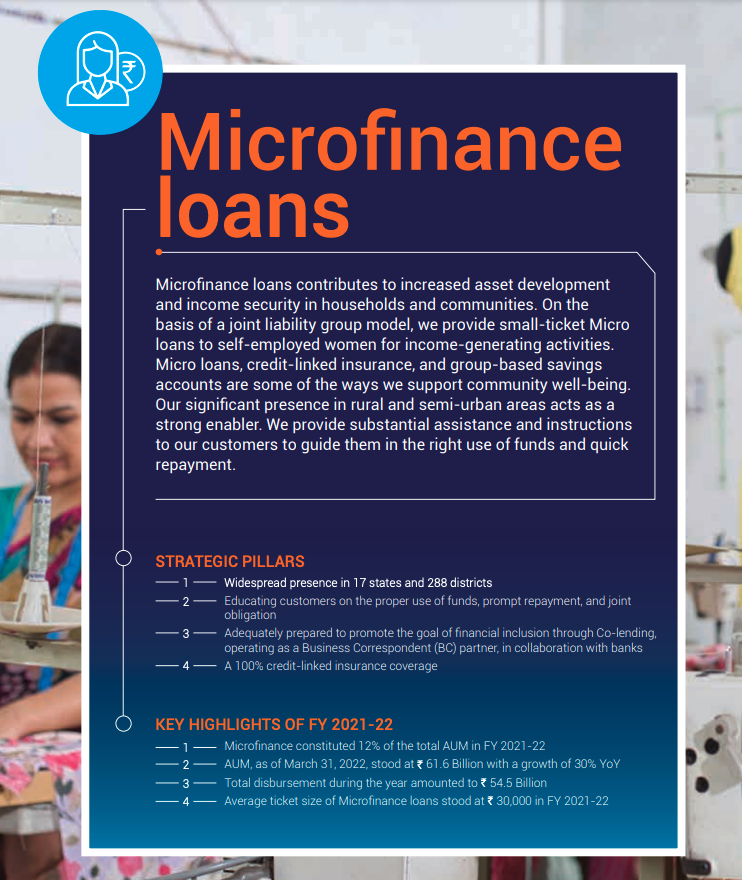

IIFL through IIFL Samasta finance provides small ticket loans to joint liability groups of self employed women for income generating activities. 30% AUM growth here YoY

This is a 2.5 lakh cr market growing at 40% CAGR until 2025. Large & expanding TAM

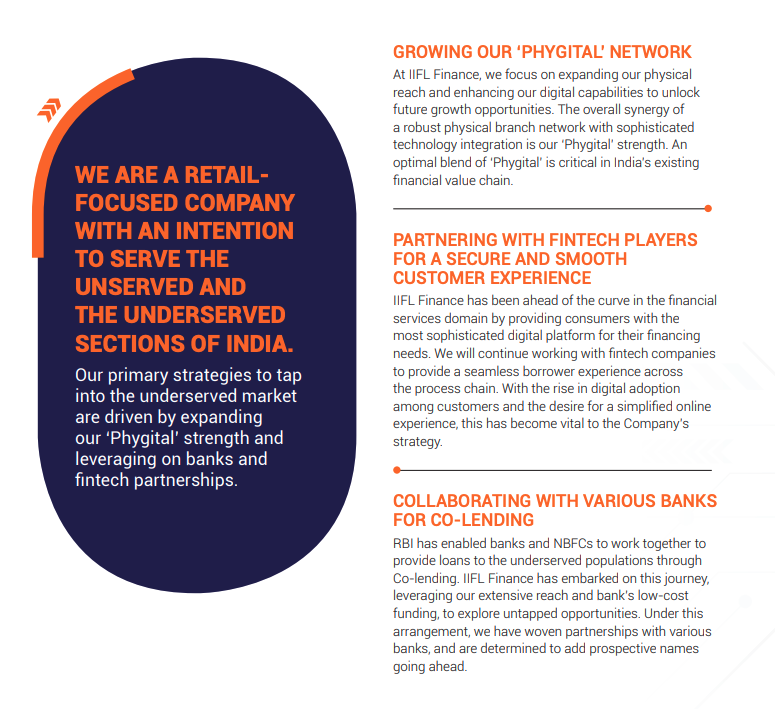

If we had to summarise the strategy:

1. Phygital growth

2. Fintech partnerships

3. Co-lending with banks

1. Phygital growth

2. Fintech partnerships

3. Co-lending with banks

Innovation:

To reach a large customer base in a low way, became the first NBFC in India to launch instant business loan on WhatsApp, covering the complete end-to-end journey of the customer

To reach a large customer base in a low way, became the first NBFC in India to launch instant business loan on WhatsApp, covering the complete end-to-end journey of the customer

20.6% ROE through 2.7% ROA, 7% NIM.

1.5 lakh loans to first time home buyers.

1.5 lakh loans to first time home buyers.

Biggest concern remains on asset quality side. IIFL talks about rbi circular impact. Are you the only NBFC in town? Why didnt any others see NPA rise due to rbi circular? However, modulo that, great job scaling up ROE, ROA, NIMS.

The thing i absolutely love to see in my lender? Geographical diversification. Otherwise too much political & geographical concentration risk. IIFL does great on this.

IIFL can now lend 10 lakh rupees in 10 minutes through whats app

Cutting friction can definitely help increase credit offtake. 1st such lender in India. ML models for underwriting.

Cutting friction can definitely help increase credit offtake. 1st such lender in India. ML models for underwriting.

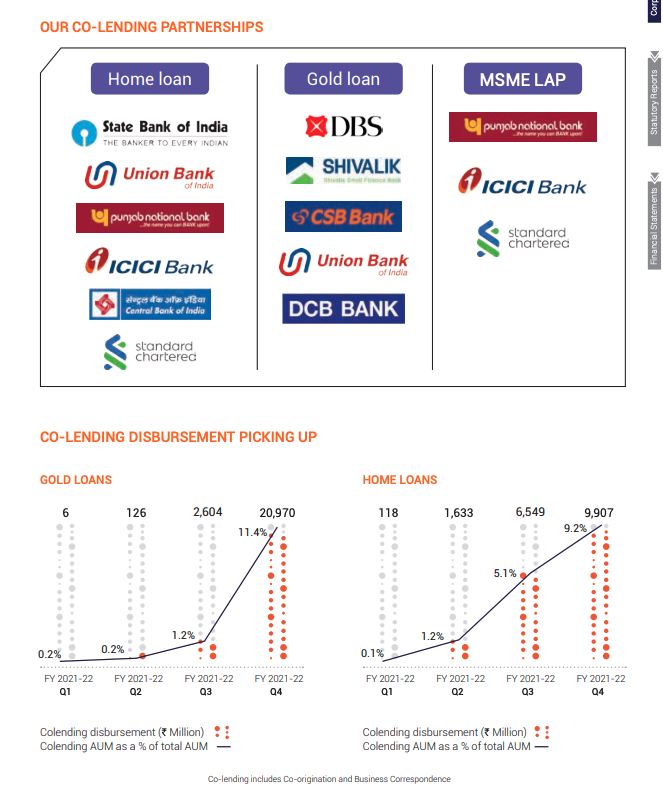

Co-lending partnerships with SBI, ICICI bank, CSB, DCB, Stan Chart

Gold loan co-lending AUM already 2097 cr. Hold loan AUM 991 cr. Still in nascent stage & can definitely scale up from here.

Gold loan co-lending AUM already 2097 cr. Hold loan AUM 991 cr. Still in nascent stage & can definitely scale up from here.

Understanding a whitespace for MSME banking, IIFL also created a JV with "open" to improve MSME banking: current account, inventory management, taxes, sales, PDS machine, chequebook, loans, debit cards, micro ATMs, QR codes

Guidance: 2B$ lending book in 2Y.

Guidance: 2B$ lending book in 2Y.

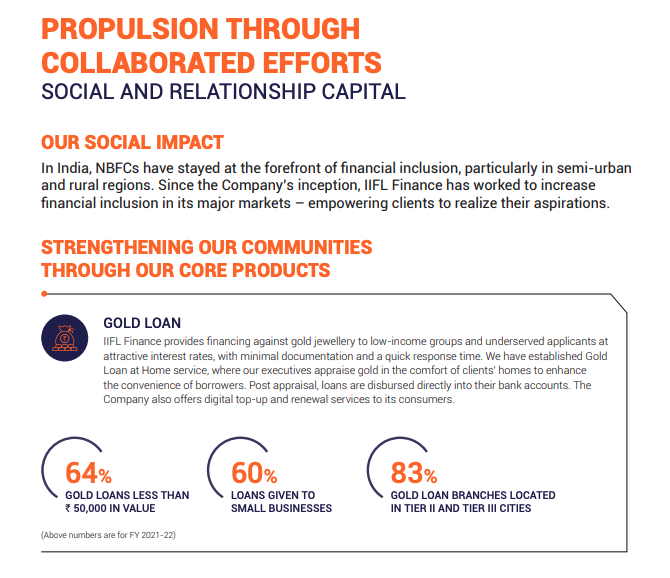

IIFL's gold loan drive financial inclusion with 83% branches in tier 2/3 cities & 64% gold loans < 50k in value.

Fact that 60% of gold loans are given to small businesses ensure that these are productive biz loans & thus generating good ROE.

Fact that 60% of gold loans are given to small businesses ensure that these are productive biz loans & thus generating good ROE.

Tanaji wadekar is a pandit. He was turned down for a home loan due to lack of income proof. IIFL provided him a home.

A bit on valuations:

A P/E of 10, check.

A P/E of 10, check.

Guidance to grow 20-25%, Check.

That makes it a possible PEG of 0.5

These generally do well if they can control asset quality.

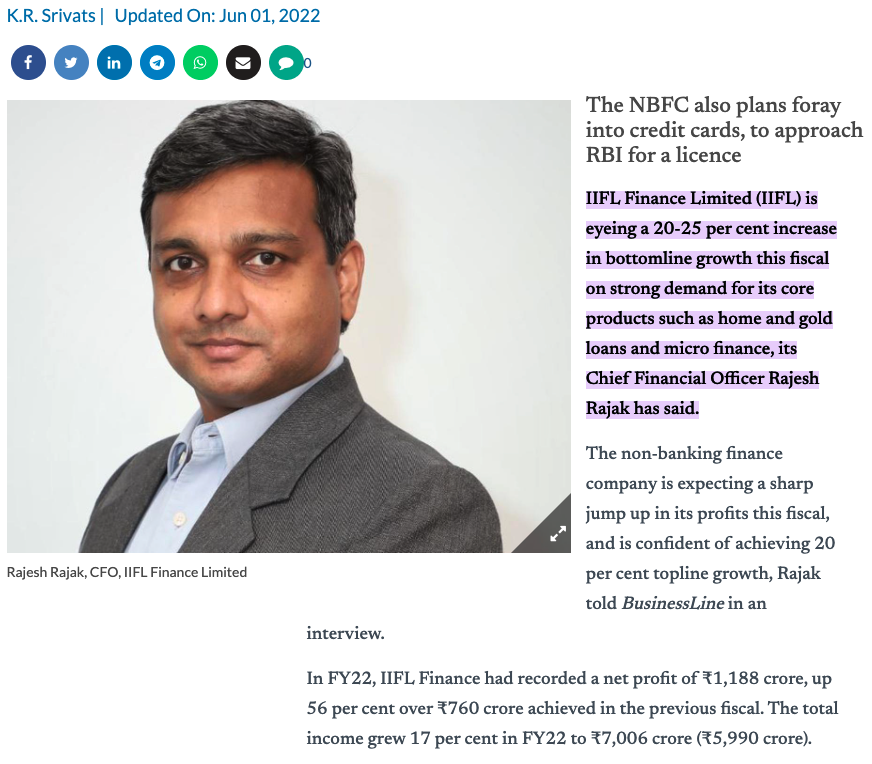

thehindubusinessline.com.

That makes it a possible PEG of 0.5

These generally do well if they can control asset quality.

thehindubusinessline.com.

Link to some other company analysis threads i have written in the past:

Consider following me at @sahil_vi if you find this thread useful. I write such threads once in a while.

Happy weekend

<End of thread>

Consider following me at @sahil_vi if you find this thread useful. I write such threads once in a while.

Happy weekend

<End of thread>

Loading suggestions...