The Basics of a Balance Sheet explained from scratch 🧮➕➖➗

In this thread we will talk about -

1. What is Balance Sheet

2. How Balance Sheet is made?

3. Each line items of Balance Sheet

4. Why it is important

Retweet for max reach!

In this thread we will talk about -

1. What is Balance Sheet

2. How Balance Sheet is made?

3. Each line items of Balance Sheet

4. Why it is important

Retweet for max reach!

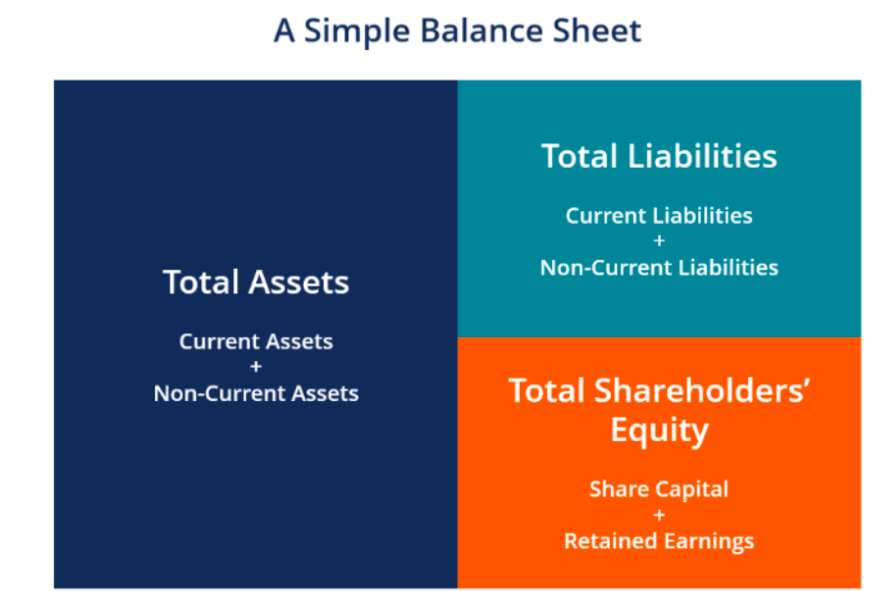

What is a Balance Sheet:

The balance sheet displays the company’s total assets and how the assets are financed, either through debt or equity. It gives an idea of the financial health of an organization. It is like a snapshot of the financial position at a specified time.

The balance sheet displays the company’s total assets and how the assets are financed, either through debt or equity. It gives an idea of the financial health of an organization. It is like a snapshot of the financial position at a specified time.

Balance sheet consists of 3 components:

1⃣Assets

2⃣Equity

3⃣Liabilities

The balance sheet is based on the fundamental equation: Assets = Equity + Liabilities.

This is also the golden rule of Finance!

1⃣Assets

2⃣Equity

3⃣Liabilities

The balance sheet is based on the fundamental equation: Assets = Equity + Liabilities.

This is also the golden rule of Finance!

Now let’s dig into each line item on the Balance sheet and understand why the Balance sheet always tallies.

Let’s see how actual balance sheet looks like:

Let’s see how actual balance sheet looks like:

The first part of the BS is Assets.

Assets are those resources or things which the company owns. They can be divided into current as well as non-current assets or long term assets.

Non-current assets: Assets which cannot be easily converted to cash. Like buildings, machinery.

Assets are those resources or things which the company owns. They can be divided into current as well as non-current assets or long term assets.

Non-current assets: Assets which cannot be easily converted to cash. Like buildings, machinery.

Current assets: Assets which can be easily converted into cash within a duration of one year. Examples are short-term deposits, marketable securities, and stock.

The first line item of Non-current assets is Property, Plant & Equipment (PP&E), PP&E captures the company’s tangible fixed assets. Tangible assets are those which can be seen and felt. They have physical form.

The line item is recorded net of accumulated depreciation. PP&E is classified into different types of assets, like Land, Building, Office Equipment, Vehicles, computers etc. All PP&E are depreciable except for Land.

The next line item is Capital Work in Progress (CWIP): Those assets which are in the construction phase or are being built are termed as CWIP. These assets will move to PP&E once construction is completed.

High CWIP as % of PPE can also be used as a screening filter for selecting companies, as high CWIP will eventually mean a company is adding a new plant and will generate more revenue in the near future.

The other item is Intangible Assets

This line item includes all of the company’s intangible fixed assets, which may or may not be identifiable. Intangible assets include patents, licences, brand, software and goodwill.

This line item includes all of the company’s intangible fixed assets, which may or may not be identifiable. Intangible assets include patents, licences, brand, software and goodwill.

It also includes Goodwill due to acquisition of another company, for example Company A buys Company B for 100 cr. But value of net asset of Company B is 80 cr then remaining 20 cr is goodwill and it will be shown under goodwill in Company A balance sheet.

Investors needs to be careful in companies where intangible assets as % of total assets is high because valuations of intangible assets are done on the basis of assumptions.

The management can easily fool the investors by doing acquisition at high cost & record goodwill in books

The management can easily fool the investors by doing acquisition at high cost & record goodwill in books

Let's understand it with an example of a US based company Teladoc Health. Teladoc is pioneer in virtual doctor visits. If we look at the financials of the company it has goodwill in his books which is more than 80% of total assets of the company.

In March 2022, it has written off $6.6 billion of goodwill which was in the books due to company’s acquisition of remote health monitoring company Livongo. The share price of the company has fallen by more than 50% from the date of results.

Another such example from the Indian market is Quess Corp, if we look into its financials in FY2019 the company has total intangible assets of INR 1435 cr which is more than 28% of its Total Assets.

Then if we move a year forward then they have also done the impairment of goodwill in exceptional items and written off 660 cr of goodwill from balance sheet in FY2020.

The next line is Investments - All those investments which are held by the company, it includes investment in equity, debt, bonds, debenture, etc. It has 2 parts

1⃣Non current Investments - If holding for more than 1 year

2⃣Current Investments - If holding for less than 1 year

1⃣Non current Investments - If holding for more than 1 year

2⃣Current Investments - If holding for less than 1 year

For example, PI Industries has done acquisition of some companies so that will be shown here under Non- current investments.

The next item is Other Financial Assets⤵️

It includes loans and advances which includes loans to related parties or loans to employees, it also covers deposits to govt authorities or security deposits for leases. It also includes advances given to suppliers.

It includes loans and advances which includes loans to related parties or loans to employees, it also covers deposits to govt authorities or security deposits for leases. It also includes advances given to suppliers.

With these we complete the non-current assets section. Now, let’s move towards Current Assets

The first line item here is Inventories, which is the closing stock of finished goods, raw materials and work in progress.

The first line item here is Inventories, which is the closing stock of finished goods, raw materials and work in progress.

The other item is trade receivables⤵️

It includes the balance of all sales revenue on credit, net of any allowances for doubtful accounts. As an investor we need to carefully check the inventory days & debtor days and compare the same within the industry.

It includes the balance of all sales revenue on credit, net of any allowances for doubtful accounts. As an investor we need to carefully check the inventory days & debtor days and compare the same within the industry.

The last item on the Assets side is Cash & cash equivalents, it includes the cash in hand, bank balances and deposits with maturities less than 3 months. High balance in current account or cash in hand for a long period of time might be suspicious (Hint:- Satyam Scam)

With these now let’s move to other part of Balance Sheet i.e, Equity & Liabilities. As we discussed above Assets = Equity + Liabilities.

Meaning of Equity

Equity consists of 2 components

1⃣Equity Share Capital

2⃣Other Equity

Equity is also known as the Net Worth of the company

Meaning of Equity

Equity consists of 2 components

1⃣Equity Share Capital

2⃣Other Equity

Equity is also known as the Net Worth of the company

Equity Share Capital⤵️

It is the amount raised by the company at its face value. This is the value of funds that shareholders have invested in the company.

Share capital = No. of shares x Face value

It is the amount raised by the company at its face value. This is the value of funds that shareholders have invested in the company.

Share capital = No. of shares x Face value

For example, you started a new company say XYZ Ltd. today with investment of Rs. 1 Lakh and company issued 10,000 shares with face value of Rs. 10 each. Then in such case my share capital will be 1 lakh.

After 5 years co has launched its IPO and issued 1 lakh shares at a share price of 500 then here my face value will be 10 & securities premium (part of other equity) will be 490. Share capital will increase by 10 lakhs (1 lakh shares x Rs 10) and 490 lakhs will be in other equity

Note that the share capital of a company doesn’t change on the basis of market price of share. It is always calculated on the basis of FV.

We like the companies where equity dilution is less. Equity dilution means raising money by issue of equity shares via QIP, Rights, ESOP.

We like the companies where equity dilution is less. Equity dilution means raising money by issue of equity shares via QIP, Rights, ESOP.

However, in some industries like Banking and Finance. Since, these are leveraged entities, their Share capital will keep increasing over a period of time due to dilution.

As for Bank and Financials

Equity=Growth Capital+Safety Capital to abide by the regulatory norms!

As for Bank and Financials

Equity=Growth Capital+Safety Capital to abide by the regulatory norms!

The next component is Other Equity, it consist of following:

1⃣Retained Earnings

2⃣General Reserve

3⃣Securities Premium

Retained earnings are the accumulated profits of the company since inception. Basically net profit or loss in P&L will be transferred to retained earnings.

1⃣Retained Earnings

2⃣General Reserve

3⃣Securities Premium

Retained earnings are the accumulated profits of the company since inception. Basically net profit or loss in P&L will be transferred to retained earnings.

The next item here is the General Reserve⤵️

It is reserve created by the company for safety purpose like any loss due to contingencies like fire or any other loss.

Securities Premium⏬

It is the amount received by the company on issue of shares at price above face value.

It is reserve created by the company for safety purpose like any loss due to contingencies like fire or any other loss.

Securities Premium⏬

It is the amount received by the company on issue of shares at price above face value.

As discussed in above example of share capital where we issues shares at 500, in that case my securities premium will be 490 per share.

In reserves investors needs to be careful if there is any event like writing off the provisions directly from reserves rather than P&L account.

In reserves investors needs to be careful if there is any event like writing off the provisions directly from reserves rather than P&L account.

Yes Bank in Q4 FY2022 has created a provision of 630 cr on few borrowers account. Normally all these provision should be charged to P&L so that Net Profit can show the correct picture but here they charged only 150 cr in P&L and remaining they directly reduced from reserves.

This is an example of Aggressive accounting🚨🚨🚨🚨

We have seen the same in one pharma company as well where they didn’t charged the foreign currency losses in P&L rather they deducted it from reserves.

Investors should be very careful in such companies where they are artificially inflating the profits of the company.

Investors should be very careful in such companies where they are artificially inflating the profits of the company.

Now the component of the Balance Sheet is Liabilities. In simple words Liabilities are the dues of the company.

These are also classified in 2 parts⏬

🥇Non current liabilities - Dues which are payable after 12 months

🥈Current Liabilities - Dues payable within 12 months

These are also classified in 2 parts⏬

🥇Non current liabilities - Dues which are payable after 12 months

🥈Current Liabilities - Dues payable within 12 months

The first line item in Non-current liabilities is Long term Borrowing, these are loans and other financial obligations which are payable to banks or other institutions.

There are 2 types of borrowings⏬

1⃣Secured - It means these loans are against some asset pledged to the bank.

There are 2 types of borrowings⏬

1⃣Secured - It means these loans are against some asset pledged to the bank.

2⃣Unsecured - These are loans which don’t require collateral; these are generally from related parties like loans from directors.

The next line item is Lease Liabilities,

It is one of the most important area which many investors miss while analysing companies.

It is one of the most important area which many investors miss while analysing companies.

Lease liability is the new concept from FY2020 with the adoption of new Accounting standard Ind AS 116: Leases. Previously the lease rentals which we pay is directly charged to P&L accounts & there was no requirement of creating lease liability and Right of Use Asset (ROU Asset).

But with the introduction of Ind AS 116 now all leases are to be recognized in the balance sheet as an Asset and Liability. The lease liability is measured at present value of lease payments to be made over lease term.

On the lease liability we will charge interest which will be reflected in P&L. With liability we will also create an asset called ROU Asset and it will depreciated over a period of lease term.

Lease=Long term debt=Liabilities

ROU=Assets

Thus, it balances!!

Lease=Long term debt=Liabilities

ROU=Assets

Thus, it balances!!

Net impact of the above change⏬

Profit & Loss Statement - Increase in EBITDA (no lease rentals) but consequent decrease in initial years in net profit (higher depreciation & interest cost).

Balance Sheet - Increase in Assets & Liabilities

Profit & Loss Statement - Increase in EBITDA (no lease rentals) but consequent decrease in initial years in net profit (higher depreciation & interest cost).

Balance Sheet - Increase in Assets & Liabilities

Let’s understand the impact of this new standard on books of Jubilant Foodworks as they have many stores on leases and this industry along with aviation, real estate, hotel and retail is highly impacted.

They have shown P&L as per the IND AS 116 adjustments⏬⏬

They have shown P&L as per the IND AS 116 adjustments⏬⏬

Their Rent expenses has been reduced drastically from 385 cr to 84 cr and depreciation and finance cost has increased due to dep on ROU asset and interest on lease liability.

The next item we will discuss is Provisions

These are the amount the company has provided for future obligations like gratuity payable to employees or leave encashment for employees, warranty claims that can arise in future These are also bifurcated between current & non current

These are the amount the company has provided for future obligations like gratuity payable to employees or leave encashment for employees, warranty claims that can arise in future These are also bifurcated between current & non current

Deferred Tax Liabilities/ Assets:

First understand what is the need of deferred tax. So as we know company prepares book of accounts as per Companies Act whereas they need to pay tax as per Income Tax Act, in both these acts there are some differences which leads to DTA or DTL.

First understand what is the need of deferred tax. So as we know company prepares book of accounts as per Companies Act whereas they need to pay tax as per Income Tax Act, in both these acts there are some differences which leads to DTA or DTL.

Say a company purchased an asset of 1 lakh as per co act they can charge dep @ 20% so dep in books will be 20k. But as per IT Act they can charge dep only @ 15% so dep will be 15k only which leads to difference of 5k. Now assuming tax rate is 30% so there will be DTA of 1500.

And the opposite of this creates the Deferred Tax liabilities!

At the end of the day, taxes are always paid as per the Income Tax Act :)

At the end of the day, taxes are always paid as per the Income Tax Act :)

The last line item in Balance Sheet is Trade Payables which is amount payable to suppliers for example, if we purchased any raw material on credit then it will be shown here.

Here companies are required to show trade payables in 2 parts

1⃣Dues to MSME

2⃣Dues to others

Here companies are required to show trade payables in 2 parts

1⃣Dues to MSME

2⃣Dues to others

Thank you so much for reading!

We teach Fundamental and Business analysis at SOIC :)

Be a part of our mailing list (more than 1L+ investors already benefitting) soic.in. Its free

Follow us on Youtube at

youtube.com

We teach Fundamental and Business analysis at SOIC :)

Be a part of our mailing list (more than 1L+ investors already benefitting) soic.in. Its free

Follow us on Youtube at

youtube.com

Loading suggestions...