Fundamental Analysis - Sirca Paints 🎨

👣Origin -

Originally incorporated in New Delhi, an idea was first seeded as Sircolor Wood Coatings Private Limited when January 19, 2006, witnessed the epic beginning. The journey eventually unfolds in the name of Sirca Paints India Limited.

Originally incorporated in New Delhi, an idea was first seeded as Sircolor Wood Coatings Private Limited when January 19, 2006, witnessed the epic beginning. The journey eventually unfolds in the name of Sirca Paints India Limited.

👨🎓Management -

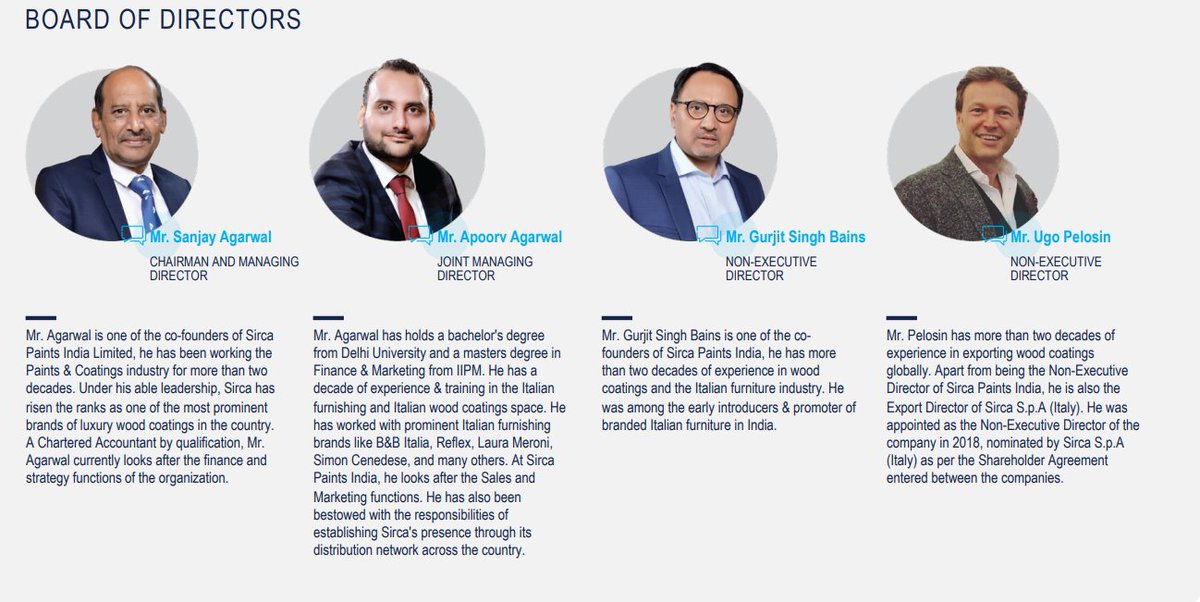

Mr. Sanjay Agarwal, Chairman & MD, co-founder of Sirca Paints, he has been working in the Paints & Coatings industry for more than 3 decades. Under his able leadership, Sirca has risen to the ranks as one of the prominent brands of luxury wood coatings.

Mr. Sanjay Agarwal, Chairman & MD, co-founder of Sirca Paints, he has been working in the Paints & Coatings industry for more than 3 decades. Under his able leadership, Sirca has risen to the ranks as one of the prominent brands of luxury wood coatings.

💼Business model -

They import PU products from Italy & Korea, repack it, and then sell them through their own dealer. Today, Sirca takes pride in being one of the leaders in northern India for wood coatings.

They import PU products from Italy & Korea, repack it, and then sell them through their own dealer. Today, Sirca takes pride in being one of the leaders in northern India for wood coatings.

💚Sustainable -

Sirca's products are research-based and are formulated keeping in mind how they should cater to the market’s varying needs.

🏡Home is one’s most aspirational assets & Sirca aims to successfully grace it with coatings that stand the test of time.

Sirca's products are research-based and are formulated keeping in mind how they should cater to the market’s varying needs.

🏡Home is one’s most aspirational assets & Sirca aims to successfully grace it with coatings that stand the test of time.

⚡️The vision of the company -

Sirca, is undergoing a phase of transformation. The objective is to broaden the portfolio of products and increase market dominance. They've been customer-centric & breaking new ground by introducing innovative and benchmark-setting products.

Sirca, is undergoing a phase of transformation. The objective is to broaden the portfolio of products and increase market dominance. They've been customer-centric & breaking new ground by introducing innovative and benchmark-setting products.

🚀Brands Portfolio -

The Company is engaged in the manufacturing & sales of wood coatings and other decorative paints, under its owned or exclusively licensed brands like Sirca, Unico, San Marco & DuranteVivan, and is also geared to begin exporting its products.

The Company is engaged in the manufacturing & sales of wood coatings and other decorative paints, under its owned or exclusively licensed brands like Sirca, Unico, San Marco & DuranteVivan, and is also geared to begin exporting its products.

🇮🇳Domestic expansion -

Sirca, a market leader in premium wood coatings in North India, is expanding its domestic footprint. They currently operate in 2 facilities, one for mass-market wood coatings products in Sonipat, Haryana, and a wall paints and putty in the NCR region.

Sirca, a market leader in premium wood coatings in North India, is expanding its domestic footprint. They currently operate in 2 facilities, one for mass-market wood coatings products in Sonipat, Haryana, and a wall paints and putty in the NCR region.

🤩Primary Goal - Make Sirca a household name in India.

Sirca is also gearing up to strengthen its presence in South, West, and East India as well as in other South Asian countries, with the goal of tapping the evolving markets.

Sirca is also gearing up to strengthen its presence in South, West, and East India as well as in other South Asian countries, with the goal of tapping the evolving markets.

🖌️Paint Industry Overview -

India’s paint industry is estimated to be a 55,000 crores market, according to industry estimates, and is one of the world’s fastest-growing major paint markets, with double-digit growth for the past two decades.

India’s paint industry is estimated to be a 55,000 crores market, according to industry estimates, and is one of the world’s fastest-growing major paint markets, with double-digit growth for the past two decades.

📊Sector dynamics -

The organized sector dominates the Indian paints and coatings market, accounting for 75 % market share, while the unorganized sector accounts for the remaining 25%.

The organized sector dominates the Indian paints and coatings market, accounting for 75 % market share, while the unorganized sector accounts for the remaining 25%.

♻️ESG TREND -

Wood coatings category is facing a shift in consumer preferences from toxic and environmentally harmful products to eco-friendly and non-toxic products.

There is a shift from harmful products like Nitrocellulose (NC) and Melamine to high-quality Polyurethane (PU)

Wood coatings category is facing a shift in consumer preferences from toxic and environmentally harmful products to eco-friendly and non-toxic products.

There is a shift from harmful products like Nitrocellulose (NC) and Melamine to high-quality Polyurethane (PU)

🔎Reason for trend shift?

a. Increasing health-consciousness

b. Growing awareness about environment-friendly products

c. Greater artistic and aesthetic value

d. lower emission of odor

e. Increased durability and resistance make these products preferable

a. Increasing health-consciousness

b. Growing awareness about environment-friendly products

c. Greater artistic and aesthetic value

d. lower emission of odor

e. Increased durability and resistance make these products preferable

🎨Paints Business has 2 segments :

1. Decorative paints & coatings

2. Industrial paints & coatings.

The decorative segment accounts for 74% of market value and 85% of the market volumes, and the balance comprises industrial paints & coatings.

1. Decorative paints & coatings

2. Industrial paints & coatings.

The decorative segment accounts for 74% of market value and 85% of the market volumes, and the balance comprises industrial paints & coatings.

👉Product line - Decorative segment

Interior and exterior paints, design range, premier, enamel, wood finishing, and waterproofing.

👉Product line - Industrial paints

Automotive paints, performance coating liquids, powder coating, marine coating, and refinishes.

Interior and exterior paints, design range, premier, enamel, wood finishing, and waterproofing.

👉Product line - Industrial paints

Automotive paints, performance coating liquids, powder coating, marine coating, and refinishes.

🌟Focus -

Sirca Paints India Limited is focused mainly on PU products, and wood coating products and more than 95% of turnover comes from wood products.

The majority of the growth comes from the trading business where they're importing products from Italy i.e. luxury PU side.

Sirca Paints India Limited is focused mainly on PU products, and wood coating products and more than 95% of turnover comes from wood products.

The majority of the growth comes from the trading business where they're importing products from Italy i.e. luxury PU side.

🪵Wood Coatings Segment Overview -

Wood coatings are used for adhesion, anti-corrosion, durability, appearance enhancing & aesthetic features on wooden furniture.

Last decade, India shaped up to be one of the largest markets for wood coatings in the Asia -Pacific region.

Wood coatings are used for adhesion, anti-corrosion, durability, appearance enhancing & aesthetic features on wooden furniture.

Last decade, India shaped up to be one of the largest markets for wood coatings in the Asia -Pacific region.

📈Product Portfolio Performance -

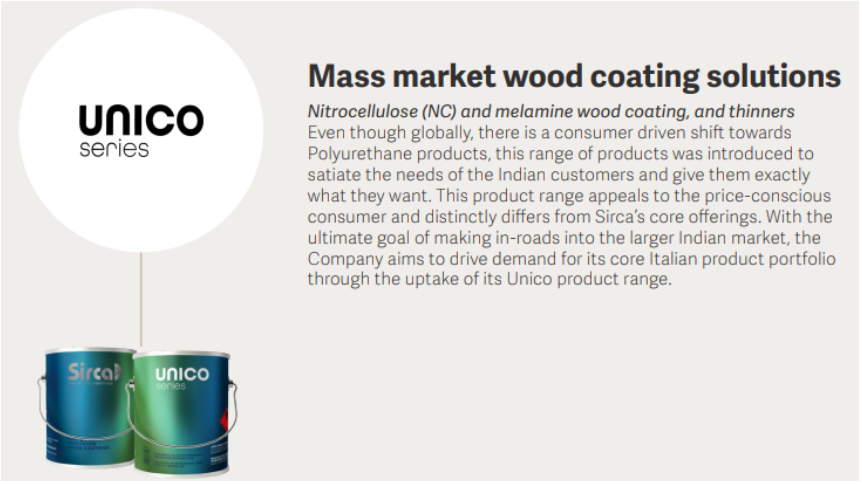

I. UNICO -

(i)They've fared well on the product portfolio front during the last quarter. With increased production and distribution efforts, Unico is expected to increase its revenue contribution in the coming quarters.

I. UNICO -

(i)They've fared well on the product portfolio front during the last quarter. With increased production and distribution efforts, Unico is expected to increase its revenue contribution in the coming quarters.

(ii) Italian PU remains the core product category for the Company.

(iii) Adding Resins Manufacturing at Sonipat Facility In efforts to establish control & achieve consistency in quality, they've decided to set up a manufacturing line for resins at its Sonipat facility.

(iii) Adding Resins Manufacturing at Sonipat Facility In efforts to establish control & achieve consistency in quality, they've decided to set up a manufacturing line for resins at its Sonipat facility.

(iv) This project has already commenced, and they will be able to commercialize this project in a couple of quarters. In addition, it will contribute to better margins and help minimize supply chain disruptions.

(v) This is the single biggest sector affecting the quality of the end product. These resins will be used to manufacture our Unico range of products, all the product kitty from NC melamine and the mass market of Indian PU.

(vi) The reason for manufacturing the resins here is mainly to come over the challenges of the supply chain which they have experienced for the last 3-4 months. Also, it brings down the cost significantly and increases the quality I mean by almost 20%-30%.

(vii) Post the in-house manufacturing of resins, approximately like we will be reducing COGS by Rs. 4 to 5 a liter and with the average pricing I think it will in the percentage be about 4% to 5%.

(viii) They're expecting revenue to grow from Unico range i.e. Indian PU (made from technology of Sirca Italy) wherein they expect within 2 years they'll reach to the maximum utilization of our current facility which will give revenue of not less than Rs. 250 to 260 crores.

(ix) Non-Italian PU sales from the Unico range and the wall paint are appro 14% of our total revenue.

The non-Italian product contribution this year was approximately about 20% & going forward they're focusing on mfg of the PU range rather than the NC and Melamine.

The non-Italian product contribution this year was approximately about 20% & going forward they're focusing on mfg of the PU range rather than the NC and Melamine.

(x) They're expecting that this year the contribution of the economical range of products especially the Unico and wall paint would increase to about 30%-35% of the total revenue.

II. SAN MARCO -

(i) They're also expecting our revenue to grow at the wall paint side, at the texture business from San Marco.

(i) They're also expecting our revenue to grow at the wall paint side, at the texture business from San Marco.

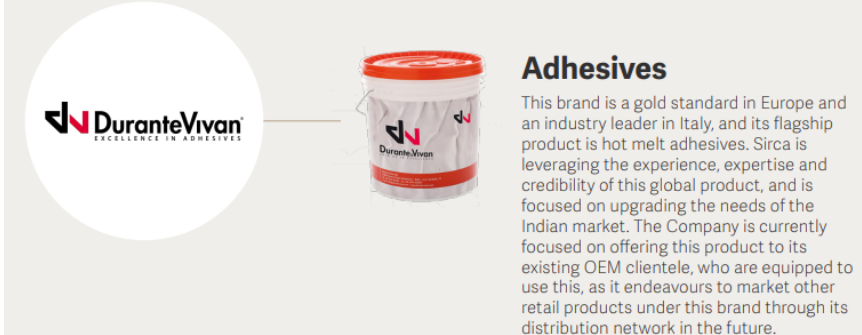

III. DURANTE VIVAN

(i) The Company also plans to launch the Durante-Vivan adhesives portfolio in some upcoming trade shows and exhibitions. It is initially targeting the OEM customer segment with its flagship hot-melt glue product offerings.

(i) The Company also plans to launch the Durante-Vivan adhesives portfolio in some upcoming trade shows and exhibitions. It is initially targeting the OEM customer segment with its flagship hot-melt glue product offerings.

(ii) The adhesive which is a new line which is, which will be launched in India in the next week and the product will be out by the end of July.

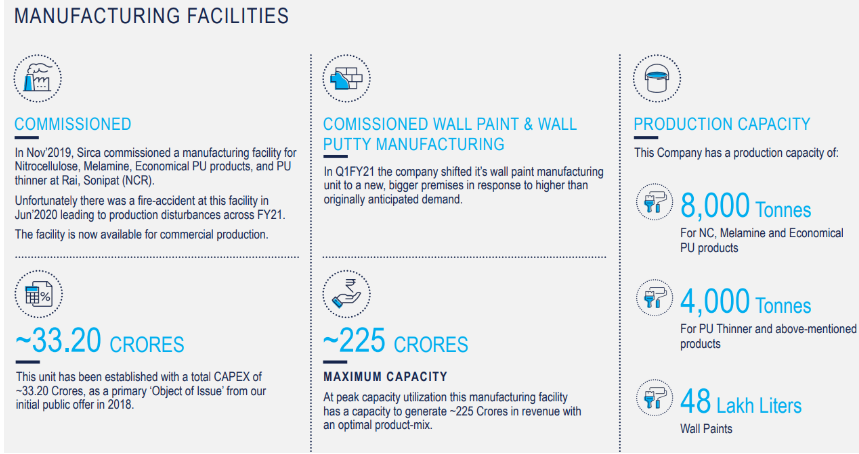

🏗️Manufacturing Capital

a. State-of-the-art wood coatings manufacturing plant at Sonipat, Haryana

b. Wall paints and putty manufacturing facility in NCR

c. Resin manufacturing line being added at Sonipat facility

d. 1 upcoming plant announced in South India

a. State-of-the-art wood coatings manufacturing plant at Sonipat, Haryana

b. Wall paints and putty manufacturing facility in NCR

c. Resin manufacturing line being added at Sonipat facility

d. 1 upcoming plant announced in South India

🏭Superior Manufacturing Capabilities -

- 8,000 Tonnes for NC, Melamine, and Economical PU products

- 4,000 Tonnes for PU Thinner and the above-mentioned products

- 48 Lakh Litres for Wall Paints

- 8,000 Tonnes for NC, Melamine, and Economical PU products

- 4,000 Tonnes for PU Thinner and the above-mentioned products

- 48 Lakh Litres for Wall Paints

💪Strategic Priorities -

• Strengthening distribution network

• Nurturing OEM relationships

• Augmenting brand equity

• Exploring export market

• Expanding product portfolio

• Building strong organizational capabilities

• Strategically located manufacturing plants

• Strengthening distribution network

• Nurturing OEM relationships

• Augmenting brand equity

• Exploring export market

• Expanding product portfolio

• Building strong organizational capabilities

• Strategically located manufacturing plants

🎁Niche Product Portfolio -

• Premium Italian wood, metal, and glass coatings

• Wall paints and putty range

• Mass market wood coatings: nitrocellulose (NC), melamine, and thinners

• Exclusive decorative and solid color finishes

• Adhesives

• Premium Italian wood, metal, and glass coatings

• Wall paints and putty range

• Mass market wood coatings: nitrocellulose (NC), melamine, and thinners

• Exclusive decorative and solid color finishes

• Adhesives

Competitive Advantage -

✍️Traditional Paint Companies such as Asian Paints, Berger Paints or even new entrants like JSW or Grasim, as of now is not a big question of competition for them, reason being that their target product is the decorative which is the wall paint.

✍️Traditional Paint Companies such as Asian Paints, Berger Paints or even new entrants like JSW or Grasim, as of now is not a big question of competition for them, reason being that their target product is the decorative which is the wall paint.

✍️Sirca Paints India Limited is focused mainly on PU products, the wood coating products, and more than 95% of our turnover comes from wood products. As of now, other companies have not announced their key entry in the wood care products or polyurethane coating.

✍️This is an opportunity because the market is going to open up in the decorative segment and going forward it is not a serious area of concern for us or a threat, the reason being that there is no recent announcement yet of their entry in the wood coating segment.

✍️A niche product portfolio and less competition gives them a great advantage in terms of pricing power. Although the barrier to entry in this segment is not that high for existing companies in the industry, but as of now they hold the dominant market share.

Mfg Facilities & Capex Plans -

a. On the infrastructure front, they have some investments anticipated and others in the works. To begin with, they are now installing a line at our Sonipat facility to produce resins for the Unico range.

a. On the infrastructure front, they have some investments anticipated and others in the works. To begin with, they are now installing a line at our Sonipat facility to produce resins for the Unico range.

b. They have done a small CAPEX to develop resin plant in the Nathupur facility which will allow them to manufacture all our key resins in-house to ensure better quality & prices and avoid disruptions in supply chain.

This is set to be commercialized in the first half of FY23.

This is set to be commercialized in the first half of FY23.

c. They do plan to open a new manufacturing facility for mass-market wood coatings to better service the South Indian market. They are going to do a next small CAPEX of about Rs. 5 to 6 crores for our South India operations which should happen by end of this year.

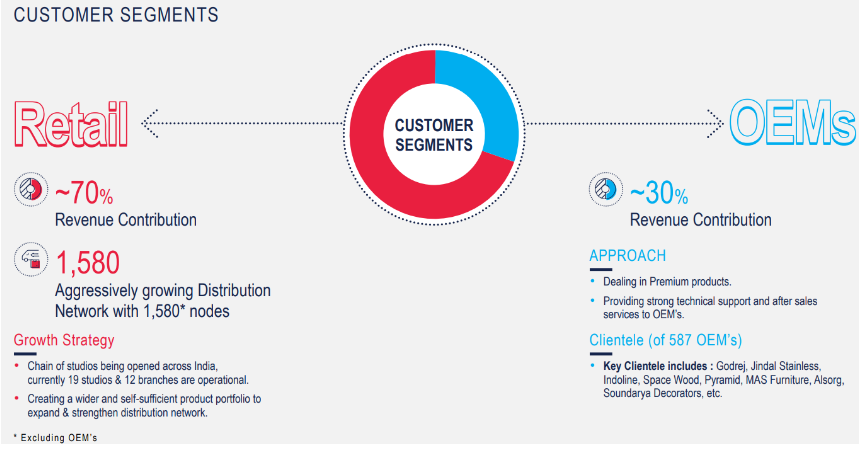

CUSTOMER SEGMENTS

1. RETAILS

2. OEM's

1. RETAILS

2. OEM's

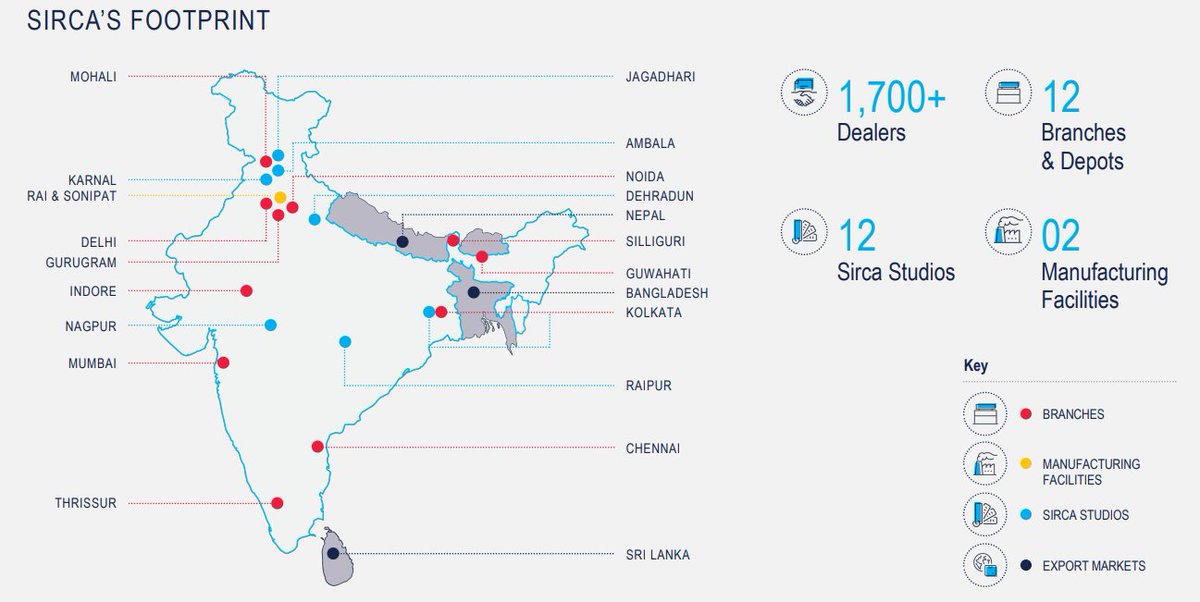

🫂Retail Segment -

🔹The Company caters to retail customers through its strong & growing distribution network of more than 1,580 dealers, further supported by a branch & depot network of 13 across its key markets.

🔹The retail segment contributes 70% of the revenue stream.

🔹The Company caters to retail customers through its strong & growing distribution network of more than 1,580 dealers, further supported by a branch & depot network of 13 across its key markets.

🔹The retail segment contributes 70% of the revenue stream.

🔹To better service its newer markets, the Company plans to establish an alternate manufacturing facility in South India to serve these markets better.

🔹A total of 1,150+ shop boards have been installed so far.

🔹A total of 1,150+ shop boards have been installed so far.

🔹The Company is also establishing a chain of exclusive Sirca Studios that showcase the application and merits of Sirca’s entire product portfolio. At present, a total of 19 such studios are operational across India.

👥OEM Segment -

🔸Since the Company’s beginning, Sirca has collaborated with furniture and fixture manufacturers. Sirca’s products are a result of several collaborations and a thorough understanding of OEM needs.

🔸Since the Company’s beginning, Sirca has collaborated with furniture and fixture manufacturers. Sirca’s products are a result of several collaborations and a thorough understanding of OEM needs.

🔸OEMs have also been early adopters of premium wood coating solutions. Sirca is the primary and, in many cases, the only choice for furniture manufacturers when it comes to wood coatings. The company has ensured utmost satisfaction by providing technical and after-sales support.

🔸The OEM segment, where the Company works with a well-diversified clientele of around 587 clients, accounts for nearly 30% of the total revenue.

🔸Some of them are the country’s largest and most recognized furniture manufacturers, including Godrej & Boyce, Jindal Stainless, Indoline, Space Wood, Pyramid, MAS Furniture, Alsorg, and Soundarya Decorators, among others.

🔸The growing prominence of ready-made, modular furniture over on-site furniture will boost this segment’s performance in the long run. Indian consumers, particularly millennials, are increasingly choosing ready-made furniture as a trend.

🔸This trend is fueled by factors such as convenience, faster turnaround times, and a growing array of options. Sirca has become a vital vendor to OEMs because of its ongoing innovation, new product introductions and outstanding technical assistance.

BROWNIE POINTS !!! 🥳

✅The company is recognized for its hallmark of superior quality wood finishes.

✅With its newly commissioned manufacturing facility, SPIL is progressing on its journey to become a leading brand in the Indian wood coatings & paints market.

✅The company is recognized for its hallmark of superior quality wood finishes.

✅With its newly commissioned manufacturing facility, SPIL is progressing on its journey to become a leading brand in the Indian wood coatings & paints market.

✅Sirca aims to keep up the momentum of its performance in the coming years, and leverage its expansion plans as the bedrock for creating value for its shareholders.

✅Among the top 3 premium category wood coatings brand in India.

✅Among the top 3 premium category wood coatings brand in India.

✅The increasing value of aesthetics and expenditure towards the furnishing segment is supportive. In the long

run, an increase in disposable income and a shift towards higher-end wood coating products in the value chain will be leading growth driver for wood coatings market.

run, an increase in disposable income and a shift towards higher-end wood coating products in the value chain will be leading growth driver for wood coatings market.

✅The Company continues to develop a sustainable platform for expanding the geographical footprint, brand recall, and sales of Sirca and other newly added brands such as Unico, San Marco, and DuranteVivan.

✅This is driven through the expansion of its sales channels coupled with a far more extensive product portfolio, expanding distribution network, strengthened physical infrastructure, and increased team strength.

🚩Risk Check -

❎Material availability and inflation: Disruption across the value chain arising out of unforeseen events leading to unavailability of material and an increase in material prices.

❎Material availability and inflation: Disruption across the value chain arising out of unforeseen events leading to unavailability of material and an increase in material prices.

❎ Operational Risk While pursuing innovative product offerings and radical business models, there are certain risks associated with product delivery, Service Level Agreement adherence, quality, and environmental impact amongst others.

❎Commodity Risk: There are several raw materials that are directly driven by crude oil. Other uncertainties like supply chain disruptions due to any political/ geographical issues in any country, market risk related to e-commerce, and intensifying competition risk.

❎Strategic Risk: These risks revolve around Competition (existing and New), brand, growth and profitability, technology, and service strategy during normal and force majeure situations.

🧪Fundamental Outlook -

- The expected sustainable EBITDA going forward considering the external factors is about 20% to 21%.

- There are price hikes which are scheduled for the month of June and July between 4% to 6% approximately.

- The expected sustainable EBITDA going forward considering the external factors is about 20% to 21%.

- There are price hikes which are scheduled for the month of June and July between 4% to 6% approximately.

- Going forward they're expecting 50%-60% of revenue growth every year. This would come from our existing range of products & expansion of the range of the products that we're doing and the majority of share of the increase in revenue will be contributed by Indian & Italian PU.

- Company anticipates improved growth prospects moving forward, particularly with regard to the increasing contribution of its emerging product categories as they grow and mature.

- They expect by end of the year, they'll be adding not less than 2,000 - 3,000 new dealers.

- They expect by end of the year, they'll be adding not less than 2,000 - 3,000 new dealers.

- Sirca is in an excellent position to create a market for its products and capitalize on the enormous opportunity unfolding in the Indian paints and coatings market as well as other niche home improvement categories.

- Indian PU (Unico PU) we expect that by maximum 1.5 to 2 years, the plant will be operating at its max capacity which will contribute to almost about 250 crores of additional revenue.

- To be conservative they're expecting 50-60% of our top-line growth in the next 3-4 years.

- To be conservative they're expecting 50-60% of our top-line growth in the next 3-4 years.

📊Metrics check -

Market Cap : 1392Cr.

ROCE : 17.5%

ROE : 13.2%

OPM : 19.5%

Debt/Equity : 0 (Debt Free)

Sales Growth 5 Years : 18.9%

Profit Growth 5 Years : 15.4%

Promoter Holding : 67.6%

Market Cap : 1392Cr.

ROCE : 17.5%

ROE : 13.2%

OPM : 19.5%

Debt/Equity : 0 (Debt Free)

Sales Growth 5 Years : 18.9%

Profit Growth 5 Years : 15.4%

Promoter Holding : 67.6%

💰Current Valuations -

P/E (Stock): 49.6

P/E (Industry) : 39.6

Market Cap/Sales : 7.11

EV/EBITDA : 30.7

P/E (Stock): 49.6

P/E (Industry) : 39.6

Market Cap/Sales : 7.11

EV/EBITDA : 30.7

Disclaimer -

This research is shared for educational purposes only. Do thorough research before investing your hard earned money.

Info has been taken from various investor forums and company website.

This research is shared for educational purposes only. Do thorough research before investing your hard earned money.

Info has been taken from various investor forums and company website.

Loading suggestions...