Excellent @petersgoodman on the complex & dangerous global economic situation.

The article is especially strong on the impact on emerging markets.

I would, however, emphasize policy a bit more & COVID/Russia a bit less. Two examples:

nytimes.com

The article is especially strong on the impact on emerging markets.

I would, however, emphasize policy a bit more & COVID/Russia a bit less. Two examples:

nytimes.com

1. GOODS CONSUMPTION -- SOURCES AND CONSEQUENCES?

The US has seen a big increase in goods consumption while services haven't recovered. The article's emphasis follows many economists in: (a) attributing this mostly to COVID and (b) arguing it has played a big role in inflation.

The US has seen a big increase in goods consumption while services haven't recovered. The article's emphasis follows many economists in: (a) attributing this mostly to COVID and (b) arguing it has played a big role in inflation.

(a) It is hard to attribute most of the goods increase to COVID when:

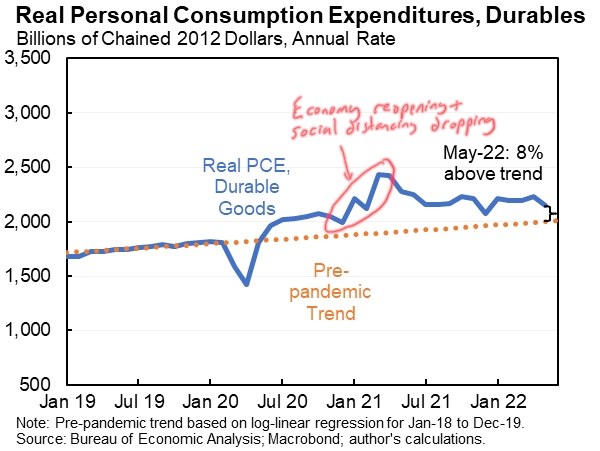

--The big increase in durable goods spending was after COVID started to retreat and as social distancing was being lifted. Real durables spending was 13% higher in June 2021 than December 2020.

--The big increase in durable goods spending was after COVID started to retreat and as social distancing was being lifted. Real durables spending was 13% higher in June 2021 than December 2020.

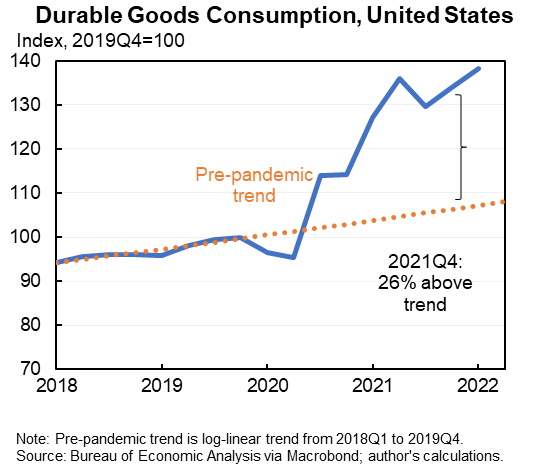

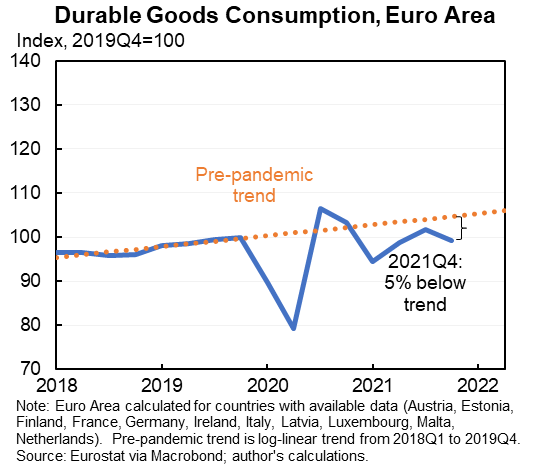

--Europe had much more stringent lockdowns that covered much more of 2021 than the United States did. But European goods consumption did not exhibit anything resembling the massive increase experienced in the United States.

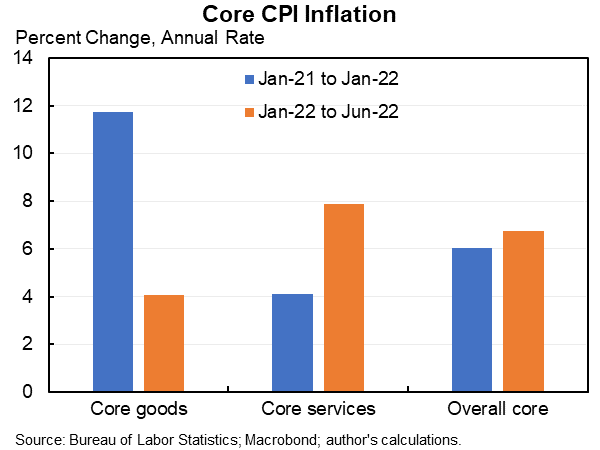

(b) Is an open question as to how much the shift from services to goods raised overall inflation. Raised goods inflation but lowered services inflation. The net depends on how elastic supply is in those two sectors and a lot of reason to believe very inelastic in services too.

In fact, since January core goods inflation has fallen dramatically but core services inflation has picked up--leaving core inflation unchanged/increased.

2. CAN MONETARY POLICY TREAT "SUPPLY" PROBLEMS?

A lot of what people call "supply" problems are really demand. Port throughput was up about 20% in 2021 from pre-COVID and imports were up dramatically. The problem was demand was even higher. Interest rates can help curb demand.

A lot of what people call "supply" problems are really demand. Port throughput was up about 20% in 2021 from pre-COVID and imports were up dramatically. The problem was demand was even higher. Interest rates can help curb demand.

There is little monetary policy can or should do to treat food & energy prices. But core PCE likely rose at about a 5 percent annual rate so far this year & very little of that is passthrough from the Russian invasion and associated food and energy prices.

Moreover, many analysts have made conceptual mistakes that have led them to overattribute inflation to supply.

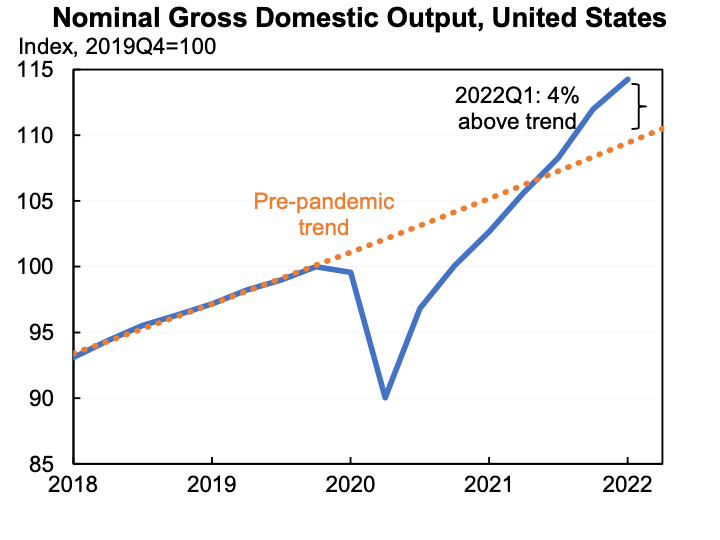

In fact, US nominal GDP is way above trend & rising. This is indicative of high demand. It is treatable--and being treated by--monetary policy.

In fact, US nominal GDP is way above trend & rising. This is indicative of high demand. It is treatable--and being treated by--monetary policy.

In conclusion, these were just two points of emphasis in the article that also made many other points (including the argument that monetary and fiscal policy may have done too much). Am using the article as a jumping off point to address arguments I see in many places.

Loading suggestions...