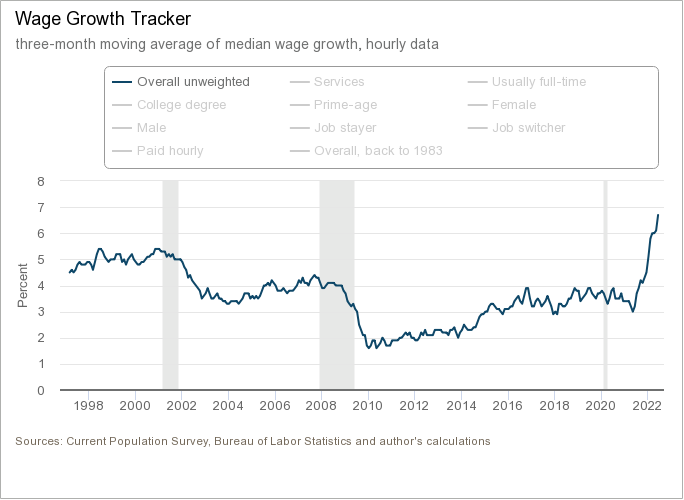

Today's large jump in the Atlanta Fed is a piece of evidence against my view that nominal wage growth is slowing.

I had thought the issue was the way the timing of the data was reported but the huge jump up in June makes that very unlikely.

I had thought the issue was the way the timing of the data was reported but the huge jump up in June makes that very unlikely.

The Atlanta Fed has the benefit of adjusting for composition (by showing growth for the same people matched over 12 months).

One disadvantage, however, is that Atlanta just shows 12-month growth when we really want to know if, eg, growth was slower in the last few months.

One disadvantage, however, is that Atlanta just shows 12-month growth when we really want to know if, eg, growth was slower in the last few months.

I had thought that the timing difference for the reporting was why Atlanta didn't show the slowing, that it simply didn't let you see that 2022-H1 was slower than 2021-H2.

But with the jump of Atlanta from 6.1% to 6.7% that is now highly implausible.

But with the jump of Atlanta from 6.1% to 6.7% that is now highly implausible.

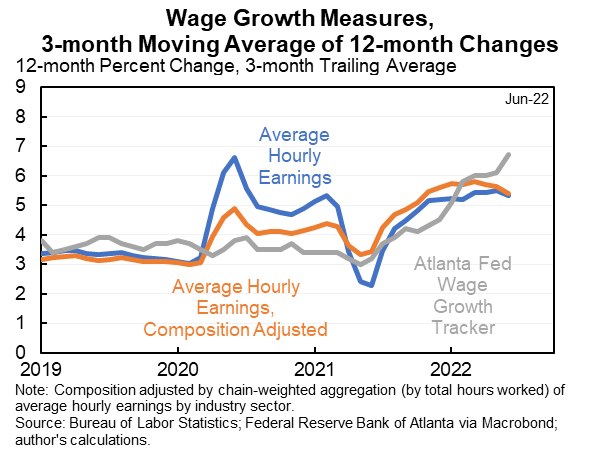

Specifically this shows the Atlanta Fed against average hourly earnings and my industry-composition-adjusted average hourly earnings series. All three are shown using the same periods for growth rates.

The Atlanta data is telling a very different story as AHE as of June.

The Atlanta data is telling a very different story as AHE as of June.

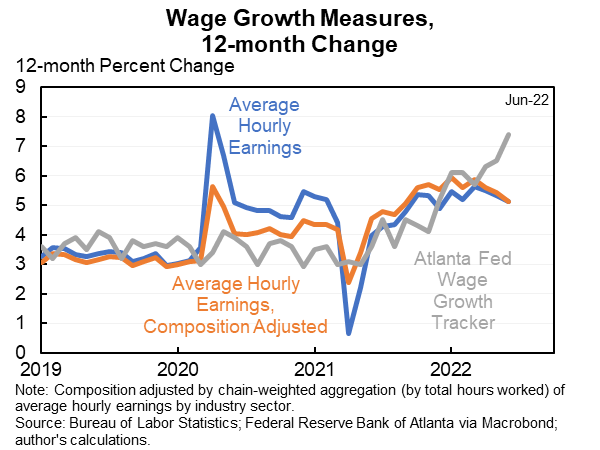

This is even clearer using the unsmoothed data. The 12-month change jumped from 6.5% to 7.4%. This is *much* higher than the 12-month change in average hourly earnings.

Is possibly but wildly implausible that a slowing monthly pattern generated the sharp 12-month rise.

Is possibly but wildly implausible that a slowing monthly pattern generated the sharp 12-month rise.

Does that mean the Atlanta Fed is right & nominal wage growth is picking up? With lots of composition shifts happening there is a big benefit to using their data. It is also more more consistent with what I expected, resolving the wage puzzle by saying the AHE data are wrong.

But Atlanta also has its own issues--self reports by workers, the issues of limiting the sample to people who were working in both periods, sample size, etc. So it's not the definitive truth either.

Makes me that much more anxious for the ECI which is better than either one.

Makes me that much more anxious for the ECI which is better than either one.

P.S. I was resisting this interpretation in a back-and-forth with @aaronsojourner and @arindube last night. But the June data was such a big increase that it really shifts things. As does the unsmoothed Atlanta data which I hadn't been looking at.

P.P.S. I might be making a mistake I generally try to avoid which is over-updating based on each new data point. Will try to resist doing that.

P.P.P.S. The 7% and rising wage growth in the Atlanta Fed data is roughly consistent with 6% and rising prices inflation. So their data has the advantage of lining up with my view of the labor market (tight market so rising wage growth) and the price-wage inflation link.

Another view from @paulkrugman: the Atlanta Fed reflects *median* wage growth and when inequality is falling that will grow faster than *mean*. But mean matters for inflation.

Not sure that is nearly enough to explain *increasing* growth but worth pondering.

Not sure that is nearly enough to explain *increasing* growth but worth pondering.

Loading suggestions...