Fundamental Analysis - S.P. Apparels

👣Origin

In 1989, Mr. P. Sundararajan, a visionary, entered the garment export industry through his venture “S.P. Apparels.” Through innovation and creative approaches, the company has consistently delivered high-quality products to customers time and again.

In 1989, Mr. P. Sundararajan, a visionary, entered the garment export industry through his venture “S.P. Apparels.” Through innovation and creative approaches, the company has consistently delivered high-quality products to customers time and again.

👥Management -

Mr. P. Sundararajan Chairman, MD, Founder director of SPAL - 36 years of experience in the textile & apparel industry, BSc. from Bangalore University.

Ms S. Latha Executive Director: Founder director of SPAL - 29 years of experience in textile & apparel industry.

Mr. P. Sundararajan Chairman, MD, Founder director of SPAL - 36 years of experience in the textile & apparel industry, BSc. from Bangalore University.

Ms S. Latha Executive Director: Founder director of SPAL - 29 years of experience in textile & apparel industry.

SPAL is one of the leading manufacturers and exporters of knitted garments for infants and children in India. Provides end-to-end garment manufacturing from Yarn to finished products including body suits, sleepsuits, tops, and bottoms.

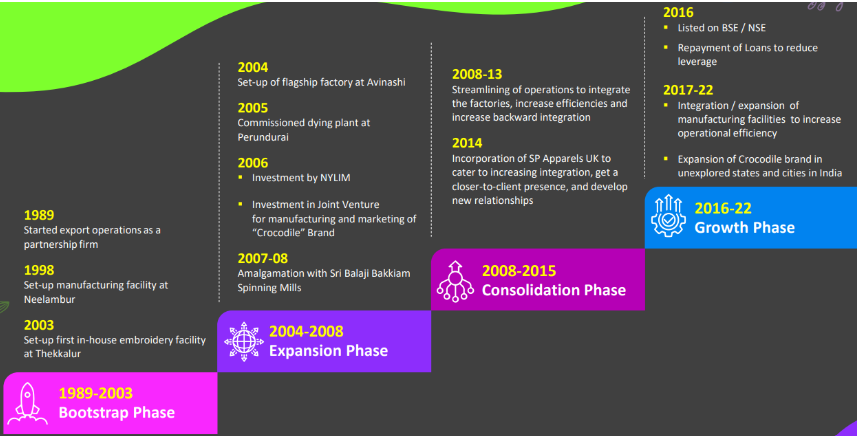

Phases -

Phases -

💼Use Case -

SPAL is a vertically integrated apparel organization operating with cutting-edge technologies in this industry. SPAL’s operations are integrated across the textile value chain from spinning to garmenting & value additions including dying, printing, & embroidery.

SPAL is a vertically integrated apparel organization operating with cutting-edge technologies in this industry. SPAL’s operations are integrated across the textile value chain from spinning to garmenting & value additions including dying, printing, & embroidery.

🌎Global Industry Dynamics

The global textile market size is expected to grow from $530.97 billion in 2021 to $575.06 billion in 2022 at a compound annual growth rate (CAGR) of 8.3%. The textiles market is expected to grow to $760.21 billion in 2026 at a CAGR of 7.2%.

The global textile market size is expected to grow from $530.97 billion in 2021 to $575.06 billion in 2022 at a compound annual growth rate (CAGR) of 8.3%. The textiles market is expected to grow to $760.21 billion in 2026 at a CAGR of 7.2%.

🇮🇳Domestic Dynamics

▪️The industry contributes 5% to country’s GDP, 7% of industry output in value terms & 12% of the country’s export earnings. It is also one of the largest in the world with a large unmatched raw material base and manufacturing strength across the value chain.

▪️The industry contributes 5% to country’s GDP, 7% of industry output in value terms & 12% of the country’s export earnings. It is also one of the largest in the world with a large unmatched raw material base and manufacturing strength across the value chain.

▪️ India is the sixth largest exporter of textiles and apparel in the world. The share of textile and apparel (T&A) in India’s total exports is 11.4% in FY 2021. India has a share of 4% of the global trade in textiles and apparel.

▪️ The government's focus has been on increasing textile manufacturing by building best-in class manufacturing infrastructure, upgrading technology, fostering innovation & skills and traditional strengths in the sector for making India's development inclusive and participative.

▪️ Under Union Budget 2022-23, the total allocation for the textile sector was ` 12,382 crore. Moreover, the 10,683 crores Production-linked Incentive scheme is expected to be a major boost for textile manufacturers.

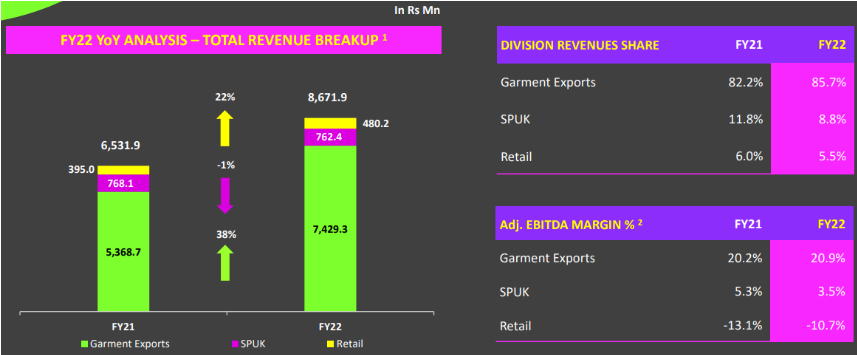

📊Revenue Breakup -

👗Infant Wear -

SPAL has a strong MOAT in this segment, a very niche category with not many competitors, and has completely integrated facilities which gives them an exceptional stronghold in a segment that has high barriers to entry.

SPAL has a strong MOAT in this segment, a very niche category with not many competitors, and has completely integrated facilities which gives them an exceptional stronghold in a segment that has high barriers to entry.

🥳Brownie Points -

*⃣ We are backwardly as well as forwardly integrated. This is the biggest advantage for us, especially in the current scenario, because if the cotton price goes up, yes there will be an impact on our garment cost, but manage it efficiently and retain orders.

*⃣ We are backwardly as well as forwardly integrated. This is the biggest advantage for us, especially in the current scenario, because if the cotton price goes up, yes there will be an impact on our garment cost, but manage it efficiently and retain orders.

*⃣ Meeting stringent compliance requirements of international customers.

*⃣ Long-standing relationships with reputed global brands. The company is working towards sustainable growth by continuously working on improving its ESG matrix.

*⃣ Long-standing relationships with reputed global brands. The company is working towards sustainable growth by continuously working on improving its ESG matrix.

*⃣ Strong Pedigree - Leading children wear manufacturer under the leadership of Mr. Sundararajan, CMD with more than 36 years of experience in the apparel industry.

*⃣ Ability to consistently deliver high quality products on timely basis.

*⃣ Ability to consistently deliver high quality products on timely basis.

*⃣ Brand Signatures - More than 3 decades of expertise in infant and children wear. They're approved suppliers to almost all major children-wear brands.

*⃣ Apt understanding of buyer preferences & specifications of knitted & embellished garments in infants and children category.

*⃣ Apt understanding of buyer preferences & specifications of knitted & embellished garments in infants and children category.

*⃣ Dedicated in-house design and merchandising team of designers located at our Corporate Office in India and design consultants hired by our Subsidiary, SPUK.

*⃣ Use of latest technology for developing products and styles which are based on prevalent fashion trends.

*⃣ Use of latest technology for developing products and styles which are based on prevalent fashion trends.

*⃣ SPAL’s core competency lies in its understanding latest fashion. Design development, sampling, and fitment form an integral part of our operations and are considered an effective tool for converting customers needs into finished products.

💪Quality Checks -

♻️Stringent quality control checks consisting of inspection and testing of fabric, greige, and processed yarn, trims, accessories, packing materials, and of each piece of garment for metal bits/needle tips/sharp edges prior to packing.

♻️Stringent quality control checks consisting of inspection and testing of fabric, greige, and processed yarn, trims, accessories, packing materials, and of each piece of garment for metal bits/needle tips/sharp edges prior to packing.

♻️All individual pieces of garments are also physically inspected to ensure that no defective/damaged pieces are delivered to our customers.

♻️The internal rejection rate is low as compared to international standards.

♻️The internal rejection rate is low as compared to international standards.

🌎 Exports -

(i) On number of garment pieces exported (volume): Current year, they've have done 50 million pieces and expecting it to increase by 10% to 15% next year.

(i) On number of garment pieces exported (volume): Current year, they've have done 50 million pieces and expecting it to increase by 10% to 15% next year.

(ii) Order book for export front: The value is right at INR 327 crore. The average price per piece now is INR 135. Last year, the sale value of the export per piece is INR 116 for 5 crore pieces.

(iii) FY23 they are looking at a revenue growth somewhere around 20% increase and going forward it should be anywhere between 10% to 15% because of the complexity of the product. So they are looking at 10% to 15% revenue growth from the FY24 onwards.

(iv) With regards to the new customer additions, they mentioned before that they are looking for the addition of two customers, both of them, they're globally present and they have stores all over the globe and they'll be working directly with these brands.

(v) New customers adding revenue - They are big brands. Their volumes are massive, and they are focused on babies and kids garments. So, in the first year, they will be just starting on a trial basis. So, the real business starts from next year, FY23 - FY24.

(vi) Capacity utilization is around 72% currently & is expected to increase by another 10% - 15% going forward, which means we expect around 82% to 85% in the next 2-3 quarters. New customers are looking for bigger factories so they are planning to add one more factory this year.

(vii) To mitigate the risk of availability of quality yarn, and consistency in supply, we have tied up with a mill on a conversion basis, so that the supply is done without volatility. In the current FY, spinning plan has demonstrated well both in terms of margins & production.

🏙️Subsidiaries -

👉 For SPUK they are looking at a revenue of close to GBP 9 million to GBP 10 million next year. And it's purely back-to-back in terms of PO’s so, working capital should hardly be 45 days there.

👉 For SPUK they are looking at a revenue of close to GBP 9 million to GBP 10 million next year. And it's purely back-to-back in terms of PO’s so, working capital should hardly be 45 days there.

👉For SPUK We are looking at a revenue of close to GBP 9 million to GBP 10 million next year. And it's purely back-to-back in terms of PO’s so, working capital should be hardly 45 days there.

👉On SP Retail (Crocodile): It will definitely be a break even this financial year. The management shows the confidence in having the ability to be growing 50% to 60% every year (albeit on a low base).

💪CAPEX PLANS -

(a) They have 5,000 machines and the utilization level is at 72%.

(b) Additional capacity should be at least 2,000 to 2,500 machines in total at full utilization levels

(a) They have 5,000 machines and the utilization level is at 72%.

(b) Additional capacity should be at least 2,000 to 2,500 machines in total at full utilization levels

(c) It could be anywhere between INR 50 crore to INR 60 crore in terms of the full project, including it.

(d) But right now, out of 2,000 machines, about 1,000 machines additions will happen in a phased manner.

(d) But right now, out of 2,000 machines, about 1,000 machines additions will happen in a phased manner.

(e) Expected capital expenditure of around Rs. 150-200 crore, to be incurred between FY2023 and FY2025, largely funded by internal accruals.

📍Risks -

❎Customer concentration risk remains high, widening client base to mitigate the risk to some extent.

❎SPAL’s top 3 customers contributed 80-90% to its revenues in FY'21 & FY'22. The same exposes its revenues to the performance of its key customers.

❎Customer concentration risk remains high, widening client base to mitigate the risk to some extent.

❎SPAL’s top 3 customers contributed 80-90% to its revenues in FY'21 & FY'22. The same exposes its revenues to the performance of its key customers.

❎Earnings exposed to fluctuations in input prices, cotton and yarn prices and exchange rates on the back of limited pricing flexibility enjoyed with key customers.

❎Inventory Days have gone up from 233 to 342 (management says due to pending order)

❎Inventory Days have gone up from 233 to 342 (management says due to pending order)

❎Severe restrictions on the use of chemicals, dyes, accessories, and other additives to prevent any side effects on infants and children.

❎SPAL faces competition from other large textile exporters from India as well as from other low-cost garment exporting countries, which limits its ability to improve prices and margins to an extent.

❎Order-backed procurement for the major portion of the stock held limits input price risk to an extent, earnings have been protected to a large extent against fluctuations in exchange rates through back-to-back hedging undertaken by SPAL with more than 80% of the receivables.

⚡️Promotors hold almost 62% stake

⚡️Dolly Khanna holds 0.31% stake of the company

⚡️They are planning to raise private equity from strategic investments in their new retail venture to grow the business and excel in this industry.

⚡️Share holding from screener.in

⚡️Dolly Khanna holds 0.31% stake of the company

⚡️They are planning to raise private equity from strategic investments in their new retail venture to grow the business and excel in this industry.

⚡️Share holding from screener.in

📈The operating performance is expected to remain strong in FY2023, driven by the consistent growth in order inflows from existing large customers, the addition of new customers &healthy margins enjoyed.

Expansion of 3,600 spindles - completed & started yielding production.

Expansion of 3,600 spindles - completed & started yielding production.

📊Fundamental Metrics -

ROCE : 15.8 %

ROE : 14.2 %

OPM : 17.7 %

Debt to Equity : 0.33

5 Years Sales growth : 6.34 %

5 Years Profit growth : 9.96 %

Market Cap to Sales : 1.10

ROCE : 15.8 %

ROE : 14.2 %

OPM : 17.7 %

Debt to Equity : 0.33

5 Years Sales growth : 6.34 %

5 Years Profit growth : 9.96 %

Market Cap to Sales : 1.10

💰Valuations -

1. Stock P/E : 11.2

P/E (Median) -

5 Years : 13.22

3 Years : 11.28

2. Stock P/B : 1.5

P/BV (Average)

5 Years : 1.42

3 Years : 1.04

3. EV/EBITDA : 6.83

EV/EBITDA (Average)

5 Years : 6.82

3 Years : 6.18

1. Stock P/E : 11.2

P/E (Median) -

5 Years : 13.22

3 Years : 11.28

2. Stock P/B : 1.5

P/BV (Average)

5 Years : 1.42

3 Years : 1.04

3. EV/EBITDA : 6.83

EV/EBITDA (Average)

5 Years : 6.82

3 Years : 6.18

Disclaimer -

Pointers have been taken from the company's website and other investor forums.

Info is shared for learning purposes only.

Do your own due diligence before investing.

Pointers have been taken from the company's website and other investor forums.

Info is shared for learning purposes only.

Do your own due diligence before investing.

Loading suggestions...