Putting some context on what I meant here-

By J-curve one would expect a non-linear growth, which will happen when you go from manufacturing say 10-50-100-500kg, over the course of Phase-I,II,III & then commercial.

By J-curve one would expect a non-linear growth, which will happen when you go from manufacturing say 10-50-100-500kg, over the course of Phase-I,II,III & then commercial.

However, in case of Syngene there are multiple pointers that indicate that this might not happen for the Mangalore facility-

One would expect that given a large CRO with multiple projects, Syngene would have a ready pipeline of projects to feed into its manufacturing business.

One would expect that given a large CRO with multiple projects, Syngene would have a ready pipeline of projects to feed into its manufacturing business.

This is what my understanding was when I invested in 2019. But that is not what management here has articulated. See snippets-

Though Syngene has started taking up integrated projects wherein that J-Curve will happen, but for next couple of years it will have to build up project pipeline for its manufacturing business from scratch.

And given the size of capacity, it would not be something that can be achieved in just 1-2 years. Even the management here has said multiple times that the capacity will be utilized fully in a period of 3-5 years only and not overnight.

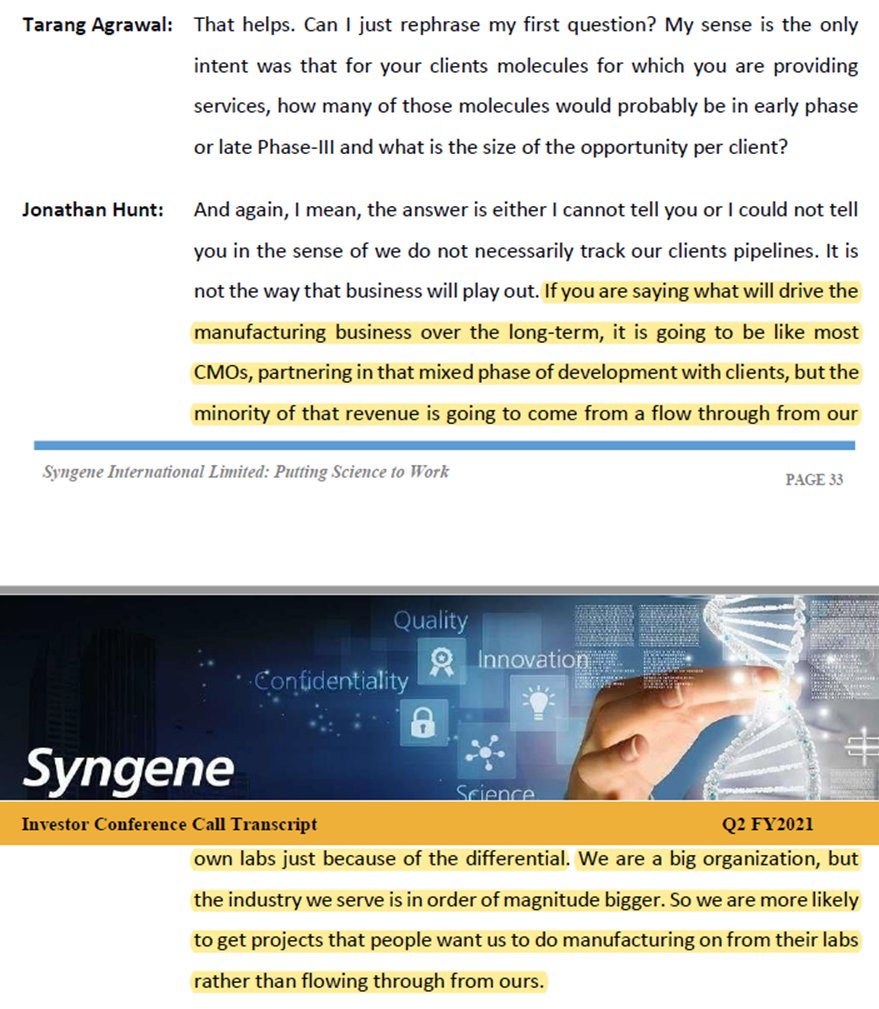

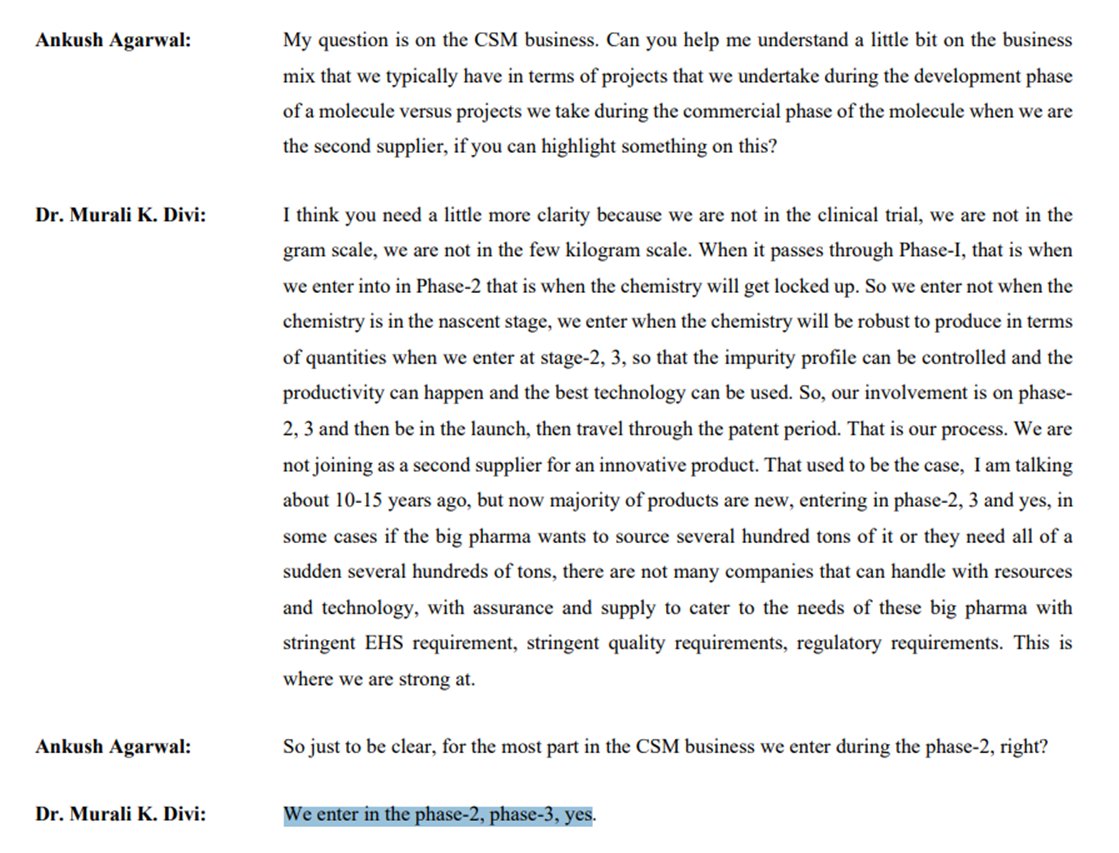

It would be more of a gradual scaleup wherein It will do commercial manufacturing work wherein innovator wants manufacturing services of commercial products not necessarily all the way starting from Phase-1 but at different stages. This is where the comparison with Divis was made

Add to this would be generic CMO opportunities as well, wherein it would be something like what Laurus does in its custom synthesis business for a customer like Aspen wherein though it is not an NCE product, but CMO for value added product on one-to-one basis.

So, it would be a mix of own development led integrated projects, NCE projects at different phases of NCE that requires high volume commercial manufacturing scale and some value added generics. And thus, a more of a gradual scale-up over the years.

Suven on the other hand is one that can see J-Curve primarily because they start at very early stage Phase-1 wherein they might start with just a couple of Kgs & then scales multi-fold & it does not have any other business like say CRO part in Syngene or Generic APIs in Divis.

And thus overall growth in business can be a J-Curve.

This is not to say that Suven has the best business model. Over the years having focused on a lot of non-linear growth opportunities, one thing that I have realized is that there is no free ride of non-linear growth without the risks of volatility and large de-growths as well.

And thus, a combination of secular/stable + non-linear growth business is a better investment vs a pure linear or pure non-linear business. And this is why Suven’s addition of a generic formulations business is a good thing for an investor. It would add some base stable business.

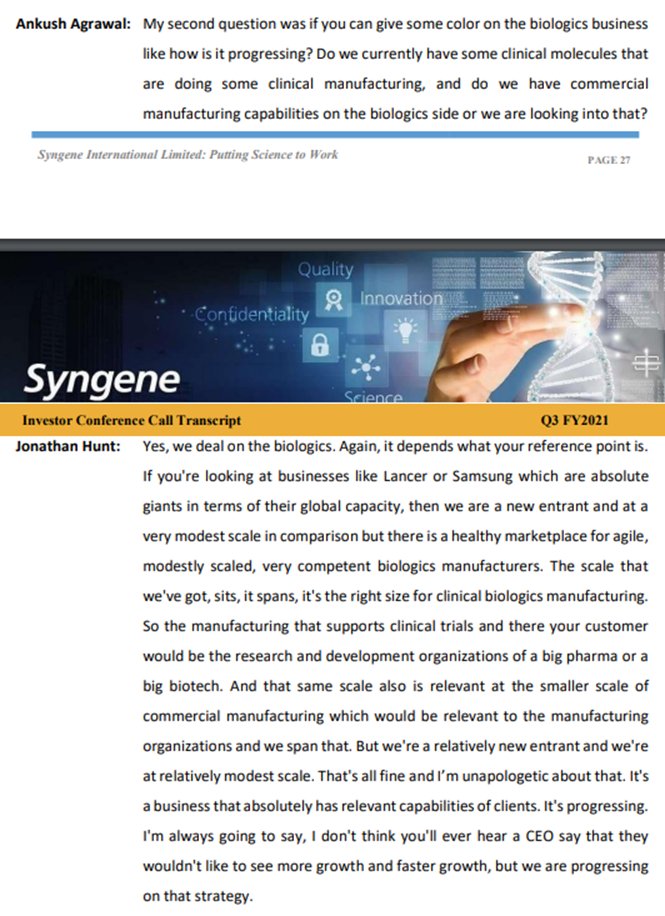

Also, on those who think that Syngene will grow big time into Biologics and do comparison with someone like Wuxi, read this-

Lastly, I’ll just that I am not negative or biased on Syngene. I think it is one of the few businesses that will see secular growth year after year for many-many years to come and what they do is real value addition work.

But it is the expectations that investors need to tame you can’t expect a Wuxi like growth here, the whole Wuxi comparison is full narrative.

I was invested here very early in 2019 and then benefited from the whole CRAMS hype in 2020 that led to sharp rerating here. But when the management said that their own CRO work will not flow into manufacturing, it just turned my thesis upside down.

I invested here with an understanding that, given a large CRO business, if Syngene adds a manufacturing piece, it could easily capitalize on the work that it has already done in the discovery & development front.

Not to add the execution is not the best here. They took nearly 6-7 years to create this capacity and then will take another 3 years into approval. Pains me to say, but Biocon group does not have the best track record when it comes to execution.

Have had same experience in Biocon as well, wherein even after having the 1st mover advantage in Biosimilars, they have not been able to execute.

Loading suggestions...