Aegis Logistics: Business Analysis

Supply Side Dominance is the vision: Will they continue to gain market share?

A Thread 🧵👇

Supply Side Dominance is the vision: Will they continue to gain market share?

A Thread 🧵👇

1/ Before we go deeper, let us understand the LPG Industry better

a. Upstream: Exploration and Production activities

b. Midstream: Storage and transportation of crude oil and gas

c. Downstream: Refining, production of petroleum products and processing, storage, marketing.

a. Upstream: Exploration and Production activities

b. Midstream: Storage and transportation of crude oil and gas

c. Downstream: Refining, production of petroleum products and processing, storage, marketing.

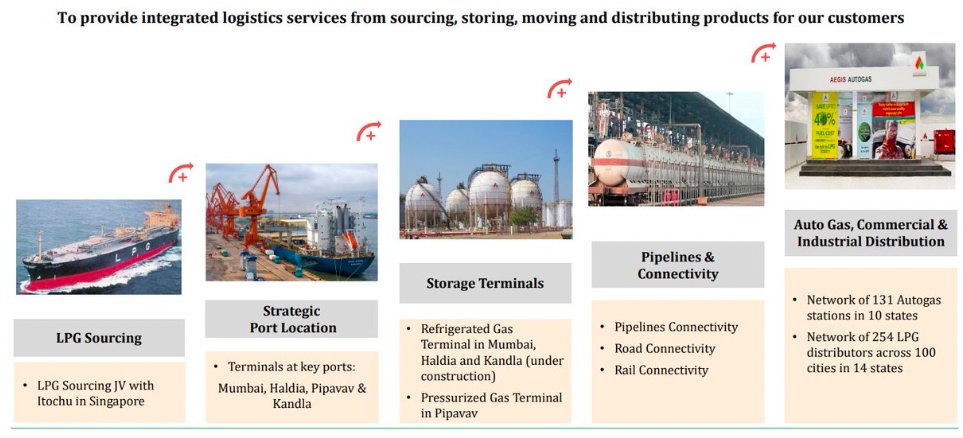

2/ Aegis is an integrated player of 'LPG' Logistics, with a firm hold on Midstream & Downstream segments (70% of EBITDA)

Other than this, they also provide liquid logistics (30% of EBITDA): which provides import, export, storage, and logistics of chemicals (More on this later)

Other than this, they also provide liquid logistics (30% of EBITDA): which provides import, export, storage, and logistics of chemicals (More on this later)

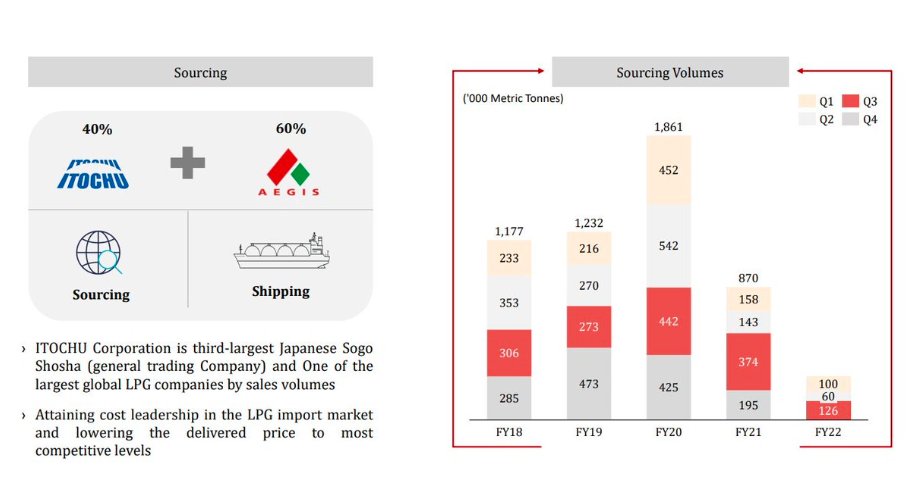

3/ They help OEMs (HPCL, BPCL, IOCL) import LPG to India

However, before we even touch imports, understand why LPG is important.

Millions of Indians die every year due to the indoor population caused by cooking with wood & dung.

LPG solves this.

thethirdpole.net

However, before we even touch imports, understand why LPG is important.

Millions of Indians die every year due to the indoor population caused by cooking with wood & dung.

LPG solves this.

thethirdpole.net

4/ Watch this video to comprehend the part of LPG in global energy needs

The story of LPG: youtube.com

Also, LPG is a low-carbon fuel, as it emits much less carbon dioxide than most conventional fossil fuels.

The story of LPG: youtube.com

Also, LPG is a low-carbon fuel, as it emits much less carbon dioxide than most conventional fossil fuels.

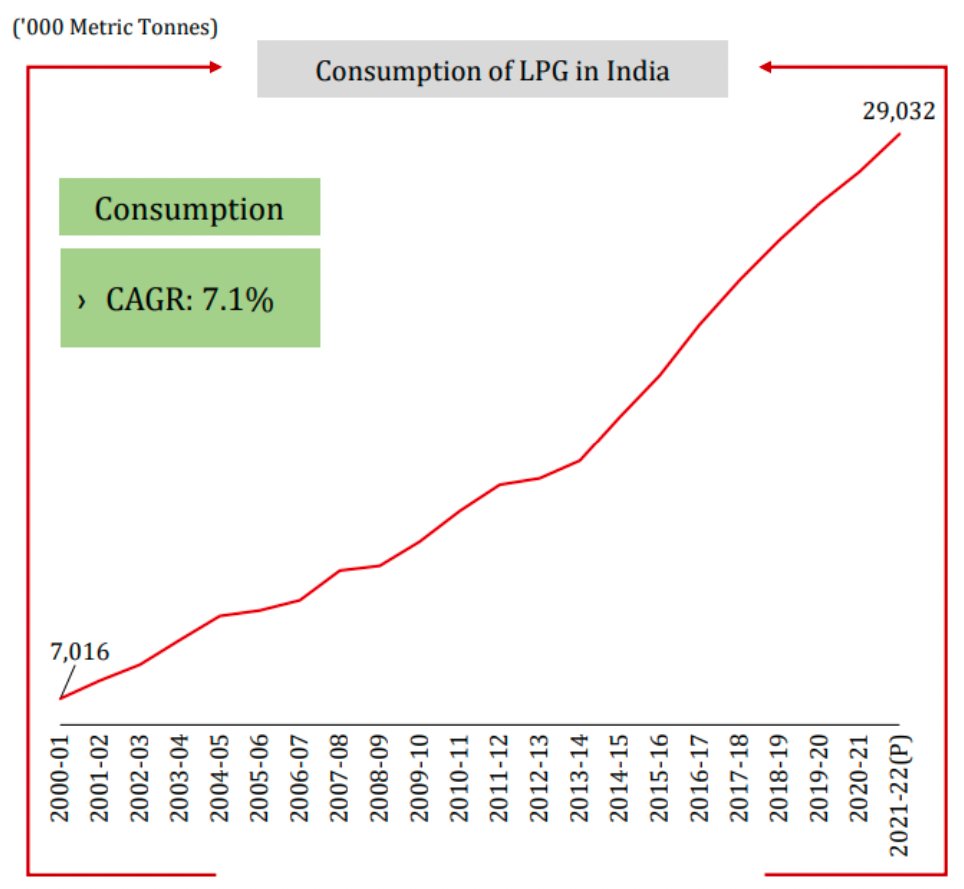

5/ This mega-trend

LPG consumption (Major boost to clean cooking) in India, growing at 7% cagr since the last 20 years 🤯

Even the government's PMUY push to increase LPG penetration has been commendable.

However, from where are we getting this much LPG from?

LPG consumption (Major boost to clean cooking) in India, growing at 7% cagr since the last 20 years 🤯

Even the government's PMUY push to increase LPG penetration has been commendable.

However, from where are we getting this much LPG from?

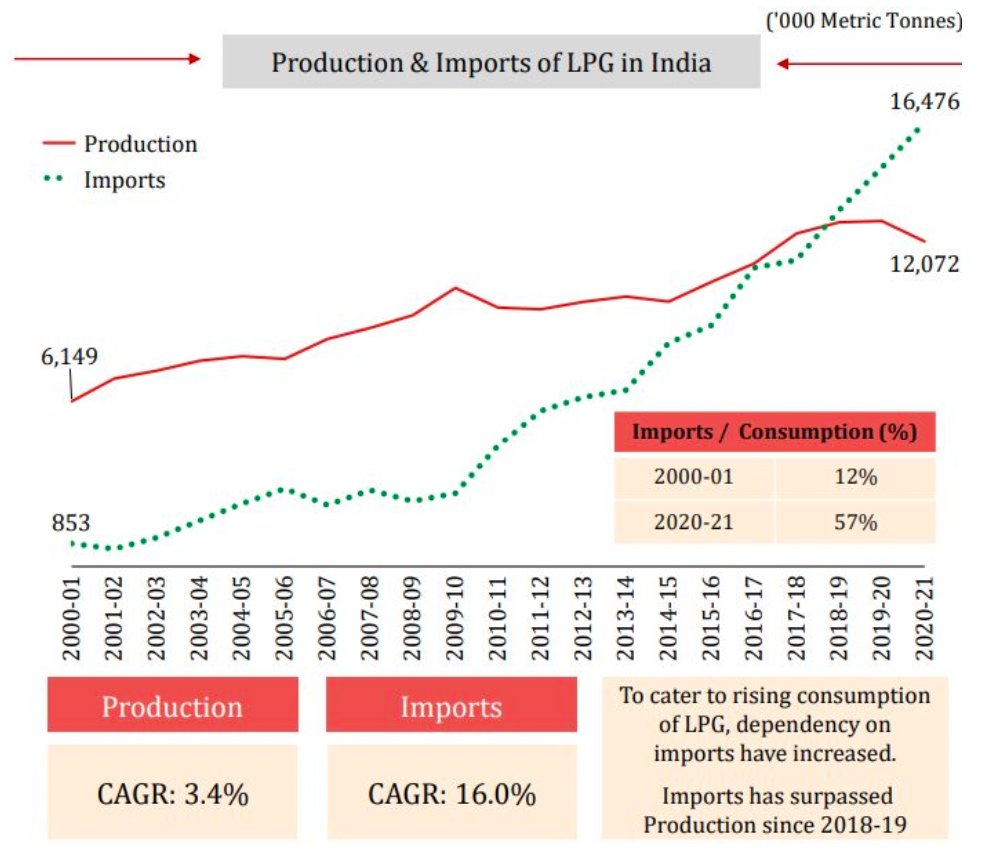

6/ Imports have been the answer.

Domestic production cagr: 3%

Imports cagr: 16%

In FY01, they made up 12% of total consumption; today, they are already at 57% & expected to increase to 70% by 2035 on a conservative basis (domestic capacity is just not keeping pace)

Domestic production cagr: 3%

Imports cagr: 16%

In FY01, they made up 12% of total consumption; today, they are already at 57% & expected to increase to 70% by 2035 on a conservative basis (domestic capacity is just not keeping pace)

7/ Naturally, the finest players in the industry must benefit. We will try to understand if Aegis Logistics is the same as we delve deeper.

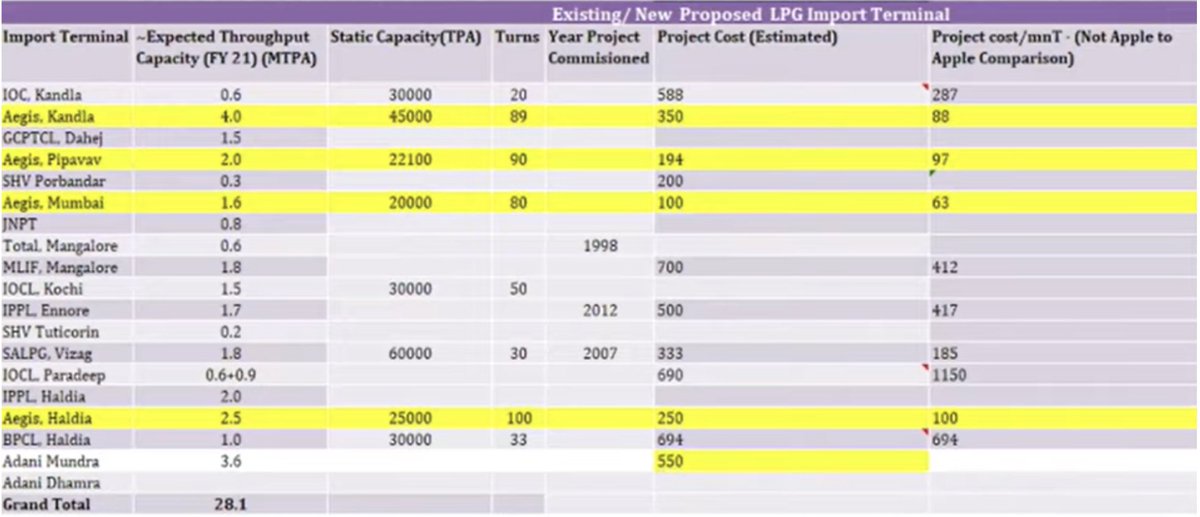

8/ They are largest private player in gas logistics with around 15-20% market share in imported LPG volumes: other large players are PSU OMCs (individually or in JV with MNCs)

See the competition, PSU to private has played out beautifully in this over the last decade.

See the competition, PSU to private has played out beautifully in this over the last decade.

9/ Drivers for market share gain? Efficiency

Whether be in terms of capex required to set up the same capacity: at least 1/2 or lower vs competitors

For example: They can put the same capacity that competitor puts for 500crores with just 200crs or less.

Whether be in terms of capex required to set up the same capacity: at least 1/2 or lower vs competitors

For example: They can put the same capacity that competitor puts for 500crores with just 200crs or less.

10/ Or Asset turns once it is established (Throughput) which is 80-100x of static capacity while competitors could only do 25-30x. Verify it yourself 👇

H/T Valupickr's passionate group

H/T Valupickr's passionate group

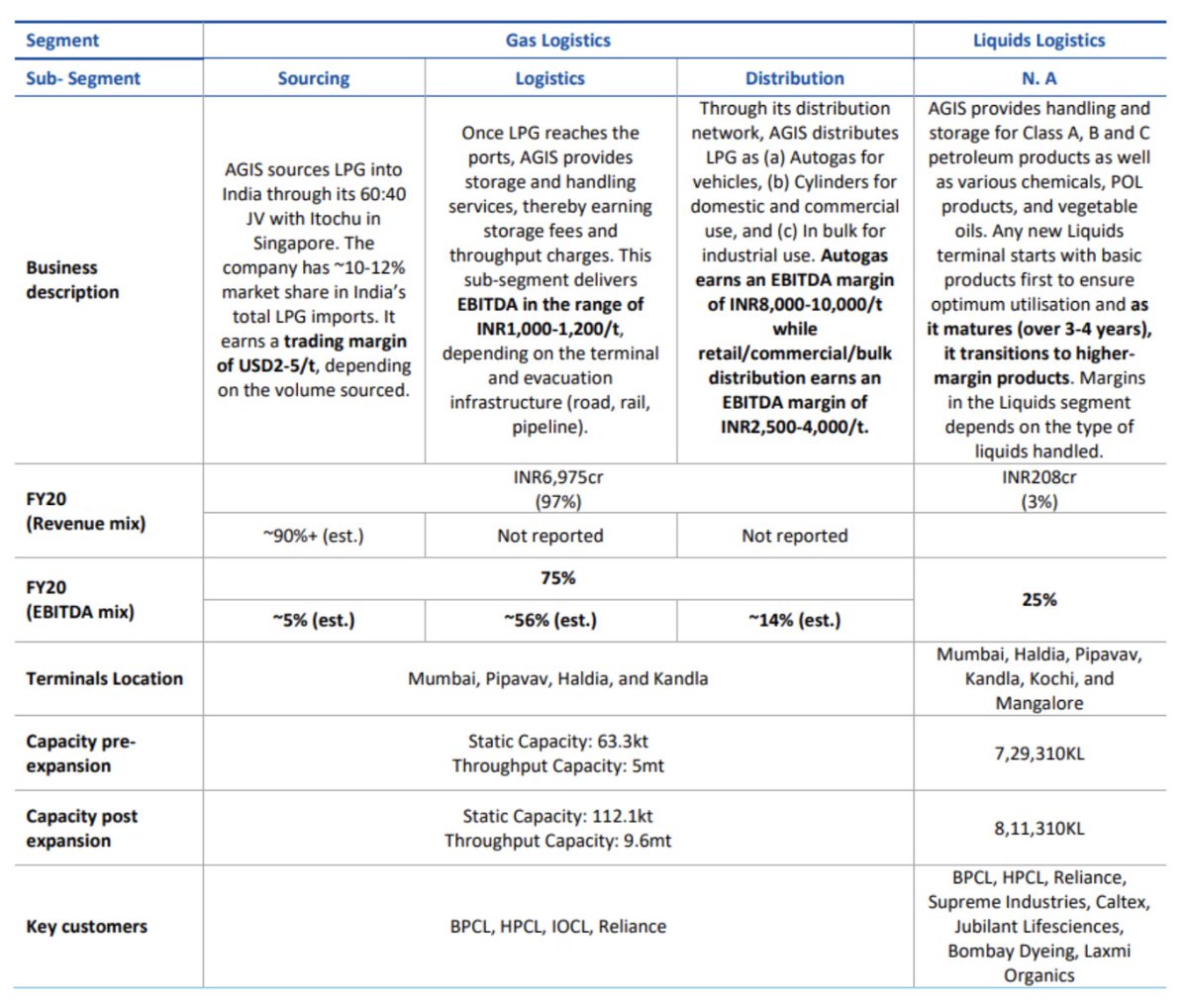

11/ LPG business has 3 parts to it.

Sourcing: 90% of their Rev, very low margins (why in Aegis, you have to look at EBITDA)

Logistics: Moderate margins (majority of Aegis' EBITDA) - The above advantages show here

Distribution: Very high margins, small in terms of size today

Sourcing: 90% of their Rev, very low margins (why in Aegis, you have to look at EBITDA)

Logistics: Moderate margins (majority of Aegis' EBITDA) - The above advantages show here

Distribution: Very high margins, small in terms of size today

12/ Why am I excited? With the recent developments, Aegis quality management can focus most of their bandwidth in growing the high margin distribution business.

Less than 1% market share in India; huge potential.

Less than 1% market share in India; huge potential.

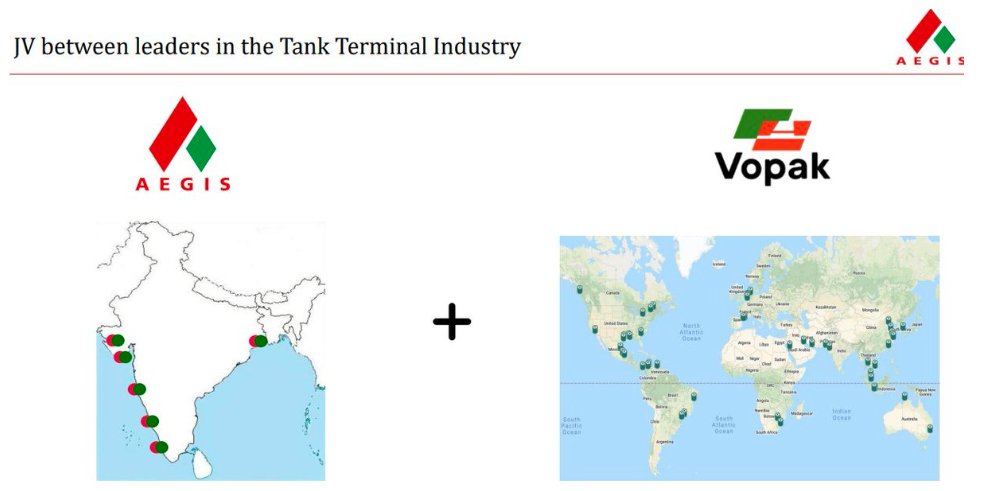

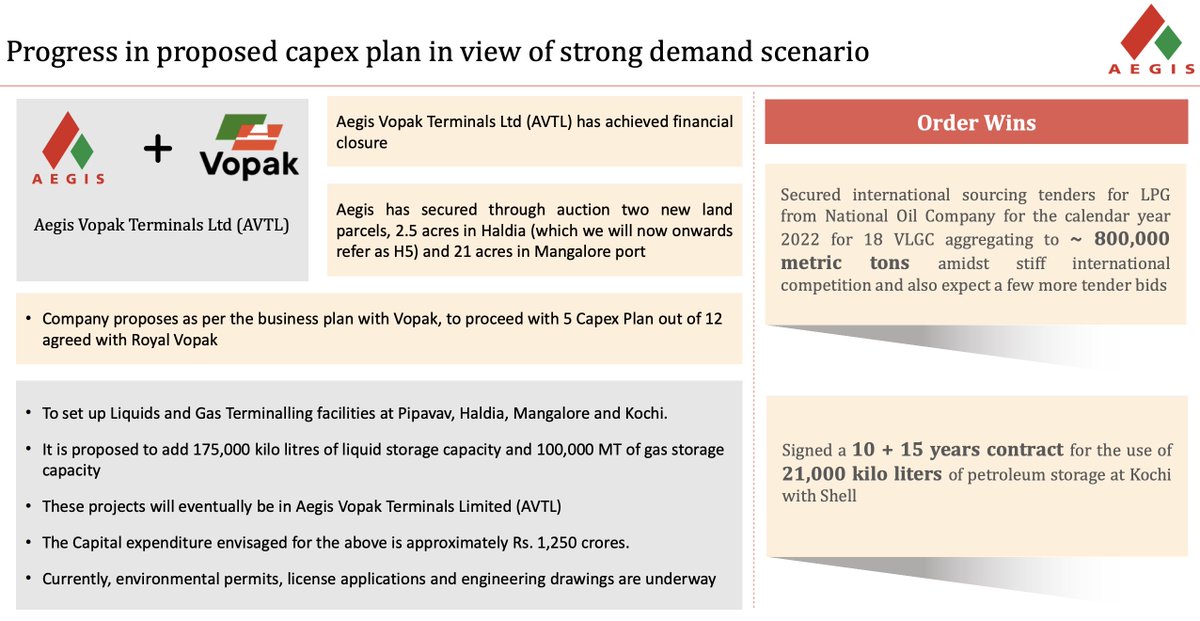

13/ What is this recent development?

Last year, Aegis did a big deal with Vopak (a global leader in the tank storage business)

It basically meant that Aegis will transfer the majority of their terminaling & Liquid assets into a JV (51:49) with Vopak

Last year, Aegis did a big deal with Vopak (a global leader in the tank storage business)

It basically meant that Aegis will transfer the majority of their terminaling & Liquid assets into a JV (51:49) with Vopak

14/ You can read more about the deal here

aegisindia.com

The deal was 2 years in the making, Aegis management wanted to better position their company for upcoming decades in terms of Indian energy requirements.

aegisindia.com

The deal was 2 years in the making, Aegis management wanted to better position their company for upcoming decades in terms of Indian energy requirements.

15/ The standalone company (Aegis) will get 2.5-2.7K crs for the 49% of these assets

& As per the terms, JV will invest 2.5-4.5K crs into the terminaling & Liquid business capacity in the next 5 years; which is near 2x of their current gross block

& As per the terms, JV will invest 2.5-4.5K crs into the terminaling & Liquid business capacity in the next 5 years; which is near 2x of their current gross block

16/ IMHO, It is a win-win for both

Aegis gets the financial power to put 5-10x larger capacities in faster times (remember the supply side dominance that I mentioned) & other storage technologies that Vopak will bring

Vopak gets the relatively fast growing indian market

Aegis gets the financial power to put 5-10x larger capacities in faster times (remember the supply side dominance that I mentioned) & other storage technologies that Vopak will bring

Vopak gets the relatively fast growing indian market

17/ Before I talk about the exceptional management, let's understand the liquid business (A cash cow: 30% of EBITDA)

Aegis offers storage facilities of chemicals on long-term contracts and on a spot basis for traders.

40-year-old client relationships here

Aegis offers storage facilities of chemicals on long-term contracts and on a spot basis for traders.

40-year-old client relationships here

18/ One caveat about this biz, is that it is a super high margin business (60-70% EBITDA)

Starts with lower margins in the initial years as they normally deal with bulk chemicals; which increases to higher margins after 3-5 years as specialty chemical contracts come in

Starts with lower margins in the initial years as they normally deal with bulk chemicals; which increases to higher margins after 3-5 years as specialty chemical contracts come in

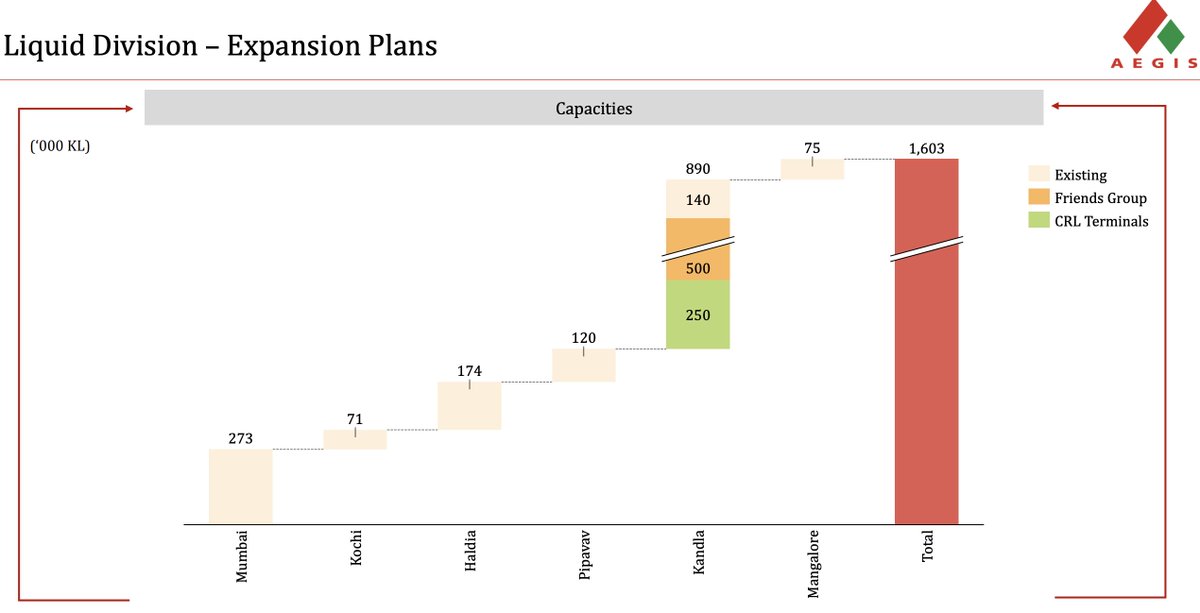

19/ With the recent augmentation of their liquid capacities through 2 acquisitions at throwaway prices (at 3-5x EV/EBITDA as per my calc.)

Becoming the biggest player -> Best economics -> Lowest prices -> Higher market share (A common theme that you will see with Aegis)

Becoming the biggest player -> Best economics -> Lowest prices -> Higher market share (A common theme that you will see with Aegis)

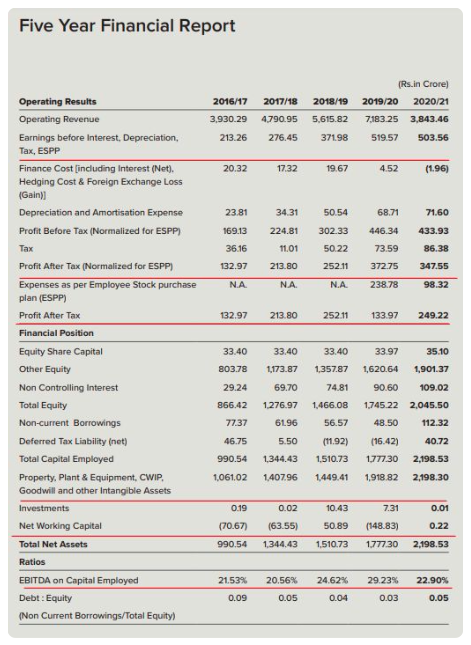

20/ LT financials are a good indicator of management quality

Business has performed rather well: need to see EBITDA before ESPP (10 year cagr: 20%+)

They introduced a huge ESOP scheme (5% dilution) for their president-level employees (impacting bottomline in FY20 & FY21)

Business has performed rather well: need to see EBITDA before ESPP (10 year cagr: 20%+)

They introduced a huge ESOP scheme (5% dilution) for their president-level employees (impacting bottomline in FY20 & FY21)

21/ The company has consistently grown its asset base (will discuss further); WC requirements are negligible | Internal accruals enough to fund this major capex (very low debt)

ROCE has consistently been above 20%, but what will be the earnings drivers (Drivers of the stock?)

ROCE has consistently been above 20%, but what will be the earnings drivers (Drivers of the stock?)

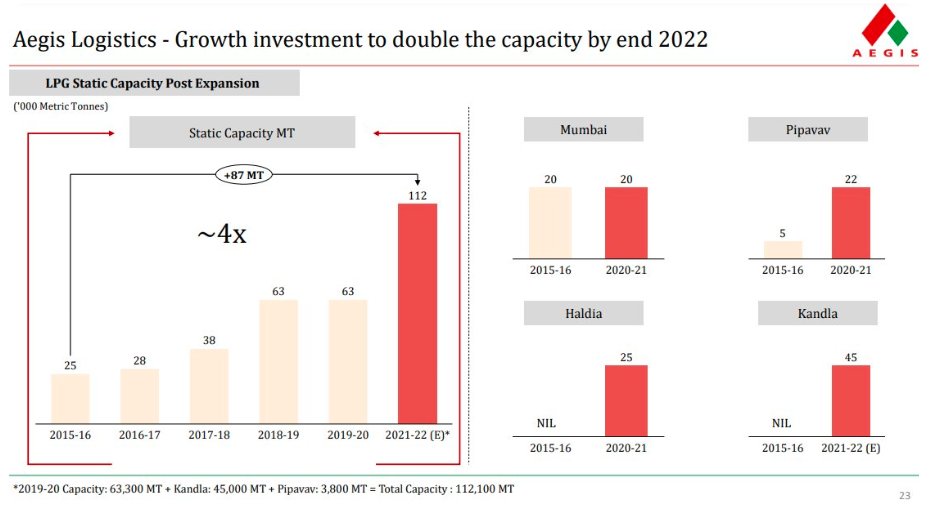

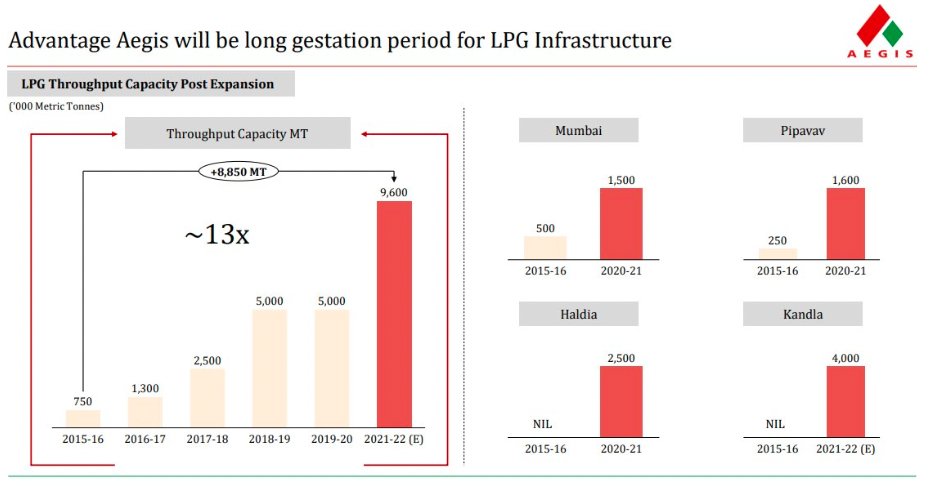

22/ Capacity expansion has literally been on steroids this past 5 years

Whether be it on Gas Terminaling (where they increased the static capacity by 4x & Thoughtput by 13x) or Liquid business (You saw before)

On the Gas side, biz is still at 30% utilization.

Whether be it on Gas Terminaling (where they increased the static capacity by 4x & Thoughtput by 13x) or Liquid business (You saw before)

On the Gas side, biz is still at 30% utilization.

23/ With the Vopak deal, the growth in earnings might look subdued for the next 1-2 years, but the business should continue to scale up in volumes big time in the next 5-7 years (amount it takes to scale up new gas capacities)

However, why is the stock down 50%?

However, why is the stock down 50%?

24/ One, market didn't like the valuations for the Vopak deal (Higher expectations)

As John Maynard Keynes wrote, “Human nature desires quick results, there is a peculiar zest in making money quickly, and remoter gains are discounted by the average man at a very high rate."

As John Maynard Keynes wrote, “Human nature desires quick results, there is a peculiar zest in making money quickly, and remoter gains are discounted by the average man at a very high rate."

25/ Also, the ramp-up of the past capex has already been slower than previously expected (COVID), so little confidence since then of more capex (2.5-4.5K crs)

A potential 50-80% holding company discount which if it applied here is a risk (prevalent in Indian markets)

A potential 50-80% holding company discount which if it applied here is a risk (prevalent in Indian markets)

26/ 2nd was a mishap that happened on Sep 21': Untimely demise of the Managing Director, Mr. Anish K. Chandaria: the visionary who built the company along with his brother Mr. Raj Chandaria

The changes in the strategic direction of the company due to this is key trackable.

The changes in the strategic direction of the company due to this is key trackable.

27/ All of these events played a key role in changing perception about the stock

However, as investors, we need to ask the key question: Has there been a structural change in the business? I do not think so.

The current price is a big discount to what I would attribute as fair.

However, as investors, we need to ask the key question: Has there been a structural change in the business? I do not think so.

The current price is a big discount to what I would attribute as fair.

28/ Other Strengths for the business includes:

Strong customer relationships with PSUs for decades (Extremely sticky)

Focus moving to the highest ROCE businesses like the retailing where sky is the limit.

Strong customer relationships with PSUs for decades (Extremely sticky)

Focus moving to the highest ROCE businesses like the retailing where sky is the limit.

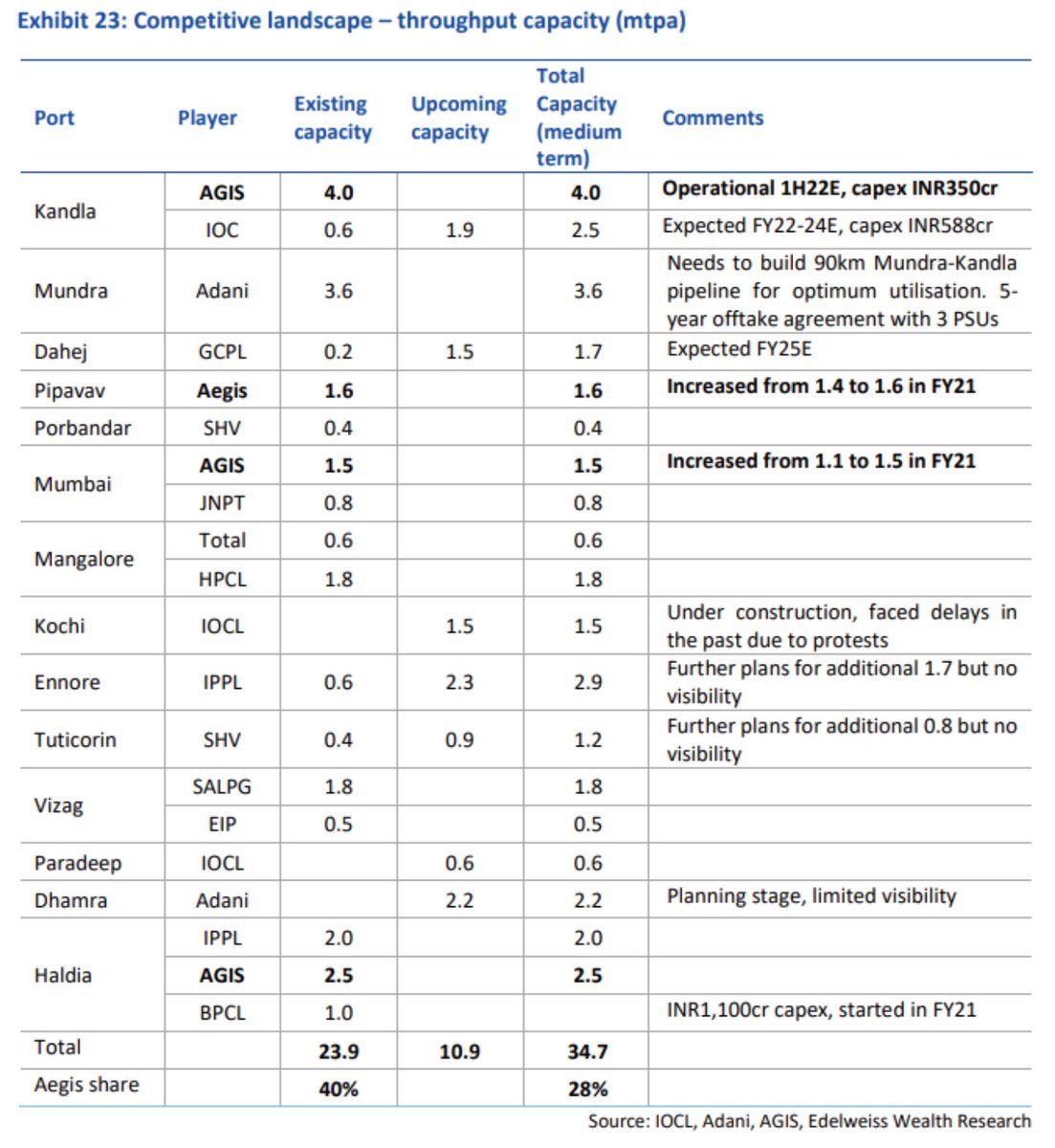

29/ Terminals are strategically located in key ports (the land is scarce here, think moat); additionally placed to benefit from the major pipeline infrastructure in India (most efficient way to transport)

Also, a huge reinvestment potential as we discussed in the megatrend part.

Also, a huge reinvestment potential as we discussed in the megatrend part.

30/ Liquid Cargo Business: Stable Cash Cow which will continue to grow at higher rates given more capacities & higher value addition in the later years.

+ Fortress balance sheet & epic cashflows to fund the incremental capex requirements.

+ Fortress balance sheet & epic cashflows to fund the incremental capex requirements.

31/ Opportunities:

As already discussed, the huge LPG import growth with the rising Indian economy: With their efficiency metrics & now a much better reputation (after JV with Royal Vopak); can continue to gain market share at a decent pace.

Order Wins+ Capex are already on 🔥

As already discussed, the huge LPG import growth with the rising Indian economy: With their efficiency metrics & now a much better reputation (after JV with Royal Vopak); can continue to gain market share at a decent pace.

Order Wins+ Capex are already on 🔥

32/ Additionally, just check out the technological capabilities of Royal Vopak.

The positive optionalities whether be it new gases, LNG (minimum investment size of a billion dollars), or renewable energy are limitless.

Imagine the scale Aegis can reach 🚀

The positive optionalities whether be it new gases, LNG (minimum investment size of a billion dollars), or renewable energy are limitless.

Imagine the scale Aegis can reach 🚀

33/ No business is without it's risks

The management spreading themselves too thin (already a bit visible in the struggling sourcing business) 👇

With the JV's ambitions, there is a huge mountain to climb by the top management to ensure sufficient capacity utilization.

The management spreading themselves too thin (already a bit visible in the struggling sourcing business) 👇

With the JV's ambitions, there is a huge mountain to climb by the top management to ensure sufficient capacity utilization.

34/ High gestation business whether be it LPG (5-7 years to reach throughput) or Liquid business (to go from bulk petrochemicals to high-value products takes 3-4 years)

Returns will be visible over years

Do you have the capacity to suffer or do you prefer to buy the breakout?

Returns will be visible over years

Do you have the capacity to suffer or do you prefer to buy the breakout?

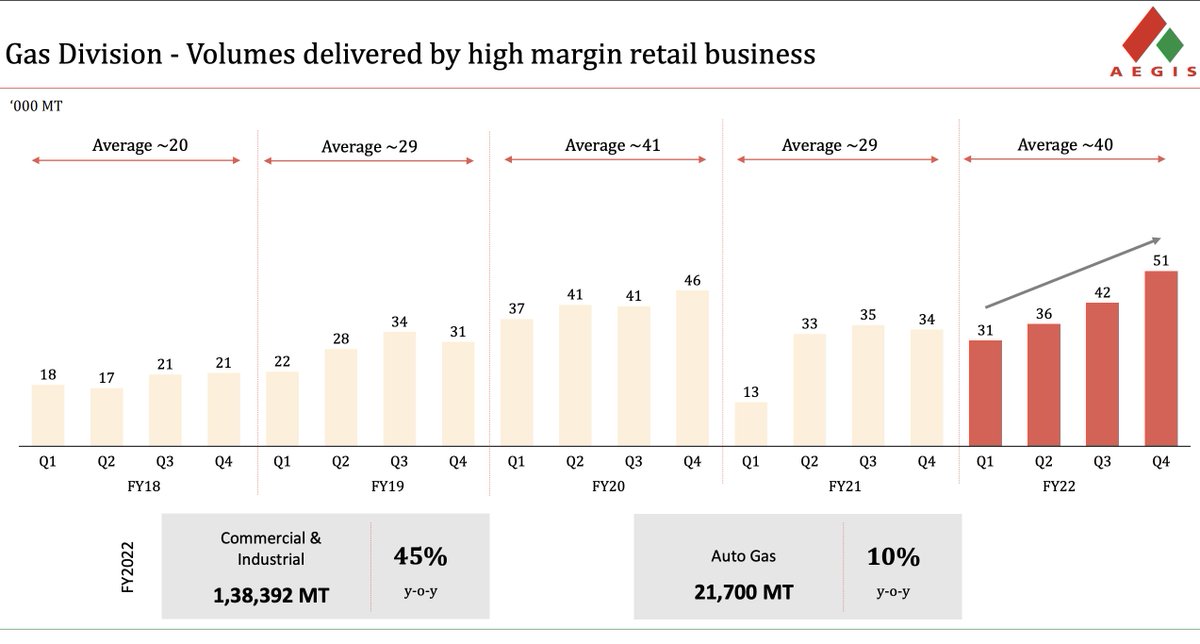

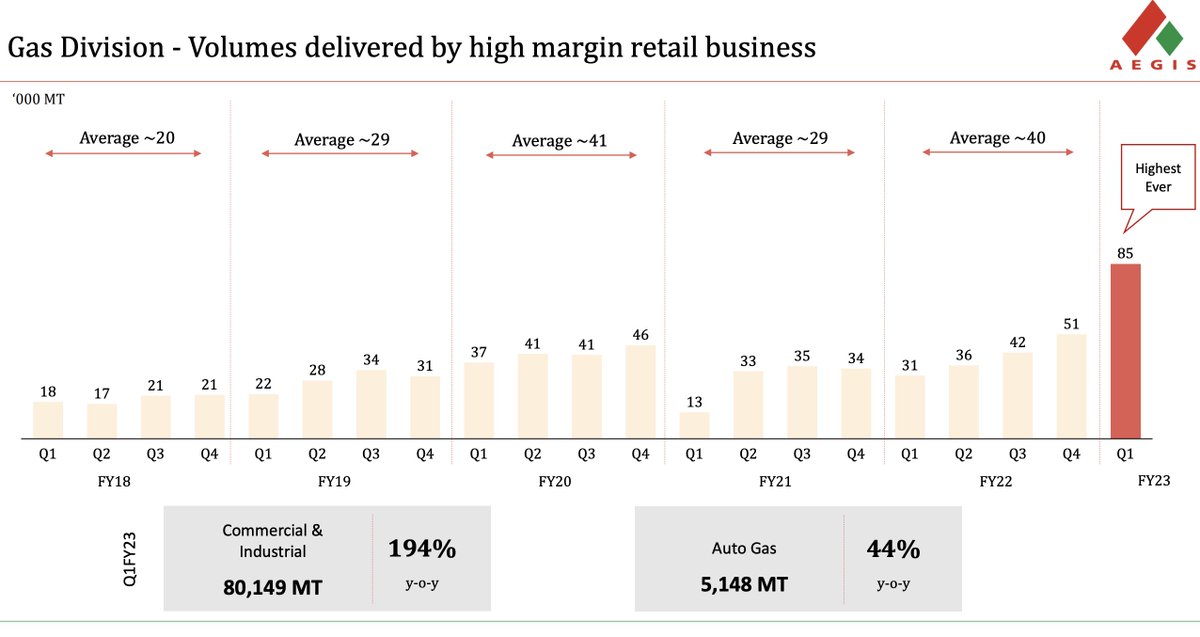

35/ Big dreams for the most lucrative retail autogas business: Execution has been a laggard here due to the weak OEM support & other demand related challenges

However, other retail engines continue to fire as Aegis has reached ATH volumes recently.

However, other retail engines continue to fire as Aegis has reached ATH volumes recently.

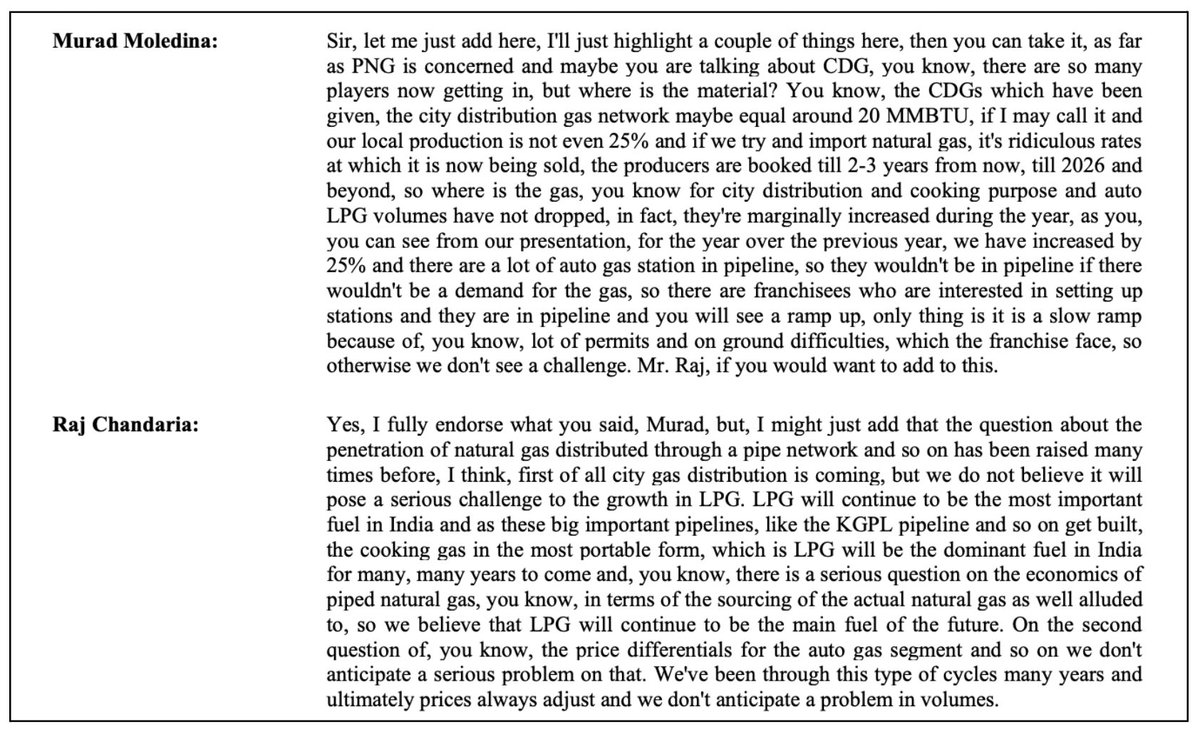

36/ One of the most talked about risk: PNG taking over LPG: why is it not a long term threat?

Not financially viable to set up the dense infrastructure required & it has been clarified multiple times in the concalls (the latest one 👇)

Not financially viable to set up the dense infrastructure required & it has been clarified multiple times in the concalls (the latest one 👇)

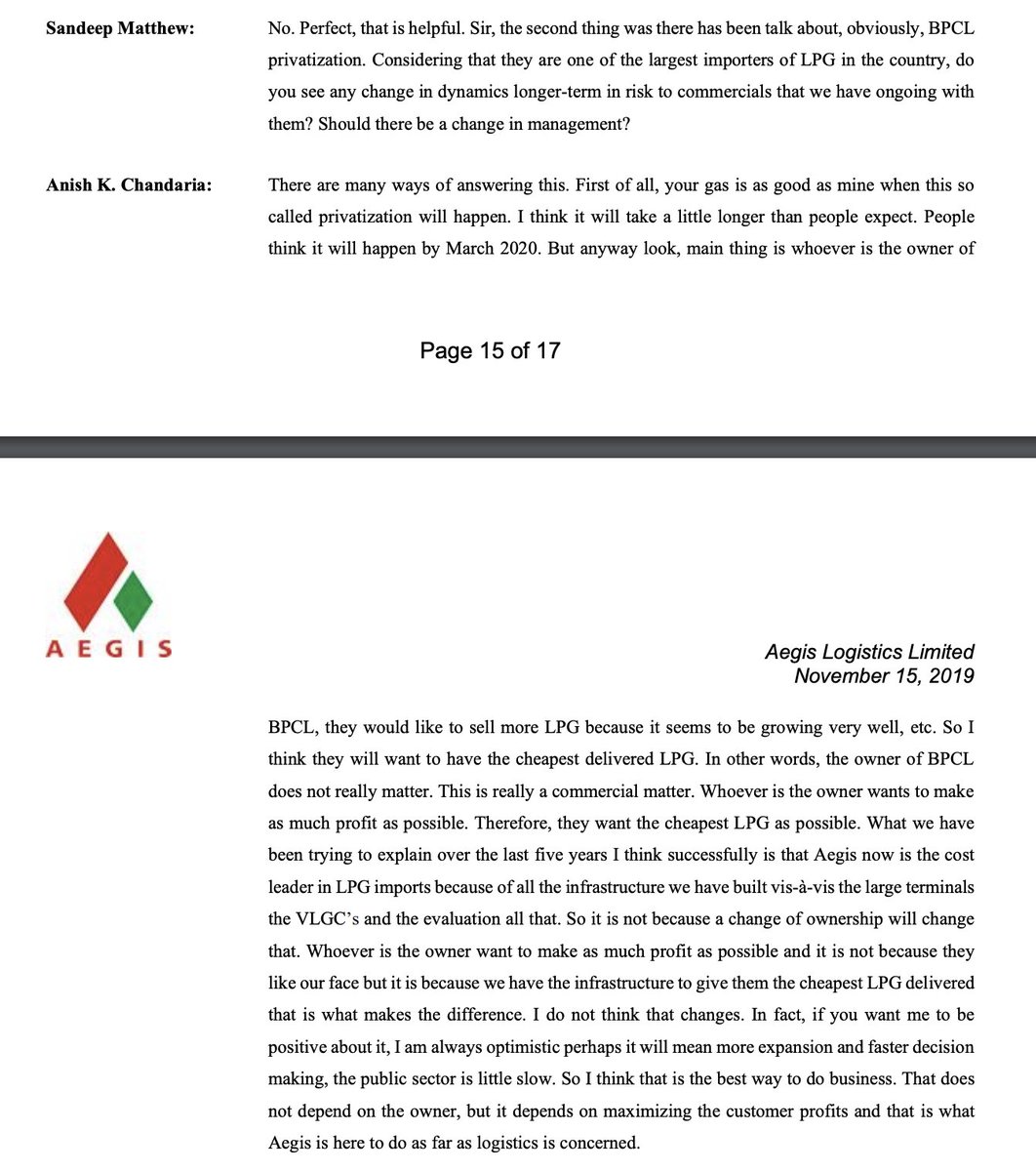

37/ BPCL privatisation: Here’s what the late MD had to say on why is it not an issue:

Aegis is the cost leader & even to set up one's own terminaling capacity takes 5 years. But, do they have the expertise to run it? Not that simple if you have read the thread till now.

Aegis is the cost leader & even to set up one's own terminaling capacity takes 5 years. But, do they have the expertise to run it? Not that simple if you have read the thread till now.

37/ Now, Let's discuss real threats:

Indian economic slowdown: short to medium-term impact.

As we have seen with COVID. The main issue with this for Aegis is the huge incremental capacity that they are coming up with, the Opex with no revenues is a risk. Also, Cyclones.

Indian economic slowdown: short to medium-term impact.

As we have seen with COVID. The main issue with this for Aegis is the huge incremental capacity that they are coming up with, the Opex with no revenues is a risk. Also, Cyclones.

38/ Changes in government policy with regards to subsidised pricing of LPG and its substitutes like CNG.

Major competitors (Adani) & customers (OMCs like HPCL, BPCL, IOCL) can scale up their terminals+ Liquids division &undercut Aegis: High Impact, low probability.

Major competitors (Adani) & customers (OMCs like HPCL, BPCL, IOCL) can scale up their terminals+ Liquids division &undercut Aegis: High Impact, low probability.

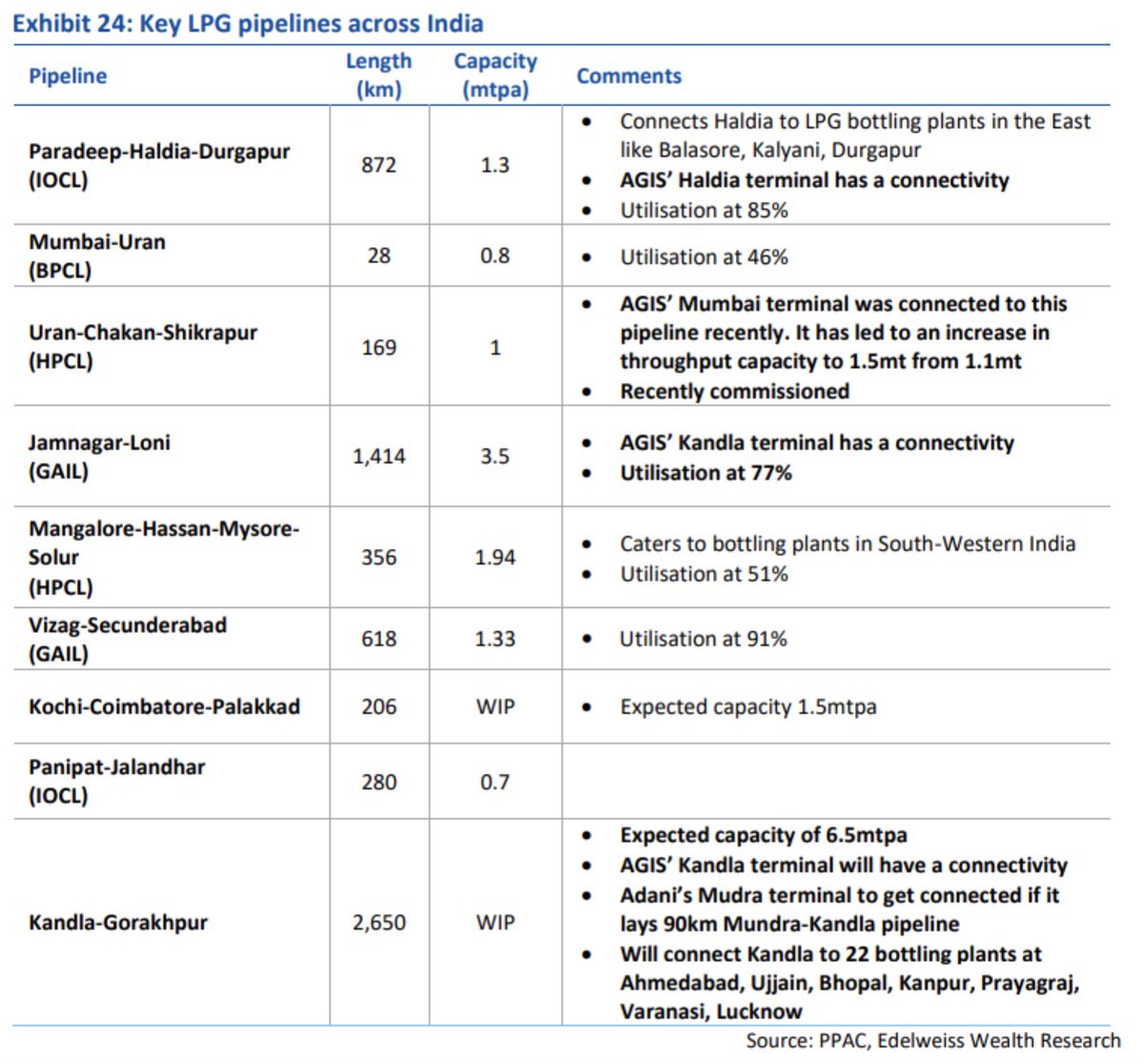

39/ Another risk is a delay in deploying pipelines by the government (plays out from time to time)

The Kandla-Gorakhpur pipeline will be a key driver of long-term growth. The ramp-up of the Kandla terminal (4mtpa capacity) to optimum capacity will be dependent on this pipeline.

The Kandla-Gorakhpur pipeline will be a key driver of long-term growth. The ramp-up of the Kandla terminal (4mtpa capacity) to optimum capacity will be dependent on this pipeline.

40/ Valuations & Conclusion

With 10-12x FY22 EBITDA (Pre-Vopak), a lot of optionalities are not built-in into the valuations & thus this company continues to pique my interest.

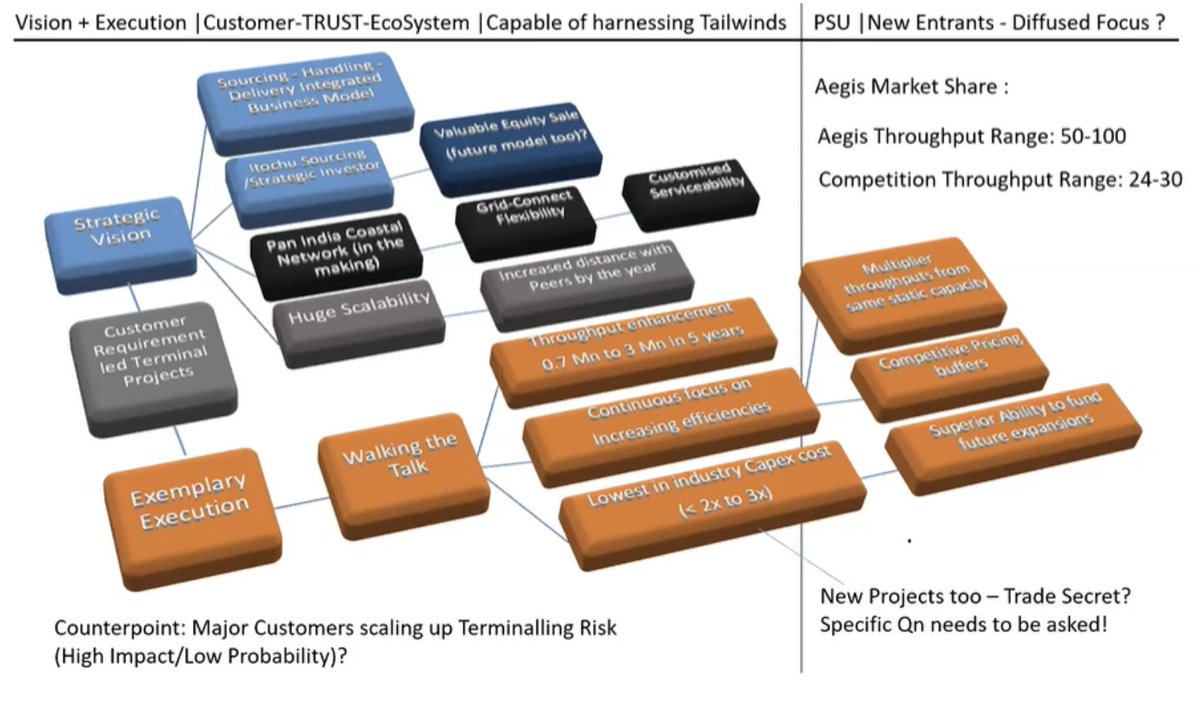

Lastly, A amazing slide on the company from a recent Valupickr presentation

With 10-12x FY22 EBITDA (Pre-Vopak), a lot of optionalities are not built-in into the valuations & thus this company continues to pique my interest.

Lastly, A amazing slide on the company from a recent Valupickr presentation

41/ The real Moat: The Oil & gas sector requires specialised infrastructure at key ports such as specialised berths, fire-fighting equipment, pipelines, transit storage and handling facilities and above all, safe and environmentally responsible handling practices.

42/ The terminalling, retail, and distribution industry in India has many participants, but only a select few possess the necessary technical and safety credentials, as well as the infrastructure to benefit from the long term prospects.

End.

End.

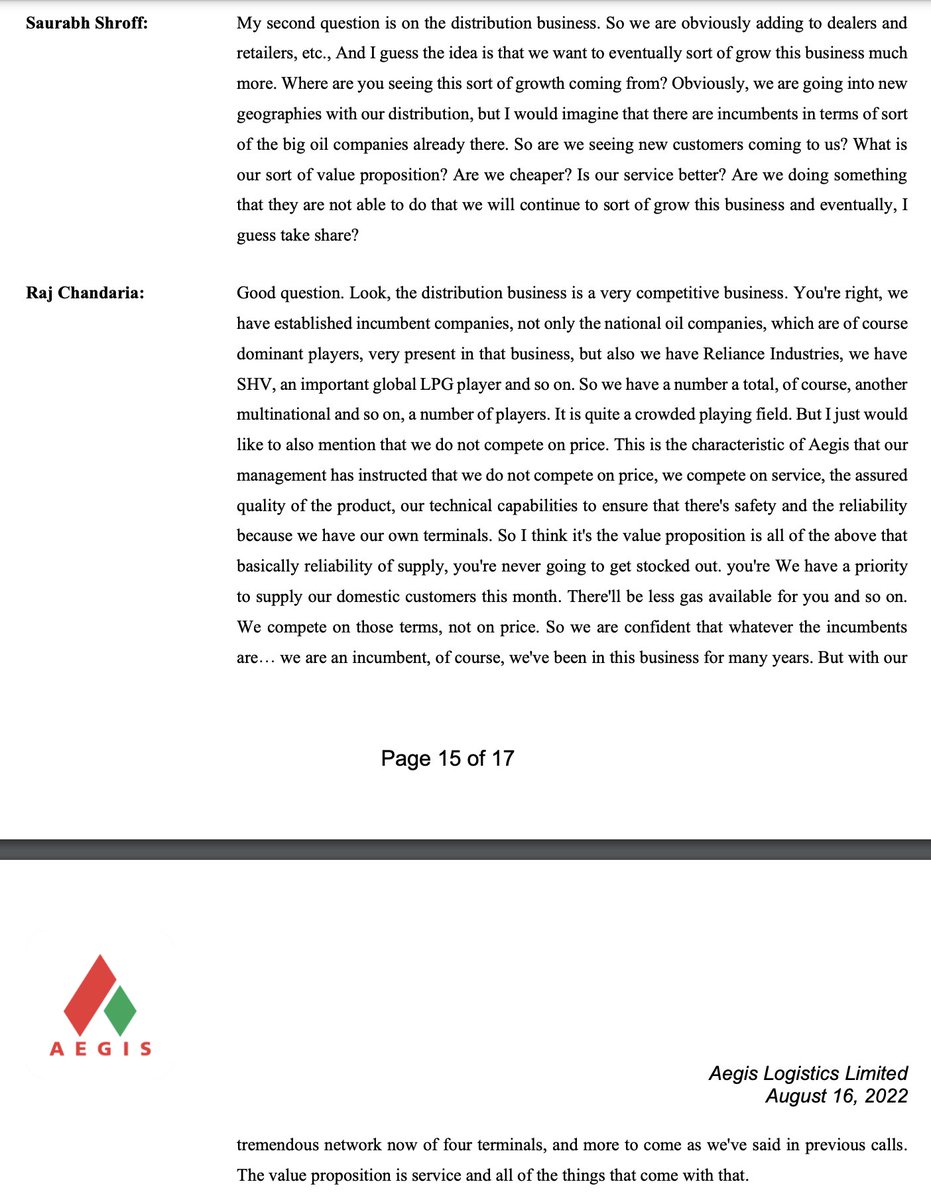

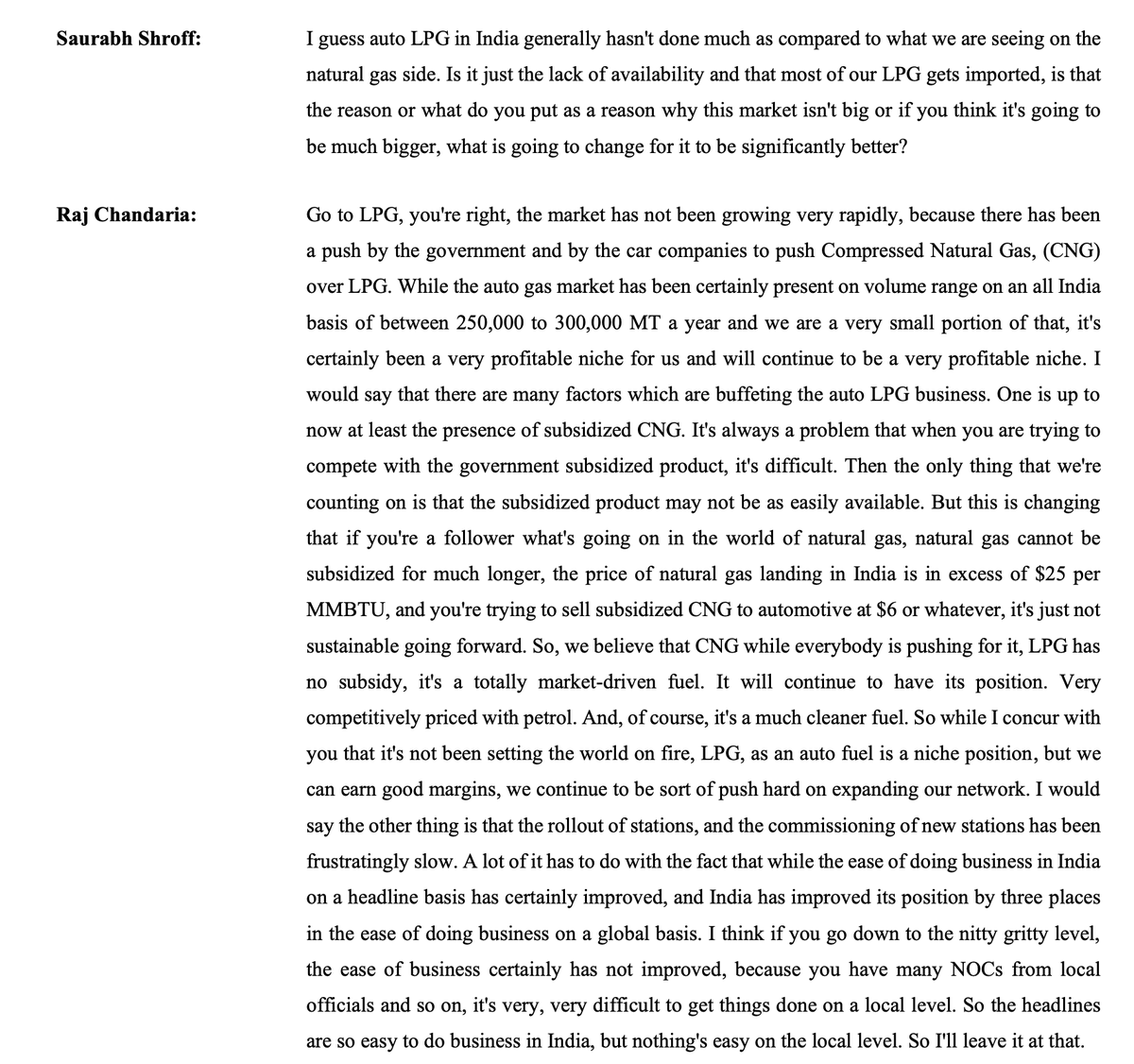

43/ Why Aegis is crushing it in gas retailing 🚀👇

Even with the current run rate, Aegis is ~1% of the Indian LPG retailing industry

Can it increase it to 5% of the industry by FY30? ⚔️

However, do not expect much from Auto LPG even though the management is trying its best.

Even with the current run rate, Aegis is ~1% of the Indian LPG retailing industry

Can it increase it to 5% of the industry by FY30? ⚔️

However, do not expect much from Auto LPG even though the management is trying its best.

Loading suggestions...